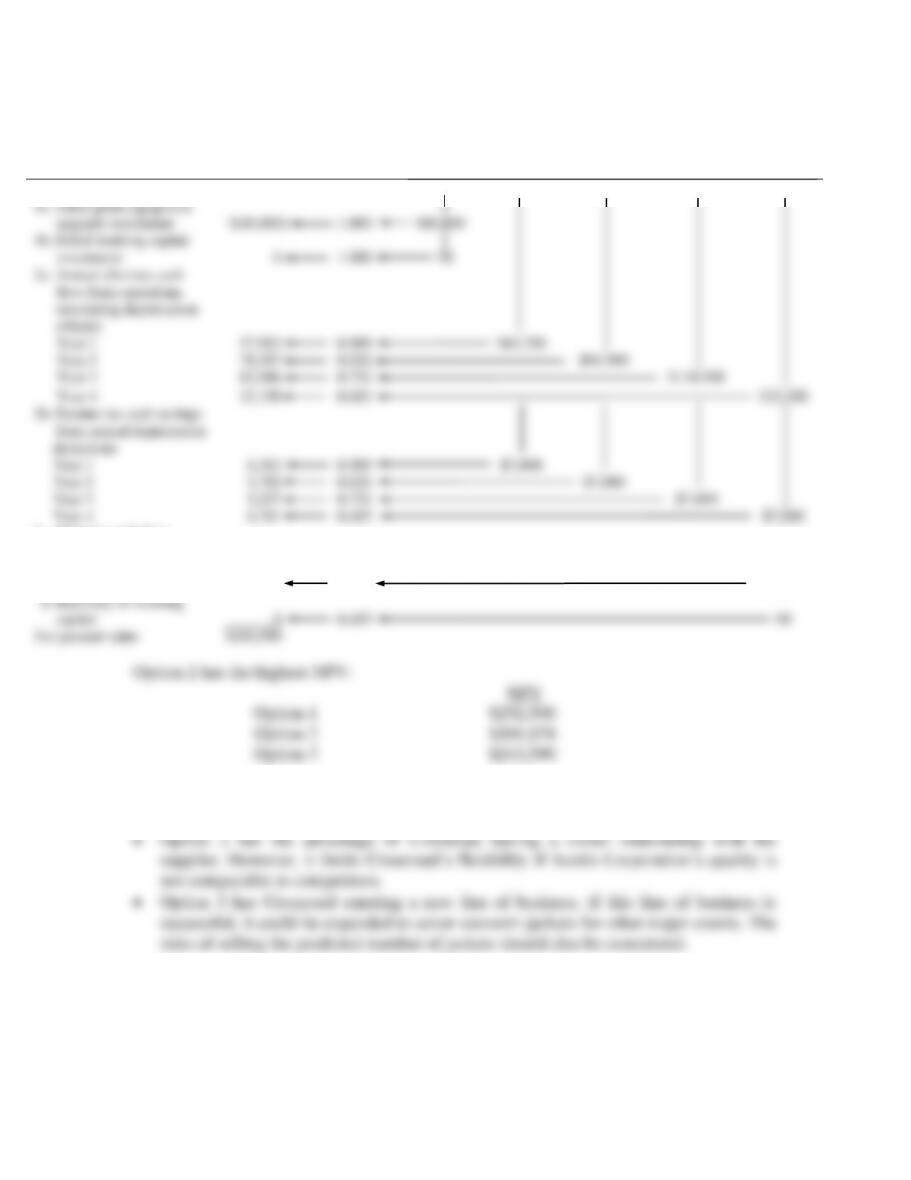

SOLUTION EXHIBIT 21-25

Total

Present

Value

Present Value

Discount

Factors

At 10%

Sketch of Relevant After-Tax Cash Flows

0

1

2

3

4

5

1a. Initial

motor

investment

$(75,000)

1.000

$(75,000)

1b. Initial working

capital investment

0

1.000

$0

2a. Annual after-

tax cash flow from

operations (excl. depr.)

Year 1

14,771

0.909

$16,250

Year 2

13,423

0.826

$16,250

Year 3

12,204

0.751

$16,250

Year 4

11,099

0.683

$16,250

Year 5

10,091

0.621

$16,250

2b Income tax cash

savings from

annual deprec.

Deductions

Year 1

4,772

0.909

$5250

Year 2

4,337

0.826

$5250

Year 3

3,943

0.751

$5250

Year 4

3,586

0.683

$5250

Year 5

3,260

0.621

$5250

3. After-tax cash

flow from:

a. Terminal

disposal of

motor

0

0.621

$0

b. Recovery of

working capital

0

0.621

$0

Net present value if

new motor is

purchased

$ 6,486

21-22

21-26 (60 min.) Selling a plant, income taxes.

1. Option 1

Current disposal price $450,000

Deduct current book value 0

Gain on disposal 450,000

1. Rent

` $ 64,994 0.909 $71,500

2. Discount on

Purchases $11,817 0.909 $13,000

21-23

Option 3

Contribution margin per jacket:

$12.00 × 9,000; 13,000;

15,000; 5,000 $108,000 $156,000 $180,000 $60,000

Fixed overhead (cash) costs 10,000 10,000 10,000 10,000

SOLUTION EXHIBIT 21-26

Total

Present

Value

Present Value

Discount

Factors at

10%

Sketch of Relevant After-Tax Cash Flows

2011

2012

2013

2014

2015

1a. Initial plant equipment

upgrade investment

$(80,000)

1.000

$80,000

1b. Initial working capital

investment

0

1.000

$0

2a. Annual after-tax cash

flow from operations

(excluding depreciation

effects)

Year 1

57,903

0.909

$63,700

Year 2

78,387

0.826

$94,900

Year 3

82,986

0.751

$110,500

Year 4

22,198

0.683

$32,500

2b. Income tax cash savings

from annual depreciation

deductions

Year 1

6,363

0.909

$7,000

Year 2

5,782

0.826

$7,000

Year 3

5,257

0.751

$7,000

Year 4

4,781

0.683

$7,000

3. After-tax cash flow

From

a. Terminal disposal

of plant

59,933

0.683

$87,750

b. Recovery of working

capital

0

0.683

$0

Net present value

$243,590

2. Nonfinancial factors that Crossroad should consider include the following:

• Option 1 gives Crossroad immediate liquidity which it can use for other projects.

21-25

1. Cash flows for modernizing alternative:

Net Cash Initial Sale of Equip.

Year Units Sold Contributions Investments at Termination

(1) (2) (3) = (2) × $18,000a (4) (5)

Jan. 1, 2012 –– –– $(33,600,000) ––

21-26

2. Payback period calculations for modernizing alternative:

(1) (2) (3) (4)

Jan. 1, 2012 –– –– $33,600,000

Dec. 31, 2012 $ 9,936000 $ 9,936000 23,664000

Dec. 31, 2013 11,016000 20,952000 12,648000

21-27

3. Modernizing alternative:

Present Value

Discount Factors Net Cash Present

Year At 12% Flow Value

Jan. 1, 2012 1.000 $(33,600000) $(33,600,000)

4. Using the payback period, the modernize alternative is preferred to the replace

alternative. On the other hand, the replace alternative has a higher NPV than the modernize

alternative and so should be preferred. However, the NPV amounts are based on best estimates.

Chips.

21-28

21-28 (40 min.) Equipment replacement, income taxes (continuation of 21-27).

1. & 2. Income tax rate = 30%

Modernize Alternative

Annual depreciation:

$33,600000 7 years = $4800000 a year.

Income tax cash savings from annual depreciation deductions:

21-29

Replace alternative

Initial machine replacement = $58,800,000

Sale on Jan. 1, 2012, of equipment = $3,600,000

After-tax cash flow from sale of old equipment: $3,600,000 0.70 = $2,520,000

Net initial investment: $58,800,000 − $2,520,000 = $56,280,000

3. Pro Chips would prefer to:

a. have lower tax rates,

21-30

21-29 (20 min.) DCF, sensitivity analysis, no income taxes.

1. Revenues, $100 × 900,000 $90,000,000

Variable cash costs, $50 × 900,000 45,000,000

Cash contribution margin 45,000,000

Fixed cash costs 9,000,000

Cash inflow from operations $36,000,000

3. Sensitivity analysis enables management to see those assumptions for which input

variations have sizable impact on NPV. Extra resources could be devoted to getting more