2-1

2-1 A cost object is anything for which a separate measurement of costs is desired. Examples

2-2 Direct costs of a cost object are related to the particular cost object and can be traced to

that cost object in an economically feasible (cost-effective) way.

2-3 Managers believe that direct costs that are traced to a particular cost object are more

2-4 Factors affecting the classification of a cost as direct or indirect include

2-5 A variable cost changes in total in proportion to changes in the related level of total

activity or volume. An example is a sales commission that is a percentage of each sales revenue

dollar.

2-6 A cost driver is a variable, such as the level of activity or volume, that causally affects

2-7 The relevant range is the band of normal activity level or volume in which there is a

2-8 A unit cost is computed by dividing some amount of total costs (the numerator) by the

related number of units (the denominator). In many cases, the numerator will include a fixed cost

2-2

2-9 Manufacturing-sector companies purchase materials and Ashtonnents and convert them

into various finished goods, for example automotive and textile companies.

1. Direct materials inventory. Direct materials in stock and awaiting use in the

manufacturing process.

3. Finished goods inventory. Goods completed but not yet sold.

2-11 Inventoriable costs are all costs of a product that are considered as assets in the balance

sheet when they are incurred and that become cost of goods sold when the product is sold. These

2-12 Direct material costs are the acquisition costs of all materials that eventually become part

of the cost object (work in process and then finished goods), and can be traced to the cost object

in an economically feasible way.

2-13 Overtime premium is the wage rate paid to workers (for both direct labor and indirect

labor) in excess of their straight-time wage rates.

2-14 A product cost is the sum of the costs assigned to a product for a specific purpose.

Purposes for computing a product cost include

2-3

2-15 Three common features of cost accounting and cost management are:

2-16 (15 min.) Computing and interpreting manufacturing unit costs.

1.

(in millions)

Supreme Deluxe Regular Total

(0.30

$16; 26; 8) 4.80 7.80 2.40 15.00

Variable costs $148.20 $153.20 $89.60 $391.00

Units produced (millions) 125 150 140

2. Based on total manuf. cost

per unit ($1.2240

150;

$1.0733

190; $0.6571

220) $183.60 $203.93 $144.56 $532.09

Correct total manuf. costs based

2-4

2-17 (15 min.) Direct, indirect, fixed and variable costs.

1. Yeast – direct, variable

Flour- direct, variable

Packaging materials –direct (or could be indirect if small and not traced to each unit), variable

Depreciation on ovens –indirect, fixed (unless “units of output” depreciation, which then

would be variable)

2. If the cost object is Mixing Department, then anything directly associated with the Mixing

Department will be a direct cost. This will include:

• Depreciation on mixing machines

2-18 (15–20 min.) Classification of costs, service sector.

Cost object: Each individual focus group

Cost variability: With respect to the number of focus groups

2-6

2-20 (15–20 min.) Classification of costs, manufacturing sector.

Cost object: Type of car assembled (Corolla or Geo Prism)

Cost Item

D or I

V or F

A

D

V

B

I

F

C

D

F

D

D

F

E

D

V

F

I

V

G

D

V

H

I

F

1.

Minutes/month

0

50

100

150

200

240

300

327.5

350

400

450

510

540

600

650

Plan A ($/month)

0

5

10

15

20

24

30

32.75

35

40

45

51

54

60

65

Plan B ($/month)

15

15

15

15

15

15

19.80

22

23.80

27.80

31.80

36.60

39

43.80

47.80

Plan C ($/month)

22

22

22

22

22

22

22

22

22

22

22

22

23.50

26.50

29

0

10

20

30

40

50

60

0100 200 300 400 500 600

Total Cost

Number of long-distance minutes

Plan A

Plan B

Plan C

2. In each region, Ashton chooses the plan that has the lowest cost. From the graph (or from

calculations)*, we can see that if Ashton expects to use 0–150 minutes of long-distance each

$0.10x = $15

$0.08 (y – 240) = $22 – $15 = $7

$7 87.5

2-7

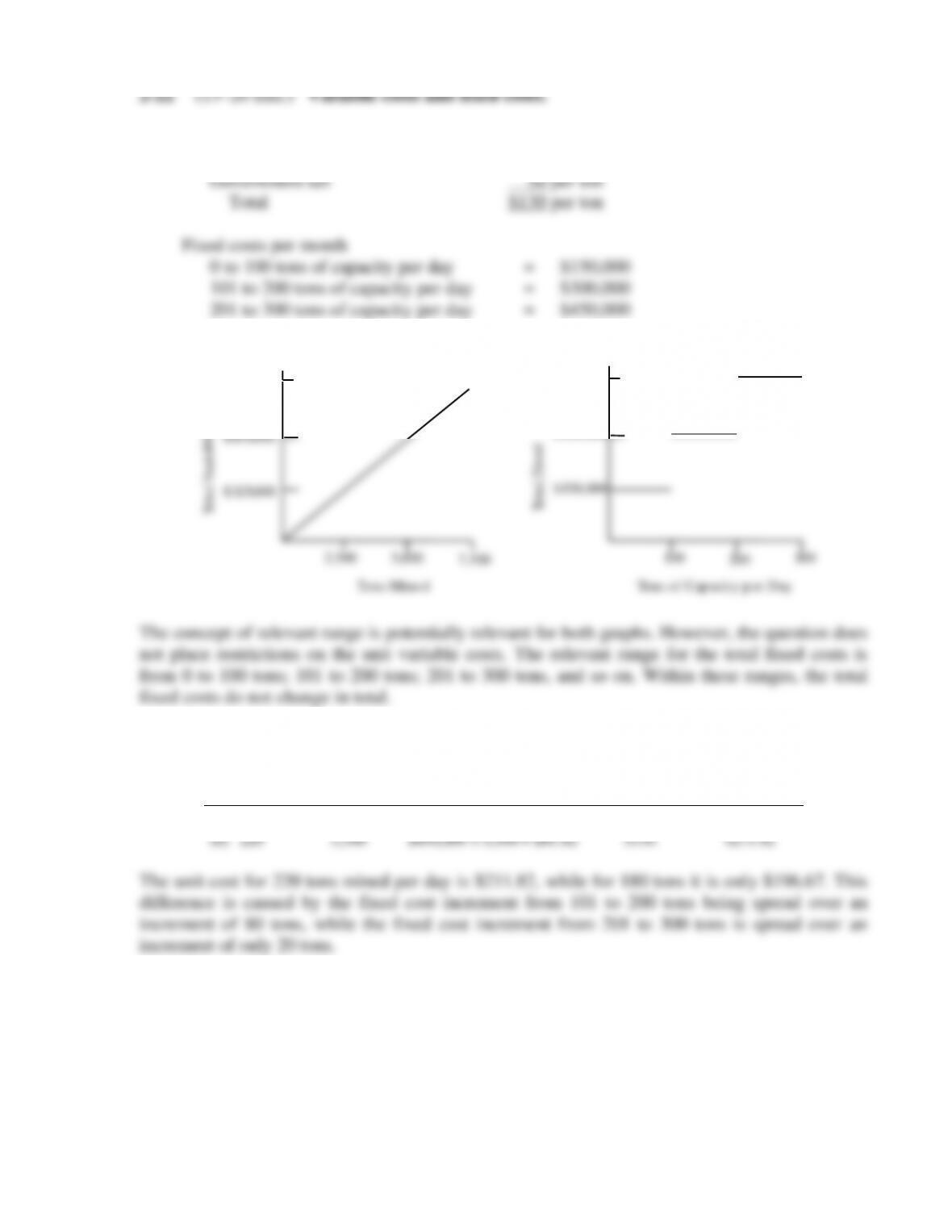

1. Variable cost per ton of beach sand mined

Subcontractor $ 80 per ton

2.

T

o

t

a

l

F

i

x

e

d

C

o

s

ts

$

4

5

0

,

0

0

0

$

3

0

0

,

0

0

0

$

1

5

0

,

0

0

0

1

0

0

2

0

0

3

0

0

T

o

n

s

o

f

C

a

p

a

c

i

t

y

p

e

r

D

a

y

$

9

7

5

,

0

0

0

$

6

5

0

,

0

0

0

$

3

2

5

,

0

0

0

2

,

5

0

0

5

,

0

0

0

7

,

5

0

0

T

o

n

s

M

i

n

e

d

T

o

t

a

l

V

a

r

i

a

b

l

e

C

o

s

ts

3.

Tons Mined

per Day

Tons Mined

per Month

Fixed Unit

Cost per Ton

Variable Unit

Cost per Ton

Total Unit

Cost per Ton

(1)

(2) = (1) × 25

(3) = FC ÷ (2)

(4)

(5) = (3) + (4)

(a) 180

4,500

$300,000 ÷ 4,500 = $66.67

$130

$196.67

(b) 220

5,500

$450,000 ÷ 5,500 = $81.82

$130

$211.82

The unit cost for 220 tons mined per day is $211.82, while for 180 tons it is only $196.67. This

difference is caused by the fixed cost increment from 101 to 200 tons being spread over an

increment of 80 tons, while the fixed cost increment from 201 to 300 tons is spread over an

increment of only 20 tons.

2-8

2-23 (20 min.) Variable costs, fixed costs, relevant range.

2. Current annual fixed manufacturing costs within the relevant range are $1,200 × 12 =

3. If demand changes from 3,800 to 7,600 jaw breakers per month, or from 3,800 × 12 =

45,600 to 7,600 × 12 = 91,200 jaw breakers per year, Sweetum will need a second machine.

Assuming Sweetum buys a second machine identical to the first machine, it will increase

capacity from 4,100 jaw breakers per month to 8,200. The annual relevant range will be between

2-9

1. Identify customer needs (what do smartphone users want?) — Design of products and

processes

Perform market research on competing brands — Design of products and processes

Design a prototype of the HCP smartphone — Design of products and processes

2.

Value Chain

Category

Activity

Cost driver

Design of

products and

processes

Identify customer needs

Number of surveys returned and processed

from competing smartphone users

Perform market research on

competing brands

Hours spent researching competing market

brands

Number of surveys returned and processed

from competing smartphone users

Design a prototype of the HCP

smartphone

Engineering hours spent on initial product

design

Make design changes to the

smartphone based on

customer feedback

Number of design changes

Production

Manufacture the HCP

smartphones

Machine hours required to run the

production equipment

Package the HCP smartphones

Number of smartphones shipped by HCP

Marketing

Market the new design to cell

phone companies

Number of cell phone companies purchasing

the HCP smartphone

Distribution

Process orders from cell phone

companies

Number of smartphone orders processed

Number of deliveries made to cell phone

companies

Deliver the HCP smartphones

to cell phone companies

Number of deliveries made to cell phone

companies

Customer

Service

Provide on–line assistance to

cell phone users for use of

the HCP smartphone

Number of smartphones shipped by HCP

Customer Service hours

2-10

1.

Function

Representative Cost Driver

2. Human Resources Number of employees

4. Research and development Number of research scientists

6. Distribution Number of deliveries made

2.

Function

Representative Cost Driver

2. Human Resources Salaries and wages of employees

4. Research and Development Number of new products being developed

6. Distribution Distance traveled to make deliveries