The total direct labor mix variance can also be computed as the sum of the direct labor mix

variances for each input:

Direct labor

mix variance

for each input

=

Actual direct

labor input

mix percentage

–

Budgeted direct

labor input

mix percentage

Actual total quantity

of all direct labor

inputs used

Budgeted price

of direct labor

inputs

14-50

14-37 (30 min.) Purposes of cost allocation

SR460. Therefore, only inventoriable costs, such as direct materials, direct labor, and

manufacturing overhead, are included in the cost of SR460 that are given to the financial

2. For the four different purposes considered in the question, the cost of one unit of SR460

would be determined as follows:

a.

b.

c.

d.

Direct materials

$28.50

$28.50

$28.50

$28.50

Direct manufacturing labor

16.35

16.35

16.35

16.35

Variable manufacturing overhead

8.76

8.76

8.76

8.76

Allocated fixed manufacturing

overhead

32.84

32.84

32.84

Research and development costs

specific to SR460

6.20

Marketing costs

5.95

Sales commissions

11.40

Allocated administrative costs of

production department

5.38

5.38

Allocated administrative costs of

corporate headquarters

18.60

Customer service costs

3.05

Distribution costs

8.80

Total

$145.83

$86.45

$53.61

$91.83

14-51

14-38 (30 min.) Customer-cost hierarchy, customer profitability.

1.

Architecture Firms

Commercial Clients

Total

Total

Total

(all customers)

Architecture

AA

BB

Commercial

CC

DD

EE

(1) = (2) + (5)

(2) = (3) + (4)

(3)

(4)

(5) = (6)+(7)+(8)

(6)

(7)

(8)

Gross Revenues

$250,305

$105,700

$58,500

$47,200

$144,605

$89,345

$36,960

$18,300

(less) Discounts

___6,765

___5,850

5,850

_____0

915

_____0

_____0

915

Net Revenues

243,540

99,850

52,650

47,200

143,690

89,345

36,960

17,385

Customer-level costs

163,885

66,050

36,750

29,300

97,835

54,645

28,930

14,260

Customer-level operating income

79,655

33,800

$15,900

$17,900

45,855

$34,700

$ 8,030

$ 3,125

Distribution-channel (Overhead) costsa

55,315

21,275

34,040

Distribution-channel-level oper. income

24,340

$ 12,525

$ 11,815

Corporate-sustaining costsa

29,785

Operating income

$ (5,445)

2.

Cumulative

Customer-Level

Operating Income

Customer-Level

Customer-Level

Cumulative

as a % of Total

Operating

Customer

Operating Income

Customer-Level

Customer-Level

Customer

Income

Revenue

as a % of Revenue

Operating Income

Operating Income

Code

(1)

(2)

(3) = (1)

(2)

(4)

(5) = (4)

$79,655

CC

$34,700

$ 89,345

38.84%

$34,700

43.6%

BB

17,900

47,200

37.92%

52,600

66.0%

AA

15,900

52,650

30.20%

68,500

86.0%

DD

8,030

36,960

21.72%

76,530

96.1%

EE

3,125

17,385

17.98%

79,655

100.0%

$79,655

$243,540

14-52

3. Designs by Denise reported a net operating loss for the quarter. All of Denise’s customers are

profitable, but the presence of substantial corporate-sustaining costs led to the overall negative

level of income. Offering a discount to Attractive Abodes in order to gain their business was a

14-53

14-39 (40 min.) Customer profitability and ethics.

1. Order taking – Customer batch-level

Product handling – Customer output-unit-level

2. Customer-level operating income based on expected cost of orders:

Customers

SR

SRU

NS

SB

SM

WS

Revenues

$50 × 250; 550; 320; 130; 450; 1,200

$12,500

$27,500

$16,000

$6,500

$22,500

$60,000

Less: Returns

$50 ×20; 35; 0; 0; 40; 60

1,000

1,750

0

0

2,000

3,000

Net Revenues

$50 ×230; 515; 320; 130; 410; 1140

11,500

25,750

16,000

6,500

20,500

57,000

Cost of goods sold

$35 × 230; 515; 320; 130; 410; 1,140

8,050

18,025

11,200

4,550

14,350

39,900

Gross margin

3,450

7,725

4,800

1,950

6,150

17,100

Customer-level operating costs:

Order taking

$30 ×6; 15; 8; 7; 20; 30

180

450

240

210

600

900

Product handling

$2 × 250; 550; 320; 130; 450; 1,200

500

1,100

640

260

900

2,400

Delivery

$0.50 × 420; 620; 470; 280; 806; 900

210

310

235

140

403

450

Expedited delivery

$325 × 0; 6; 0; 0; 2; 5

0

1,950

0

0

650

1,625

Restocking

$100 ×2; 1; 0; 0; 2; 6

200

100

0

0

200

600

Visits to customers

150

150

150

150

150

150

Sales commissions

$25× 6; 15; 8; 7; 20; 30

150

375

200

175

500

750

Total customer-level operating costs

1,390

4,435

1,465

935

3,403

6,875

Customer-level operating income

$ 2,060

$ 3,290

$ 3,335

$1,015

$ 2,747

$10,225

14-54

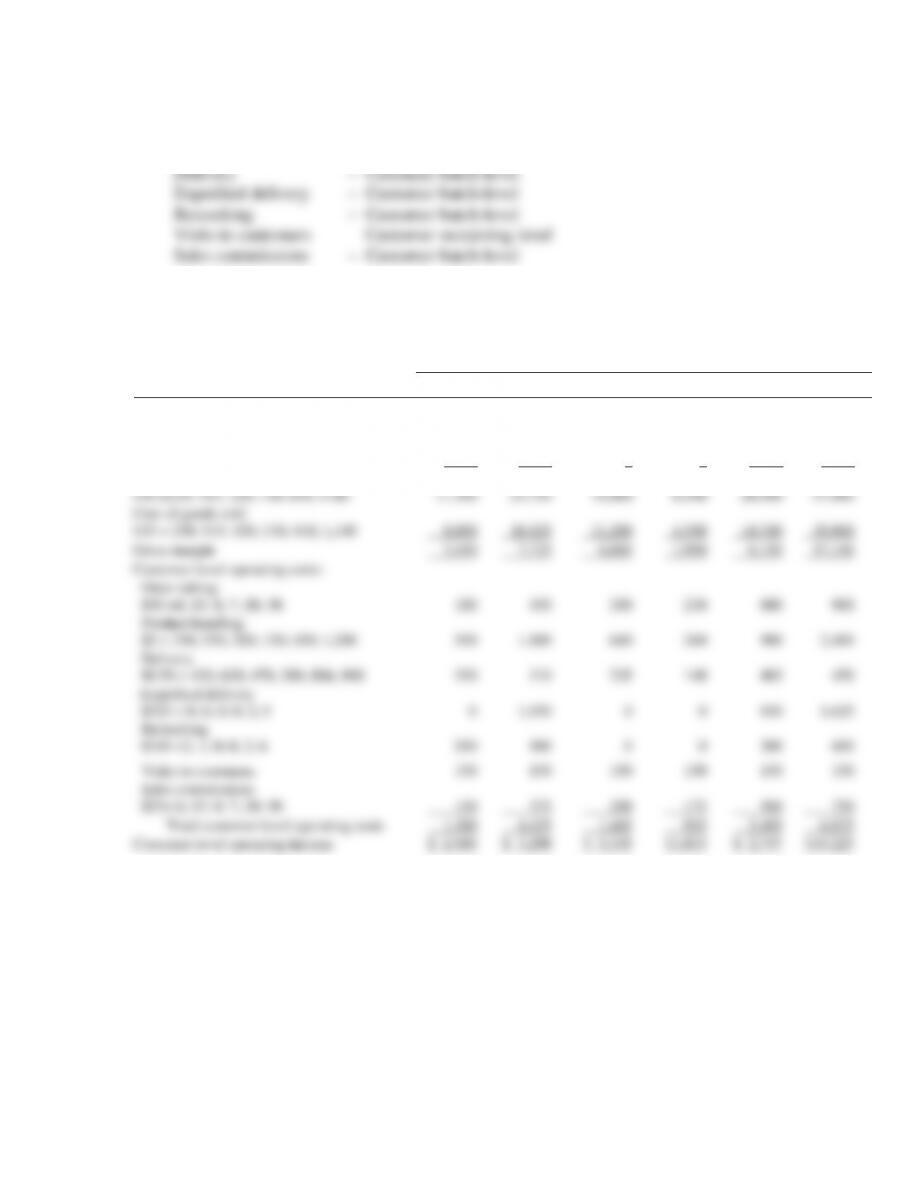

3. Customer level operating income based on actual order costs:

Customer

SR

SRU

NS

SB

SM

WS

Revenues

$50 × 250; 550; 320; 130; 450; 1,200

$12,500

$27,500

$16,000

$6,500

$22,500

$60,000

Less: Returns

$50 ×20; 35; 0; 0; 40; 60

1,000

1,750

0

0

2,000

3,000

Net Revenues

$50 ×230; 515; 320; 130; 410; 1,140

11,500

25,750

16,000

6,500

20,500

57,000

Cost of good sold

$35 × 230; 515; 320; 130; 410; 1,140

8,050

18,025

11,200

4,550

14,350

39,900

Gross margin

3,450

7,725

4,800

1,950

6,150

17,100

Customer-level operating costs:

Order taking

$14 × 6; $30 × 15; $14 × 8; $14 × 7;

$14 × 20; $14 × 30

84

450

112

98

280

420

Product handling

$2 × 250; 550; 320; 130; 450; 1,200

500

1,100

640

260

900

2,400

Delivery

$0.50 × 420; 620; 470; 280; 806; 900

210

310

235

140

403

450

Expedited delivery

$325 × 0; 6; 0; 0; 2; 5

0

1,950

0

0

650

1,625

Restocking

$100 ×2; 1; 0; 0; 2; 6

200

100

0

0

200

600

Visits to customers

150

150

150

150

150

150

Sales commissions

$25× 6; 15; 8; 7; 20; 30

150

375

200

175

500

750

Total customer-level operating costs

1,294

4,435

1,337

823

3,083

6,395

Customer-level operating income

$ 2,156

$ 3,290

$ 3,463

$1,127

$ 3,067

$ 10,705

Comparing the answers in requirements 2 and 3, it appears that operating income is higher than

expected, so the management of Snark Corporation would be very pleased with the performance

of the salespeople for reducing order costs. Except for SRU, all of the customers are more

profitable than originally reported.

14-55

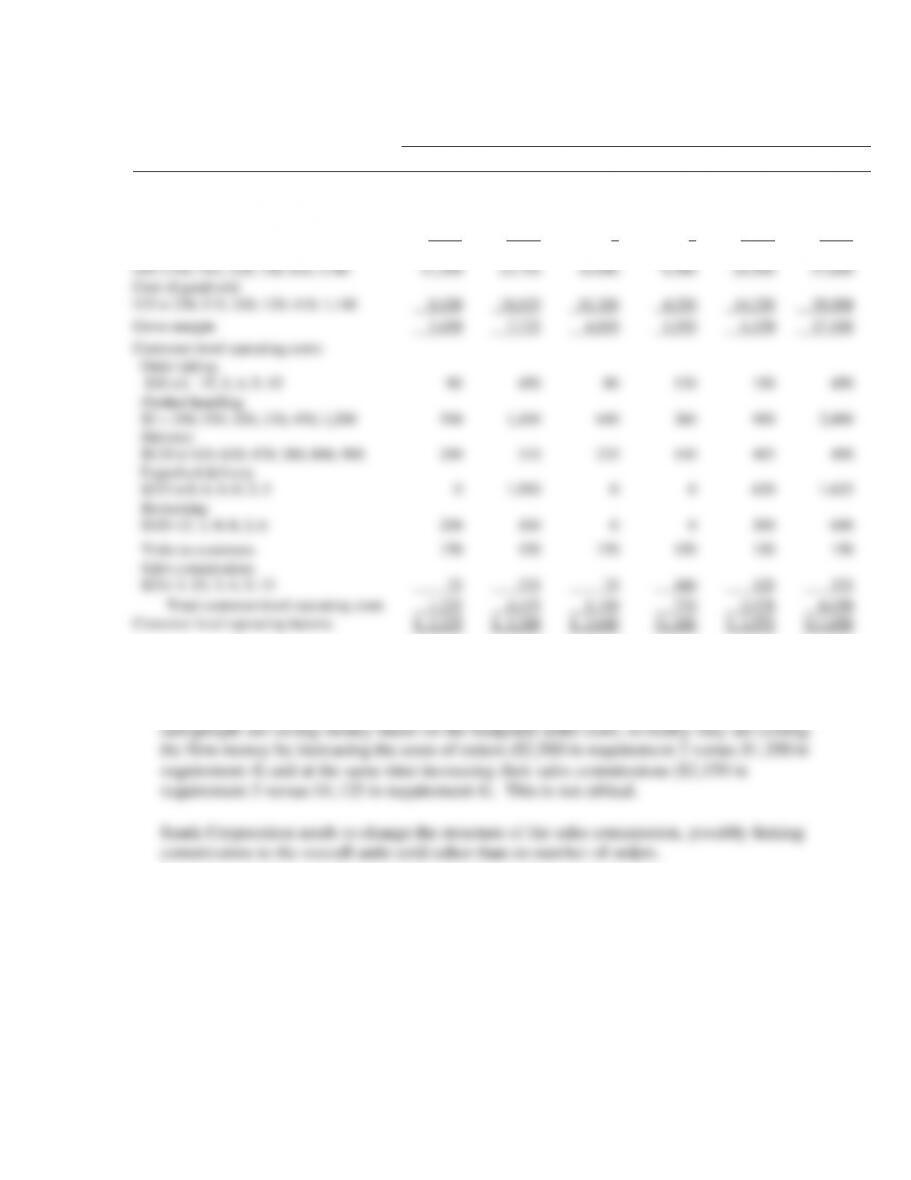

4. Customer-level operating income based on actual orders and adjusted commissions

Customer

SR

SRU

NS

SB

SM

WS

Revenues

$50 × 250; 550; 320; 130; 450; 1,200

$12,500

$27,500

$16,000

$6,500

$22,500

$60,000

Less: Returns

$50 ×20; 35; 0; 0; 40; 60

1,000

1,750

0

0

2,000

3,000

Net Revenues

$50 ×230; 515; 320; 130; 410; 1140

11,500

25,750

16,000

6,500

20,500

57,000

Cost of good sold

$35 × 230; 515; 320; 130; 410; 1,140

8,050

18,025

11,200

4,550

14,350

39,900

Gross margin

3,450

7,725

4,800

1,950

6,150

17,100

Customer-level operating costs:

Order taking

$30 ×3; 15; 3; 4; 5; 15

90

450

90

120

150

450

Product handling

$2 × 250; 550; 320; 130; 450; 1,200

500

1,100

640

260

900

2,400

Delivery

$0.50 × 420; 620; 470; 280; 806; 900

210

310

235

140

403

450

Expedited delivery

$325 × 0; 6; 0; 0; 2; 5

0

1,950

0

0

650

1,625

Restocking

$100 ×2; 1; 0; 0; 2; 6

200

100

0

0

200

600

Visits to customers

150

150

150

150

150

150

Sales commissions

$25× 3; 15; 3; 4; 5; 15

75

375

75

100

125

375

Total customer-level operating costs

1,225

4,435

1,190

770

2,578

6,050

Customer-level operating income

$ 2,225

$ 3,290

$ 3,610

$1,180

$ 3,572

$11,050

5. The behavior of the salespeople is costing Snark Corporation $1,119 in profit (the

difference between the incomes in requirements 3 and 4.) Although management thinks the