4-33 (25–30 min.) Service industry, job costing, two direct– and indirect-cost categories,

law firm (continuation of 4-32).

Although not required, the following overview diagram is helpful to understand Keating’s job–

costing system.

Professional

Labor-Hours

General

Support

COST OBJECT:

JOB FOR

CLIENT

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

}

DIRECT

COST

Indirect Costs

Direct Costs

Partner

Labor-Hours

Secretarial

Support

Professional

Associate Labor

Professional

Partner Labor

1.

Professional

Partner Labor

Professional

Associate Labor

Budgeted compensation per professional

Divided by budgeted hours of billable

time per professional

Budgeted direct-cost rate

$ 200,000

÷1,600

$125 per hour*

$80,000

÷1,600

$50 per hour†

*Can also be calculated as

Total budgeted partner labor costs

Total budgeted partner labor – hours

=

$200,000 5

1,600 5

=

000,8

$1,000,000

= $125

†Can also be calculated as

Total budgeted associate labor costs

Total budgeted associate labor –hours

=

$80,000 20

1,600 20

=

$1,600,000

32 000,

= $ 50

2.

General

Support

Secretarial

Support

Budgeted total costs

Divided by budgeted quantity of allocation base

Budgeted indirect cost rate

$1,800,000

÷ 40,000 hours

$45 per hour

$400,000

÷ 8,000 hours

$50 per hour

4-32

3.

Richardson

Punch

Direct costs:

Professional partners,

$125 60 hr.; $125 30 hr.

Professional associates,

$50 40 hr.; $50 120 hr.

Direct costs

Indirect costs:

General support,

$45 100 hr.; $45 150 hr.

Secretarial support,

$50 60 hr.; $50 30 hr.

Indirect costs

Total costs

$7,500

2,000

$ 9,500

4,500

3,000

7,500

$17,000

$3,750

6,000

$ 9,750

6,750

1,500

8,250

$18,000

4.

Richardson

Punch

Single direct – Single indirect

(from Problem 4-32)

Multiple direct – Multiple indirect

(from requirement 3 of Problem 4-33)

Difference

$12,000

17,000

$ 5,000

undercosted

$18,000

18,000

$ 0

no change

The Richardson and Punch jobs differ in their use of resources. The Richardson job has a

mix of 60% partners and 40% associates, while Punch has a mix of 20% partners and 80%

associates. Thus, the Richardson job is a relatively high user of the more costly partner-related

resources (both direct partner costs and indirect partner secretarial support). The Punch job, on

the other hand, has a mix of partner and associate-related hours (1 : 4) that exactly equals the mix

of partner and associate hours for the firm as a whole. The refined-costing system in Problem 4–

33 increases the reported cost in Problem 4-32 for the Richardson job by 41.7% (from $12,000 to

$17,000) while it happens to correctly cost the Punch job.

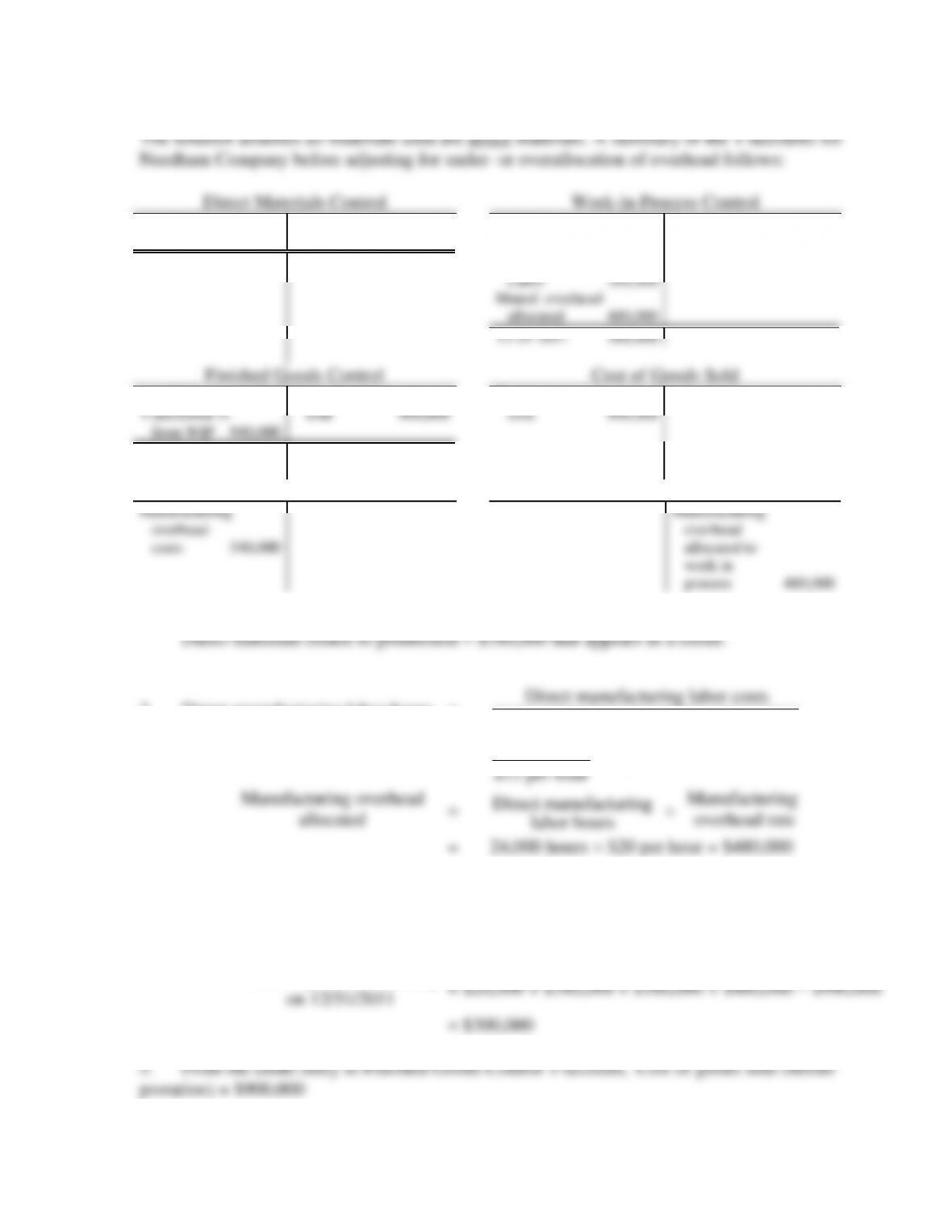

1. Budgeted manufacturing overhead rate is $4,800,000 ÷ 80,000 hours = $60 per machine-hour.

2.

Manufacturing overhead

underallocated

=

Manufacturing overhead

incurred

–

Manufacturing overhead

allocated

= $4,900,000 – $4,500,000*

= $400,000

4-34

3. Alternative (c) is theoretically preferred over (a) and (b) because the underallocated

amount and the balances in work–in-process and finished goods inventories are material.

rate.

4-35 (15 min.) Normal costing, overhead allocation, working backward.

1a. Manufacturing overhead allocated = 200% × Direct manufacturing labor cost

$3,600,000 = 2 × Direct manufacturing labor cost

$3,600,000

2.

Work in process

1/1/2011

+

Total

manufacturing cost

=

Cost of goods

manufactured

+

Work in process

12/31/2011

4-36 (40 min.) Proration of overhead with two indirect cost pools.

1. a. Molding department:

1. b. Painting department:

Overhead allocated = $2,306 + $1,897 + $24,982 = $29,185

Underallocated overhead = Actual overhead costs – Overhead allocated

Account

Account Balance

(Before Proration)

(1)

Proration of $1,500

Underallocated

Overhead

(2)

Account Balance

(After Proration)

(3) = (1) + (2)

WIP

$ 27,720.00

0

$ 27,720.00

Finished Goods

15,523.20

0

15,523.20

Cost of Goods Sold

115,156.80

–$800 + $2,300

116,656.80

Total

$158,400.00

$ 1,500

$159,900.00

2b. Underallocated overhead prorated based on ending balances

Account

Account

Balance

(Before

Proration)

(1)

Account Balance

as a Percent of Total

(2) = (1) ÷ $2,000,000

Proration of $1,500

Underallocated Overhead

(3) = (2)

10,000

Account

Balance

(After

Proration)

(4) = (1) + (3)

WIP

$ 27,720.00

0.175

0.175

$1,500 = $ 262.50

$ 27,982.50

Finished Goods

15,523.20

0.098

0.098

$1,500 = 147.00

15,670.20

Cost of Goods Sold

115,156.80

0.727

0.727

$1,500 = 1,090.50

116,247.30

Total

$158,400.00

1.000

$1,500.00

$159,900.00

2c. Under/overallocated overhead prorated based on overhead in ending balances. (Note:

overhead must be allocated separately from each department. This can be done using the number

of machine hours/direct labor hours as a surrogate for overhead in ending balances.)

For Molding department:

Account

Allocated Overhead

in Account Balance

(1)

Allocated Overhead in

Account Balance

as a Percent of Total

(2) = (1) ÷ $18,048

Proration of $800

Overallocated

Overhead

(3) = (2)

$800

WIP

$ 4,602

0.255

0.255

$800 = $204.00

Finished Goods

957

0.053

0.053

$800 = 42.40

Cost of Goods Sold

12,489

0.692

0.692

$800 = 553.60

Total

$18,048

1.000

$800.00

For finishing department:

Account

Allocated Overhead

in Account Balance

(4)

Allocated Overhead

in Account Balance

as a Percent of Total

(5) = (4) ÷ $29,185

Proration of $2,300

Underallocated Overhead

(6) = (5)

$2,300

WIP

$ 2,306

0.079

0.079

$2,300 = $ 181.70

Finished Goods

1,897

0.065

0.065

$2,300 = 149.50

Cost of Goods Sold

24,982

0.856

0.856

$2,300 = 1,968.80

Total

$29,185

1.000

$2,300.00

Account

Account Balance

(Before Proration)

(7)

Underallocated/

Overallocated

Overhead

(8) = (3) – (6)

Account Balance

(After Proration)

(9) = (7) + (8)

WIP

$27,720.00

–$204 + $181.70 = $ (22.30)

$ 27,697.70

Finished Goods

15,523.20

–$42.40 + $149.50 = 107.10

15,630.30

Cost of Goods Sold

115,156.80

–$553.60 + $1,968.80 = 1,415.20

116,572.00

Total

$158,400.00

$1,500.00

$159,900.00

3. The first method is simple and Cost of Goods Sold accounts for almost 73% of the three

4-37 (35 min.) General ledger relationships, under- and overallocation.

6.

Manufacturing overhead

underallocated

=

Debits to Manufacturing

Overhead Control

–

Credit to Manufacturing

Overhead Allocated

7. a. Write-off to Cost of Goods Sold will increase (debit) Cost of Goods Sold by $60,000.

Hence, Cost of Goods Sold = $900,000 + $60,000 = $960,000.