20-11

1.

(a). Record purchases of direct

materials

Inventory Control

Accounts Payable Control

2,754,000

2,754,000

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

723,600

Wages Payable Control)

723,600

(c) Record cost of good

finished units completed

No entry

(d) Record cost of finished

goods sold

Cost of Goods Solda

Inventory Controla

3,432,000

2,692,800

Conversion Costs Allocateda

739,200

(e) Record underallocated or over-

allocated conversion costs

Conversion Costs Allocated

Costs of Goods Sold

739,200

15,600

Conversion Costs Control

723,600

a26,400 × ($102 + $28) = $3,432,000; 26,400 × $102 = $2,692,800; 26,400 × $28 = $739,200

2.

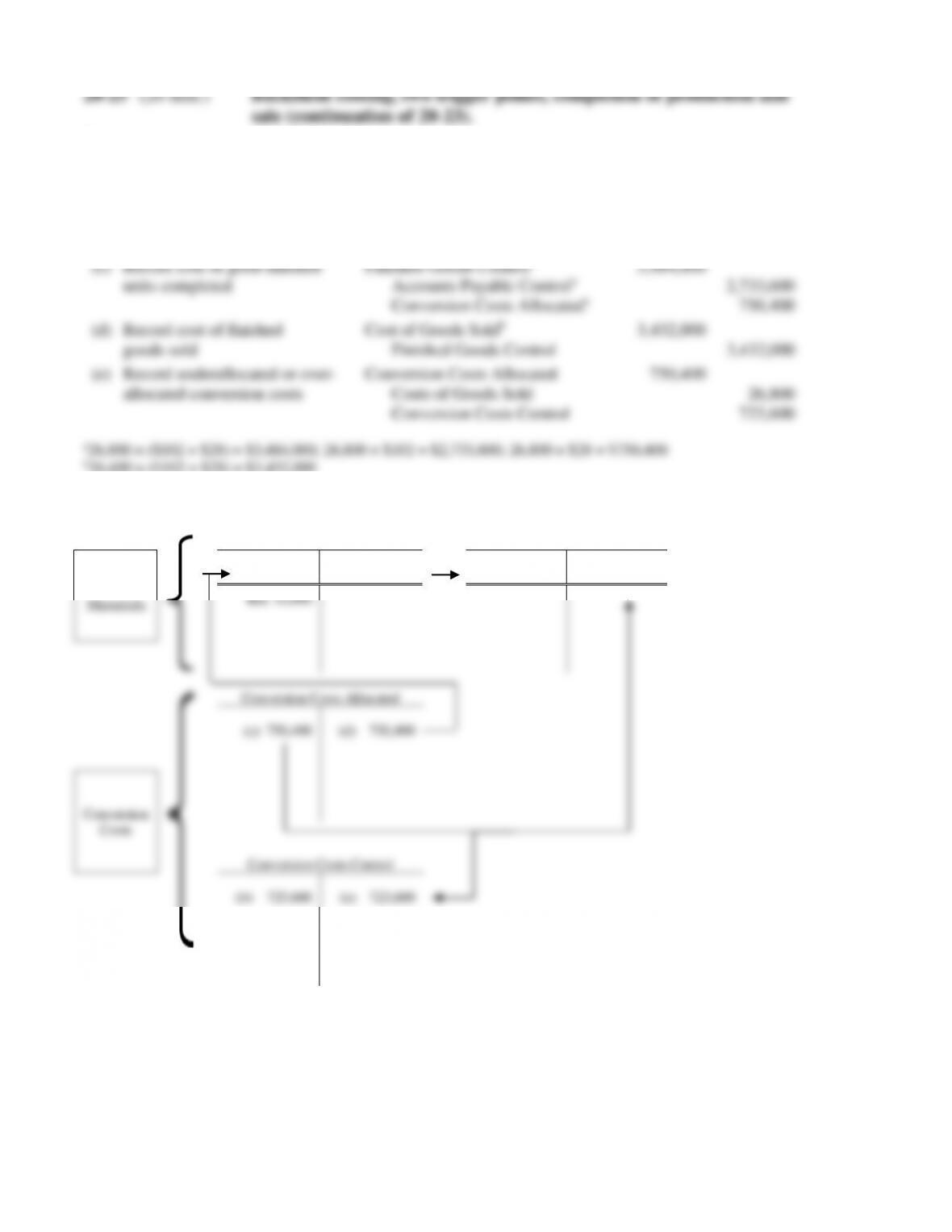

Inventory Control

Cost of Goods Sold

Direct

Materials

(a) 2,754,000

(d) 2,692,800

(d) 3,432,000

(e) 15,600

Bal. 61,200

Bal. 52,000

Conversion Costs Allocated

(e) 739,200

(d) 739,200

Conversion

Costs

Conversion Costs Control

(b) 723,600

(e) 723,600

20-12

1.

(a). Record purchases of direct

materials

No Entry

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

723,600

Wages Payable Control)

723,600

(c) Record cost of good finished

units completed

Finished Goods Controla

Accounts Payable Controla

3,484,000

2,733,600

Conversion Costs Allocateda

750,400

(d) Record cost of finished

goods sold

Cost of Goods Soldb

Finished Goods Control

3,432,000

3,432,000

(e) Record underallocated or over-

allocated conversion costs

Conversion Costs Allocated

Costs of Goods Sold

750,400

26,800

Conversion Costs Control

723,600

2.

Finished Goods Control

Cost of Goods Sold

Direct

Materials

(a) 3,484,000

(d) 3,432,800

(d) 3,432,000

(e) 26,800

Bal. 52,000

Conversion Costs Allocated

(e) 750,400

(d) 750,400

Conversion

Costs

Conversion Costs Control

(b) 723,600

(e) 723,600

1.

Scenario

1

2

3

4

5

Demand (units) (D)

380,000

380,000

380,000

380,000

380,000

Cost per purchase order (P)

$ 57.00

$ 57.00

$ 57.00

$ 57.00

$ 57.00

Annual carrying cost per package (C)

$ 12.00

$ 12.00

$ 12.00

$ 12.00

$ 12.00

Order quantity per purchase order (units) (Q)

760

1,000

1,900

3,800

4,750

Number of purchase orders per year (D

Q)

500

380

200

100

80

Annual ordering costs (D

Q)

P

$28,500

$21,660

$11,400

$ 5,700

$ 4,560

Annual carrying costs (QC

2)

$ 4,560

$ 6,000

$11,400

$22,800

$28,500

Total relevant costs of ordering and carrying inventory

$33,060

$27,660

$22,800

$28,500

$33,060

2. When the ordering cost per purchase order is reduced to $30:

EOQ =

2 380,000 $30 1,378.4 packages (or 1,378 packages)

$12

=

The EOQ drops from 1,900 packages to 1,378 packages when Soothing Meadow’s ordering cost

3. As summarized below, the new Mona Lisa web-based ordering system, by lowering the

EOQ to 1,378 packages, will lower the carrying and ordering costs by $6,260. Soothing Meadow

20-27 (30 min.) EOQ, uncertainty, safety stock, reorder point.

2 DP 2 120,000 $250

2. Weekly demand = Monthly demand ÷ 4

3. Solution Exhibit 20-27 presents the safety stock computations for Warehouse OR2 when

the reorder point excluding safety stock is 2,500 pairs of shoes. The exhibit shows that annual

relevant total stockout and carrying costs are the lowest ($1,080) when a safety stock of 250

20-15

1. Under a MRP system:

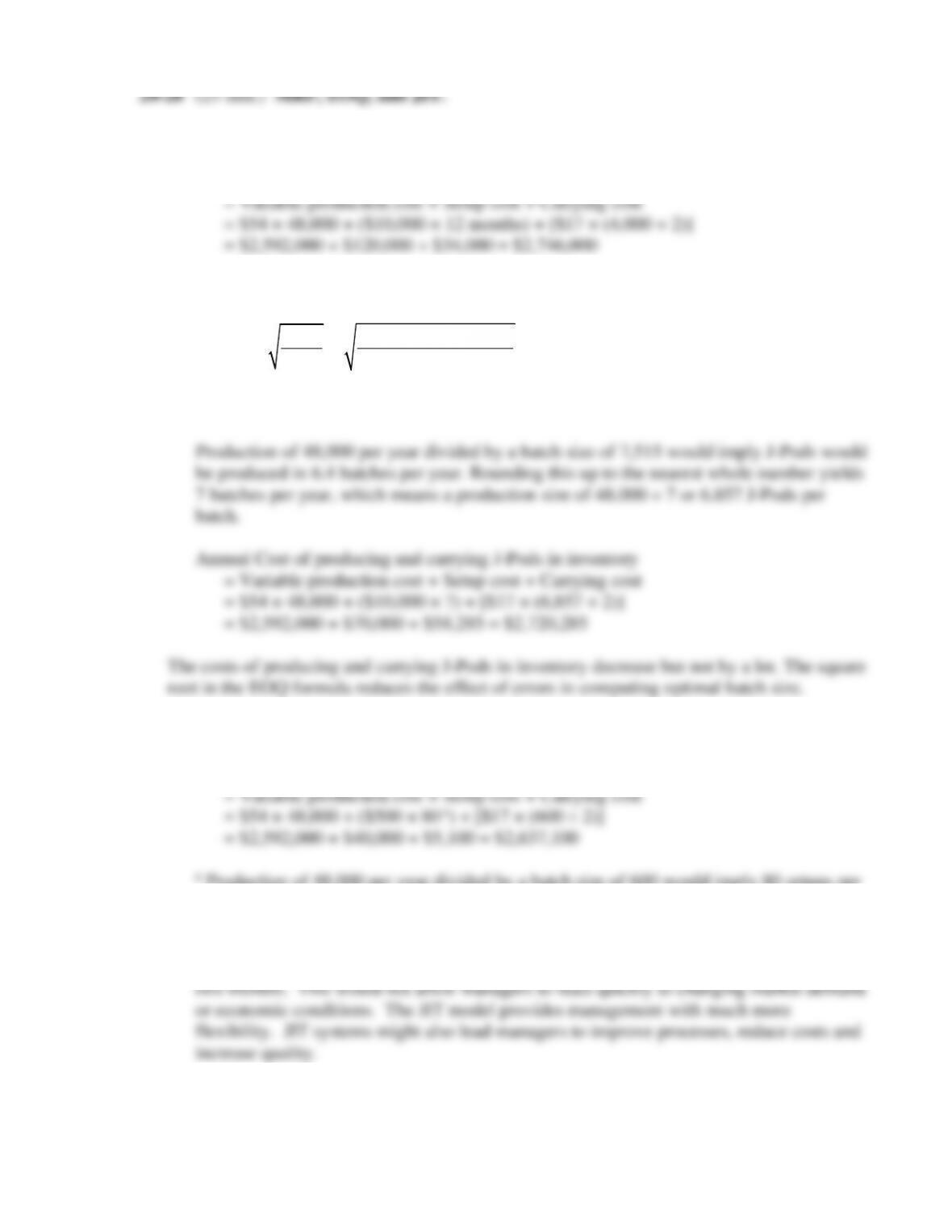

Annual cost of producing and carrying J-Pods in inventory

2. Using an EOQ model to determine batch size:

2 48,000 $10,000

2 DP

EOQ C $17

==

= 7,515 J-Pods per batch

3. Under a JIT system

Annual Cost of producing and carrying J-Pods in inventory

year.

4. The JIT model resulted in the lowest costs because set up and carrying costs were lower

than for the EOQ model. The EOQ model also limits production to almost once every

20-29 (30 min.) Effect of management evaluation criteria on EOQ model.

2 DP 2 500,000 $800

2. Number of orders per year =

D 500,000

EOQ 4,000

=

= 125 orders

Total relevant

=

ordering costs

D P

Q

=

500,000 $800

4,000

= $100,000

=

Total relevant

Q C

4,000 $50

carrying costs

2 DP 2 500,000 $800

D P

Q

500,000 $800

5,164

Q C

20-17

20-30 (30 min.) JIT purchasing, relevant benefits, relevant costs.

2. Conditions that should exist in order for a company to successfully adopt just-in-time

purchasing include the following:

• Top management must be committed and provide the necessary leadership support to

ensure a company-wide, coordinated effort.