5-41

4.

Backpacks

Purses

Total

Direct materials

$412,920

$379,290

$ 792,210

Direct manufacturing labor

120,000

98,000

218,000

Setup

($347 × 130; 60 batches)

45,110

20,820

65,930

Shipping

($389 × 130; 60 batches)

50,570

23,340

73,910

Design

($41,500 × 2; 2 designs)

83,000

83,000

166,000

Plant utilities and administration

($60 × 1,450; 2,600 hours)

87,000

156,000

243,000

Budgeted total costs

$798,600

$760,450

$1,559,050

Divided by number of backpacks/purses

÷ 6,050

÷ 3,350

Budgeted cost per backpack/purse

$ 132.00

$ 227.00

5. Based on this analysis, over 50% of product cost relates to direct material. Managers should

determine whether the material costs can be reduced. Producing in small lots increases the setup

5-37 (40 min.) ABC, health care.

1a. Medical supplies rate =

years–patient ofnumber Total

costs supplies Medical

=

$220,000

110

= $2,000 per patient-year

$440,000

costs maint. clinic andRent

$126,000

food

and laundry

years–patient ofnumber Total

110

= $4,000 per patient-year

Laboratory services rate =

testslaboratory ofnumber Total

costs services Laboratory

=

$84,000

2,100

= $40 per test

5-43

1c. The ABC system more accurately allocates costs because it identifies better cost drivers.

The ABC system chooses cost drivers for overhead costs that have a cause-and-effect

relationship between the cost drivers and the costs. Of course, Clayton should continue to

evaluate if better cost drivers can be found than the ones they have identified so far.

2. The concern with using costs per patient-year as the rule to allocate resources among its

programs is that it emphasizes “input” to the exclusion of “outputs” or effectiveness of the

5-44

1.

Basketballs

Volleyballs

Total

Number of batches

300

400

700

Machine-hours

11,000

12,500

23,500

Setup cost per batch = $143,500 ÷ 700 batches = $205 per batch.

Equipment and maintenance = $109,900 ÷ 23,500 machine–hours = $4.6766 per machine-hour.

Lease rent, insurance, utilities = $216,000 ÷ 12,000 sq. ft. of capacity = $18 per sq. ft.

Capacity used for Capacity used for

2. Unused capacity Total capacity =−

basketball production volleyball production

−

12,000 3,360 5,040 3,600 sq. ft.= − − =

Cost of unused capacity = $18 per sq. ft × 3,600 sq. ft. = $64,800

3.

Basketballs

Volleyballs

Total

Direct materials

$209,750

$358,290

$ 568,040

Direct manufacturing labor

107,333

102,969

210,302

Setup

($205 × 300; 400)

61,500

82,000

143,500

Equipment and maintenance

($4.6766 × 11,000; 12,500)

51,443

58,457

109,900

Lease rent, etc.

($18 × 3,360; 5,040)

60,480

90,720

151,200

Budgeted total costs

$490,506

$692,436

$1,182,942

Divided by number of units

÷ 66,000

÷100,000

Budgeted cost per unit

$ 7.43

$ 6.92

4. Currently, Nivag only utilizes 70% of its available capacity. Managers should consider

whether the excess capacity is sufficient to produce footballs. Other issues to consider include

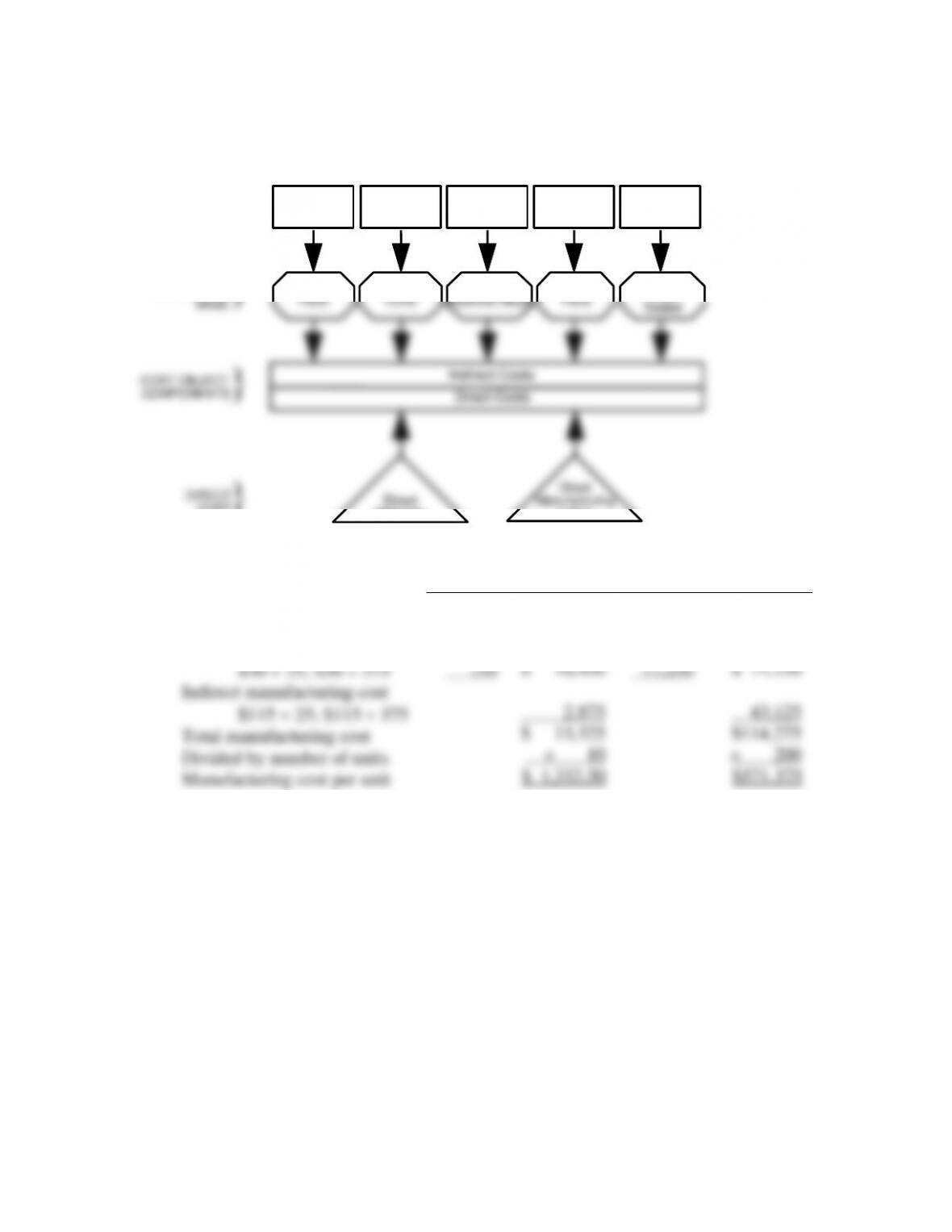

5-39 (40−50 min.) Activity-based job costing, unit-cost comparisons.

An overview of the product-costing system is:

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

DIRECT

COST

Materials

Handling

Number of

Parts

Direct

Materials

COST OBJECT:

COMPONENTS

Indirect Costs

Direct Costs

Direct

Manufacturing

Labor

Lathe

Work

Number of

Turns

Milling

Number of

Machine-Hours

Grinding

Number of

Parts

Testing

Number of

Units

Tested

1.

Job Order 410

Job Order 411

Direct manufacturing cost

Direct materials

Direct manufacturing labor

$30 25; $30 375

Indirect manufacturing cost

$115 25; $115 375

Total manufacturing cost

Divided by number of units

Manufacturing cost per unit

$9,700

750 $ 10,450

2,875

$ 13,325

÷ 10

$ 1,332.50

$59,900

11,250 $ 71,150

43,125

$114,275

÷ 200

$571.375

2.

Job Order 410

Job Order 411

Direct manufacturing cost

Direct materials

Direct manufacturing labor

$30 25; $30 375

Indirect manufacturing cost

Materials handling

$0.40 500; $0.40 2,000

Lathe work

$0.20 20,000; $0.20 59,250

Milling

$20.00 150; $20.00 1,050

Grinding

$0.80 500; $0.80 2,000

Testing

$15.00 10; $15.00 200

Total manufacturing cost

Divided by number of units

Manufacturing cost per unit

$9,700

750 $10,450

200

4,000

3,000

400

150 7,750

$18,200

÷ 10

$ 1,820

$59,900

11,250 $ 71,150

800

11,850

21,000

1,600

3,000 38,250

$109,400

÷ 200

$ 547

3.

Job Order 410

Job Order 411

Number of units in job 10 200

Costs per unit with prior costing system $1,332.50 $571.375

Costs per unit with activity-based costing 1,820.00 547