A summary of the variances is:

Sales-Volume Variance

Mint chocolate chip $24,360 F

Vanilla 43,500 U

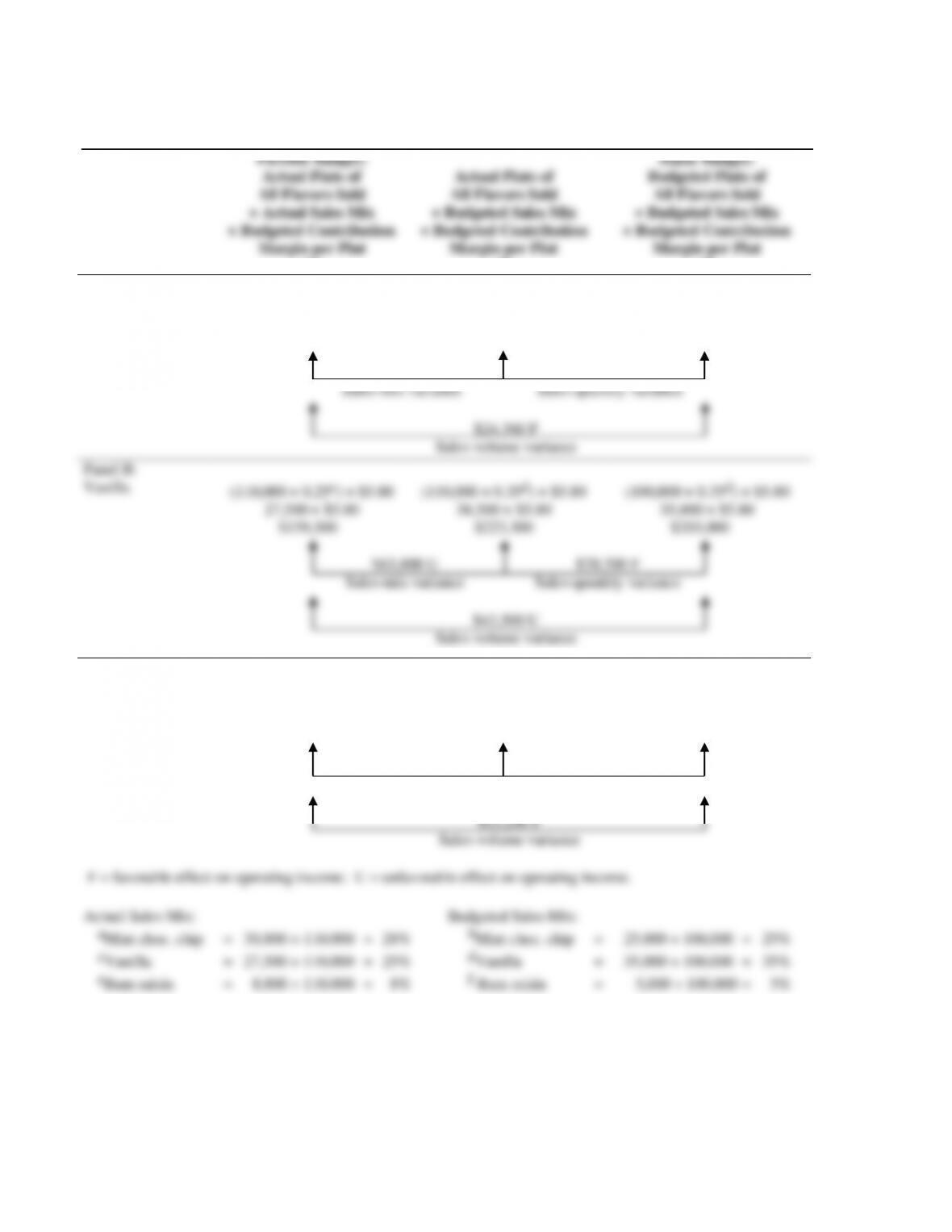

SOLUTION EXHIBIT 14-34

Columnar Presentation of Sales-Volume, Sales-Quantity, and Sales-Mix Variances

for The Split Banana

Flexible Budget:

Actual Pints of

All Flavors Sold

× Actual Sales Mix

× Budgeted Contribution

Margin per Pint

(1)

Actual Pints of

All Flavors Sold

× Budgeted Sales Mix

× Budgeted Contribution

Margin per Pint

(2)

Static Budget:

Budgeted Pints of

All Flavors Sold

× Budgeted Sales Mix

× Budgeted Contribution

Margin per Pint

(3)

Panel A:

Mint choc. chip

(110,000 × 0.28a) × $4.20

30,800 × $4.20

(110,000 × 0.25b) × $4.20

27,500 × $4.20

(100,000 × 0.25b) × $4.20

25,000 × $4.20

$129,360 $115,500 $105,000

Panel B:

Vanilla

(110,000 × 0.25c) × $5.80

27,500 × $5.80

(110,000 × 0.35d) × $5.80

38,500 × $5.80

(100,000 × 0.35d) × $5.80

35,000 × $5.80

$159,500 $223,300 $203,000

Panel C:

Rum Raisin

(110,000 × 0.08e) × $4.00

8,800 × $4.00

(110,000 × 0.05f) × $4.00

5,500 × $4.00

(100,000 × 0.05f) × $4.00

5,000 × $4.00

$35,200 $22,000 $20,000

$13,860 F

Sales-mix variance

$10,500 F

Sales-quantity variance

$24,360 F

Sales-volume variance

$63,800 U

Sales-mix variance

$20,300 F

Sales-quantity variance

$43,500 U

Sales-volume variance

$13,200 F

Sales-mix variance

$2,000 F

Sales-quantity variance

$15,200 F

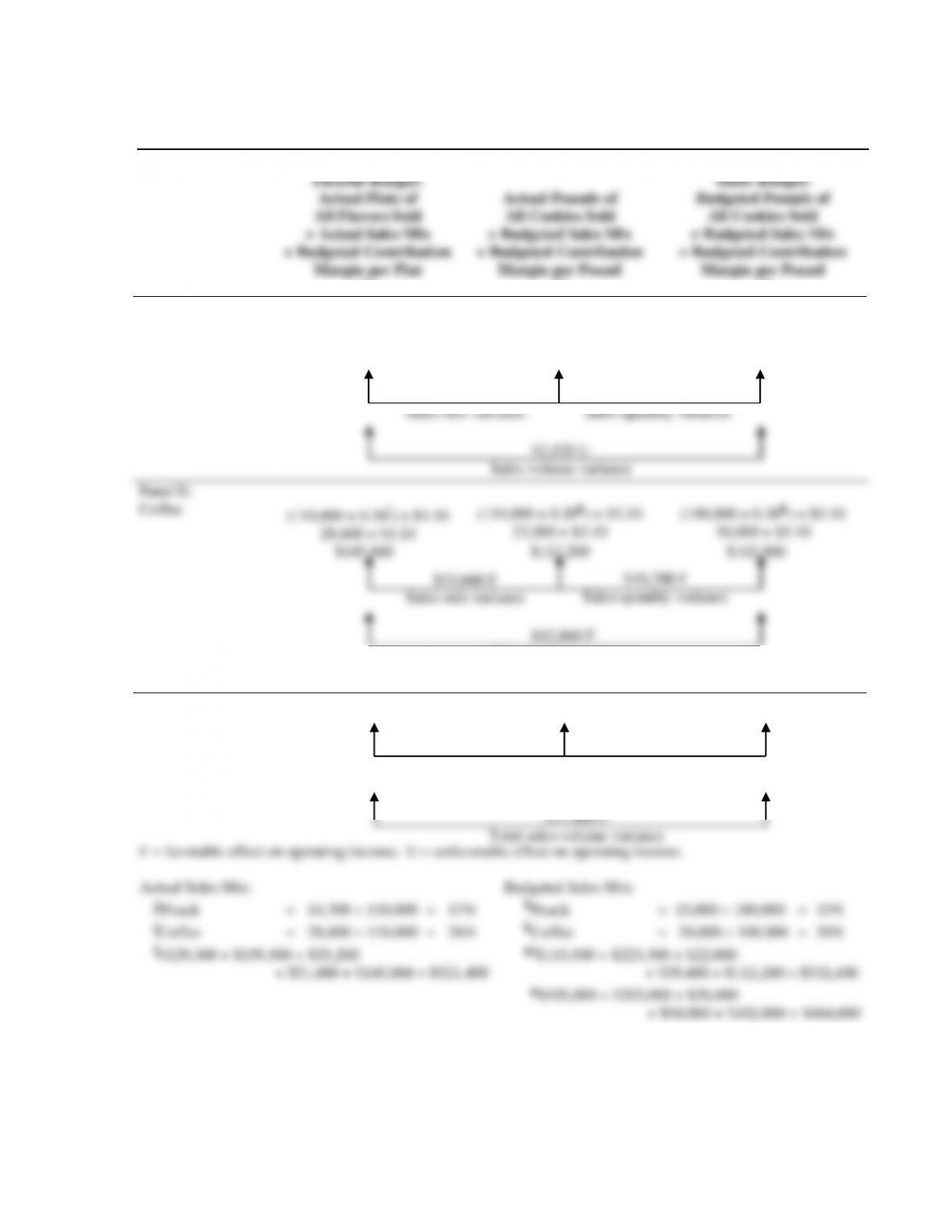

SOLUTION EXHIBIT 14-34 (Cont’d.)

Columnar Presentation of Sales-Volume, Sales-Quantity, and Sales-Mix Variances

for The Split Banana

Flexible Budget:

Actual Pints of

All Flavors Sold

× Actual Sales Mix

× Budgeted Contribution

Margin per Pint

(1)

Actual Pounds of

All Cookies Sold

× Budgeted Sales Mix

× Budgeted Contribution

Margin per Pound

(2)

Static Budget:

Budgeted Pounds of

All Cookies Sold

× Budgeted Sales Mix

× Budgeted Contribution

Margin per Pound

(3)

Panel D:

Peach

(110,000 × 0.13g) × $3.60

14,300 × $3.60

(110,000 × 0.15h) × $3.60

16,500 × $3.60

(100,000 × 0.15h) × $3.60

15,000 × $3.60

$51,480 $59,400 $54,000

Panel E:

Coffee

(110,000 × 0.26j) × $5.10

28,600 × $5.10

(110,000 × 0.20k) × $5.10

22,000 × $5.10

(100,000 × 0.20k) × $5.10

20,000 × $5.10

$145,860 $112,200 $102,000

Panel F: $521,400l $532,400m $484,000n

All Flavors

F = favorable effect on operating income; U = unfavorable effect on operating income.

Actual Sales Mix:

gPeach = 14,300 ÷ 110,000 = 13%

jCoffee = 28,600 ÷ 110,000 = 26%

l$129,360 + $159,500 + $35,200

+ $51,480 + $145,860 = $521,400

Budgeted Sales Mix:

hPeach = 15,000 ÷ 100,000 = 15%

kCoffee = 20,000 ÷ 100,000 = 20%

m$115,500 + $223,300 + $22,000

+ $59,400 + $112,200 = $532,400

n$105,000 + $203,000 + $20,000

+ $54,000 + $102,000 = $484,000

$7,920 U

Sales-mix variance

$5,400 F

Sales-quantity variance

$2,520 U

Sales-volume variance

$33,660 F

Sales-mix variance

$10,200 F

Sales-quantity variance

$43,860 F

Sales-volume variance

$11,000 U

Total sales-mix variance

$48,400 F

Total sales-quantity variance

$37,400 F

Total sales-volume variance

1. Almonds ($1 × 180 cups) $ 180

Cashews ($2 × 300 cups) 600

2. Solution Exhibit 14-35A presents the total price variance ($0), the total efficiency

variance ($610 U), and the total flexible-budget variance ($610 U).

Total direct materials efficiency variance can also be computed as:

Direct materials

efficiency variance

for each input

=

( )

Actual quantity Budgeted quantity of input

of input allowed for actual output

−

×

Budgeted

price of input

Almonds = (5,280 – 4,500) × $1 = $ 780 U

Cashews = (7,520 – 7,500) × $2 = 40 U

Pistachios = (2,720 – 2,250) × $3 = 1,410 U

Seasoning = ( 480 – 750) × $6 = 1,620 F

Total direct materials efficiency variance $ 610 U

SOLUTION EXHIBIT 14-35A

Columnar Presentation of Direct Materials Price and Efficiency Variances for Nature’s Best

Company.

Actual Costs

Incurred

(Actual Input Quantity

× Actual Price)

(1)

Actual Input Quantity

× Budgeted Price

(2)

Flexible Budget

(Budgeted Input Quantity

Allowed for Actual Output

× Budgeted Price)

(3)

Almonds

5,280 × $1 = $ 5,280

5,280 × $1 = $ 5,280

4,500 × $1 = $ 4,500

Cashews

7,520 × $2 = 15,040

7,520 × $2 = 15,040

7,500 × $2 = 15,000

Pistachios

2,720 × $3 = 8,160

2,720 × $3 = 8,160

2,250 × $3 = 6,750

Seasonings

480 × $6 = 2,880

480 × $6 = 2,880

750 × $6 = 4,500

$31,360

$31,360

$30,750

$0 $610 U

Total price variance Total efficiency variance

$610 U

Total flexible-budget variance

F = favorable effect on operating income; U = unfavorable effect on operating income

14-45

4. Solution Exhibit 14-35B presents the total direct materials yield and mix variances.

The total direct materials yield variance can also be computed as the sum of the direct

materials yield variances for each input:

Direct

materials

yield variance

for each input

=

Actual total Budgeted total quantity

quantity of all of all direct materials inputs

direct materials allowed for actual output

inputs used

−

×

Budgeted

direct materials

input mix

percentage

×

Budgeted

price of

direct materials

inputs

Almonds = (16,000 – 15,000) × 0.30a × $1 = 1,000 × 0.30 × $1 = $ 300 U

Cashews = (16,000 – 15,000) × 0.50b × $2 = 1,000 × 0.50 × $2 = 1,000 U

Pistachios = (16,000 – 15,000) × 0.15c × $3 = 1,000 × 0.15 × $3 = 450 U

Seasoning = (16,000 – 15,000) × 0.05d × $6 = 1,000 × 0.05 × $6 = 300 U

Total direct materials yield variance $2,050 U

a 180

600; b 300

600; c 90

600; d30

600

The total direct materials mix variance can also be computed as the sum of the direct materials

mix variances for each input:

Direct

materials

mix variance

for each input

=

Actual Budgeted

direct materials direct materials

input mix input mix

percentage percentage

−

×

Actual total

quantity of all

direct materials

inputs used

×

Budgeted

price of

direct materials

inputs

Almonds = (0.33 – 0.30) × 16,000 × $1 = 0.03 × 16,000 × $1 = $ 480 U

Cashews = (0.47 – 0.50) × 16,000 × $2 = –0.03 × 16,000 × $2 = 960 F

Pistachios = (0.17 – 0.15) × 16,000 × $3 = 0.02 × 16,000 × $3 = 960 U

Seasoning = (0.03 – 0.05) × 16,000 × $6 = –0.02 × 16,000 × $6 = 1,920 F

Total direct materials mix variance $1,440 F

SOLUTION EXHIBIT 14-35B

Columnar Presentation of Direct Materials Yield and Mix Variances for Nature’s Best Company.

Actual Total Quantity

of All Inputs Used

× Actual Input Mix

× Budgeted Price

(1)

Actual Total Quantity

of All Inputs Used

× Budgeted Input Mix

× Budgeted Price

(2)

Flexible Budget:

Budgeted Total Quantity of

All Inputs Allowed for

Actual Output ×

Budgeted Input Mix

× Budgeted Price

(3)

Almonds 16,000 × 0.33 × $1 = $ 5,280

Cashews 16,000 × 0.47 × $2 = 15,040

Pistachios 16,000 × 0.17 × $3 = 8,160

Seasoning 16,000 × 0.03 × $6 = 2,880

$31,360

16,000 × 0.30 × $1 = $ 4,800

16,000 × 0.50 × $2 = 16,000

16,000 × 0.15 × $3 = 7,200

16,000 × 0.05 × $6 = 4,800

$32,800

15,000 × 0.30 × $1 = $ 4,500

15,000 × 0.50 × $2 = 15,000

15,000 × 0.15 × $3 = 6,750

15,000 × 0.05 × $6 = 4,500

$30,750

$1,440 F $2,050 U

Total mix variance Total yield variance

$610 U

Total efficiency variance

F = favorable effect on operating income; U = unfavorable effect on operating income.

The direct materials mix variance of $1,440 F indicates that the actual product mix uses relatively more

of less expensive ingredients than planned. In this case, the actual mix contains slightly more almonds

and pistachios, while using fewer cashews and substantially less seasoning.

The direct materials yield variance of $2,050 U occurs because the amount of total inputs needed

(16,000 cups) exceeded the budgeted amount (15,000 cups) expected to produce 2,500 tins.

The direct materials yield variance is significant enough to be investigated. The mix variance may be

within expectations, but should be monitored since it is favorable largely due to the use of less

seasoning, which is considered an important element of the product’s appeal to customers.

14-47

1.

George ($30 × 6 hrs.)

$ 180

Earl ($20 × 4 hrs.)

80

Cost per guitar

$ 260

Number of guitars

× 25 units

Total budgeted cost

$ 6,500

2. Solution Exhibit 14-36A presents the total price variance ($0), the total efficiency variance

($10 U), and the total flexible-budget variance ($10U).

Total direct labor price variance can also be computed as:

Direct labor

price variance

for each input

=

Actual Budgeted

price of price of

input input

−

×

Actual

quantity

of input

George = ($30 – $30) × 145 = $0

Earl = ($20 – $20) × 108 = 0

Total direct labor price variance $0

Total direct labor efficiency variance can also be computed as:

Direct labor

efficiency variance

for each input

=

( )

Actual quantity Budgeted quantity of input

of input allowed for actual output

−

×

Budgeted

price of input

George = (145 – 150) × $30.00 = $150 F

Earl = (108 – 100) × $20.00 = 160 U

Total direct labor efficiency variance $ 10 U

SOLUTION EXHIBIT 14-36A

Columnar Presentation of Direct Labor Price and Efficiency Variances for Trevor Joseph Guitars

Actual Costs

Incurred

(Actual Input Quantity

× Actual Price)

(1)

Actual Input Quantity

× Budgeted Price

(2)

Flexible Budget

(Budgeted Input Quantity

Allowed for Actual Output

× Budgeted Price)

(3)

George

145 $30 = $4,350

145 $30 = $4,350

150 $30 = $4,500

Earl

108 $20 = 2,160

108 $20 = 2,160

100 $20 = 2,000

$6,510

$6,510

$6,500

$0 $10 U

Total price variance Total efficiency variance

$10 U

Total flexible-budget variance

F = favorable effect on operating income; U = unfavorable effect on operating income

3.

Actual Quantity

of Input

Actual

Mix

Budgeted Quantity

of Input for Actual Output

Budgeted

Mix

George

145 hours

57.3%

6 hours × 25 units = 150 hours

60%

Earl

108 hours

42.7%

4 hours × 25 units = 100 hours

40%

Total

253 hours

100.0%

250 hours

100%

4. Solution Exhibit 14-36B presents the total direct labor yield and mix variances for Trevor

Joseph Guitars.

The total direct labor yield variance can also be computed as the sum of the direct labor

yield variances for each input:

Direct labor

Actual total

quantity of all

Budgeted total quantity

of all direct labor

Budgeted direct

Budgeted price