18-29

18-39 (30−35 min.) Weighted-average method, inspection at 80% completion (chapter

appendix).

The computation and allocation of spoilage is the most difficult part of this problem. The units in

the ending inventory have passed inspection. Therefore, of the 100,000 units to account for

(12,500 beginning + 87,500 started), 12,500 must have been spoiled in May [100,000 – (62,500

complete.

• Direct materials units are included for ending work in process, which is 95%

complete, but not for beginning work in process, which is 25% complete. The reason

is that direct materials are added when production is 90% complete. The ending work

in process, therefore, contains direct materials units; the beginning work in process

does not.

18-30

SOLUTION EXHIBIT 18-39

Weighted-Average Method of Process Costing with Spoilage;

Finishing Department of the Kim Company for August.

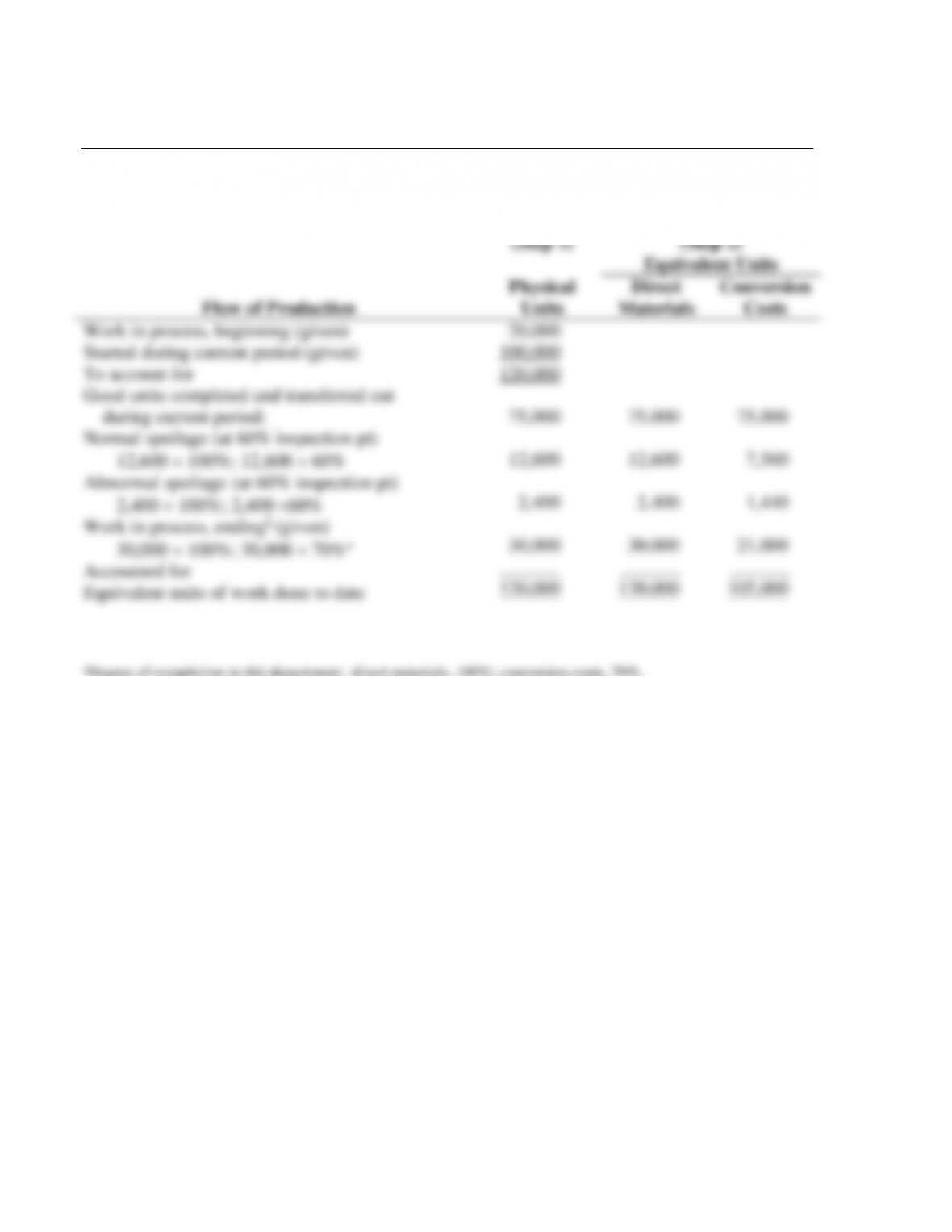

PANEL A: Steps 1 and 2—Summarize Output in Physical Units and Compute Output in

Equivalent Units

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

during current period:

Normal spoilage on good units*

6,250 100%; 6,250 0%; 6,250 80%

Work in process, ending‡ (given)

25,000 100%; 25,000 100%; 25,000 95%

Normal spoilage on ending WIP**

2,500 100%; 2,500 0%; 2,500 80%

Abnormal spoilage†

3,750 100%; 3,750 0%; 3,750 80%

Accounted for

Equivalent units of work done to date

12,500

87,500

100,000

62,500

6,250

25,000

2,500

3,750

100,000

62,500

6,250

25,000

2,500

3,750

100,000

62,500

0

25,000

0

0

87,500

62,500

5,000

23,750

2,000

3,000

96,250

*Normal spoilage is 10% of good units that pass inspection: 10% 62,500 = 6,250 units. Degree of completion of normal

spoilage in this department: transferred-in costs, 100%; direct materials, 0%; conversion costs, 80%.

‡Degree of completion in this department: transferred-in costs, 100%; direct materials, 100%; conversion costs, 95%.

**Normal spoilage is 10% of the good units in ending WIP that have passed the inspection point, 10% 25,000 = 2,500 units.

Degree of completion of normal spoilage in this department: transferred-in costs, 100%; direct materials, 0%; conversion

costs, 80%.

†Abnormal spoilage = Actual spoilage − Normal spoilage = 12,500 − 8,750 = 3,750 units. Degree of completion of abnormal

18-31

SOLUTION EXHIBIT 18-39

PANEL B: Steps 3, 4, and 5— Summarize Total Costs to Account For, Compute Cost per

Equivalent Unit, and Assign Total Costs to Units Completed, to Spoiled Units, and to Units

in Ending Work in Process

Total

Production

Costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs incurred to date

Divided by equivalent units of work done

to date

Cost per equivalent unit

(Step 5) Assignment of costs

Good units completed and transferred out

(62,500 units)

$ 156,125

3,192,875

$3,349,000

$103,625

809,375

$913,000

$913,000

100,000

$ 9.13

$ −

819,000

$819,000

$819,000

87,500

$ 9.36

$ 52,500

1,564,500

$1,617,000

$1,617,000

96,250

$ 16.80

Costs before adding normal spoilage

Normal spoilage (6,250 units)

(A) Total costs of good units completed

and transferred out

(B) Abnormal spoilage (3,750 units)

Work in process, ending (25,000 units)

WIP ending, before normal spoilage

Normal spoilage on ending WIP

(C) Total costs of ending WIP

(A)+(B)+(C) Total costs accounted for

$2,205,625

141,063

2,346,688

84,638

861,250

56,425

917,675

$3,349,000

62,500# ($9.13 + $9.36 + $16.80)

(6,250# $9.13) + (0# $9.36) + (5,000# $16.80)

(3,750# $9.13) + (0# $9.36) + (3,000# $16.80)

(25,000# $9.13) + (25,000# $9.36) + (23,750# $16.80)

(2,500# $9.13) + (0# $9.36) + (2,000# $16.80)

$913,000 + $819,000 + $1,617,000

#Equivalent units of transferred-in costs, direct materials, and conversion costs calculated in Step 2 in Panel A.

18-32

18-40 (20 min.) Job costing, rework.

1. Manufacturing Overhead Control (rework costs) 1,800

Materials Control ($12 50) 600

Wages Payable ($9 50) 450

2. Total rework costs for XD1 chips in August 2011 are as follows:

3. Manufacturing costs of job #3879 before rework:

200 units ($60+$12+$38) $22,000

Add: Normal rework costs 1,800

Total cost of job #3879 $23,800

18-33

18-41 Physical units, inspection at various levels of completion, weighted average process

costing report

1.

Inspection

Inspection

Inspection

at 30%

at 60%

at 100%

Work in process, beginning (40%)*

Started during November

To account for

20,000

100,000

120,000

20,000

100,000

120,000

20,000

100,000

120,000

Good units completed and transferred out

Normal spoilage

75,000a

10,200b

75,000a

12,600c

75,000a

9,000d

Abnormal spoilage (15,000 – normal spoilage)

Work in process, ending (70%)*

Accounted for

4,800

30,000

120,000

2,400

30,000

120,000

6,000

30,000

120,000

*Degree of completion for conversion costs at the dates of the work-in-process inventories

a20,000 beginning inventory +100,000 –15,000 spoiled – 30,000 ending inventory = 75,000.

b12% (100,000 units started – 15,000 units spoiled) = 12% 85,000 = 10,200; beginning work-in-process

inventory is excluded because it was already 40% complete at Nov 1 and past the inspection point.

c12% (120,000 units – 15,000 ) = 12% 105,000 = 12,600, because all units passed the 60% completion

inspection point in November.

d 12% 75,000 = 9,000, because 75,000 units are fully completed and inspected during November.

2. There are different amounts of normal and abnormal spoilage because the spoilage is detected

at different points in the process. At the 30% inspection point, the beginning work in process

problem.)

3. Solution Exhibit 18-41 summarizes total costs to account for, calculates the equivalent units of

18-34

SOLUTION EXHIBIT 18-41

Weighted-Average Method of Process Costing with Spoilage;

Forging Department of Lester Company for November.

PANEL A: Steps 1 and 2—Summarize Output in Physical Units and Compute Output in

Equivalent Units

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

Good units completed and transferred out

during current period:

Normal spoilage (at 60% inspection pt)

12,600 100%; 12,600 60%

Abnormal spoilage (at 60% inspection pt)

2,400 100%; 2,400 60%

Work in process, ending‡ (given)

30,000 100%; 30,000 70%a

Accounted for

Equivalent units of work done to date

20,000

100,000

120,000

75,000

12,600

2,400

30,000

120,000

75,000

12,600

2,400

30,000

120,000

75,000

7,560

1,440

21,000

105,000

aDegree of completion in this department: direct materials, 100%; conversion costs, 70%.

18-35

SOLUTION EXHIBIT 18-41

PANEL B: Steps 3, 4, and 5— Summarize Total Costs to Account For, Compute Cost per

Equivalent Unit, and Assign Total Costs to Units Completed, to Spoiled Units, and to Units

in Ending Work in Process

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

Costs added in current period (given)

Total costs to account for

(Step 4) Costs incurred to date

Divided by equivalent units of work done to date

Cost per equivalent unit

(Step 5) Assignment of costs

Good units completed and transferred out (75,000 units)

$ 166,500

1,200,000

$1,366,500

$ 64,000

200,000

$264,000

$264,000

120,000

$ 2.20

$ 102,500

1,000,000

$1,102,500

$1,102,500

105,000

$ 10.50

Costs before adding normal spoilage

Normal spoilage (12,600# units, 7560# units)

(A) Total costs of good units completed and

transferred out

(B) Abnormal spoilage (2,400# units, 1,440# units)

(C) Work in process, ending (30,000# units, 21,000# units)

(A)+(B)+(C) Total costs accounted for

$ 952,500

107,100

1,059,600

20,400

286,500

$1,366,500

(75,000 $2.20) +

(12,600 2.20) +

(2,400# 2.20) +

(30,000 2.20) +

$264,000 +

(75,000 10.50)

(7,560 10.50)

(1,440 10.50)

(21,000 10.50)

$1,102,500

#Equivalent units of direct materials and conversion costs calculated in Step 2 in Panel A above.