15-11

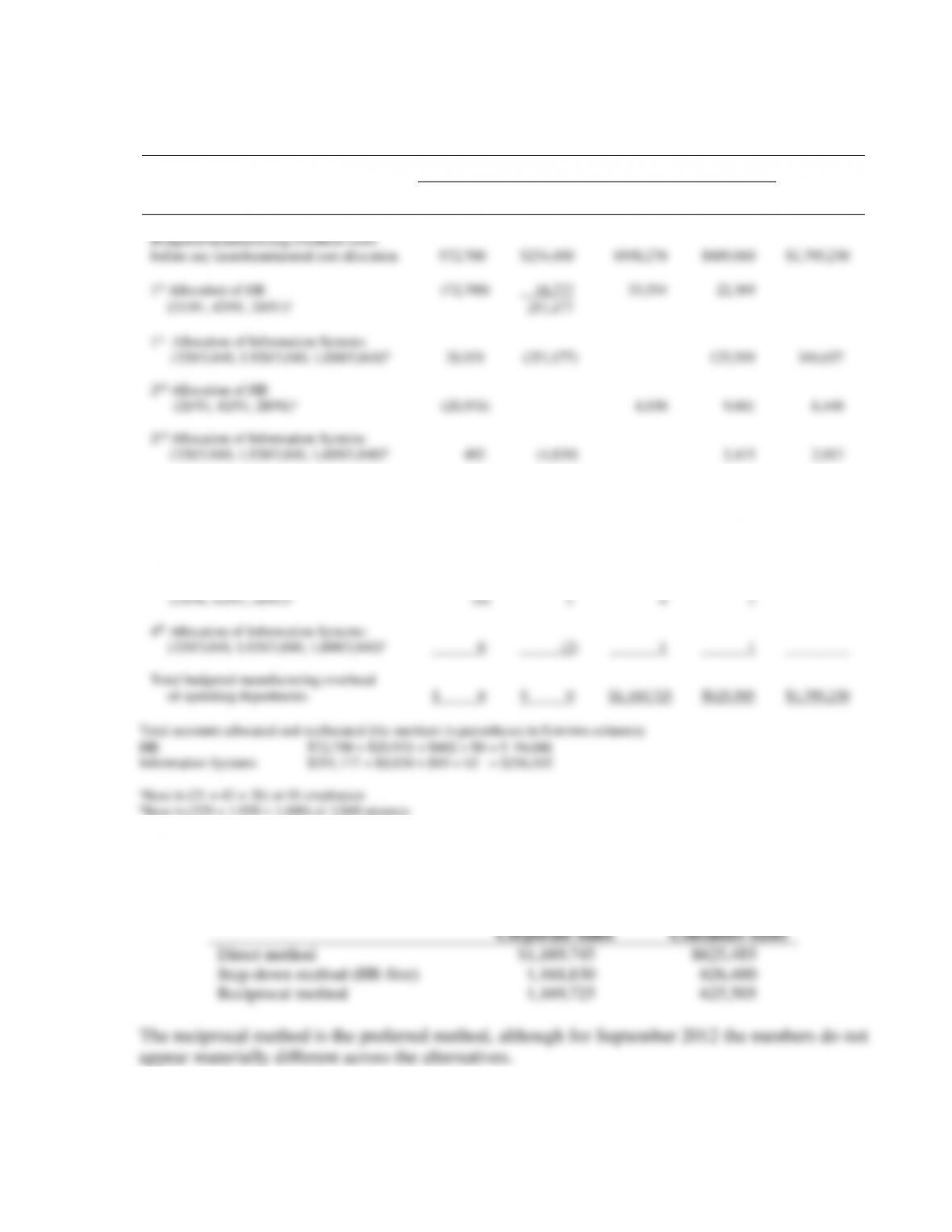

SOLUTION EXHIBIT 15-22

Reciprocal Method of Allocating Support Department Costs for September 2012 at

E-books Using Repeated Iterations

Support Departments

Operating Departments

Human

Resources

Information

Systems

Corporate

Sales

Consumer

Sales

Total

Budgeted manufacturing overhead costs

before any interdepartmental cost allocation

$72,700

$234,400

$998,270

$489,860

$1,795,230

1st Allocation of HR

(72,700)

16,777

33,554

22,369

(21/91, 42/91, 28/91)a

251,177

1st Allocation of Information Systems

(320/3,840, 1,920/3,840, 1,600/3,840)b

20,931

(251,177)

125,589

104,657

2nd Allocation of HR

(21/91, 42/91, 28/91)a

(20,931)

4,830

9,661

6,440

2nd Allocation of Information Systems

(320/3,840, 1,920/3,840, 1,600/3,840)b

402

(4,830)

2,415

2,013

3rd Allocation of HR

(21/91, 42/91, 28/91)a

(402)

93

185

124

3rd Allocation of Information Systems

(320/3,840, 1,920/3,840, 1,600/3,840)b

8

(93)

46

39

4th Allocation of HR

(21/91, 42/91, 28/91)a

(8)

2

4

2

4th Allocation of Information Systems:

(320/3,840, 1,920/3,840, 1,600/3,840)b

0

(2)

1

1

_________

Total budgeted manufacturing overhead

of operating departments

$ 0

$ 0

$1,169,725

$625,505

$1,795,230

Total accounts allocated and reallocated (the numbers in parentheses in first two columns)

HR $72,700 + $20,931 + $402 + $8 = $ 94,041

Information Systems $251,177 + $4,830 + $93 + $2 = $256,102

aBase is (21 + 42 + 28) or 91 employees

bBase is (320 + 1,920 + 1,600) or 3,840 minutes

3. The reciprocal method is more accurate than the direct and step-down methods when there

are reciprocal relationships among support departments.

A summary of the alternatives is:

Corporate Sales

Consumer Sales

Direct method

$1,169,745

$625,485

Step-down method (HR first)

1,168,830

626,400

Reciprocal method

1,169,725

625,505

The reciprocal method is the preferred method, although for September 2012 the numbers do not

appear materially different across the alternatives.

15-23 (20−25 min.) Allocation of common costs.

1. Three methods of allocating the $55 are:

Ben

Gary

Stand-alone

Incremental (Gary primary)

Incremental (Ben primary)

Shapley value

$52

15

60

55

$13

50

5

10

15-13

2. The Shapley value approach is recommended. It is fairer than the incremental method

because it avoids considering one user as the primary user and allocating more of the common

costs to that user. It also avoids disputes about who is the primary user. It allocates costs in a

manner that is close to the costs allocated under the stand-alone method but takes a more

comprehensive view of the common cost allocation problem by considering primary and

1. Alternative approaches for the allocation of the $1,600 airfare include the following:

a. The stand-alone cost allocation method. This method would allocate the air fare on

the basis of each client’s percentage of the total of the individual stand-alone costs.

Baltimore client

( )

$1,200

$1,200 $800+

$1,600 = $ 960

$800

15-15

comprehensive view of the common cost allocation problem by considering primary and

incremental users, which the stand-alone method ignores.

The Shapley value (or the stand-alone cost allocation method) would be the preferred

3. A simple approach is to split the $80 equally between the two clients. The limousine

costs at the Sacramento end are not a function of distance traveled on the plane.

An alternative approach is to add the $80 to the $1,600 and repeat requirement 1:

a. Stand-alone cost allocation method.

Baltimore client

( )

$1,280

$1,280 $880+

$1,680 = $995.56

( )

$1,280 $880+

$880

15-25 (20 min.) Revenue allocation, bundled products.

1a. Under the stand alone revenue-allocation method based on selling price, Monaco will be

allocated 30% of all revenues, or $39 of the bundled selling price, and Innocence will be

allocated 70% of all revenues, or $91 of the bundled selling price, as shown below.

Stand-alone method, based on selling

prices

Monaco

Innocence

Total

Selling price

$48

$112

$160

Selling price as a % of total

($48

$160; $112

$160)

30%

70%

100%

Allocation of $130 bundled selling price

(30%

$130; 70%

$130)

$39

$91

$130

1b. Under the incremental revenue-allocation method, with Monaco ranked as the primary

product, Monaco will be allocated $48 (its own stand-alone selling price) and Innocence will be

allocated $82 of the $130 selling price, as shown below.

Incremental Method

(Monaco rank 1)

Monaco

Innocence

Selling price

$48

$112

Allocation of $130 bundled selling price

($48; $82 = $130 – $48)

$48

$82

1c. Under the incremental revenue-allocation method, with Innocence ranked as the primary

product, Innocence will be allocated $112 (its own stand-alone selling price) and Monaco will be

Selling price

$112

Allocation of $130 bundled selling price

$112

Monaco

Innocence

Allocation when Monaco = Rank 1;

Average of allocated selling price

15-17

2. A summary of the allocations based on the four methods in requirement 1 is shown below.

Stand-alone

(Selling Prices)

Incremental

(Monaco first)

Incremental

(Innocence first)

Shapley

Monaco

$ 39

$ 48

$ 18

$ 33

Innocence

91

82

112

97

Total for L’Amour

$130

$130

$130

$130

15-18

15-26 (20-25 min. ) Allocation of Common Costs

1. a. Dandridge’s method based on number of cars sold:

Sales

Location

Number of

cars sold

Percentage

Joint

Cost

Allocation

1. b. Stand-alone method:

Sales

Location

Stand-alone

cost

Percentage (costs in

thousands)

Joint

Cost

Allocation

1. c. Incremental method (locations ranked in order of largest advertising dollars to smallest

advertising dollars):

Sales Location

Allocated Cost

Cost Remaining to Allocate

South $ 756,000 ($1,800,000 – $756,000 = $1,044,000)

North 648,000 ($1,044,000 – $648,000 = $ 396,000)

West 396,000 ($ 396,000 – $396,000 = $ 0)

East 0

$1,800,000

2. In this situation, the stand-alone method is probably the best method because the weights it

uses for allocation are based on the individual advertising cost for each location as a separate

entity. Therefore, each entity gets the same relative proportion of advertising costs and each

location will have lower total advertising costs. The sales managers would likely not consider the

15-19

15-27 (20 min.) Single-rate, dual-rate, and practical capacity allocation.

Budgeted number of gifts wrapped = 6,650

1.a. Allocation based on budgeted usage of gift-wrapping services:

Women’s Face Wash (2,470 × $1.40)

$3,458

Men’s Face Wash (825 × $1.40)

1,155

Fragrances (1,805 × $1.40)

2,527

Body Wash (430 × $1.40)

602

Hair Products (1,120 × $1.40)

1,568

Total

$9,310

1.b. Allocation based on actual usage of gift-wrapping services:

Women’s Face Wash (2,020 × $1.40)

$2,828

Men’s Face Wash (730 × $1.40)

1,022

Fragrances (1,560 × $1.40)

2,184

Body Wash (545 × $1.40)

763

Hair Products (1,495 × $1.40)

2,093

Total

$8,890

1.c. Practical gift-wrapping capacity = 7,000

Budgeted fixed costs = $6,650

Fixed cost per gift based on practical capacity = $6,650 ÷ 7,000 = $0.95

2. Budgeted rate for fixed costs =

Budgeted fixed costs

Practical capacity

= $6,650 ÷ 7,000 gifts = $0.95 per gift

Fixed costs allocated on budgeted usage.