20-1

CHAPTER 20

20-1 Cost of goods sold (in retail organizations) or direct materials costs (in organizations with

a manufacturing function) as a percentage of sales frequently exceeds net income as a percentage

1. purchasing costs;

3. carrying costs;

5. costs of quality; and

20-3 Five assumptions made when using the simplest version of the EOQ model are:

2. Demand, ordering costs, carrying costs, and the purchase-order lead time are certain.

4. No stockouts occur.

20-4 Costs included in the carrying costs of inventory are incremental costs for such items as

20-5 Examples of opportunity costs relevant to the EOQ decision model but typically not

recorded in accounting systems are the following:

2. lost contribution margin on existing sales when a stockout occurs; and

20-6 The steps in computing the costs of a prediction error when using the EOQ decision

model are:

20-2

20-7 Goal congruence issues arise when there is an inconsistency between the EOQ decision

20-8 Just-in-time (JIT) purchasing is the purchase of materials (or goods) so that they are

20-9 Factors causing reductions in the cost to place purchase orders of materials are:

• Companies are establishing long-run purchasing agreements that define price and

20-10 Disagree. Choosing the supplier who offers the lowest price will not necessarily result in

the lowest total purchase cost to the buyer. This is because the price or purchase cost of the

20-11 Supply-chain analysis describes the flow of goods, services, and information from the

initial sources of materials and services to the delivery of products to consumers, regardless of

20-12 Just-in-time (JIT) production is a “demand–pull” manufacturing system that has the

following features:

manner.

20-13 Traditional normal and standard costing systems use sequential tracking, in which journal

entries are recorded in the same order as actual purchases and progress in production, typically at

20-3

20-14 Versions of backflush costing differ in the number and placement of trigger points at

which journal entries are made in the accounting system:

Number of

Journal Entry

Trigger Points

Location in Cycle Where

Journal Entries Made

Version 1

3

Stage A. Purchase of direct materials and incurring of

conversion costs

Stage C. Completion of good finished units of product

Stage D. Sale of finished goods

Version 2

2

Stage A. Purchase of direct materials and incurring of

conversion costs

Stage D. Sale of finished goods

Version 3

2

Stage C. Completion of good finished units of product

Stage D. Sale of finished goods

20-15 Traditional accounting systems cost individual products, and separate product costs from

selling, general, and administrative costs. Lean accounting costs the entire value stream instead

20-16 (20 min.) Economic order quantity for retailer.

1. D = 10,000 jerseys per year, P = $200, C = $7 per jersey per year

200$000,102

DP 2

3.

day working each Demand

=

days workingofNumber

D

=

365

000,10

= 27.40 jerseys per day

1. D = 10,000 jerseys per year, P = $30, C = $7 per jersey per year

30$000,102

DP 2

20-5

20-19 (20 min.) EOQ for manufacturer.

1. Relevant carrying costs per part per year:

Required annual return on investment 15% $60 = $ 9

Relevant insurance, materials handling, breakage, etc.

2.

Relevant annual

ordering costs

=

D P

Q

$150

000,18

3. At the EOQ, total relevant ordering costs and total relevant carrying costs will be exactly

equal. Therefore, total relevant carrying costs at the EOQ = $4,500 (from requirement 2). We

4. Purchase order lead time is half a month.

Monthly demand is 18,000 units ÷ 12 months = 1,500 units per month.

20-6

20-20 (20 min.) Sensitivity of EOQ to changes in relevant ordering and carrying costs.

1. A straightforward approach to the requirement is to construct the following table for

EOQ at relevant carrying and ordering costs. Annual demand is 10,000 units. The formula for the

EOQ model is:

EOQ =

2DP DP QC

and for Relevant Total Costs (RTC) =

C Q 2

+

$40 224 2

2. For a given demand level, as relevant carrying costs increase and relevant ordering costs

3. If Alpha estimates C = $10 per unit per year and P = $400 per order, then from

requirement 1,

EOQ = 224 units and Relevant Total Cost (RTC) = $8,944

20-7

20-21 (15 min.) Inventory management and the balanced scorecard.

1. The incremental increase in operating profits from employee cross-training (ignoring the cost

of the training) is:

2. At a cost of $600,000, DSC will be indifferent between current expenditures and increasing

3. Besides increasing short-term operating profits, additional employee cross-training can

improve employee satisfaction because their jobs can have more variety, potentially leading to

20-8

20-22 (20 min.) JIT production, relevant benefits, relevant costs.

2. Other nonfinancial and qualitative factors that Champion should consider in deciding

whether it should implement a JIT system include:

a. The possibility of developing and implementing a detailed system for integrating the

sequential operations of the manufacturing process. Direct materials must arrive when

needed for each subassembly so that the production process functions smoothly.

for Champion Hardware Company

Relevant Items

Relevant

Costs under

Current

Production

System

Relevant

Costs under

JIT

Production

System

Annual tooling costs

–

$100,000

Required return on investment:

15% per year $1,000,000 of average inventory per year

$150,000

15% per year $200,000a of average inventory per year

30,000

Insurance, space, materials handling, and setup costs

300,000

225,000b

Rework costs

200,000

140,000c

Incremental revenues from higher selling prices

–

(160,000)d

Total net incremental costs

$650,000

$335,000

20-9

3. Personal observation by production line workers and managers is more effective in JIT

plants than in traditional plants. A JIT plant’s production process layout is streamlined.

Operations are not obscured by piles of inventory or rework. As a result, such plants are easier to

evaluate by personal observation than cluttered plants where the flow of production is not

logically laid out.

20-10

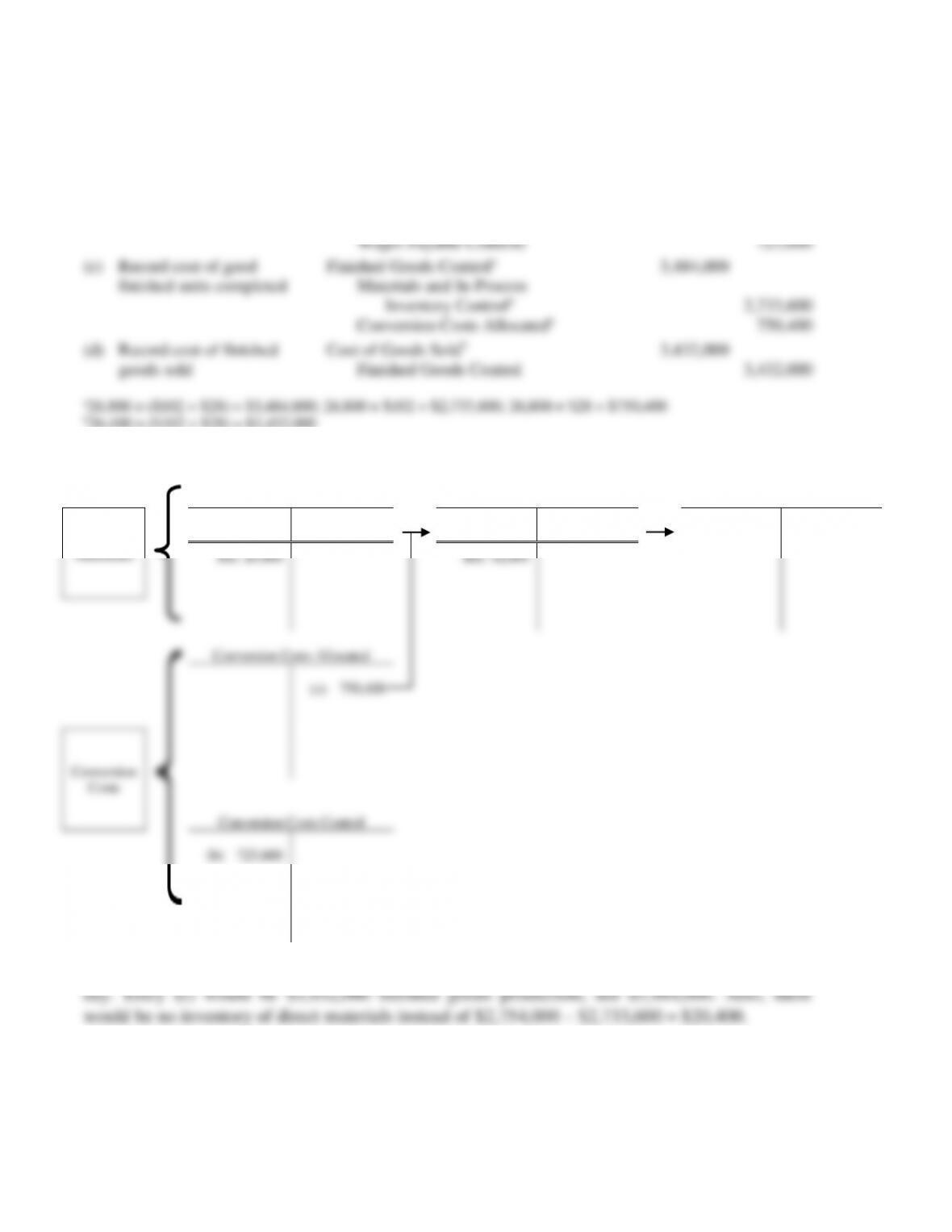

20-23 (30 min.) Backflush costing and JIT production.

1.

(a) Record purchases of

direct materials

Materials and In-Process Inventory Control

Accounts Payable Control

2,754,000

2,754,000

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

723,600

Wages Payable Control)

723,600

(c) Record cost of good

finished units completed

Finished Goods Controla

Materials and In-Process

3,484,000

Inventory Controla

2,733,600

Conversion Costs Allocateda

750,400

(d) Record cost of finished

goods sold

Cost of Goods Soldb

Finished Goods Control

3,432,000

3,432,000

2.

Materials and In-Process

Inventory Control

Finished Goods Control

Cost of Goods Sold

Direct

Materials

(a) 2,754,000

(c) 2,733,600

(c) 3,484,000

(d) 3,432,000

(d) 3,432,000

Bal. 20,400

Bal. 52,000

Conversion Costs Allocated

(c) 750,400

Conversion

Costs

Conversion Costs Control

(b) 723,600

3. Under an ideal JIT production system, there would be zero inventories at the end of each