14-1

CHAPTER 14

14-1 Disagree. Cost accounting data plays a key role in many management planning and

control decisions. The division president will be able to make better operating and strategy

1. To provide information for economic decisions.

3. To justify costs or compute reimbursement amounts.

14-3 Exhibit 14-2 lists four criteria used to guide cost allocation decisions:

2. Benefits received.

4. Ability to bear.

purpose.

14-4 Disagree. In general, companies have three choices regarding the allocation of corporate

costs to divisions: allocate all corporate costs, allocate some corporate costs (those “controllable”

14-5 Disagree. If corporate costs allocated to a division can be reallocated to the indirect cost

pools of the division on the basis of a logical cause-and-effect relationship, then it is in fact

preferable to do so—this will result in fewer division indirect cost pools and a more cost-

14-2

14-6 Customer profitability analysis highlights to managers how individual customers

14-7 Companies that separately record (a) the list price and (b) the discount have sufficient

14-8 No. A customer-profitability profile highlights differences in current period’s profitability

across customers. Dropping customers should be the last resort. An unprofitable customer in one

14-9 Five categories in a customer cost hierarchy are identified in the chapter. The examples

given relate to the Spring Distribution Company used in the chapter:

• Customer output-unit-level costs—costs of activities to sell each unit (case) to a customer.

An example is product-handling costs of each case sold.

14-10 Charting cumulative profits by customer or product type generates a whale curve. This

14-11 Using the levels approach introduced in Chapter 7, the sales-volume variance is a Level 2

variance. By sequencing through Level 3 (sales-mix and sales-quantity variances) and then

14-12 The total sales-mix variance arises from differences in the budgeted contribution margin

14-13 A favorable sales-quantity variance arises because the actual units of all products sold

exceed the budgeted units of all products sold.

14-14 The sales-quantity variance can be decomposed into (a) a market-size variance (which

arises when the actual total market size in units is different from the budgeted market size in

14-15 The direct materials efficiency variance is a Level 3 variance. Further insight into this

variance can be gained by moving to a Level 4 analysis where the effect of mix and yield

1. Direct costs = $2.40

$2.40 = 380%

2. The answers here are less than clear-cut in some cases.

Overhead Cost Item

Allocation Criteria

Processing of paperwork for purchase

Supplies room management fee

Operating-room and patient-room handling costs

Administrative hospital costs

University teaching-related costs

Malpractice insurance costs

Cost of treating uninsured patients

Profit component

Cause and effect

Benefits received

Cause and effect

Benefits received

Ability to bear

Ability to bear or benefits received

Ability to bear

None. This is not a cost.

3. Assuming that Meltzer’s insurance company is responsible for paying the $4,800 bill,

Meltzer probably can only express outrage at the amount of the bill. The point of this question is

14-4

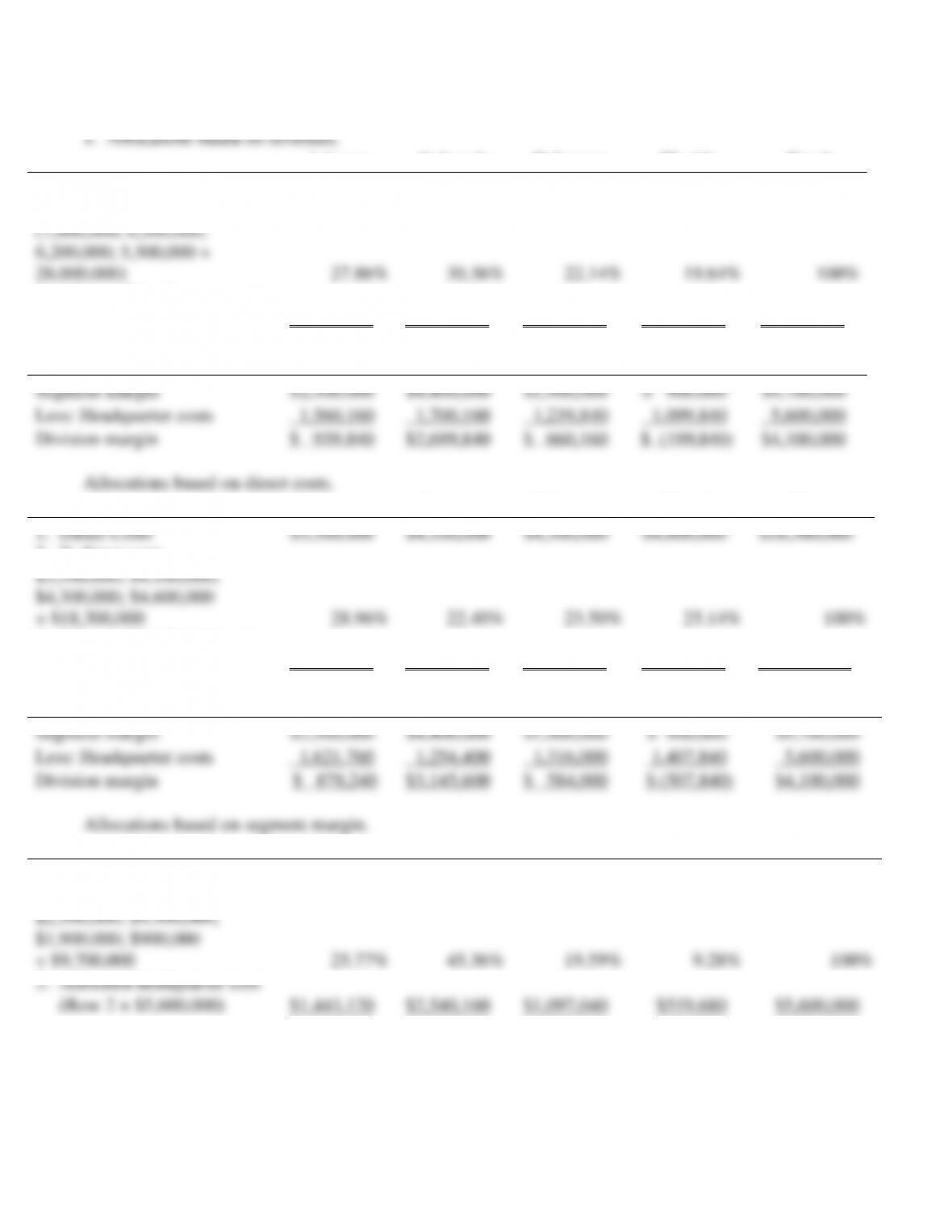

14-17 (15 min.) Cost Allocation and Decision Making

Arizona

Colorado

Delaware

Florida

Total

1. Revenues

7,800,000

8,500,000

6,200,000

5,500,000

28,000,000

2. % revenues

(7,800,000; 8,500,000;

6,200,000; 5,500,000 ÷

28,000,000)

27.86%

30.36%

22.14%

19.64%

100%

3. Allocated headquarter cost

(Row 2 × $5,600,000)

$1,560,160

$1,700,160

$1,239,840

$1,099,840

$5,600,000

Arizona

Colorado

Delaware

Florida

Total

Segment margin

$2,500,000

$4,400,000

$1,900,000

$ 900,000

$9,700,000

Less: Headquarter costs

1,560,160

1,700,160

1,239,840

1,099,840

5,600,000

Division margin

$ 939,840

$2,699,840

$ 660,160

$ (199,840)

$4,100,000

Allocations based on direct costs.

Arizona

Colorado

Delaware

Florida

Total

1. Direct Costs

$5,300,000

$4,100,000

$4,300,000

$4,600,000

$18,300,000

2. % direct costs

$5,300,000; $4,100,000;

$4,300,000; $4,600,000

÷ $18,300,000

28.96%

22.40%

23.50%

25.14%

100%

3. Allocated headquarter cost

(Row 2 × $5,600,000)

$1,621,760

$1,254,400

$1,316,000

$1,407,840

$ 5,600,000

Arizona

Colorado

Delaware

Florida

Total

Segment margin

$2,500,000

$4,400,000

$1,900,000

$ 900,000

$9,700,000

Less: Headquarter costs

1,621,760

1,254,400

1,316,000

1,407,840

5,600,000

Division margin

$ 878,240

$3,145,600

$ 584,000

$ (507,840)

$4,100,000

Allocations based on segment margin.

Arizona

Colorado

Delaware

Florida

Total

1. Segment Margins

$2,500,000

$4,400,000

$1,900,000

$900,000

$9,700,000

2. % segment margins

$2,500,000; $4,400,000;

$1,900,000; $900,000

÷ $9,700,000

25.77%

45.36%

19.59%

9.28%

100%

3. Allocated headquarter cost

(Row 2 × $5,600,000)

$1,443,120

$2,540,160

$1,097,040

$519,680

$5,600,000

14-5

Arizona

Colorado

Delaware

Florida

Total

Segment margin

$2,500,000

$4,400,000

$1,900,000

$900,000

$9,700,000

Less: Headquarter costs

1,443,120

2,540,160

1,097,040

519,680

5,600,000

Division margin

$1,056,880

$1,859,840

$ 802,960

$380,320

$4,100,000

Allocations based on number of employees.

Arizona

Colorado

Delaware

Florida

Total

1. Number of Employees

2,000

4,000

1,500

500

8,000

2. % segment margins

$2,000; $4,000; $1,500; 500

÷ $8,000

25%

50%

18.75%

6.25%

100%

3. Allocated headquarter cost

(Row 2 × $5,600,000)

$1,400,000

$2,800,000

$1,050,000

$350,000

$5,600,000

Arizona

Colorado

Delaware

Florida

Total

Segment margin

$2,500,000

$4,400,000

$1,900,000

$900,000

$9,700,000

Less: Headquarter costs

1,400,000

2,800,000

1,050,000

350,000

5,600,000

Division margin

$1,100,000

$1,600,000

$ 850,000

$550,000

$4,100,000

3. The Arizona Division and the Delaware Division receive roughly the same percentage

25.1%). All four methods are reasonable options, but none clearly meets the cause-and-

effect criterion for selecting the allocation base. If larger divisions tend to consume more

4. If Greenbold elects to use direct costs as the allocation base, the Florida Division will

appear to have a $507,840 operating loss. Even so, the Florida Division generates a

$900,000 segment margin before allocating the cost of the corporate headquarters. As seen

14-6

1.

Hotel

Restaurant

Casino

Rembrandt

Revenue

$16,425,000

$5,256,000

$12,340,000

$34,021,000

Direct costs

9,819,260

3,749,172

4,248,768

17,817,200

Segment margin

$ 6,605,740

$1,506,828

$ 8,091,232

16,203,800

Fixed overhead costs

14,550,000

Income before taxes

$ 1,653,800

Segment margin %

40.22%

28.67%

65.57%

2.

Hotel

Restaurant

Casino

Rembrandt

Direct costs

$9819260

$3749172

$4248768

$17817200

Direct cost %

55.11%

21.04%

23.85%

100.00%

Square footage

80,000

16,000

64,000

160,000

Square footage %

50.00%

10.00%

40.00%

100.00%

Number of employees

200

50

250

500

Number of employees %

40.00%

10.00%

50.00%

100.00%

A: Cost allocation based on direct costs:

Hotel

Restaurant

Casino

Rembrandt

Revenue

$16,425,000

$ 5,256,000

$12,340,000

$34,021,000

Direct costs

9,819,260

3,749,172

4,248,768

17,817,200

Segment margin

6,605,740

1,506,828

8,091,232

16,203,800

Allocated fixed overhead costs

8,018,505

3,061,320

3,470,175

14,550,000

Segment pre-tax income

$ (1,412,765)

$(1,554,492)

$ 4,621,057

$ 1,653,800

Segment pre-tax income % of rev.

-8.60%

-29.58%

37.45%

B: Cost allocation based on floor space:

Hotel

Restaurant

Casino

Rembrandt

Allocated fixed overhead costs

$ 7,275,000

$ 1,455,000

$ 5,820,000

$14,550,000

Segment pre-tax income

$ (669,260)

$ 51,828

$ 2,271,232

$ 1,653,800

Segment pre-tax income % of rev.

-4.07%

0.99%

18.41%

C: Cost allocation based on number of employees

Hotel

Restaurant

Casino

Rembrandt

Allocated fixed overhead costs

$ 5,820,000

$ 1,455,000

$ 7,275,000

$14,550,000

Segment pre-tax income

$ 785,740

$ 51,828

$ 816,232

$ 1,653,800

Segment pre-tax income % of rev.

4.78%

0.99%

6.61%

14-7

3. Requirement 2 shows the dramatic effect of the choice of cost allocation base on segment

pre-tax income as a percentage of revenues:

Pre-tax Income Percentage

Allocation Base

Hotel

Restaurant

Casino

Direct costs

–8.60%

–29.58%

37.45%

Floor space

–4.07

0.99

18.41

Number of employees

4.78

0.99

6.61

The decision context should guide (a) whether costs should be allocated, and (b) the

preferred cost allocation base. Decisions about, say, performance measurement, may be made on

a combination of financial and nonfinancial measures. It may well be that Rembrandt may prefer

to exclude allocated costs from the financial measures to reduce areas of dispute.

Where cost allocation is required, the cause-and-effect and benefits-received criteria are

recommended in Chapter 14. The $14,550,000 is a fixed overhead cost. This means that on a

short-run basis, the cause-and-effect criterion is not appropriate but Rembrandt could attempt to

identify the cost drivers for these costs in the long run when these costs are likely to be more

variable. Rembrandt should look at how the $14,550,000 cost benefits the three divisions. This

will help guide the choice of an allocation base in the short run.

4. The analysis in requirement 2 should not guide the decision on whether to shut down any

of the divisions. The overhead costs are fixed costs in the short run. It is not clear how these

14-8

14-19 (25 min.) Cost allocation to divisions.

Percentages for various allocation bases (old and new):

Pulp

Paper

Fibers

Total

(1) Division margin percentages

$2,400,000; $7,100,000; $9,500,000

$19,000,000

12.63157%

37.36843%

50.0%

100.0%

(2) Share of employees

$350; 250; 400

1,000

35.0

25.0

40.0

100.0

(3) Share of floor space

35,000; 24,000; 66,000

125,000

28.0

19.2

52.8

100.0

(4) Share of total division administrative costs

$2,000,000; $1,800,000; $3,200,000

$7,000,000

28.57142

25.71428

45.71428

100.0

1.

Pulp

Paper

Fibers

Total

(5) Division margin

$2,400,000

$ 7,100,000

$ 9,500,000

$19,000,000

(6) Corporate overhead allocated on segment

margins = (1)

$9,000,000

1,136,842

3,363,158

4,500,000

9,000,000

(7) Operating margin with division-margin-based

allocation = (5) – (6)

$1,263,158

$ 3,736,842

$ 5,000,000

$10,000,000

(8) Revenues

$8,500,000

$17,500,000

$24,000,000

$50,000,000

Operating margin as a percentage of revenues

14.9%

21.3%

20.8%

20.0%

2.

Pulp

Paper

Fibers

Total

(5) Division margin

$2,400,000

$ 7,100,000

$ 9,500,000

$19,000,000

HRM costs (alloc. base: no. of employees)

= (2)

$1,800,000

630 ,000

450,000

720,000

1,800,000

Facility costs (alloc. base: floor space)

= (3)

$2,700,000

756,000

518,400

1,425,600

2,700,000

Corp. admin (alloc. base: div. admin costs)

= (4)

$4,500,000

1,285,714

1,157,143

2,057,143

4,500,000

Corp. overhead allocated to each division

2,671,714

2,125,543

4,202,743

9,000,000

Operating margin with cause-and-effect

allocation

$(271,714)

$ 4,974,457

$ 5,297,257

$10,000,000

(8) Revenues

$8,500,000

$17,500,000

$24,000,000

$50,000,000

Operating margin as a percentage of revenues

-3.2%

28.4%

22.1%

20.0 %

14-9

3. When corporate overhead is allocated to the divisions on the basis of division margins

(requirement 1), each division is profitable (has positive operating margin) and the Paper

division is the most profitable (has the highest operating margin percentage) by a slim margin,

while the Pulp division is the least profitable. When Bardem’s suggested bases are used to

4. The new approach is preferable because it is based on cause-and-effect relationships

between costs and their respective cost drivers in the long run.

Human resource management costs are allocated using the number of employees in each

division because the costs for recruitment, training, etc., are mostly related to the number of

14-10

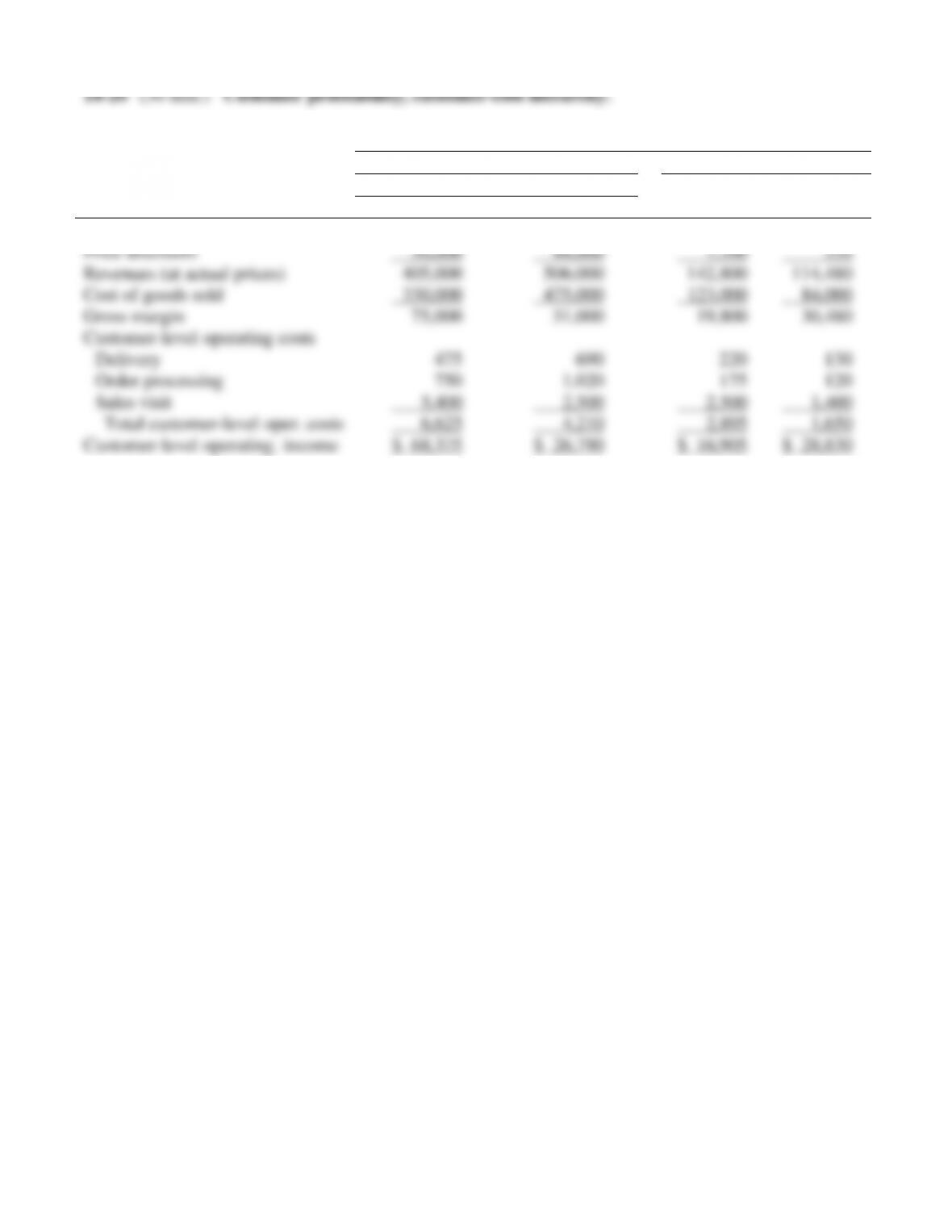

1.

All amounts in thousands of U.S. dollars

Wholesale

Retail

North America

South America

Big Sam

World

Wholesaler

Wholesaler

Stereo

Market

Revenues at list prices

$435,000

$550,000

$150,000

$115,000

Price discounts

30,000

44,000

7,200

520

Revenues (at actual prices)

405,000

506,000

142,800

114,480

Cost of goods sold

330,000

475,000

123,000

84,000

Gross margin

75,000

31,000

19,800

30,480

Customer-level operating costs

Delivery

475

690

220

130

Order processing

750

1,020

175

120

Sales visit

5,400

2,500

2,500

1,400

Total customer-level oper. costs

6,625

4,210

2,895

1,650

Customer-level operating. income

$ 68,375

$ 26,790

$ 16,905

$ 28,830