11-1

CHAPTER 11

DECISION MAKING AND RELEVANT INFORMATION

1. Identify the problem and uncertainties

3. Make predictions about the future

5. Implement the decision, evaluate performance, and learn

11-2 Relevant costs are expected future costs that differ among the alternative courses of

11-3 No. Relevant costs are defined as those expected future costs that differ among

11-4 Quantitative factors are outcomes that are measured in numerical terms. Some

quantitative factors are financial––that is, they can be easily expressed in monetary terms. Direct

11-5 Two potential problems that should be avoided in relevant cost analysis are

(i) Do not assume all variable costs are relevant and all fixed costs are irrelevant.

relevant.

11-7 No. Some of the total manufacturing cost per unit of a product may be fixed, and, hence,

will not differ between the make and buy alternatives. These fixed costs are irrelevant to the

11-8 Opportunity cost is the contribution to income that is forgone (rejected) by not using a

limited resource in its next-best alternative use.

11-2

11-9 No. When deciding on the quantity of inventory to buy, managers must consider both the

purchase cost per unit and the opportunity cost of funds invested in the inventory. For example,

11-10 No. Managers should aim to get the highest contribution margin per unit of the

11-11 No. For example, if the revenues that will be lost exceed the costs that will be saved, the

11-12 Cost written off as depreciation is irrelevant when it pertains to a past cost such as

11-13 No. Managers often favor the alternative that makes their performance look best so they

11-14 The three steps in solving a linear programming problem are

11-15 The text outlines two methods of determining the optimal solution to an LP problem:

(i) Trial-and-error approach

11-3

1. This is an unfortunate situation, yet the $78,000 costs are irrelevant regarding the

decision to remachine or scrap. The only relevant factors are the future revenues and future costs.

By ignoring the accumulated costs and deciding on the basis of expected future costs, operating

2. This, too, is an unfortunate situation. But the $101,000 original cost is irrelevant to this

decision. The difference in relevant costs in favor of replacing is $3,500 as follows:

(a) (b)

11-4

1.

Make

Buy

Relevant costs

Variable costs

$190

Avoidable fixed costs

10

Purchase price

____

$260

Unit relevant cost

$200

$260

Dalton Computers should reject Peach’s offer. The $80 of fixed costs are irrelevant because they

will be incurred regardless of this decision. When comparing relevant costs between the choices,

Peach’s offer price is higher than the cost to continue to produce.

2.

Keep

Replace

Difference

Cash operating costs (3 years)

$52,500

$46,500

$6,000

Current disposal value of old machine

(2,200)

2,200

Cost of new machine

_ _____

9,000

(9,000)

Total relevant costs

$52,500

$53,300

$ (800)

AP Manufacturing should keep the old machine. The cost savings are less than the cost to

purchase the new machine.

11-18 (15 min.) Multiple choice.

1. (b) Special order price per unit $6.00

Variable manufacturing cost per unit 4.50

2. (b) Costs of purchases, 20,000 units $60 $1,200,000

Total relevant costs of making:

Variable manufacturing costs, $6 + $30 + $12 $48

11-5

11-19 (30 min.) Special order, activity-based costing.

1. Direct materials cost per unit ($262,500 7,500 units) = $35 per unit

Direct manufacturing labor cost per unit ($300,000 7,500 units) = $40 per unit

Variable cost per batch = $500 per batch

Award Plus’ operating income under the alternatives of accepting/rejecting the special

order are:

Without One-

Time Only

Special Order

7,500 Units

With One–

Time Only

Special Order

10,000 Units

Difference

2,500 Units

Revenues $1,125,000 $1,375,000 $250,000

Variable costs:

Direct materials 262,500 350,0001 87,500

Direct manufacturing labor 300,000 400,0002 100,000

Batch manufacturing costs 75,000 87,5003 12,500

Fixed costs:

Fixed manufacturing costs 275,000 275,000 ––

Fixed marketing costs 175,000 175,000 ––

Total costs 1,087,500 1,287,500 200,000

Operating income $ 37,500 $ 87,500 $ 50,000

1$262,500 + ($35 2,500 units) 2$300,000 + ($40 2,500 units) 3$75,000 + ($500 25 batches)

Alternatively, we could calculate the incremental revenue and the incremental costs of the

11-6

2. Award Plus has a capacity of 9,000 medals. Therefore, if it accepts the special one-time

order of 2,500 medals, it can sell only 6,500 medals instead of the 7,500 medals that it currently

sells to existing customers. That is, by accepting the special order, Award Plus must forgo sales

of 1,000 medals to its regular customers. Alternatively, Award Plus can reject the special order

and continue to sell 7,500 medals to its regular customers.

1Award Plus makes regular medals in batch sizes of 50. To produce 6,500 medals requires 130 (6,500 ÷ 50) batches.

Accepting the special order will result in a decrease in operating income of $15,000

($37,500 – $22,500). The special order should, therefore, be rejected.

A more direct approach would be to focus on the incremental effects––the benefits of

accepting the special order of 2,500 units versus the costs of selling 1,000 fewer units to regular

3. Award Plus should not accept the special order.

Increase in operating income by selling 2,500 units

1. The expected manufacturing cost per unit of CMCBs in 2012 is as follows:

Total

Manufacturing

Costs of CMCB

(1)

Manufacturing

Cost per Unit

(2) = (1) ÷ 10,000

Direct materials, $170 10,000

Direct manufacturing labor, $45 10,000

Variable batch manufacturing costs, $1,500 80

Fixed manufacturing costs

Avoidable fixed manufacturing costs

Unavoidable fixed manufacturing costs

Total manufacturing costs

$1,700,000

450,000

120,000

320,000

800,000

$3,390,000

$170

45

12

32

80

$339

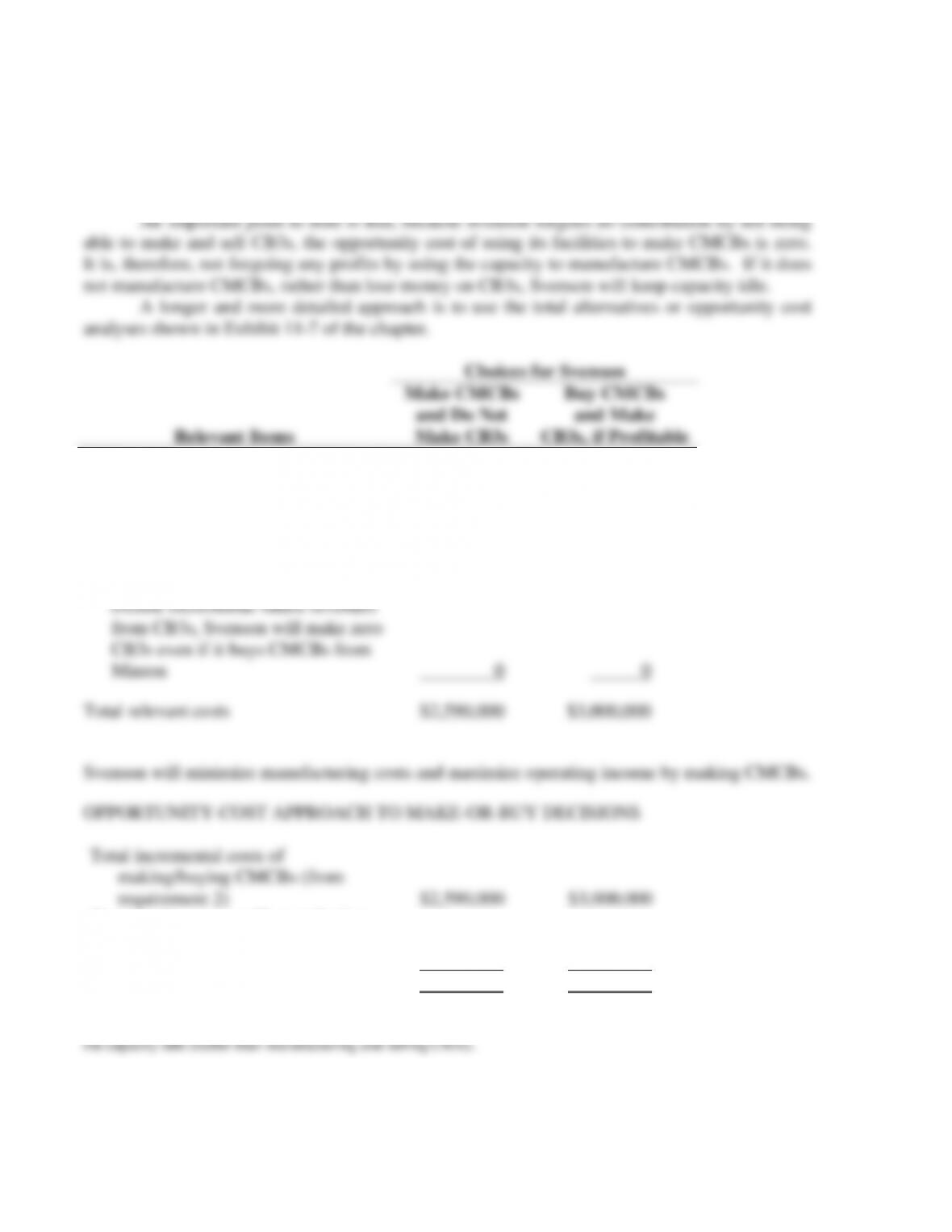

2. The following table identifies the incremental costs in 2012 if Svenson (a) made CMCBs

and (b) purchased CMCBs from Minton.

Total

Incremental Costs

Per-Unit

Incremental Costs

Incremental Items

Make

Buy

Make

Buy

Cost of purchasing CMCBs from Minton

Direct materials

Direct manufacturing labor

Variable batch manufacturing costs

Avoidable fixed manufacturing costs

Total incremental costs

$1,700,000

450,000

120,000

320,000

$2,590,000

$3,000,000

$3,000,000

$170

45

12

32

$259

$300

$300

Difference in favor of making

$410,000

$41

Note that the opportunity cost of using capacity to make CMCBs is zero since Svenson would

keep this capacity idle if it purchases CMCBs from Minton.

Svenson should continue to manufacture the CMCBs internally since the incremental

costs to manufacture are $259 per unit compared to the $300 per unit that Minton has quoted.

Note that the unavoidable fixed manufacturing costs of $800,000 ($80 per unit) will continue to

be incurred whether Svenson makes or buys CMCBs. These are not incremental costs under

either the make or the buy alternative and hence, are irrelevant.

3. Svenson should continue to make CMCBs. The simplest way to analyze this problem is

to recognize that Svenson would prefer to keep any excess capacity idle rather than use it to

make CB3s. Why? Because expected incremental future revenues from CB3s, $2,000,000, are

less than expected incremental future costs, $2,150,000. If Svenson keeps its capacity idle, we

know from requirement 2 that it should make CMCBs rather than buy them.

11-21 (10 min.) Inventory decision, opportunity costs.

1. Unit cost, orders of 22,000 $7.00

Unit cost, order of 264,000 (0.98 $7.00) $6.86

Alternatives under consideration:

3. The following table presents the two alternatives:

Alternative A:

Purchase

264,000

spark plugs at

beginning of

year

(1)

Alternative B:

Purchase

22,000

spark plugs

at beginning

of each month

(2)

Difference

(3) = (1) – (2)

Annual purchase-order costs

(1 $260; 12 $260)

Annual purchase (incremental) costs

(264,000 $6.86; 264,000 $7)

Annual interest income that could be earned

if investment in inventory were invested

(opportunity cost)

(10% $905,520; 10% $77,000)

Relevant costs

$ 260

1,811,040

90,552

$1,901,852

$ 3,120

1,848,000

7,700

$1,858,820

$ (2,860)

(36,960)

82,852

$43,032

Column (3) indicates that purchasing 22,000 spark plugs at the beginning of each month is

preferred relative to purchasing 264,000 spark plugs at the beginning of the year because the

opportunity cost of holding larger inventory exceeds the lower purchasing and ordering costs. If

other incremental benefits of holding lower inventory such as lower insurance, materials

handling, storage, obsolescence, and breakage costs were considered, the costs under Alternative

A would have been higher, and Alternative B would be preferred even more.

11-10

1.

Cola

Lemonade

Punch

Natural

Orange

Juice

Selling price $18.75 $20.50 $27.75 $39.30

2. The argument fails to recognize that shelf space is the constraining factor. There are only

12 feet of front shelf space to be devoted to drinks. Sexton should aim to get the highest daily

Cola

Lemonade

Punch

Natural

Orange

Juice

Contribution margin per case $ 5.00 $ 4.90 $ 7.05 $ 8.90

Sales (number of cases) per foot

of shelf space per day 22 12 6 13

Daily contribution per foot

of front shelf space $110.00 $58.80 $42.30 $115.70

3. The allocation that maximizes the daily contribution from soft drink sales is:

Daily Contribution

Feet of

per Foot of

Total Contribution

Shelf Space

Front Shelf Space

Margin per Day

Natural Orange Juice

6

$115.70

$ 694.20

Cola

4

110.00

440.00

Lemonade

1

58.80

58.80

Punch

1

42.30

42.30

$1,235.30