12-1

CHAPTER 12

PRICING DECISIONS AND COST MANAGEMENT

1. Customers

3. Costs

12-2 Not necessarily. For a one-time–only special order, the relevant costs are only those costs

1. Pricing for a one-time–only special order with no long-term implications.

12-4 Activity-based costing helps managers in pricing decisions in two ways.

2. It helps managers to manage costs during value engineering by identifying the cost impact

of eliminating, reducing, or changing various activities.

1. Market-based pricing, an important form of which is target pricing. The market–based

2. Cost-based pricing which asks, “What does it cost us to make this product and, hence,

what price should we charge that will recoup our costs and achieve a target return on investment?”

unit.

12-7 Value engineering is a systematic evaluation of all aspects of the value-chain business

12-8 A value-added cost is a cost that customers perceive as adding value, or utility, to a

product or service. Examples are costs of materials, direct labor, tools, and machinery. A

12-9 No. It is important to distinguish between when costs are locked in and when costs are

incurred, because it is difficult to alter or reduce costs that have already been locked in.

12-2

12-10 Cost-plus pricing is a pricing approach in which managers add a markup to cost in order to

determine price.

12-11 Cost-plus pricing methods vary depending on the bases used to calculate prices. Examples

1. The difference in prices charged for a telephone call, hotel room, or car rental during busy

versus slack periods is often much greater than the difference in costs to provide these services.

2. The difference in costs for an airplane seat sold to a passenger traveling on business or a

passenger traveling for pleasure is roughly the same. However, airline companies price

12-14 Three benefits of using a product life-cycle reporting format are:

2. Differences among products in the percentage of total costs committed at early stages in

the life cycle are highlighted.

12-15 Predatory pricing occurs when a business deliberately prices below its costs in an effort to

drive competitors out of the market and restrict supply, and then raises prices rather than enlarge

12-3

1. Relevant revenues, $4.00 1,000 $4,000

Relevant costs

Direct materials, $1.60 1,000 $1,600

Direct manufacturing labor, $0.90 1,000 900

2. The president’s reasoning is defective on at least two counts:

excluded.

3. Key issues are:

a. Will the existing customer base demand price reductions? If this 1,000-tape order is

not independent of other sales, cutting the price from $5.00 to $4.00 can have a large

12-4

1. Analysis of special order:

Sales, 3,000 units $75 $225,000

Variable costs:

Direct materials, 3,000 units $35 $105,000

2. Whether McMahon’s decision to quote full price is correct depends on many factors. He is

incorrect if the capacity would otherwise be idle and if his objective is to increase operating

income in the short run. If the offer is rejected, San Carlos, in effect, is willing to invest $49,000 in

12-5

1. Per kilogram of hard cheese:

Milk (8 liters

$2.00 per liter)

$16

Direct manufacturing labor

5

Variable manufacturing overhead

4

Fixed manufacturing cost allocated

6

Total manufacturing cost

$31

If Colorado Mountains Dairy can get all the Holstein milk it needs, and has sufficient production

capacity, then the minimum price per kilo it should charge for the hard cheese is the variable cost

per kilo = $16 + $5 + $4 = $25 per kilo.

2. If milk is in short supply, then each kilo of hard cheese displaces 2 kilos of soft cheese

(8 liters of milk per kilo of hard cheese versus 4 liters of milk per kilo of soft cheese). Then, for

12-19 (25–30 min.) Value-added, nonvalue-added costs.

1.

Category

Examples

Value-added costs

a. Materials and labor for regular repairs

$800,000

Nonvalue-added costs

b. Rework costs

c. Expediting costs caused by work delays

g. Breakdown maintenance of equipment

Total

$ 75,000

60,000

55,000

$190,000

Gray area

d. Materials handling costs

e. Materials procurement and inspection costs

f. Preventive maintenance of equipment

Total

$ 50,000

35,000

15,000

$100,000

2. Total costs in the gray area are $100,000. Of this, we assume 65%, or $65,000, are value–

added and 35%, or $35,000, are nonvalue-added.

12-7

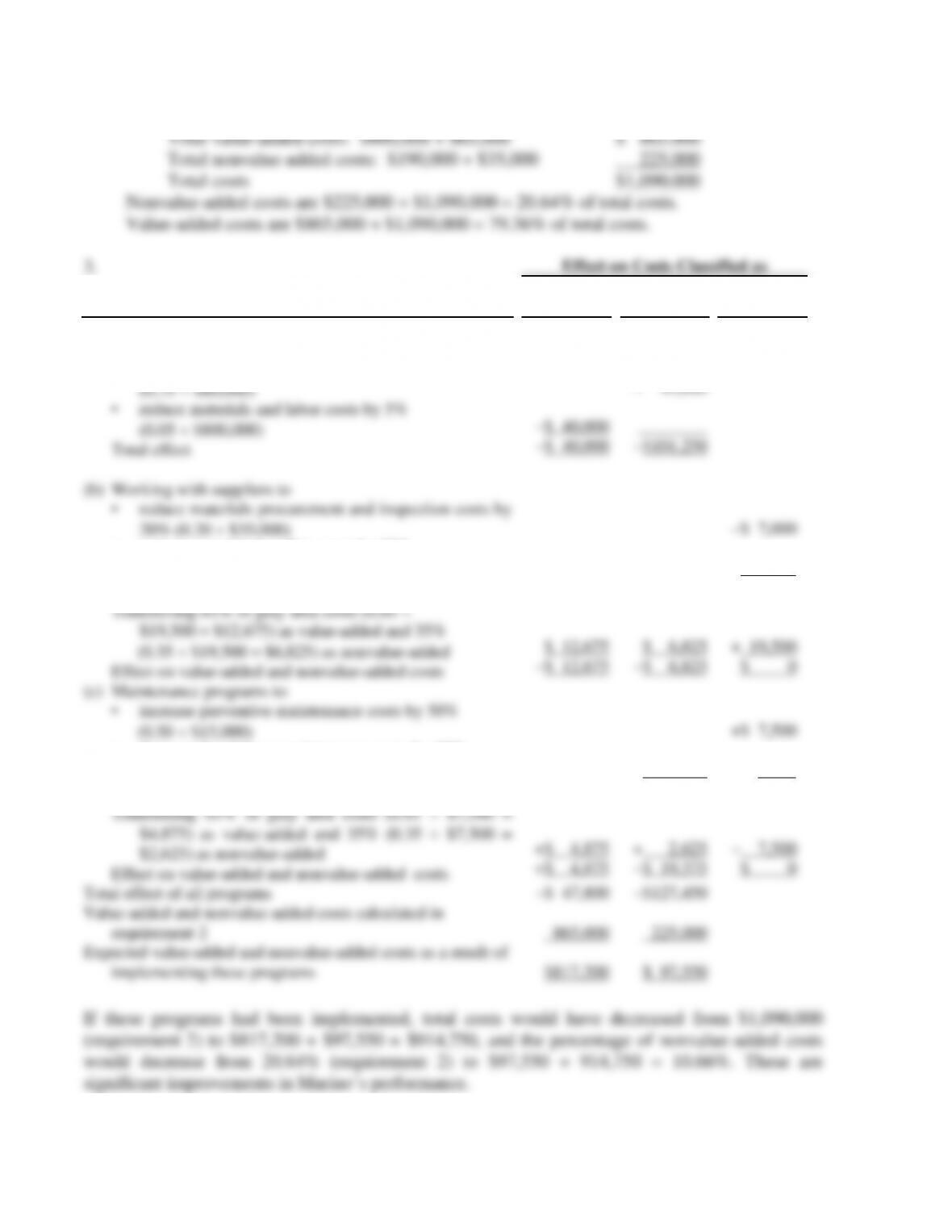

1. The classification of total costs in 2012 into value-added, nonvalue-added, or in the gray

area in between follows:

Value Gray Nonvalue- Total

Added Area added (4) =

(1) (2) (3) (1)+(2)+(3)

Total professional labor costs 319,800 11,700 58,500 390,000

Administrative and support costs at 44%

($171,600 ÷ $390,000) of professional

labor costs 140,712 5,148 25,740 171,600

Travel 15,000 — 15,000

2. Reduction in professional labor–hours by

a. Correcting errors in drawings (8% × 7,500) 600 hours

b. Correcting errors to conform to building code (7% × 7,500) 525 hours

12-8

3. Currently 85% × 7,500 hours = 6,375 hours are billed to clients generating revenues of

$701,250. The remaining 15% of professional labor-hours (15% × 7,500 = 1,125 hours) is lost in

making corrections. Calvert bills clients at the rate of $701,250 ÷ 6,375 = $110 per professional

labor-hour. If the 1,125 professional labor-hours currently not being billed to clients were billed to

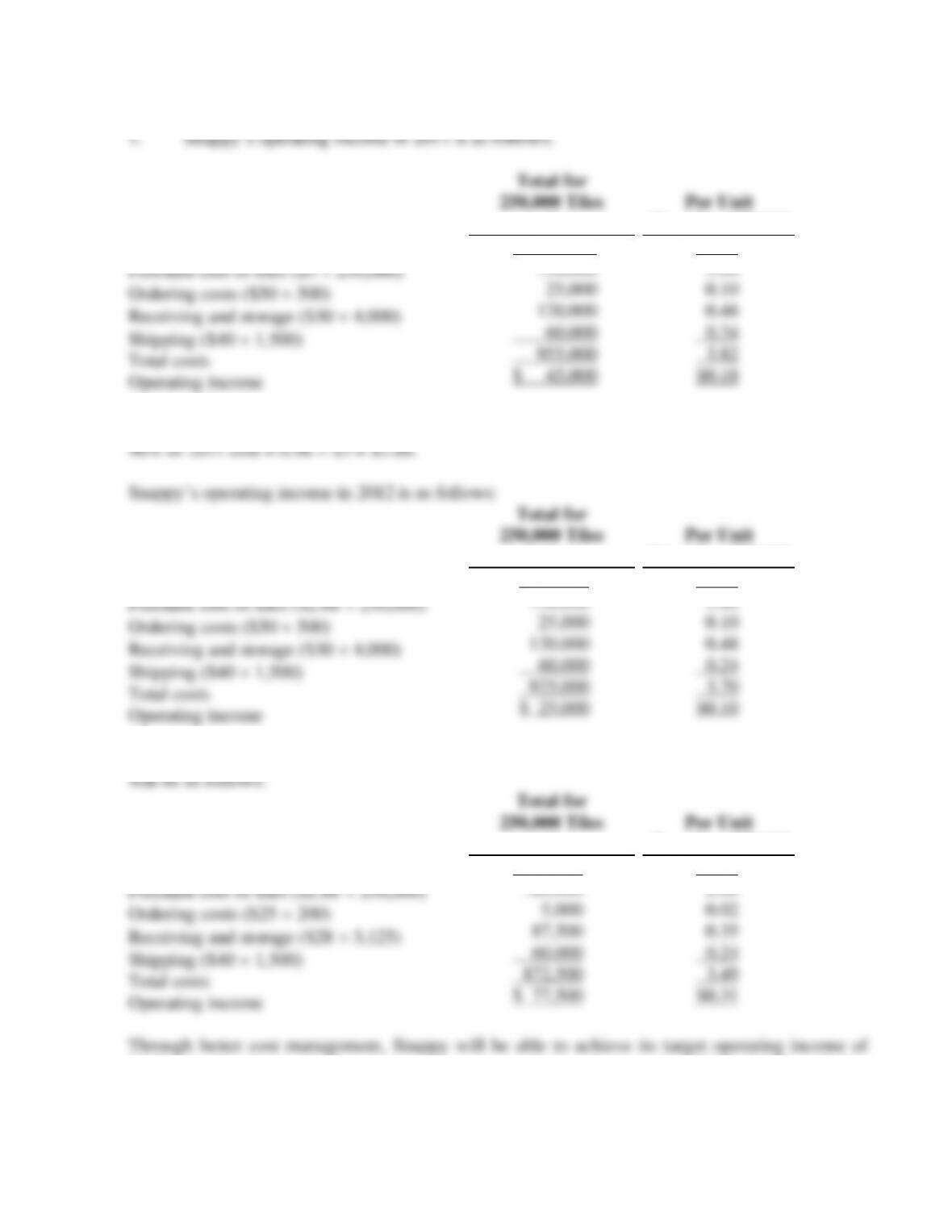

12-21 (25–30 min.) Target prices, target costs, activity-based costing.

12-10

12-22 (20 min.) Target costs, effect of product-design changes on product costs.

1. and 2. Manufacturing costs of HJ6 in 2010 and 2011 are as follows:

2010 2011

Per Unit Per Unit

Total (2) = Total (4) =

3.

Target manufacturing cost

per unit of HJ6 in 2011

=

Manufacturing cost

per unit in 2010

× 90%

4. To reduce the manufacturing cost per unit in 2011, Medical Instruments reduced the cost

per unit in each of the four cost categories—direct materials costs, batch-level costs,

manufacturing operations costs, and engineering change costs. It also reduced machine-hours and