8-11

Fixed Manufacturing Costs and Variances

a. Fixed Manufacturing Overhead Control

20,550

Salaries Payable, Acc. Depreciation, various other accounts

20,550

To record actual fixed manufacturing overhead costs incurred.

b. Work–in–Process Control

20,736

Fixed Manufacturing Overhead Allocated

20,736

To record fixed manufacturing overhead allocated.

c. Fixed Manufacturing Overhead Allocated

20,736

Fixed Manufacturing Overhead Spending Variance

1,350

Fixed Manufacturing Overhead Production-Volume Variance

1,536

Fixed Manufacturing Overhead Control

20,550

To isolate variances for the accounting period.

d. Fixed Manufacturing Overhead Production-Volume Variance

1,536

Fixed Manufacturing Overhead Spending Variance

1,350

Cost of Goods Sold

186

To write off fixed manufacturing overhead variances to cost of goods sold.

3. Planning and control of variable manufacturing overhead costs has both a long-run and a

short-run focus. It involves Solutions planning to undertake only value-added overhead activities

Variable

Fixed

1. Spending variance

2. Efficiency variance

3. Production-volume variance

4. Flexible-budget variance

5. Underallocated (overallocated) MOH

$200 U

2,200 F

NEVER

2,000 F

2,000 F

$4,600 U

NEVER

1,200 F

4,600 U

3,400 U

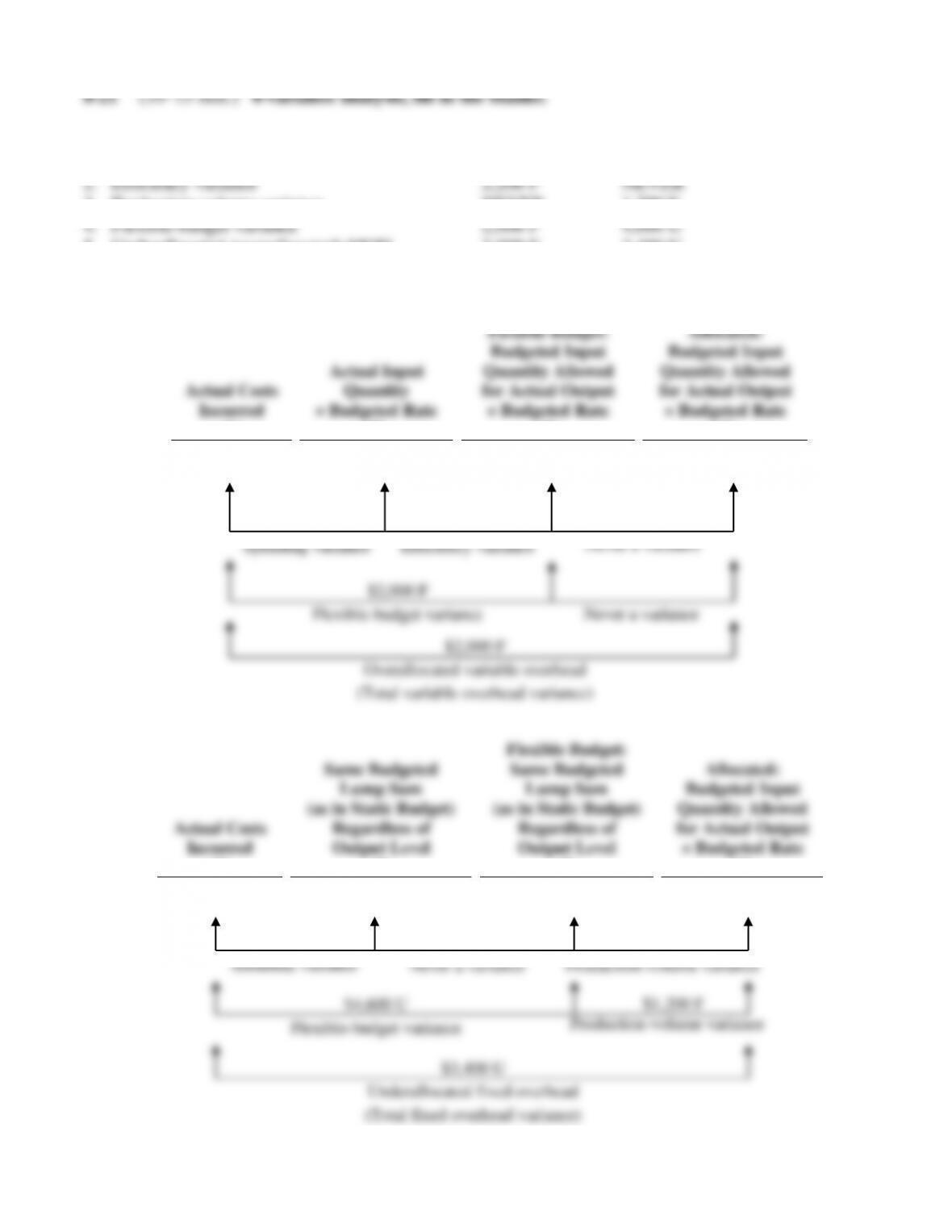

These relationships could be presented in the same way as in Exhibit 8-4.

Actual Costs

Incurred

(1)

Actual Input

Quantity

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(4)

Variable

MOH

$31,000

$30,800

$33,000

$33,000

MOH

$13,400

$200 U

Spending variance

$2,200 F

Efficiency variance

Never a variance

8-13

An overview of the 4 overhead variances is:

4-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production–

Volume

Variance

Variable

Overhead

$200 U

$2,200 F

Never a variance

Fixed

Overhead

$4,600 U

Never a variance

$1,200 F

8-22 (20–30 min.) Straightforward 4-variance overhead analysis.

1. The budget for fixed manufacturing overhead is 4,000 units × 6 machine-hours × $15

machine-hours/unit = $360,000.

An overview of the 4-variance analysis is:

4-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production–

Volume Variance

Variable

Manufacturing

Overhead

$17,800 U

$16,000 U

Never a Variance

Fixed

Manufacturing

Overhead

$13,000 U

Never a Variance

$36,000 F

Solution Exhibit 8-22 has details of these variances.

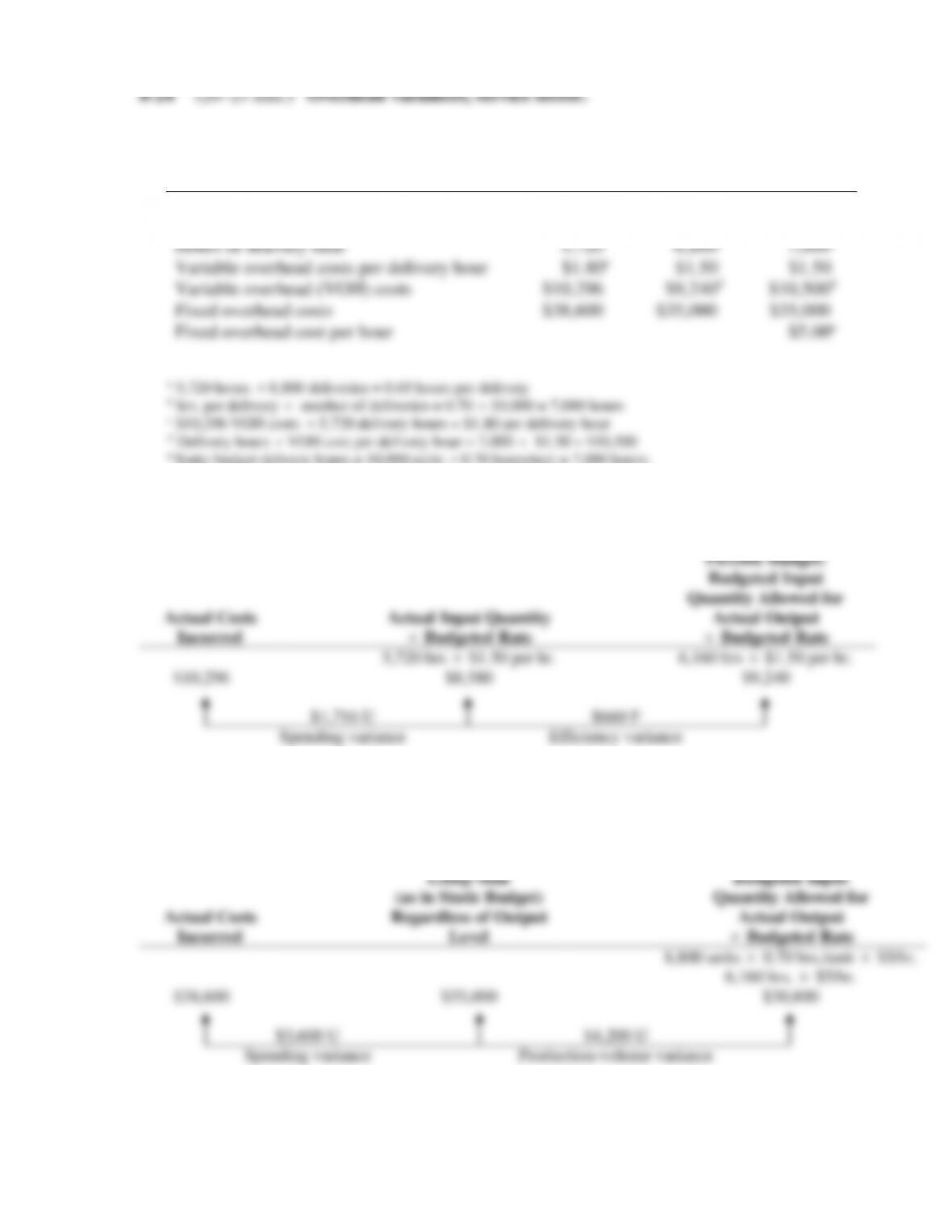

A detailed comparison of actual and flexible budgeted amounts is:

Actual

Flexible Budget

Output units (auto parts)

4,400

4,400

Allocation base (machine-hours)

28,400

26,400a

Allocation base per output unit

6.45b

6.00

Variable MOH

$245,000

$211,200c

Variable MOH per hour

$8.63d

$8.00

Fixed MOH

$373,000

$360,000e

Fixed MOH per hour

$13.13f

–

a4,400 units × 6.00 machine-hours/unit = 26,400 machine-hours

b28,400 ÷ 4,400 = 6.45 machine-hours per unit

c 4,400 units × 6.00 machine-hours per unit × $8.00 per machine-hour = $211,200

d $245,000 ÷ 28,400 = $8.63

e 4,000 units × 6.00 machine-hours per unit × $15 per machine-hour = $360,000

f $373,000 ÷ 28,400 = $13.13

8-14

2. Variable Manufacturing Overhead Control 245,000

Accounts Payable Control and other accounts 245,000

Work-in-Process Control 211,200

Variable Manufacturing Overhead Allocated 211,200

3. Individual fixed manufacturing overhead items are not usually affected very much by

day-to–day control. Instead, they are controlled periodically through planning decisions and

4. The fixed overhead spending variance is caused by the actual realization of fixed costs

differing from the budgeted amounts. Some fixed costs are known because they are

contractually specified, such as rent or insurance, although if the rental or insurance contract

expires during the year, the fixed amount can change. Other fixed costs are estimated, such as

SOLUTION EXHIBIT 8-22

Actual Costs

Incurred

(1)

Actual Input

Quantity

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(4)

Variable

MOH

$245,000

(28,400 × $8)

$227,200

(4,400 × 6 × $8)

$211,200

(4,400 × 6 × $8)

$211,200

$17,800 U

Spending variance

$16,000 U

Efficiency variance

Never a variance

1. Solution Exhibit 8-23 shows the computations. Summary details are:

Actual

Flexible Budget

Output units

65,500

65,500

Allocation base (machine-hours)

76,400

78,600a

Allocation base per output unit

1.17b

1.2

Variable MOH

$618,840

$628,800c

Variable MOH per hour

$8.92d

$8.00

Fixed MOH

$145,790

$144,000

Fixed MOH per hour

$1.91e

–

a 65,500 × 1.2 = 78,600 d $618,840 ÷ 76,400 = $8.10

b 76,400 ÷ 65,500 = 1.17 e $145,790 ÷ 76,400 = $1.91

c 65,500 × 1.2 × $8 = $628,800

8-17

2. Variable Manufacturing Overhead Control 618,840

Accounts Payable Control and other accounts 618,840

Work-in–Process Control 628,800

Variable Manufacturing Overhead Allocated 628,800

3. The control of variable manufacturing overhead requires the identification of the cost

drivers for such items as energy, supplies, and repairs. Control often entails monitoring

4. The variable overhead spending variance is unfavorable. This means the actual rate

applied to the manufacturing costs is higher than the budgeted rate. Since variable overhead

consists of several different costs, this could be for a variety of reasons, such as the utility rates

SOLUTION EXHIBIT 8-23

Actual Costs

Incurred

(1)

Actual Input

Quantity

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(4)

Variable

Manufacturing

Overhead

$618,840

(76,400 × $8)

$611,200

(78,600 × $8)

$628,800

(78,600 × $8)

$628,800

$7,640 U

Spending variance

$17,600 F

Efficiency variance

Never a variance

1.

Meals on Wheels

(May 2012)

Actual

Results

Flexible

Budget

Static

Budget

Output units (number of deliveries)

8,800

8,800

10,000

Hours per delivery

0.65a

0.70

0.70

Hours of delivery time

5,720

6,160b

7,000b

Variable overhead costs per delivery hour

$1.80c

$1.50

$1.50

Variable overhead (VOH) costs

$10,296

$9,240d

$10,500d

Fixed overhead costs

$38,600

$35,000

$35,000

Fixed overhead cost per hour

$5.00e

a 5,720 hours

0.70 hours/unit = 7,000 hours;

Fixed overhead rate = Fixed overhead costs

Static budget delivery hours = $35,000

7,000 hours = $5 per hour

VARIABLE OVERHEAD

Actual Costs

Incurred

Actual Input Quantity

Budgeted Rate

Flexible Budget:

Budgeted Input

Quantity Allowed for

Actual Output

Budgeted Rate

5,720 hrs

$1.50 per hr.

6,160 hrs

$1.50 per hr.

$10,296

$8,580

$9,240

$1,716 U $660 F

Spending variance Efficiency variance

2.

FIXED OVERHEAD

Actual Costs

Incurred

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of Output

Level

Allocated:

Budgeted Input

Quantity Allowed for

Actual Output

Budgeted Rate

8,800 units

0.70 hrs./unit

$5/hr.

6,160 hrs.

$5/hr.

$38,600

$35,000

$30,800

$3,600 U $4,200 U

Spending variance Production-volume variance

8-20

3. The spending variances for variable and fixed overhead are both unfavorable. This means

that MOW had increases over budget in either or both the cost of individual items (such as

0.65 hours versus a budgeted 0.70 hours.

MOW can best manage its fixed overhead costs by long-term planning of capacity rather

than day-to–day decisions. This involves planning to undertake only value-added fixed-overhead