5-32 (50 min.) Plantwide, department, and activity-cost rates.

1. Plant-wide costing rate

Fighters

Cargo

Total

Direct materials

Assembly

$2.50

$3.75

$6.25

Painting

0.50

1.00

1.50

Total

$3.00

$4.75

$7.75

Direct Labor

Assembly

$3.50

$2.00

$5.50

Painting

2.25

1.50

3.75

Total

$5.75

$3.50

$9.25

Fighters

Cargo

Total

Direct materials

($3.00 × 800 units; $4.75 × 740 units)

$2,400

$3,515

$ 5,915

Direct manufacturing labor

($5.75 × 800 units; $3.50 × 740 units)

4,600

2,590

7,190

Total direct costs

$7,000

$6,105

$13,105

Total direct costs

Overhead allocated (0.85311 × $7,000; $6,105)

Total costs

Divided by number of units

740

Total cost per unit

Budgeted

overhead rate

Painting Dept.

Budgeted Painting Department overhead costs

Budgeted Painting Department direct costs

=

$4,150

$2.75 × 800 units + $2.50 740 units

=

$4,150 $4,150 $1.02469 per direct cost dollar

$2,200 $1,850 $4,050

= = =

+

Fighters

Cargo

Total

Direct materials

$ 2,400

$ 3,515

$ 5,915

Direct manufacturing labor

4,600

2,590

7,190

Total direct costs

7,000

6,105

13,105

Allocated overhead:

Assembly Department

(1.64252 $2,800a; $1,480a)

4,599

2,431

7,030

Painting Department

(1.02469 $2,200b; $1,850b)

2,254

1,896

4,150

Total costs

$13,853

$10,432

$24,285

Divided by number of units

800

740

$ 17.32

$ 14.10

aDirect manufacturing labor costs in Assembly Department calculated previously:

3. Activity-based Costing

Assembly Department

Budgeted

materials

handling rate

$1,700 $8.58586 per batch

198 batches

==

Painting Department

Budgeted

materials

handling rate

$900 $6.81818 per batch

132 batches

==

132 batches

5-34

5-33 (30-40 min.) Department and activity-cost rates service sector.

1. Overhead costs = $19,000 + $260,000 + $267,900 + $121,200 = $668,100

Budgeted overhead rate

=

$668,100 $1.70 per direct labor dollar

$393,000 =

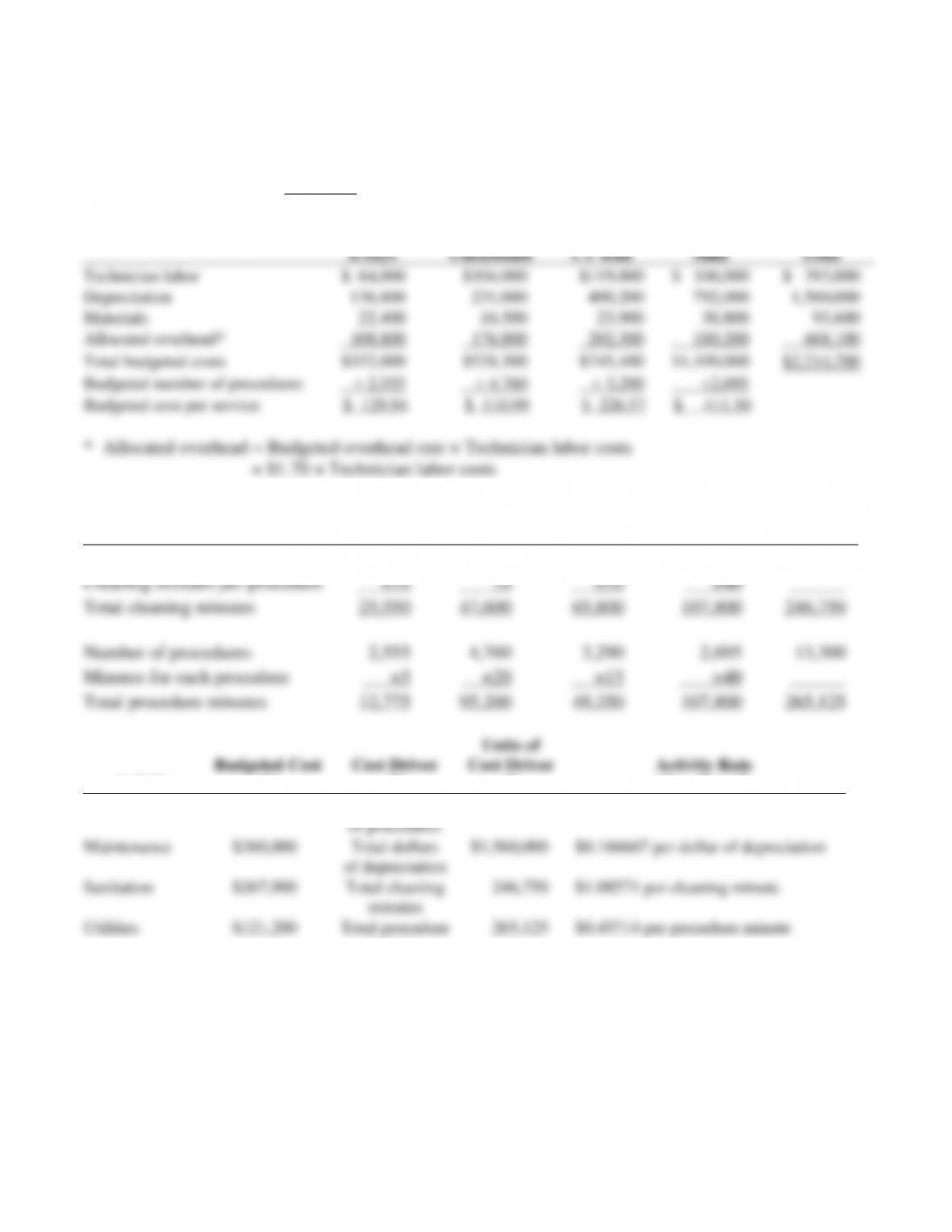

X-rays

Ultrasound

CT scan

MRI

Total

Technician labor

$ 64,000

$104,000

$119,000

$ 106,000

$ 393,000

Depreciation

136,800

231,000

400,200

792,000

1,560,000

Materials

22,400

16,500

23,900

30,800

93,600

Allocated overhead*

108,800

176,800

202,300

180,200

668,100

Total budgeted costs

$332,000

$528,300

$745,400

$1,109,000

$2,714,700

Budgeted number of procedures

÷ 2,555

÷ 4,760

÷ 3,290

÷2,695

Budgeted cost per service

$ 129.94

$ 110.99

$ 226.57

$ 411.50

* Allocated overhead = Budgeted overhead rate × Technician labor costs

= $1.70 × Technician labor costs

2. Budgeted Information

X-rays

Ultrasound

CT scan

MRI

Total

Number of procedures

2,555

4,760

3,290

2,695

13,300

Cleaning minutes per procedure

×10

10

×20

×40

Total cleaning minutes

25,550

47,600

65,800

107,800

246,750

Number of procedures

2,555

4,760

3,290

2,695

13,300

Minutes for each procedure

×5

×20

×15

×40

Total procedure minutes

12,775

95,200

49,350

107,800

265,125

Activity

Budgeted Cost

(1)

Cost Driver

(2)

Units of

Cost Driver

(3)

Activity Rate

(4) = (1) ÷ (3)

Administration

$ 19,000

Total number

of procedures

13,300

$1.42857 per procedure

Maintenance

$260,000

Total dollars

of depreciation

$1,560,000

$0.166667 per dollar of depreciation

Sanitation

$267,900

Total cleaning

minutes

246,750

$1.08571 per cleaning minute

Utilities

$121,200

Total procedure

minutes

265,125

$0.45714 per procedure minute

5-35

X-rays

Ultrasound

CT Scan

MRI

Total

Technician labor

$ 64,000

$104,000

$119,000

$ 106,000

$ 393,000

Depreciation

136,800

231,000

400,200

792,000

1,560,000

Materials

22,400

16,500

23,900

30,800

93,600

Allocated activity costs:

Administration

($1.42857 × 2,555; 4,760; 3,290;

2,695)

3,650

6,800

4,700

3,850

19,000

Maintenance

$0.166667 × $136,800; $231,000;

$400, 200; $792,000)

22,800

38,500

66,700

132,000

260,000

Sanitation

($1.08571 × 25,550; 47,600; 65,800;

107,800)

27,740

51,680

71,440

117,040

267,900

Utilities

($0.45714 × 12,775; 95,200; 49,350;

107,800)

5,840

43,520

22,560

49,280

121,200

Total budgeted cost

$283,230

$492,000

$708,500

$1,230,970

$2,714,700

Budgeted number of procedures

÷ 2,555

÷ 4,760

÷ 3,290

÷ 2,695

Budgeted cost per service

$ 110.85

$ 103.36

$ 215.35

$ 456.76

3. Using the disaggregated activity-based costing data, managers can see that the MRI actually

costs substantially more and x-rays and ultrasounds substantially less than the traditional system

5-36

1. Direct costs = Dance teacher salaries, Child care teacher salaries, Fitness instructor salaries

2.

Indirect Cost

Cost Driver

Budgeted Cost Driver Rate

Supplies

Number of participants

$21,984 ÷ 2,205 = $9.97 per participant

Rent, maintenance, and utilities

Square footage

$97,511÷ 11,650 = $8.37 per square foot

Administration salaries

Number of participants

$50,075 ÷ 2,205 = $22.71 per participant

Marketing expenses

Number of advertisements

$21,000 ÷ 70 = $300 per advertisement

3.

Dance

Childcare

Fitness

Total

Salaries

$ 62,100

$ 24,300

$ 39,060

$ 125,460

Allocated costs:

Supplies

($9.97×1,485; 450; 270)

14,805

4,487

2,692

21,984

Rent, maintenance, and utilities

($8.37×6,000; 3,150; 2,500)

50,220

26,366

20,925

97,511

Administration salaries

($22.71×1,485; 450; 270)

33,724

10,219

6,132

50,075

Marketing expenses

($300×26; 24; 20)

7,800

7,200

6,000

21,000

Budgeted total costs

$ 168,649

$ 72,572

$ 74,809

$ 316,030

÷ Number of participants

÷ 1,485

÷450

÷270

Budgeted cost per participant

$ 113.57

$ 161.27

$ 277.07

4. By dividing the full cost of each service line by the number of participants, Annie can see that

fitness classes should be charged a higher price. Most of the higher unit cost is attributable to the

5-37

1.

General

Supermarket

Chains

Drugstore

Chains

Mom-and-Pop

Single

Stores

Total

Revenues $3,708,000 $3,150,000 $1,980,000 $8,838,000

2. The per-unit cost driver rates are:

2. Line item ordering,

$63,840 ÷ 21,280 (1,960 + 4,320 + 15,000) line items = $ 3 per line item

4. Cartons shipped,

$76,000 ÷ 76,000 (36,000 + 24,000 + 16,000) cartons = $ 1 per carton

3. The activity-based costing of each distribution market for 2011 is:

General

Supermarket

Chains

Drugstore

Chains

Mom-and-

Pop

Single Stores

Total

1. Customer purchase order processing

($40 140; 360; 1,500)

$ 5,600

$14,400

$ 60,000

$ 80,000

2. Line item ordering

($3 1,960; 4,320; 15,000)

5,880

12,960

45,000

63 ,840

3. Store delivery,

($47.973 120; 360; 1,000)

5,757

17,270

47,973

71,000

4. Cartons shipped

($1 36,000; 24,000; 16,000)

36,000

24,000

16,000

76,000

5. Shelf-stocking

($16 360; 180; 100)

5,760

2,880

1,600

10,240

$58,997

$71,510

$170,573

$301,080

5-38

The revised operating income statement is:

General Mom-and-Pop

Supermarket Drugstore Single

4. The ranking of the three markets are:

Using Gross Margin Using Operating Income

2. Drugstore Chains 4.76% 2. General Supermarket Chains 1.32%

3. General Supermarket Chains 2.91% 3. Mom-and-Pop Single Stores 0.48%

The activity-based analysis of costs highlights how the Mom-and-Pop Single Stores use a larger

amount of Pharmacare’s resources per revenue dollar than do the other two markets. The ratio of

5-39

Other issues for Pharmacare to consider include

a. Choosing the appropriate cost drivers for each area. The problem gives a cost driver

for each chosen activity area. However, it is likely that over time further refinements

in cost drivers would be necessary. For example, not all store deliveries are equally

easy to make, depending on parking availability, accessibility of the storage/shelf

5-40

5-36 (30-40 min.) Choosing cost drivers, activity-based costing, activity-based

management.

1.

Direct materials—purses

Output unit-level costs

Direct materials—backpacks

Output unit-level costs

Direct manufacturing labor—purses

Output unit-level costs

Direct manufacturing labor—backpacks

Output unit-level costs

Setup

Batch-level costs

Shipping

Batch-level costs

Design

Product-sustaining costs

Plant utilities and administration

Facility-sustaining costs

2.

Direct materials—purses

Number of purses

Direct materials—backpacks

Number of backpacks

Direct manufacturing labor—purses

Number of purses

Direct manufacturing labor—backpacks

Number of backpacks

Setup

Number of batches

Shipping

Number of batches

Design

Number of designs

Plant utilities and administration

Hours of production

3.

Direct materials—purses

$379,290 ÷ 3,350 purses = $113.22 per purse

Direct materials—backpacks

$412,920 ÷ 6,050 backpacks = $68.25 per backpack

Direct manufacturing labor—purses

$98,000 ÷ 3,350 purses = $29.25 per purse

Direct manufacturing labor—backpacks

$120,000 ÷ 6,050 backpacks = $19.83 per backpack

Setup

$65,930 190 batches = $347 per batch

Shipping

$73,910 190 batches = $389 per batch

Design

$166,000 ÷ 4 designs = $41,500 per design

Plant utilities and administration

$243,000 ÷ 4,050 hours = $60 per hour