13-1

CHAPTER 13

13-2 The five key forces to consider in industry analysis are: (a) competitors, (b) potential

13-3 Two generic strategies are (1) product differentiation, an organization’s ability to offer

products or services perceived by its customers to be superior and unique relative to the products

13-4 A customer preference map describes how different competitors perform across various

product attributes desired by customers, such as price, quality, customer service and product

features.

13-5 Reengineering is the fundamental rethinking and redesign of business processes to

13-6 The four key perspectives in the balanced scorecard are: (1) Financial perspective—this

perspective evaluates the profitability of the strategy and the creation of shareholder value, (2)

Customer perspective—this perspective identifies the targeted customer and market segments

13-7 A strategy map is a diagram that describes how an organization creates value by

1. It tells the story of a company’s strategy by articulating a sequence of cause-and-effect

relationships.

targets.

3. It places strong emphasis on financial objectives and measures in for-profit companies.

4. It limits the number of measures to only those that are critical to the implementation of

strategy.

13-2

5. It highlights suboptimal tradeoffs that managers may make when they fail to consider

operational and financial measures together.

1. Don’t assume the cause-and-effect linkages are precise; they are merely hypotheses. An

organization must gather evidence of these linkages over time.

3. Don’t use only objective measures in the balanced scorecard.

5. Don’t ignore nonfinancial measures when evaluating managers and employees.

1. The growth component which measures the change in operating income attributable

solely to the change in quantity of output sold from one year to the next.

next.

3. The productivity component which measures the change in costs attributable to a change

13-11 An analyst can incorporate other factors such as the growth in the overall market and

reductions in selling prices resulting from productivity gains into a strategic analysis of operating

13-12 Engineered costs result from a cause-and-effect relationship between the cost driver,

13-13 Downsizing (also called rightsizing) is an integrated approach configuring processes,

13-14 A partial productivity measure is the quantity of output produced divided by the quantity

of an individual input used (e.g., direct materials or direct manufacturing labor).

13-15 No. Total factor productivity (TFP) and partial productivity measures work best together

because the strengths of one offset weaknesses in the other. TFP measures are comprehensive,

13-3

13-16 (15 min.) Balanced scorecard.

1. Ridgecrest’s 2012 strategy is a cost leadership strategy. Ridgecrest plans to grow by

producing high-quality boxes at a low cost delivered to customers in a timely manner.

2. Solution Exhibit 13-16A shows the customer preference map for corrugated boxes for

Ridgecrest and Mesa on price, timeliness, quality and design.

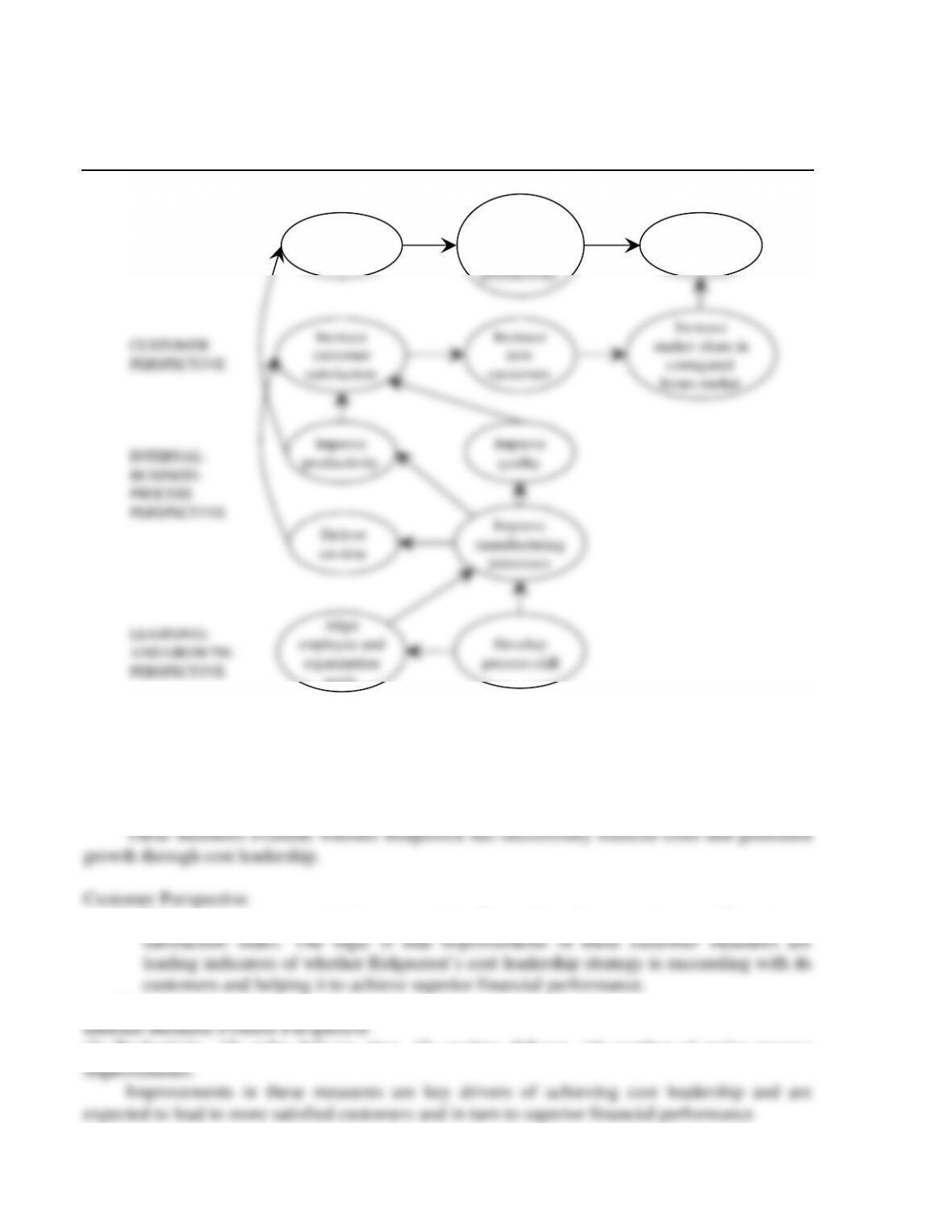

3. Solution Exhibit 13-16B presents the strategy map for Ridgecrest for 2012.

SOLUTION EXHIBIT 13-16B

Strategy Map for Ridgecrest for 2012

FINANCIAL

PERSPECTIVE

CUSTOMER

PERSPECTIVE

INTERNAL–

BUSINESS-

PROCESS

PERSPECTIVE

LEARNING-

AND GROWTH–

PERSPECTIVE

Reduce

Costs

Increase

operating

income from

productivity

Improve

manufacturing

processes

Develop

process skill

Increase

market share in

corrugated

boxes market

Grow

operating

income

Increase

customer

satisfaction

Increase

new

customers

Improve

productivity Improve

quality

Deliver

on–time

Align

employee and

organization

goals

4. Measures that we would expect to see on a Ridgecrest’s balanced scorecard for 2012 are

Financial Perspective

(1) Operating income from productivity gain, (2) operating income from growth, (3) cost

13-5

Learning and Growth Perspective

(1) Percentage of employees trained in process and quality management, (2) employee

satisfaction ratings.

1. Ridgecrest’s operating income gain is consistent with the cost leadership strategy

identified in requirement 1 of Exercise 13-16. The increase in operating income in 2012 was

2. The productivity component measures the change in costs attributable to a change in the

quantity and mix of inputs used in a year relative to the quantity and mix of inputs that would

have been used in a previous year to produce the current year output. It measures the amount by

which operating income increases and costs decrease through the productive use of input

13-6

13-18 (20 min.) Strategy, balanced scorecard, merchandising operation.

1. Roberto & Sons follows a product differentiation strategy. Roberto’s designs are

product.

2. Possible key elements of Roberto’s balance scorecard, given its product differentiation

strategy:

Financial Perspective

(1) Increase in operating income from charging higher margins, (2) price premium earned on

products.

(1) Market share in distinctive, name-brand T-shirts, (2) customer satisfaction, (3) new

customers, (4) number of mentions of Roberto’s T–shirts in the leading fashion magazines

(1) Quality of silk-screening (number of colors, use of glitter, durability of the design), (2)

frequency of new designs, (3) time between concept and delivery of design

(3) continuous education and skill levels of marketing and sales staff, (4) employee satisfaction.

Improvements in these measures are expected to improve Roberto’s capabilities to

1. Operating Income Statement

2010

2011

Revenues ($25

198,000; $26

246,700)

$4,950,000

$6,414,200

Costs

T-shirts purchased ($10

200,000; $8.50

250,000)

2,000,000

2,125,000

Administrative costs

1,200,000

1,162,500

Total costs

3,200,000

3,287,500

Operating income

$1,750,000

$3,126,700

Change in operating income

$1,376,700 F

2. The Growth Component

Revenue effect

of growth

=

Actual units of Actual units of

output sold output sold

in 2011 in 2010

−

×

Selling

price

in 2010

price

in 2010

13-8

The Price-Recovery Component

Revenue effect of

price-recovery

( )

Actual units

Selling price Selling price

= of output

in 2011 in 2010 sold in 2011

−

The Productivity Component

Cost effect of

productivity for

variable costs

=

Actual units of Units of input

input used required to

to produce produce 2011

2011 output ouput in 2010

−

Input

price

in 2011

Cost effect of

Actual Actual units of capacity in

units of 2010 because adequate

Price per

unit of

Income

Statement

Amounts

in 2010

(1)

Revenue and

Cost Effects

of Growth

in 2011

(2)

Revenue and

Cost Effects of

Price-Recovery

in 2011

(3)

Cost Effect

of

Productivity

in 2011

(4)

Income

Statement

Amounts

in 2011

(5) =

(1) + (2) + (3) + (4)

Revenues

$4,950,000

$1,217,500 F

$246,700 F

−−

$6,414,200

Costs

3,200,000

491,920 U

333,788 F

$70,632 F

3,287,500

Operating income

$1,750,000

$ 725,580 F

$580,488 F

$70,632 F

$3,126,700

$1,376,700 F

Change in operating income

3. The analysis of operating income indicates that growth, price-recovery, and productivity

all resulted in favorable changes in operating income in 2011. Further, a significant amount of

13-10

13-20 (20 min.) Analysis of growth, price-recovery, and productivity components

(continuation of 13-19).

Effect of the industry–market-size factor on operating income

Of the 48,700-unit (246,700 – 198,000) increase in sales between 2010 and 2011, 19,800

(10% 198,000) units are due to growth in market size, and 28,900 units are due to an increase

700,48

Change in operating income due to product differentiation $1,011,068 F

Effect of cost leadership on operating income

The change in operating income from cost leadership is:

Productivity component $ 70,632 F

The change in operating income between 2010 and 2011 can be summarized as follows: