17-40

The FIFO ending inventory is higher than the weighted-average ending inventory by

$3,750. This is because FIFO assumes that all the lower-cost prior-period units in work in

process (resulting from the lower transferred-in costs in beginning inventory) are the first to be

completed and transferred out while ending work in process consists of only the higher-cost

current-period units. The weighted-average method, however, smoothes out cost per equivalent

FIFO Method of Process Costing,

Binding Department of Bookworm, Inc. for April 2012.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-in

Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

1,050

(work done before current period)

Transferred-in during current period (given)

2,400

To account for

3,450

Completed and transferred out during current period:

From beginning work in processa

1,050

[1,050

(100% – 100%); 1,050

(100% – 0%); 1,050

(100% – 50%)]

0

1,050

525

Started and completed

1,650b

(1,650

100%; 1,650

100%; 1,650

100%)

1,650

1,650

1,650

Work in process, endingc (given)

750

(750

100%; 750 0%; 750

70%)

____

750

0

525

Accounted for

3,450

____

____

____

Equivalent units of work done in current period

2,400

2,700

2,700

a Degree of completion in this department: Transferred-in costs, 100%; direct materials, 0%; conversion costs, 50%.

b 2,700 physical units completed and transferred out minus 1,050 physical units completed and transferred out from beginning

work–in-process inventory.

c Degree of completion in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 70%.

17-41

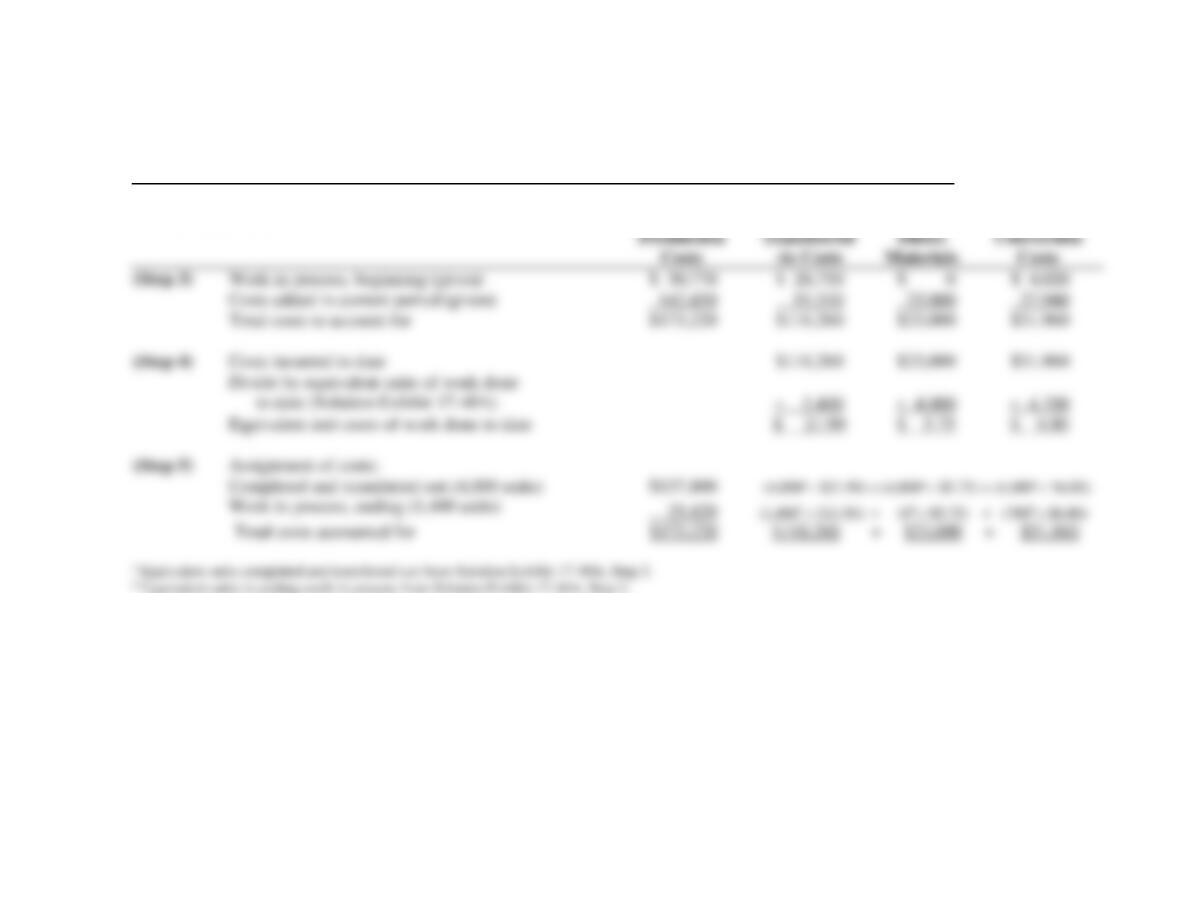

SOLUTION EXHIBIT 17-39B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to Units

Completed and to Units in Ending Work in Process;

FIFO Method of Process Costing,

Binding Department of Bookworm, Inc. for April 2012.

Total

Production

Costs

Transferred-in Costs

Direct

Materials

Conversion

Costs

(Step 3)

Work in process, beginning (given)

$ 50,400

$ 36,750

$ 0

$13,650

Costs added in current period (given)

218,490

124,800

23,490

70,200

Total costs to account for

$268,890

$161,550

$23,490

$83,850

(Step 4)

Costs added in current period

$124,800

$23,490

$70,200

Divide by equivalent units of work done in current period (Sol.

Exhibit 17-39A)

÷ 2,400

÷ 2,700

÷ 2,700

Cost per equivalent unit of work done in current period

$ 52.00

$ 8.70

$ 26.00

(Step 5)

Assignment of costs:

Completed and transferred out (2,700 units)

Work in process, beginning (1,050 units)

$ 50,400

$36,750 + $0 + $13,650

Costs added to beginning work in process in current period

22,785

(0a × $52.00) + (1,050a × $8.70) + (525a × $26)

Total from beginning inventory

73,185

Started and completed (1,650 units)

143,055

(1,650b × $52.00) + (1,650b × $8.70) + (1,650b × $26)

Total costs of units completed and transferred out

216,240

Work in process, ending (750 units):

52,650

(750c × $52.00) + (0c × $8.70) + (525c × $26)

Total costs accounted for

$268,890

$161,550

+ $23,490

+ $83,850

a Equivalent units used to complete beginning work in process from Solution Exhibit 17-39A, step 2.

b Equivalent units started and completed from Solution Exhibit 17-39A, step 2.

c Equivalent units in ending work in process from Solution Exhibit 17-39A, step 2.

17-42

17-40 (45 min.) Transferred-in costs, weighted-average and FIFO methods.

1. Solution Exhibit 17-40A computes the equivalent units of work done to date in the

Drying and Packaging Department for transferred-in costs, direct materials, and conversion

2. Solution Exhibit 17-40C computes the equivalent units of work done in week 37 in the

Drying and Packaging Department for transferred-in costs, direct materials, and conversion

costs. Solution Exhibit 17-40D summarizes total Drying and Packaging Department costs for

week 37, calculates the cost per equivalent unit of work done in week 37 in the Drying and

Packaging Department for transferred-in costs, direct materials, and conversion costs, and

17-43

SOLUTION EXHIBIT 17-40B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total

Costs to Units Completed and to Units in Ending Work in Process;

Weighted-Average Method of Process Costing,

Drying and Packaging Department of Frito-Lay Inc. for Week 37.

Total

Production

Costs

Transferred

-in Costs

Direct

Materials

Conversion

Costs

(Step 3)

Work in process, beginning (given)

$ 30,770

$ 26,750

$ 0

$ 4,020

Costs added in current period (given)

142,450

91,510

23,000

27,940

Total costs to account for

$173,220

$118,260

$23,000

$31,960

(Step 4)

Costs incurred to date

$118,260

$23,000

$31,960

Divide by equivalent units of work done

to date (Solution Exhibit 17-40A)

5,400

4,000

4,700

Equivalent unit costs of work done to date

$ 21.90

$ 5.75

$ 6.80

(Step 5)

Assignment of costs:

Completed and transferred out (4,000 units)

$137,800

(4,000a $21.90) + (4,000a $5.75) + (4,000a $6.80)

Work in process, ending (1,400 units)

35,420

(1,400b $21.90) + (0b $5.75) + (700b $6.80)

Total costs accounted for

$173,220

$118,260 + $23,000 + $31,960

a Equivalent units completed and transferred out from Solution Exhibit 17-40A, Step 2.

b Equivalent units in ending work in process from Solution Exhibit 17-40A, Step 2.

17-44

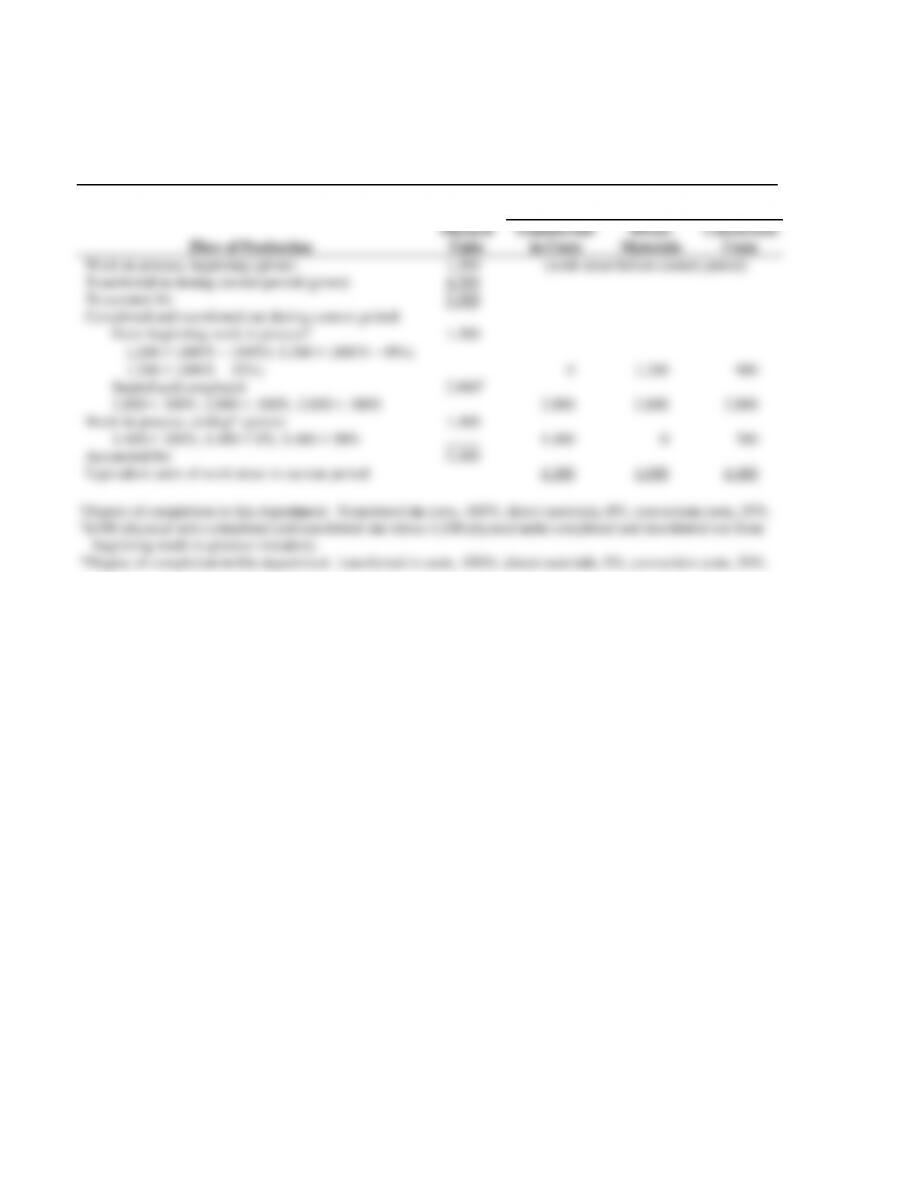

SOLUTION EXHIBIT 17-40C

Steps 1 and 2: Summarize Output in Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing,

Drying and Packaging Department of Frito-Lay Inc. for Week 37.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Transferred-in during current period (given)

To account for

1,200

4,200

5,400

(work done before current period)

Completed and transferred out during current period:

From beginning work in process§

1,200

(100% − 100%); 1,200

(100% − 0%);

1,200

(100% − 25%)

1,200

0

1,200

900

Started and completed

2,800

100%; 2,800

100%; 2,800

100%

2,800†

2,800

2,800

2,800

Work in process, ending* (given)

1,400

100%; 1,400

0%; 1,400

50%

1,400

1,400

0

700

Accounted for

5,400

Equivalent units of work done in current period

4,200

4,000

4,400

§Degree of completion in this department: Transferred-in costs, 100%; direct materials, 0%; conversion costs, 25%.

†4,000 physical units completed and transferred out minus 1,200 physical units completed and transferred out from

beginning work-in-process inventory.

*Degree of completion in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 50%.

SOLUTION EXHIBIT 17-40D

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to

Units Completed and to Units in Ending Work in Process;

FIFO Method of Process Costing,

17-46

17-41 (30-35 min.) Weighted-average and standard-costing method.

2. and 3. Solution Exhibit 17-41B summarizes total costs of the Penelope’s Pearls

Company for November 30, 2012 and, using the standard cost per equivalent unit for direct

materials and conversion costs, assigns these costs to units completed and transferred out and to

units in ending work in process. The exhibit also summarizes the cost variances for direct

materials and conversion costs for November 2012.

17-47

SOLUTION EXHIBIT 17-41B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per

Equivalent Unit, and Assign Total Costs to Units Completed and to Units in

Ending Work in Process;

Standard-Costing Method of Process Costing,

17-48

1. Since there was no additional work needed on the beginning inventory with respect to

materials, the initial mulch must have been 100% complete with respect to materials.

2. It is clear that the ending WIP is also 100% complete with respect to direct materials

3. We can first obtain the total standard costs per unit. The number of units started and

completed during August is 845,000, and a total cost of $6,717,750 is attached to

them. The per unit standard cost is therefore ($6,717,750 ÷ 845,000) = $7.95. If x

4. The opening WIP inventory contained 965,000 equivalent units of materials and