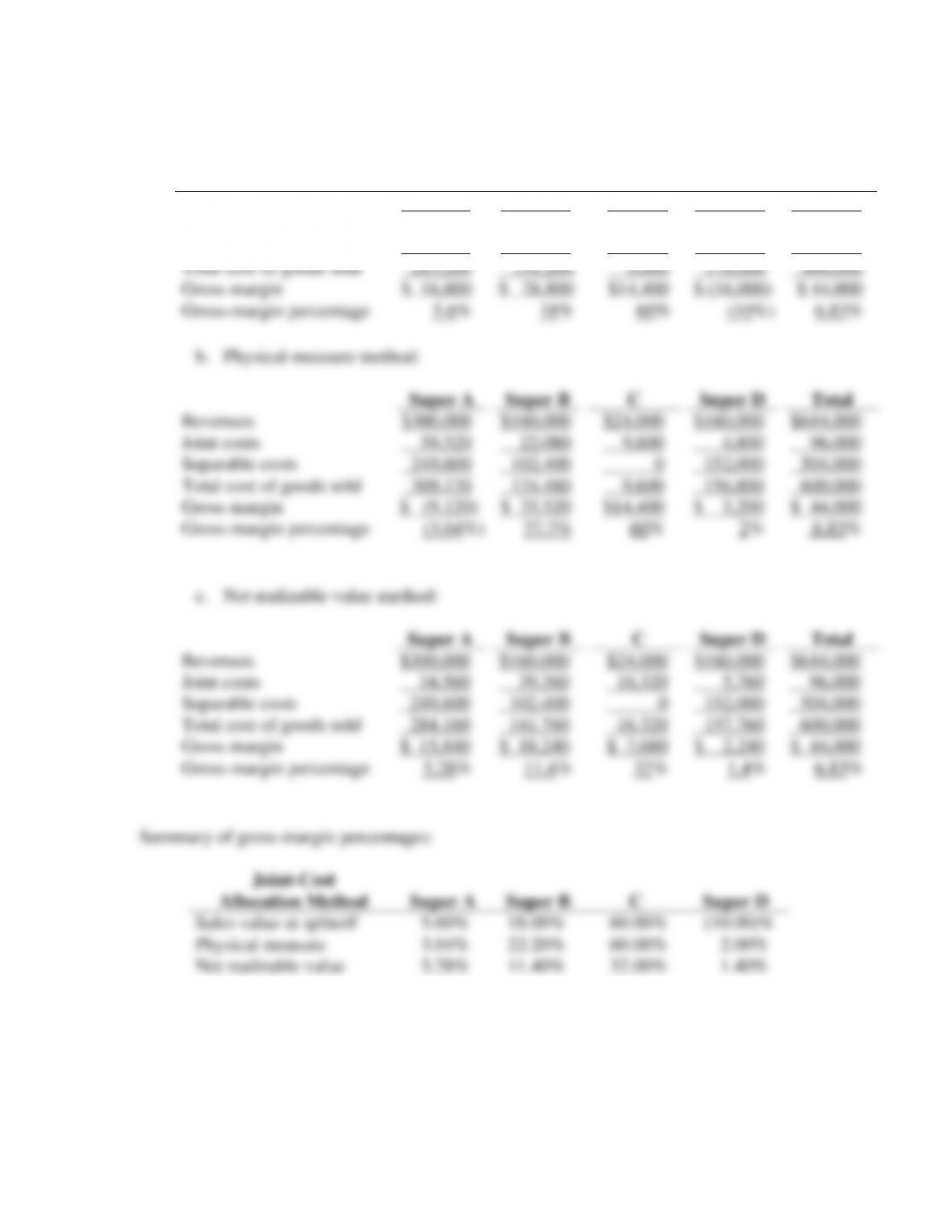

Computation of gross-margin percentages:

a. Sales value at splitoff method:

Super A

Super B

C

Super D

Total

Revenues

$300,000

$160,000

$24,000

$160,000

$644,000

Joint costs

33,600

28,800

9,600

24,000

96,000

Separable costs

249,600

102,400

0

152,000

504,000

Total cost of goods sold

283,200

131,200

9,600

176,000

600,000

Gross margin

$ 16,800

$ 28,800

$14,400

$ (16,000)

$ 44,000

Gross-margin percentage

5.6%

18%

60%

(10%)

6.83%

b. Physical-measure method:

Super A

Super B

C

Super D

Total

Revenues

$300,000

$160,000

$24,000

$160,000

$644,000

Joint costs

59,520

22,080

9,600

4,800

96,000

Separable costs

249,600

102,400

0

152,000

504,000

Total cost of goods sold

309,120

124,480

9,600

156,800

600,000

Gross margin

$ (9,120)

$ 35,520

$14,400

$ 3,200

$ 44,000

Gross-margin percentage

(3.04%)

22.2%

60%

2%

6.83%

Revenues

$300,000

$160,000

$24,000

$160,000

$644,000

Joint costs

34,560

39,360

16,320

5,760

96,000

Separable costs

249,600

102,400

0

152,000

504,000

Total cost of goods sold

284,160

141,760

16,320

157,760

600,000

Gross margin

$ 15,840

$ 18,240

$ 7,680

$ 2,240

$ 44,000

Allocation Method

Super B

C

Sales value at splitoff

18.00%

Physical measure

22.20%

Net realizable value

11.40%

16-22

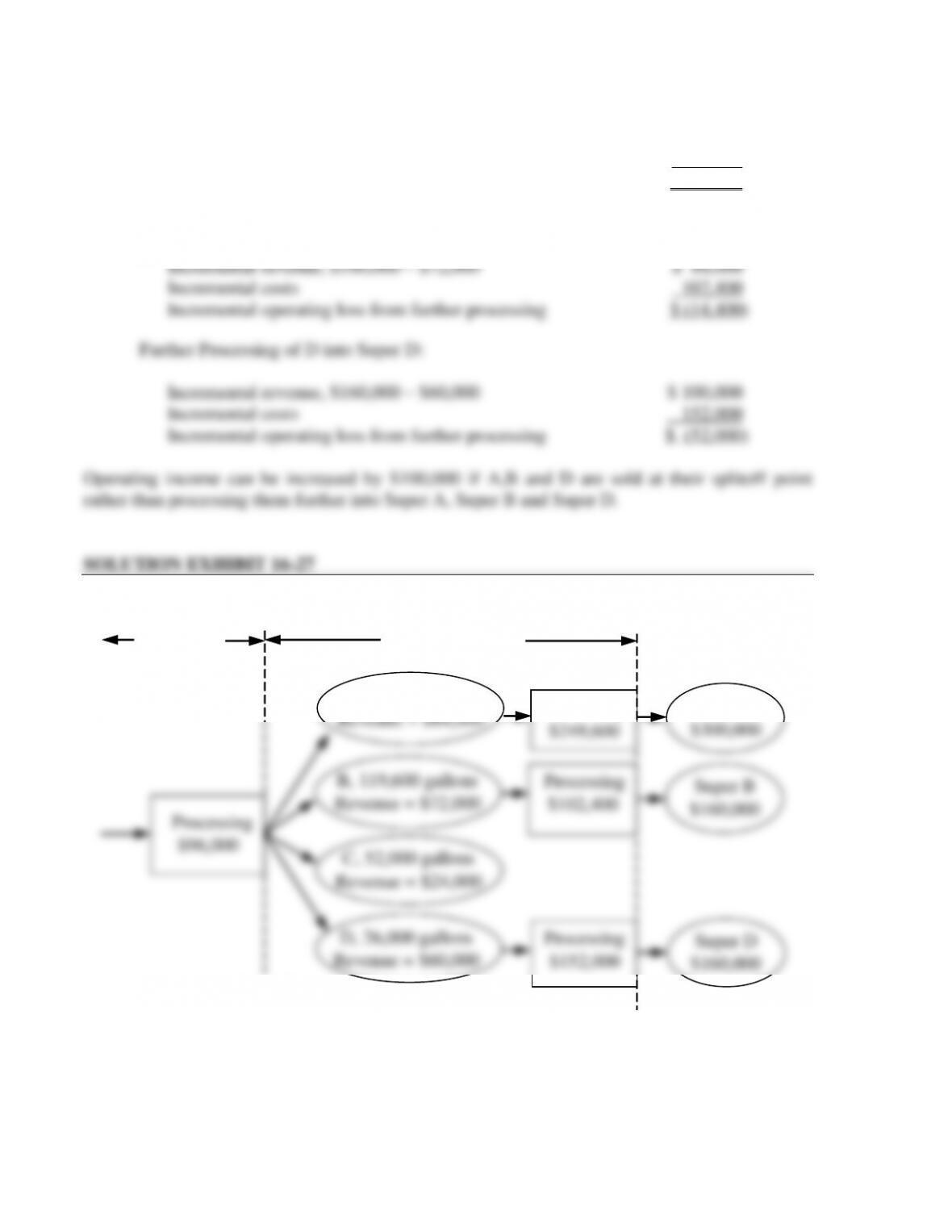

2. Further Processing of A into Super A:

Incremental revenue, $300,000 – $84,000 $216,000

Incremental costs 249,600

Incremental operating loss from further processing $ (33,600)

Further processing of B into Super B:

Processing

$96000

A, 322400 gallons

Revenue = $84000

B, 119600 gallons

Revenue = $72000

D, 26000 gallons

Revenue = $60000

C, 52000 gallons

Revenue = $24000

Joint Costs

Revenues at Splitoff

and Separable Costs

Processing

$249600

Processing

$102400

Processing

$152000

Super A

$300000

Super B

$160000

Super D

$160000

Splitoff

Point

16-23

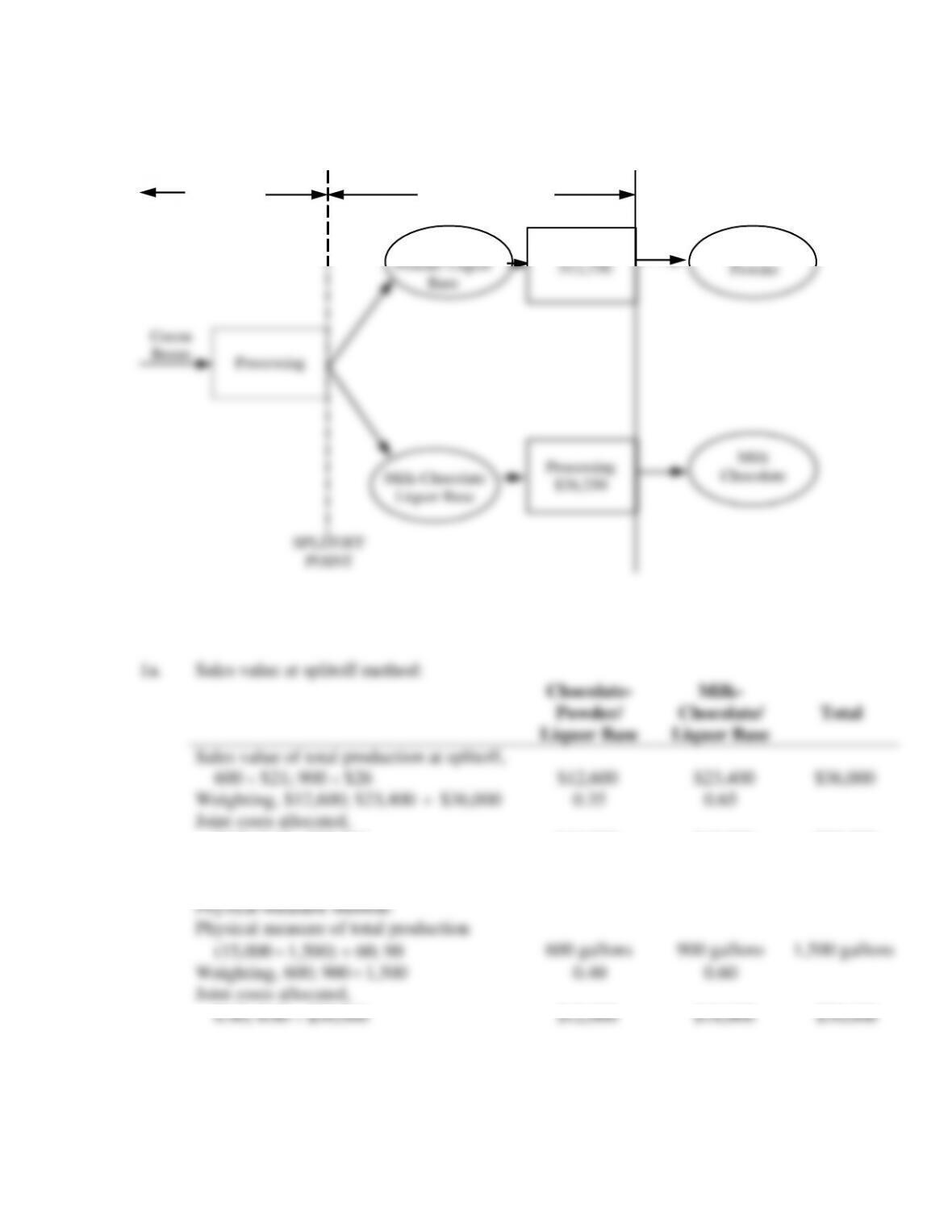

16-28 (40–60 min.) Comparison of alternative joint-cost allocation methods, further-

processing decision, chocolate products.

Chocolate-

Powder Liquor

Base

Milk-Chocolate

Liquor Base

Processing

Processing

$26,250

Joint Costs

$30,000

Separable Costs

Processing

$12,750

Chocolate

Powder

SPLITOFF

POINT

Cocoa

Beans

Milk

Chocolate

1a. Sales value at splitoff method:

Chocolate-

Powder/

Liquor Base

Milk-

Chocolate/

Liquor Base

Total

Sales value of total production at splitoff,

600 $21; 900 $26

$12,600

$23,400

$36,000

Weighting, $12,600; $23,400

$36,000

0.35

0.65

Joint costs allocated,

0.35; 0.65 $30,000

$10,500

$19,500

$30,000

1b.

Physical-measure method:

Physical measure of total production

(15,000

1,500) 60; 90

600 gallons

900 gallons

1,500 gallons

Weighting, 600; 900

1,500

0.40

0.60

Joint costs allocated,

0.40; 0.60 $30,000

$12,000

$18,000

$30,000

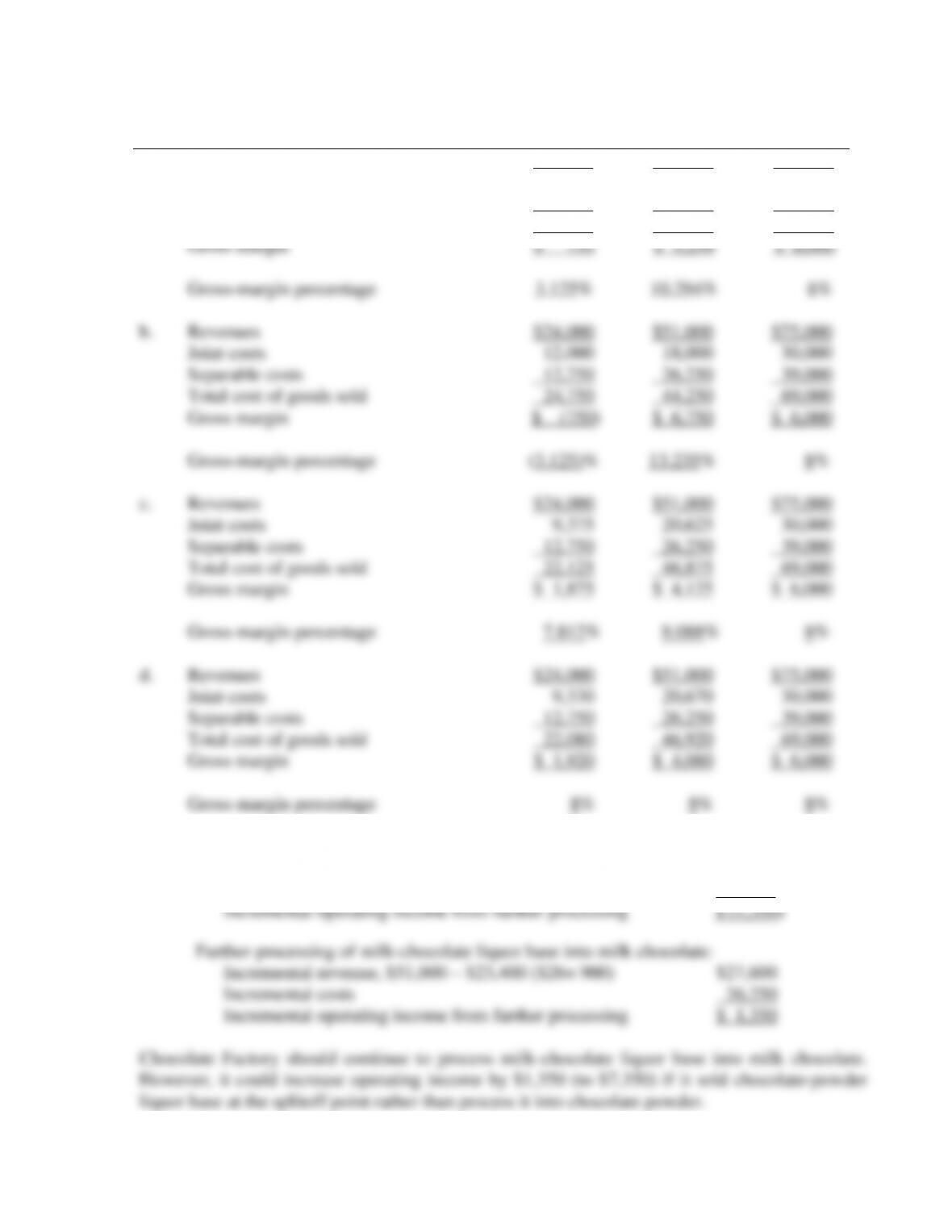

16-24

1c. Net realizable value method:

Chocolate-

Powder

Milk-

Chocolate

Total

Final sales value of total production,

6,000 $4; 10,200 $5

$24,000

$51,000

$75,000

Deduct separable costs

12,750

26,250

39,000

Net realizable value at splitoff point

$11,250

$24,750

$36,000

Weighting, $11,250; $24,750

$36,000

0.3125

0.6875

Joint costs allocated,

0.3125; 0.6875 $30,000

$ 9,375

$20,625

$30,000

d. Constant gross-margin percentage NRV method:

Step 1:

Final sales value of total production, (6,000 $4) + (10,200 $5) $75,000

Deduct joint and separable costs, ($30,000 + $12,750 + $26,250) 69,000

Chocolate-

Milk-

Powder

Chocolate

Total

Final sales value of total production,

6,000 $4; 10,200 $5

$24,000

$51,000

$75,000

Deduct gross margin, using overall

gross-margin percentage of sales (8%)

1,920

4,080

6,000

Total production costs

22,080

46,920

69,000

Step 3:

Deduct separable costs

12,750

26,250

39,000

Joint costs allocated

$ 9,330

$20,670

$30,000

16-25

2.

Chocolate-

Milk-

Powder

Chocolate

Total

a.

Revenues

$24,000

$51,000

$75,000

Joint costs

10,500

19,500

30,000

Separable costs

12,750

26,250

39,000

Total cost of goods sold

23,250

45,750

69,000

Gross margin

$ 750

$ 5,250

$ 6,000

Gross-margin percentage

3.125%

10.294%

8%

b.

Revenues

$24,000

$51,000

$75,000

Joint costs

12,000

18,000

30,000

Separable costs

12,750

26,250

39,000

Total cost of goods sold

24,750

44,250

69,000

Gross margin

$ (750)

$ 6,750

$ 6,000

Gross-margin percentage

(3.125)%

13.235%

8%

c.

Revenues

$24,000

$51,000

$75,000

Joint costs

9,375

20,625

30,000

Separable costs

12,750

26,250

39,000

Total cost of goods sold

22,125

46,875

69,000

Gross margin

$ 1,875

$ 4,125

$ 6,000

Gross-margin percentage

7.812%

8.088%

8%

d.

Revenues

$24,000

$51,000

$75,000

Joint costs

9,330

20,670

30,000

Separable costs

12,750

26,250

39,000

Total cost of goods sold

22,080

46,920

69,000

Gross margin

$ 1,920

$ 4,080

$ 6,000

Gross-margin percentage

8%

8%

8%

3. Further processing of chocolate-powder liquor base into chocolate powder:

Incremental revenue, $24,000 – $12,600 ($21× 600) $11,400

Incremental costs 12,750

16-26

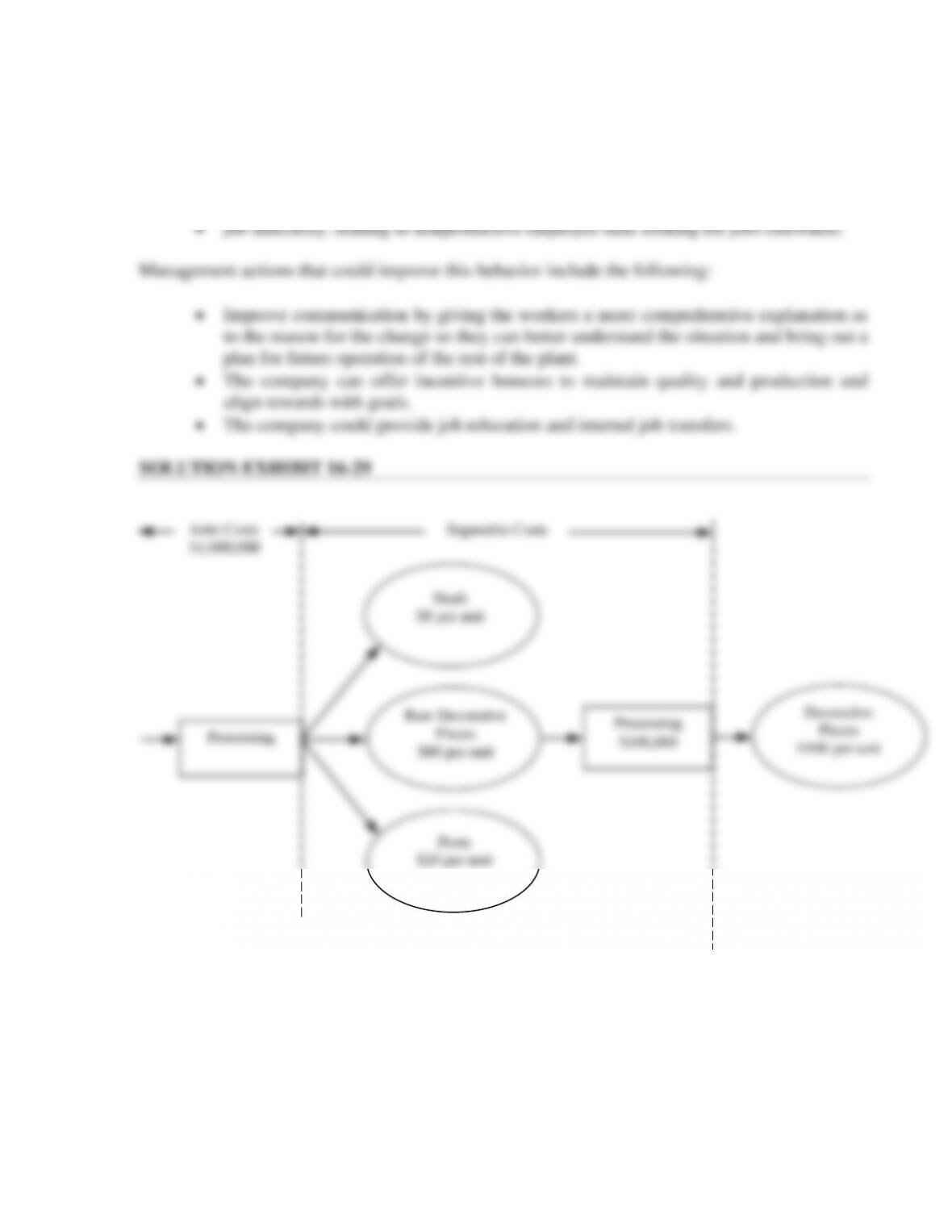

16-29 (30 min.) Joint-cost allocation, process further or sell.

A diagram of the situation is in Solution Exhibit 16-29.

1.

a. Sales value at splitoff method.

Monthly

Unit

Output

Selling

Price

Per Unit

Sales Value

of Total Prodn.

at Splitoff

Weighting

Joint Costs

Allocated

Studs (Building)

75,000

$ 8

$ 600,000

46.1539%

$ 461,539

Decorative Pieces

5,000

60

300,000

23.0769

230,769

Posts

20,000

20

400,000

30.7692

307,692

Totals

$1,300,000

100.0000%

$1,000,000

b. Physical measure method.

Physical

Measure of

Total Prodn.

Weighting

Joint Costs

Allocated

Studs (Building)

75,000

75.00%

$ 750,000

Decorative Pieces

5,000

5.00

50,000

Posts

20,000

20.00

200,000

Totals

100,000

100.00%

$1,000,000

c. Net realizable value method.

Monthly

Units of

Total Prodn.

Fully

Processed

Selling

Price

per Unit

Net

Realizable

Value at

Splitoff

Weighting

Joint Costs

Allocated

Studs (Building)

75,000

$ 8

$ 600,000

44.4445%

$ 444,445

Decorative Pieces

4,500a

100

350,000b

25.9259

259,259

Posts

20,000

20

400,000

29.6296

296,296

Totals

$1,350,000

100.0000%

$1,000,000

a 5,000 monthly units of output – 10% normal spoilage = 4,500 good units.

b 4,500 good units $100 = $450,000 – Further processing costs of $100,000 = $350,000

2. Presented below is an analysis for Sonimad Sawmill, Inc., comparing the processing of

decorative pieces further versus selling the rough-cut product immediately at splitoff:

Units

Dollars

Monthly unit output

5,000

Less: Normal further processing shrinkage

500

Units available for sale

4,500

Final sales value (4,500 units $100 per unit)

$450,000

Less: Sales value at splitoff

300,000

Incremental revenue

150,000

Less: Further processing costs

100,000

Additional contribution from further processing

$ 50,000

3. Assuming Sonimad Sawmill, Inc., announces that in six months it will sell the rough-cut

product at splitoff due to increasing competitive pressure, behavior that may be demonstrated by

the skilled labor in the planing and sizing process include the following:

• lower quality,

• reduced motivation and morale, and

16-28

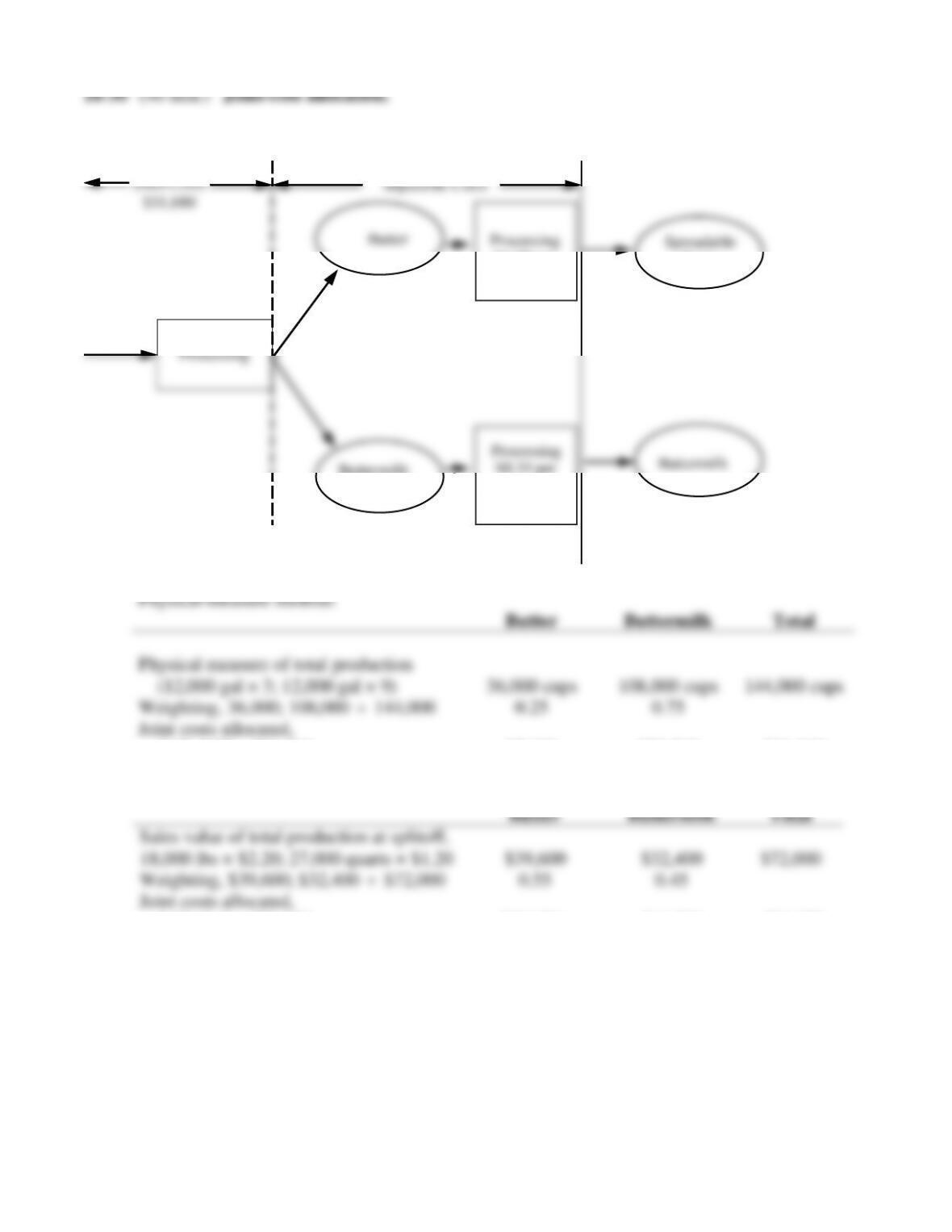

1.

Butter

Buttermilk

Processing

Processing

$0.35 per

pint

Joint Costs

$31,680

Separable Costs

Buttermilk

Processing

$1.60 per

pound

Spreadable

Butter

SPLITOFF

POINT

Milk

a.

Physical-measure method:

Butter

Buttermilk

Total

Physical measure of total production

(12,000 gal × 3; 12,000 gal × 9)

36,000 cups

108,000 cups

144,000 cups

Weighting, 36,000; 108,000

144,000

0.25

0.75

Joint costs allocated,

0.25; 0.75 × $31,680

$7,920

$23,760

$31,680

b. Sales value at splitoff method:

Butter

Buttermilk

Total

Sales value of total production at splitoff,

18,000 lbs × $2.20; 27,000 quarts × $1.20

$39,600

$32,400

$72,000

Weighting, $39,600; $32,400

$72,000

0.55

0.45

Joint costs allocated,

0.55; 0.45 $31,680

$17,424

$14,256

$31,680

c. Net realizable value method:

Butter

Buttermilk

Total

Final sales value of total production,

36,000 tubs $2.30; 27,000 quarts $1.20

$82,800

$32,400

$115,200

Deduct separable costs

28,800

0

28,800

Net realizable value

$54,000

$32,400

$ 86,400

Weighting, $54,000; $32,400

$86,400

0.625

0.375

Joint costs allocated,

0.625; 0.375 $31,680

$19,800

$11,880

$ 31,680

d. Constant gross-margin percentage NRV method:

Step 1:

Final sales value of total production (see 1c.) $115,200

Deduct joint and separable costs ($31,680 + $28,800) 60,480

Final sales value of total production

Deduct gross margin, using overall

gross-margin percentage of sales (47.50%)

Total production costs

Deduct separable costs

Joint costs allocated

16-30

2. Advantages and disadvantages:

– Physical-Measure

Advantage: Low information needs. Only knowledge of joint cost and physical

distribution is needed.

Disadvantage: Allocation is unrelated to the revenue-generating ability of products.

3. When selling prices for all products exist at splitoff, the sales value at split off method is the

preferred technique. It is a relatively simple technique that depends on a common basis for cost

allocation – revenues. It is better than the physical method because it considers the relative