23-11

1. Bleefl would be better off if the machine is replaced. Its cost of capital is 6% and the IRR of

the investment is 11%, indicating that this is a positive net present value project.

2. The ROIs for the first five years are:

Year 1

Year 2

Year 3

Year 4

Year 5

Operating income1

$2,000

$2,000

$2,000

$2,000

$2,000

End of year net assets

27,000

24,000

21,000

18,000

15,000

Average net assets

28,5002

25,500

22,500

19,500

16,500

ROI

7.02%

7.84%

8.89%

10.26%

12.12%

1Income is cash savings of $5,000 less $3,000 annual depreciation expense.

3. Bleefl could use long term rather than short term ROI, or use ROI and some other long term

measures to evaluate the Patio Furniture division to create goal congruence. Evaluating the

23-12

23-22 (25 min.) ROI, RI, EVA®.

1. The required division ROIs using total assets as a measure of investment is shown in the

row labeled (1) in Solution Exhibit 23-22.

SOLUTION EXHIBIT 23-22

New Car

Division

Performance

Parts Division

Total assets

$33,000,000

$28,500,000

Current liabilities

$6,600,000

$8,400,000

Operating income

$2,475,000

$2,565,000

Required rate of return

12%

12%

Total assets – current liabilities

$26,400,000

$20,100,000

(1)

ROI (based on total assets)

($2,475,000

$33,000,000; $2,565,000

$28,500,000)

7.5%

9.0%

(2)

RI (based on total assets – current liabilities)

($2,475,000 – (12%

$26,400,000); $2,565,000 –

(12%

$20,100,000))

($693,000)

$153,000

(3)

RI (based on total assets) ($2,475,000 – (12%

$33,000,000); $2,565,000 – (12%

$28,500,000))

($1,485,000)

($855,000)

2. The required division RIs using total assets minus current liabilities as a measure of

investment is shown in the row labeled (2) in the table above.

3. The row labeled (3) in the table above shows division RIs using assets as a measure of

assets.

4. After-tax cost of debt financing = (1– 0.4) 10% = 6%

After-tax cost of equity financing = 15%

Weighted average

($18,000,000 6%) + ($12,000,000 15%)

0.6 operating income before tax $ 1,485,000 $1,539,000

9.6% Investment

5. Both the residual income and the EVA calculations indicate that the Performance Parts

Division is performing nominally better than the New Car Division. The Performance Parts

23-13

23-23 (25–30 min.) ROI, RI, measurement of assets.

The method for computing profitability preferred by each manager follows:

Manager of

Method Chosen

Radnor

Easttown

Marion

RI based on net book value

RI based on gross book value

ROI based on either gross or net book value

Supporting Calculations:

ROI Calculations

Division

Value Book Gross

Income Operating

*Value BookNet

Income Operating

Radnor

Easttown

Marion

$142,050 ÷ $1,200,000 = 11.84% (3)

$137,550 ÷ $1,140,000 = 12.07% (2)

$ 92,100 ÷ $ 750,000 = 12.28% (1)

$142,050 ÷ $555,000 = 25.59% (3)

$137,550 ÷ $525,000 = 26.20% (2)

$ 92,100 ÷ $330,000 = 27.91% (1)

RI Calculations

Division

Operating Income – 10% Gross BV

Operating Income – 10% Net BV1

Radnor

Easttown

Marion

$142,050 – $120,000 = $22,050 (2)

$137,550 – $114,000 = $23,550 (1)

$ 92,100 – $ 75,000 = $17,100 (3)

$142,050 – $55,500 = $86,550 (1)

$137,550 – $52,500 = $85,050 (2)

$ 92,100 – $33,000 = $59,100 (3)

1Net book value is gross book value minus accumulated depreciation.

The biggest weakness of ROI is the tendency to reject projects that will lower historical ROI

even though the prospective ROI exceeds the required ROI. RI achieves goal congruence

because subunits will make investments as long as they earn a rate in excess of the required

return for investments. The biggest weakness of RI is that it favors larger divisions in ranking

performance. The greater the amount of the investment (the size of the division), the more likely

that larger divisions will be favored assuming that income grows proportionately. The strength of

ROI is that it is a ratio and so does not favor larger divisions. In general, though, achieving goal

congruence is very important. Therefore, the RI measure is often preferred to ROI.

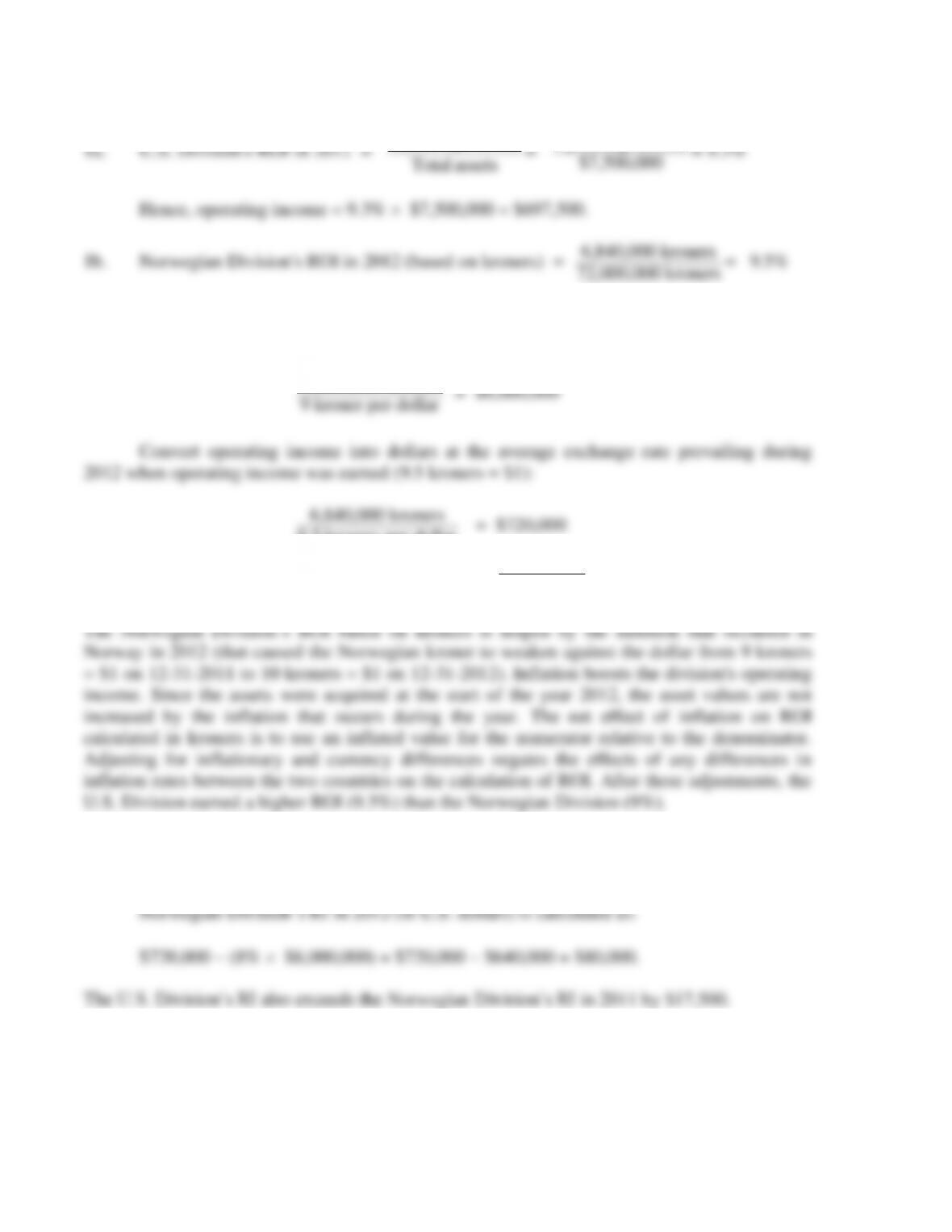

23-24 (20 min.) Multinational performance measurement, ROI, RI.

income Operating

Operating income

23-15

23-25 (20 min.) ROI, RI, EVA and Performance Evaluation.

1. ROI and residual income:

Clothing

Cosmetics

Operating income after tax

$ 600,000

$ 1,600,000

Net assets

$3,000,000

$10,000,000

ROI

($600,000 ÷ $3,000,000; $1,600,000 ÷ $10,000,000)

20.00%

16.00%

RI

($600,000 − 10% × 3,000,000; $1,600,000− 10% × $10,000,000)

$ 300,000

$ 600,000

2.

Clothing

Cosmetics

Adjusted operating income

$ 720,000

$1,430,000

Net assets less current liabilities

$2,600,000

$9,800,000

Revised ROI

($720,000 ÷ $2,600,000; $1,430,000 ÷ 9,800,000)

27.69%

14.59%

EVA

($720,000 − 10% × $2,600,000; $1,430,000 − 10% × $9,800,000)

$ 460,000

$ 450,000

3. Since this is a manufacturing firm, there are a variety of non-financial performance measures

23-16

23-26 (20–30 min.) Risk sharing, incentives, benchmarking, multiple tasks.

1. An evaluation of the three proposals to compensate Marks, the general manager of the

Dexter Division follows:

(i) Paying Marks a flat salary will not subject Marks to any risk, but it will provide no

incentives for Marks to undertake extra physical and mental effort.

(ii) Rewarding Marks only on the basis of Dexter Division’s ROI would motivate Marks to

2. Marks’s complaint does not appear to be valid. The senior management of AMCO is

proposing to benchmark Marks’s performance using a relative performance evaluation (RPE)

system. RPE controls for common uncontrollable factors that similarly affect the performance of

managers operating in the same environments (for example, the same industry). If business

23-17

3. Superior performance measures change significantly with the manager’s performance and

not very much with changes in factors that are beyond the manager’s control. If Marks has no

authority for making capital investment decisions, then ROI is not a good measure of Marks’s

performance––it varies with the actions taken by others rather than the actions taken by Marks.

4. There are three main concerns with Marks’s plans. First, creating very strong sales

incentives imposes excessive risk on the sales force because a salesperson’s performance is

affected not only by his or her own effort, but also by random factors (such as a recession in the

industry) that are beyond the salesperson’s control. If salespersons are risk averse, the firm will

23-18

1. RI =Operating income – (WACC x Assets)

2. EVA = Adjusted operating income – (WACC x (Total assets – Current liabilities))

Operating income is adjusted as follows:

Operating income $ 630,000

Add back this period’s advertising expense 90,000

3. The differences between the RI and EVA results are due to two factors in this problem: the

definition of capital and the treatment of advertising. EVA subtracts current liabilities from total

assets when computing capital. Since some types of current liabilities represent sources of “free”

23-19

1. ROI using historical cost measures:

Passion Fruit $260,000 ÷ $ 680,000 = 38.24%

2. The gross book values (i.e., the original costs of the plants) under historical cost are

calculated as the useful life of each plant (12 years) the annual depreciation:

Passion Fruit 12 $140,000 = $1,680,000

Kiwi Fruit 12 $200,000 = $2,400,000

Mango Fruit 12 $240,000 = $2,880,000

23-20

Step 4: Compute current-cost depreciation expense in 2011 dollars.

Gross book value of long-term assets at current cost at the end of 2011 (from Step 1) ÷ 12

Passion Fruit $2,856,000 ÷ 12 = $238,000

Kiwi Fruit $3,000,000 ÷ 12 = $250,000

Mango Fruit $3,060,000 ÷ 12 = $255,000

3. Use of current costs increases the comparability of ROI measures across divisions’