6-1

6-1 The budgeting cycle includes the following elements:

a. Planning the performance of the company as a whole as well as planning the performance

6-2 The master budget expresses management’s operating and financial plans for a specified

6-3 Strategy, plans, and budgets are interrelated and affect one another. Strategy specifies

how an organization matches its own capabilities with the opportunities in the marketplace to

plans.

6-4 We agree that budgeted performance is a better criterion than past performance for

6-5 Production and marketing traditionally have operated as relatively independent business

functions. Budgets can assist in reducing conflicts between these two functions in two ways.

6-6 In many organizations, budgets impel managers to plan. Without budgets, managers drift

test.

6-7 A rolling budget, also called a continuous budget, is a budget or plan that is always

6-2

1. Prepare the revenues budget

3. Prepare the direct material usage budget and direct material purchases budget

5. Prepare the manufacturing overhead budget

7. Prepare the cost of goods sold budget

9. Prepare the budgeted income statement

6-10 Sensitivity analysis adds an extra dimension to budgeting. It enables managers to

6-11 Kaizen budgeting explicitly incorporates continuous improvement anticipated during the

budget period into the budget numbers.

6-12 Nonoutput-based cost drivers can be incorporated into budgeting by the use of activity–

6-13 The choice of the type of responsibility center determines what the manager is

6-14 Budgeting in multinational companies may involve budgeting in several different foreign

currencies. Further, management accountants must translate operating performance into a single

6-15 No. Cash budgets and operating income budgets must be prepared simultaneously. In

preparing their operating income budgets, companies want to avoid unnecessary idle cash and

6-16 (15 min.) Sales budget, service setting.

1.

Rouse & Sons

2011

Volume

At 2011

Selling Prices

Expected 2012

Change in Volume

Expected 2012

Volume

Radon Tests

12,200

$290

+6%

12,932

Lead Tests

16,400

$240

-10%

14,760

Radon Tests

$3,750,280

Lead Tests

$7,292,680

2011

Radon Tests

$290

Lead Tests

$230

-7%

Radon Tests

6-4

6-17 (5 min.) Sales and production budget.

Budgeted sales in units 200,000

6-18 (5 min.) Direct materials purchases budget.

Direct materials to be used in production (bottles) 2,500,000

6-19 (10 min.) Budgeting material purchases.

Production Budget:

Finished Goods

(units)

6-5

6-20 (30 min.) Revenues and production budget.

1.

Selling

Price

Units

Sold

Total

Revenues

12-ounce bottles

$0.25

4,800,000a

$1,200,000

4-gallon units

1.50

1,200,000b

1,800,000

$3,000,000

a 400,000 × 12 months = 4,800,000

b 100,000 × 12 months = 1,200,000

2. Budgeted unit sales (12-ounce bottles) 4,800,000

Add target ending finished goods inventory 600,000

3.

Beginning Budgeted Target Budgeted

= +

inventory sales ending inventory production

−

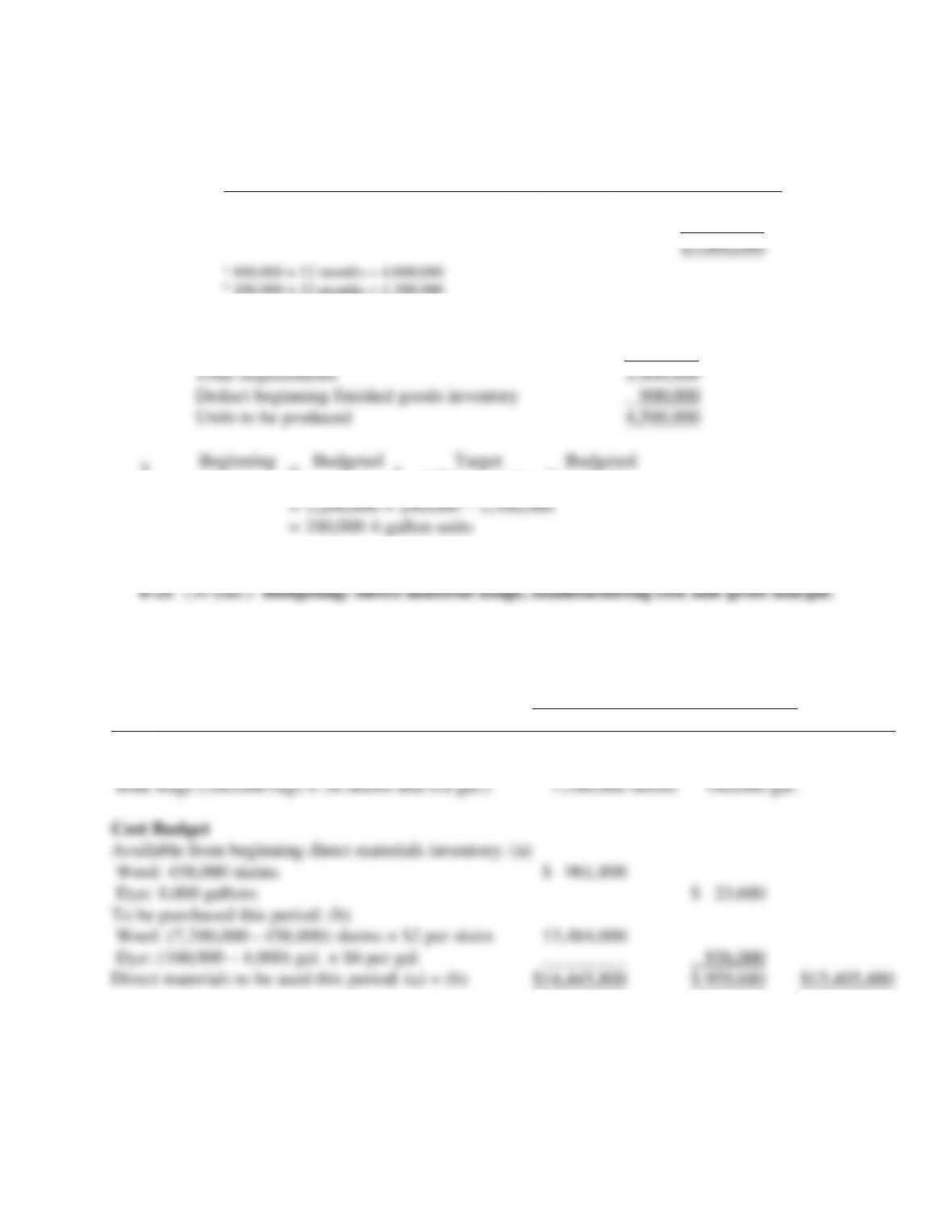

1.

Direct Material Usage Budget in Quantity and Dollars

Material

Wool

Dye

Total

Physical Units Budget

Direct materials required for

Blue Rugs (200,000 rugs × 36 skeins and 0.8 gal.)

7,200,000 skeins

160,000 gal.

Cost Budget

Available from beginning direct materials inventory: (a)

Wool: 458,000 skeins

$ 961,800

Dye: 4,000 gallons

$ 23,680

To be purchased this period: (b)

Wool: (7,200,000 – 458,000) skeins × $2 per skein

13,484,000

Dye: (160,000 – 4,000) gal. × $6 per gal.

_________

936,000

Direct materials to be used this period: (a) + (b)

$14,445,800

$ 959,680

$15,405,480

6-6

2.

Weaving budgeted

overhead rate

=

$31,620,000

12,400,000 DMLH

= $2.55 per DMLH

overhead rate

1,440,000 MH

3.

Budgeted Unit Cost of Blue Rug

Cost per

Unit of Input

Input per

Unit of

Output

Total

Wool

$2

36 skeins

$ 72.00

Dye

6

0.8 gal.

4.80

Direct manufacturing labor

13

62 hrs.

806.00

Dyeing overhead

12

7.21 mach-hrs.

86.40

Weaving overhead

2.55

62 DMLH

158.10

Total

$1127.30

10.2 machine hour per skein

36 skeins per rug = 7.2 machine-hrs. per rug.

4.

Revenue Budget

Units

Selling

Price

Total Revenues

Blue Rugs

200,000

$2,000

$400,000,000

Blue Rugs

185,000

$2,000

$370,000,000

5a.

Sales = 200,000 rugs

Cost of Goods Sold Budget

From Schedule

Total

Beginning finished goods inventory

$ 0

Direct materials used

$15,405,480

Direct manufacturing labor ($806 × 200,000)

161,200,000

Dyeing overhead ($86.40 × 200,000)

17,280,000

Weaving overhead ($158.10 × 200,000)

31,620,000

225,505,480

Cost of goods available for sale

225,505,480

Deduct ending finished goods inventory

0

Cost of goods sold

$225,505,480

6-7

5b.

Sales = 185,000 rugs

Cost of Goods Sold Budget

From Schedule

Total

Beginning finished goods inventory

$ 0

Direct materials used

$ 15,405,480

Direct manufacturing labor ($806 × 200,000)

161,200,000

Dyeing overhead ($86.40 × 200,000)

17,280,000

Weaving overhead ($158.10 × 200,000)

31,620,000

225,505,480

Cost of goods available for sale

225,505,480

Deduct ending finished goods inventory

($1,127.30 × 15,000)

16,909,500

Cost of goods sold

$208,595,980

6.

200,000 rugs sold

185,000 rugs sold

Revenue

$400,000,000

$370,000,000

Less: Cost of goods sold

225,505,480

208,595,980

Gross margin

$ 174,494,520

$ 161,404,020

1. 900,000 motorcycles 400,000 yen = 360,000,000,000 yen

2. Budgeted sales (motorcycles) 900,000

Add target ending finished goods inventory 80,000

3. Direct materials to be used in production,

880,000 × 2 (wheels) 1,760,000

Add target ending direct materials inventory 60,000

6-8

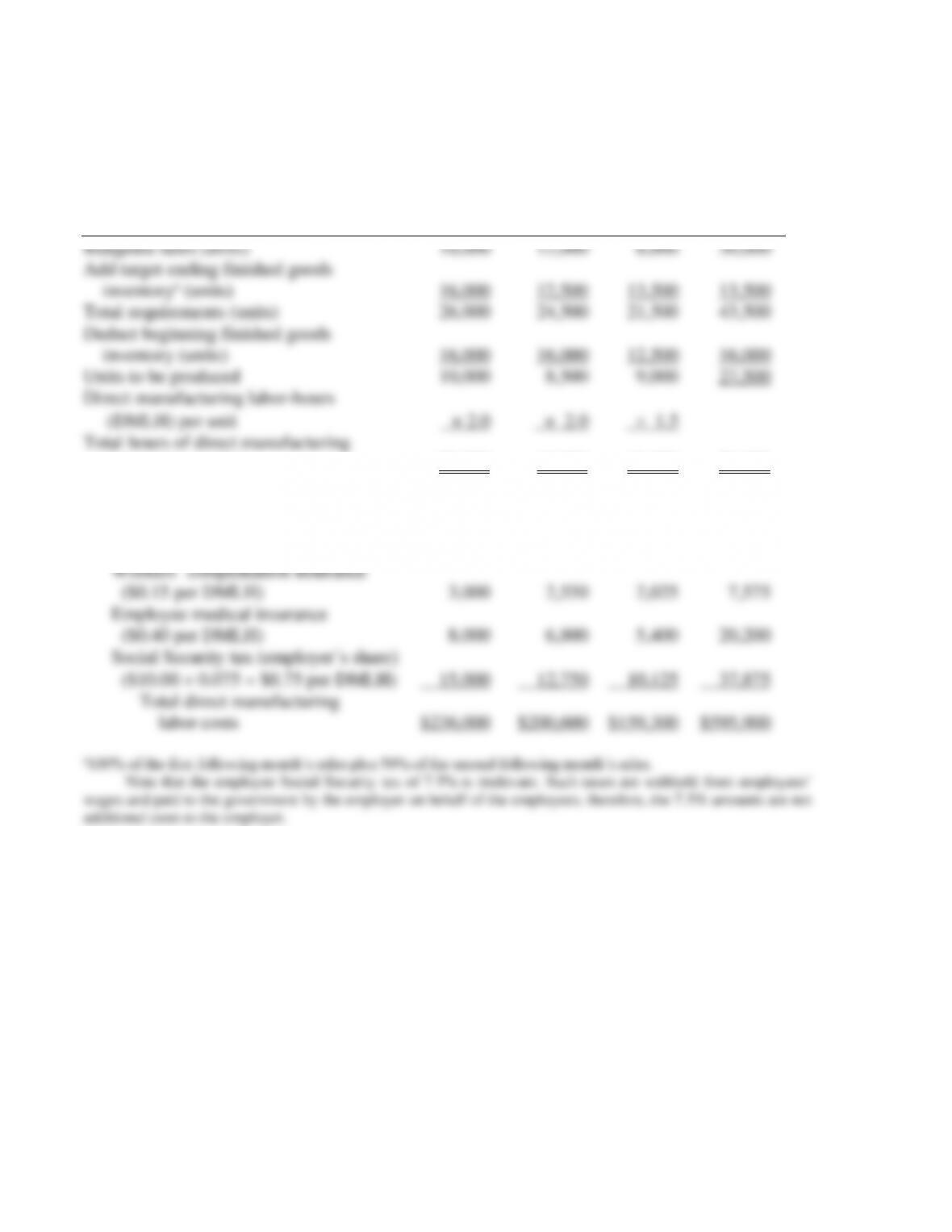

6-23 (15-25 min.) Budgets for production and direct manufacturing labor.

Roletter Company

Budget for Production and Direct Manufacturing Labor

for the Quarter Ended March 31, 2013

January February March Quarter

labor time needed 20,000 17,000 13,500 50,500

Direct manufacturing labor costs:

Wages ($10.00 per DMLH) $200,000 $170,000 $135,000 $505,000

Pension contributions

($0.50 per DMLH) 10,000 8,500 6,750 25,250

1. This question links to the ABC example used in the Problem for Self-Study in Chapter 5

and to Question 5-24 (ABC, retail product-line profitability).

Activity

Cost

Hierarchy

Soft

Drinks

Fresh

Produce

Packaged

Food

Total

Ordering

$90 14; 24; 14

Delivery

$82 12; 62; 19

Shelf-stocking

$21 16; 172; 94

Customer support

$0.18 4,600; 34,200; 10,750

Total budgeted indirect costs

Percentage of total indirect costs

Batch-level

Batch-level

Output-unit-

level

Output-unit-

level

$1,260

984

336

828

$3,408

12.5%

$ 2,160

5,084

3,612

6,156

$17,012

62.7%

$1,260

1,558

1,974

1,935

$6,727

24.8%

$ 4,680

7,626

5,922

8,919

$27,147

(62.7%) of the indirect resources. Fresh produce demands the highest level of ordering, delivery,

3. An ABB approach recognizes how different products require different mixes of support

activities. The relative percentage of how each product area uses the cost driver at each activity

area is:

Activity

Cost

Hierarchy

Soft

Drinks

Fresh

Produce

Packaged

Food

Total

Ordering

Delivery

Shelf-stocking

Customer support

Batch-level

Batch-level

Output-unit-level

Output-unit-level

27%

13

6

9

46%

67

61

69

27%

20

33

22

100%

100

100

100

By recognizing these differences, FS managers are better able to budget for different unit sales

levels and different mixes of individual product-line items sold. Using a single cost driver (such

as COGS) assumes homogeneity in the use of indirect costs (support activities) across product

lines which does not occur at FS. Other benefits cited by managers include: (1) better

identification of resource needs, (2) clearer linking of costs with staff responsibilities, and (3)

identification of budgetary slack.

6-10

1.

Budgeted Cost-Driver Rates

Activity

Cost Hierarchy

January

February

March

Ordering

Delivery

Shelf-stocking

Customer support

Batch-level

Batch-level

Output-unit-level

Output-unit-level

$90.00

82.00

21.00

0.18

$89.6400

81.6720

20.9160

0.1793

$89.2814

81.3453

20.8323

0.1786

The March 2011 rates can be used to compute the total budgeted cost for each activity area in

March 2011:

Activity

Cost

Hierarchy

Soft

Drinks

Fresh

Produce

Packaged

Food

Total

Ordering

$89.2814

14; 24; 14

Delivery

$81.3453

12; 62; 19

Shelf-stocking

$20.8323

16; 172; 94

Customer support

$0.1786

4,600;

34,200; 10,750

Total

Batch-level

Batch-level

Output-unit-level

Output-unit-level

$1,250

976

333

821

$3,380

$ 2,143

5,043

3,583

6,108

$16,877

$1,250

1,546

1,958

1,920

$6,674

$ 4,643

7,565

5,874

8,849

$26,931

2. A kaizen budgeting approach signals management’s commitment to systematic cost

reduction. Compare the budgeted costs from Question 6–24 and 6-25.

Ordering

Delivery

Shelf-

Stocking

Customer

Support

Question 6-24

$4,680

$7,626

$5,922

$8,919

Question 6-25 (Kaizen)

4,643

7,565

5,874

8,849

The kaizen budget number will show unfavorable variances for managers whose activities do not

meet the required monthly cost reductions. This likely will put more pressure on managers to