6-31

6-36 (30 min.) Cash budgeting, chapter appendix.

1. Projected Sales

May

June

July

August

September

October

Sales in units

80

120

200

100

60

40

Revenues (Sales in units × $450)

$36,000

$54,000

$90,000

$45,000

$27,000

Collections of Receivables

May

June

July

August

September

October

From sales in:

May (30% $36,000)

$10,800

June (50%; 30% $54,000)

27,000

$16,200

July (20%; 50%; 30% $90,000)

18,000

45,000

$ 27,000

August (20%; 50% $45,000)

9,000

22,500

September (20% $27,000)

5,400

Total

$55,800

$70,200

$54,900

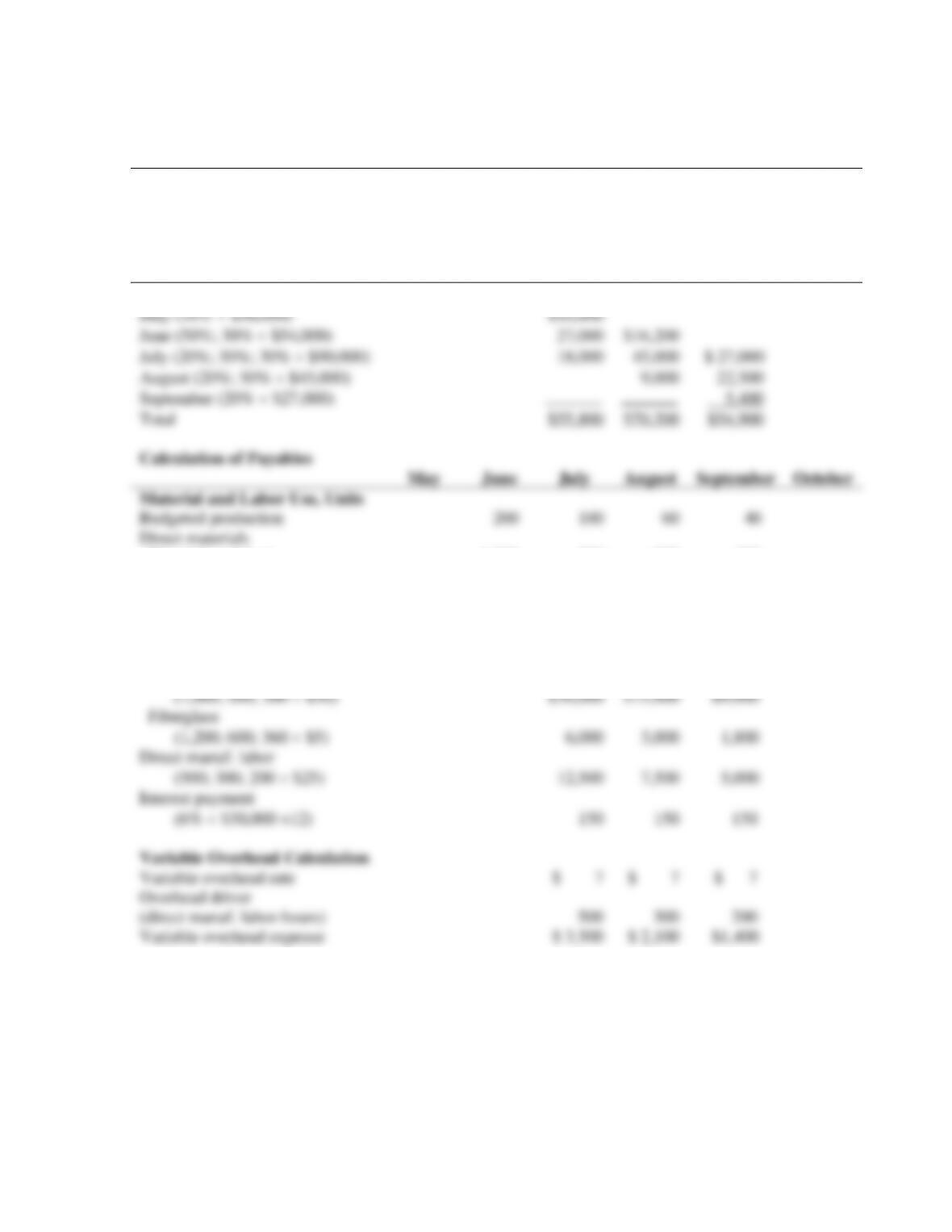

Calculation of Payables

May

June

July

August

September

October

Material and Labor Use, Units

Budgeted production

200

100

60

40

Direct materials

Wood (board feet)

1,000

500

300

200

Fiberglass (yards)

1,200

600

360

240

Direct manuf. labor (hours)

1,000

500

300

200

Disbursement of Payments

Direct materials

Wood

(1,000; 500; 300 $30)

$30,000

$15,000

$9,000

Fiberglass

(1,200; 600; 360 $5)

6,000

3,000

1,800

Direct manuf. labor

(500; 300; 200 $25)

12,500

7,500

5,000

Interest payment

(6% $30,000 ÷12)

150

150

150

Variable Overhead Calculation

Variable overhead rate

$ 7

$ 7

$ 7

Overhead driver

(direct manuf. labor-hours)

500

300

200

Variable overhead expense

$ 3,500

$ 2,100

$1,400

6-32

Cash Budget for the months of July, August, September 2012

July

August

September

Beginning cash balance

$10,000

$ 5,650

$40,100

Add receipts: Collection of receivables

55,800

70,200

54,900

Total cash available

$65,800

$75,850

$95,000

Deduct disbursements:

Material purchases

$36,000

$18,000

$10,800

Direct manufacturing labor

12,500

7,500

5,000

Variable costs

3,500

2,100

1,400

Fixed costs

8,000

8,000

8,000

Interest payments

150

150

150

Total disbursements

60,150

35,750

25,350

Ending cash balance

$ 5,650

$40,100

$69,650

3. No. Slopes does not maintain a $10,000 minimum cash balance in July. To maintain a

bank.

6-33

6-37 (40–50 min.) Cash budgeting.

Itami Wholesale Co.

Statement of Budgeted Cash Receipts and Disbursements

For the Months of December 2011 and January 2012

December 2011

January 2012

Cash balance, beginning

$ 88,000

$ 18,470

Add receipts:

Collections of receivables (Schedule 1)

295,250

265,050

(a) Total cash available for needs

383,250

283,520

Deduct disbursements:

For merchandise purchases (Schedule 2)

$291,280

$223,040

For variable costs (Schedule 3)

66,000

50,000

For fixed costs (Schedule 3)

7,500

7,500

(b) Total disbursements

364,780

280,540

Cash balance, end of month (a – b)

$ 18,470

$ 2,980

Under the current projections, the cash balance as of January 31, 2012, is $2,980, which is not

sufficient to enable repayment of the $100,000 note.

Schedule 1: Collections of Receivables

Collections in Oct. Sales Nov. Sales Dec. Sales Jan. Sales Total

December $39,200a $96,000b $160,050c —- $295,250

January $44,800d $ 99,000e $121,250f $265,050

a 0.14 × $280,000 b 0.30 × $320,000 c 0.50 × $330,000 × .97

d 0.14 × $320,000 e 0.30 × $330,000 f 0.50 × $250,000 × .97

6-34

Schedule 2: Payments for Merchandise

December January

Target ending inventory (in units) 750a 740c

Add units sold (sales ÷ $100) 3,300 2,500

Total requirements 4,050 3,240

6-38 (60 min.) Comprehensive problem; ABC manufacturing, two products.

1.

Revenues Budget

For the Year Ending December 31, 2011

Units

Selling

Price

Total Revenues

Combs

12,000

$ 6

$72,000

Brushes

14.000

$20

$280,000

Total

$352,000

2a. Total budgeted marketing costs = Budgeted variable marketing costs + Budgeted fixed

marketing costs

= $14,100 + $60,000 = $74,100

12,000

14,000

13,200

15,400

12,600

6-36

4a.

Combs

Brushes

Total

Machine setup overhead

Units to be produced

12,600

14,200

Units per batch

÷200

÷100

Number of setups

63

142

Hours to setup per batch

×1/3

×1

Total setup hours

21

142

163

Total budgeted setup costs = Budgeted variable setup costs + Budgeted fixed setup costs

= $6,830 + $11,100 = $17,930

Machine setup

allocation rate

= $17,930 / 163 setup hours = $110 per setup hour

b.

Combs:

12,600 units × .025 MH per unit

315 MH

Brushes:

14,200 units × 0.1 MH per unit

1,420 MH

Total

1,735 MH

5.

Direct Material Usage Budget in Quantity and Dollars

For the Year Ending December 31, 2011

Material

Plastic

Bristles

Total

Physical Units Budget

Direct materials required for

Combs (12,600 units × 5 oz and 0 bunches)

63,000 oz.

Brushes (14,200 units × 8 oz and 16 bunches)

113,600 oz.

227,200 bunches

Total quantity of direct materials to be used

176,600 oz.

227,200 bunches

6-37

Cost Budget

Available from beginning direct materials inventory

(under a FIFO cost-flow assumption)

$ 304

$ 946

To be purchased this period

Plastic: (176,600 oz. ─ 1,600 oz) × $0.20 per oz.

35,000

Bristles: (227,200 bunches ─ 1,820) × $0.5 per bunch

______

112,690

Direct materials to be used this period

$35,304

$ 113,636

$148,940

Direct Materials Purchases Budget

For the Year Ending December 31, 2011

Material

Plastic

Bristles

Total

Physical Units Budget

To be used in production (requirement 5)

176,600 oz.

227,200 bunches

Add: Target ending direct material inventory

1,766

2,272

Total requirements

178,366 oz.

229,472 bunches

Deduct: Beginning direct material inventory

1,600 oz.

1,820 bunches

Purchases to be made

176,766 oz.

227,652 bunches

Cost Budget

Plastic: 176,766 oz.

$0.20 per oz

$ 35,353

Bristles : 227,652 bunches

$0.5 per bunch

_______

$ 113,826

Purchases

$ 35,353

$ 113,826

$149,179

Total budgeted materials handling costs = Budgeted variable

Materials handling costs + Budgeted fixed materials handling

costs

allocation rate

7.

Direct Manufacturing Labor Costs Budget

For the Year Ending December 31, 2011

Output Units

Direct Manufacturing

Total

Hourly Wage

Total

Produced

Labor-Hours per Unit

Hours

Rate

Combs

12,600

0.05

630

$12

$ 7,560

Brushes

14,200

0.2

2,840

12

34,080

Total

$41,640

6-38

8.

Manufacturing Overhead Cost Budget

For the Year Ending December 31, 2011

Variable

Fixed

Total

Materials handling

$ 11,490

$ 15,000

$ 26,490

Machine setup

6,830

11,100

17,930

Processing

7,760

20,000

27,760

Inspection

7,000

1,040

8,040

TOTALS $ 33,080 $ 47,140 $ 80,220

6-39

9.

Unit Costs of Ending Finished Goods Inventory

For the Year Ending December 31, 2011

Combs

Brushes

Cost per

Input per

Input per

Unit of

Input

Unit of

Output

Total

Unit of

Output

Total

Plastic

$0.20

5 oz.

$1.00

8 oz

$ 1.60

Bristles

0.50

─

─

16 bunches

8.00

Direct manufacturing labor

12

.05 hrs.

0.60

0.2 hour

2.40

Materials handling

0.15

5 oz.

0.75

8 oz

1.20

Machine setup

110

0.00167 hrs.1

0.18

0.01 setup-hr1

1.10

Processing

16

.025 MH

0.40

0.1 MH

1.60

Inspection

0.30

1 unit

0.30

1 unit

0.30

Totals

$3.23

$16.20

1 21 setup–hours ÷ 12,600 units = 0.00167 hours per unit; 142 setup hours ÷ 14,200 units = 0.01 hours per unit

Ending Inventories Budget

December 31, 2011

Quantity

Cost per unit

Total

Direct Materials

Plastic

1,766 oz

$0.20

$353.20

Bristles

2,272 bunches

0.50

1,136.00

$1,489.20

Finished goods

Combs

1,200

$3.23

$3,876.00

Brushes

1,400

16.20

22,680.00

26,556.00

Total ending inventory

$28,045.20

10.

Cost of Goods Sold Budget

For the Year Ending December 31, 2011

Beginning finished goods inventory, Jan. 1 ($1,800 + $18,120)

$ 19,920

Direct materials used (requirement 5)

$148,940

Direct manufacturing labor (requirement 7)

41,640

Manufacturing overhead (requirement 8)

80,220

Cost of goods manufactured

270,800

Cost of goods available for sale

290,720

Deduct: Ending finished goods inventory, December 31 (reqmt. 9)

26,556

Cost of goods sold

$264,164