9-1

9-1 No. Differences in operating income between variable costing and absorption costing are

due to accounting for fixed manufacturing costs. Under variable costing only variable

9-2 The term direct costing is a misnomer for variable costing for two reasons:

a. Variable costing does not include all direct costs as inventoriable costs. Only variable

9-3 No. The difference between absorption costing and variable costs is due to accounting for

9-4 The main issue between variable costing and absorption costing is the proper timing of

the release of fixed manufacturing costs as costs of the period:

9-5 No. A company that makes a variable-cost/fixed-cost distinction is not forced to use any

specific costing method. The Stassen Company example in the text of Chapter 9 makes a

incurred.

9-6 Variable costing does not view fixed costs as unimportant or irrelevant, but it maintains

9-7 Under absorption costing, heavy reductions of inventory during the accounting period

9-8 (a) The factors that affect the breakeven point under variable costing are:

2. Contribution margin per unit.

9-2

1. Fixed (manufacturing and operating) costs.

3. Production level in units in excess of breakeven sales in units.

9-9 Examples of dysfunctional decisions managers may make to increase reported operating

income are:

9-10 Approaches used to reduce the negative aspects associated with using absorption costing

include:

a. Change the accounting system:

• Adopt either variable or throughput costing, both of which reduce the incentives

9-11 The theoretical capacity and practical capacity denominator-level concepts emphasize

9-12 The downward demand spiral is the continuing reduction in demand for a company’s

9-13 No. It depends on how a company handles the production-volume variance in the end-of-

9-14 For tax reporting in the U.S., the IRS requires only that indirect production costs are

“fairly” apportioned among all items produced. Overhead rates based on normal or master–

9-15 No. The costs of having too much capacity/too little capacity involve revenue

opportunities potentially forgone as well as costs of money tied up in plant assets.

9-3

9-16 (30 min.) Variable and absorption costing, explaining operating-income differences.

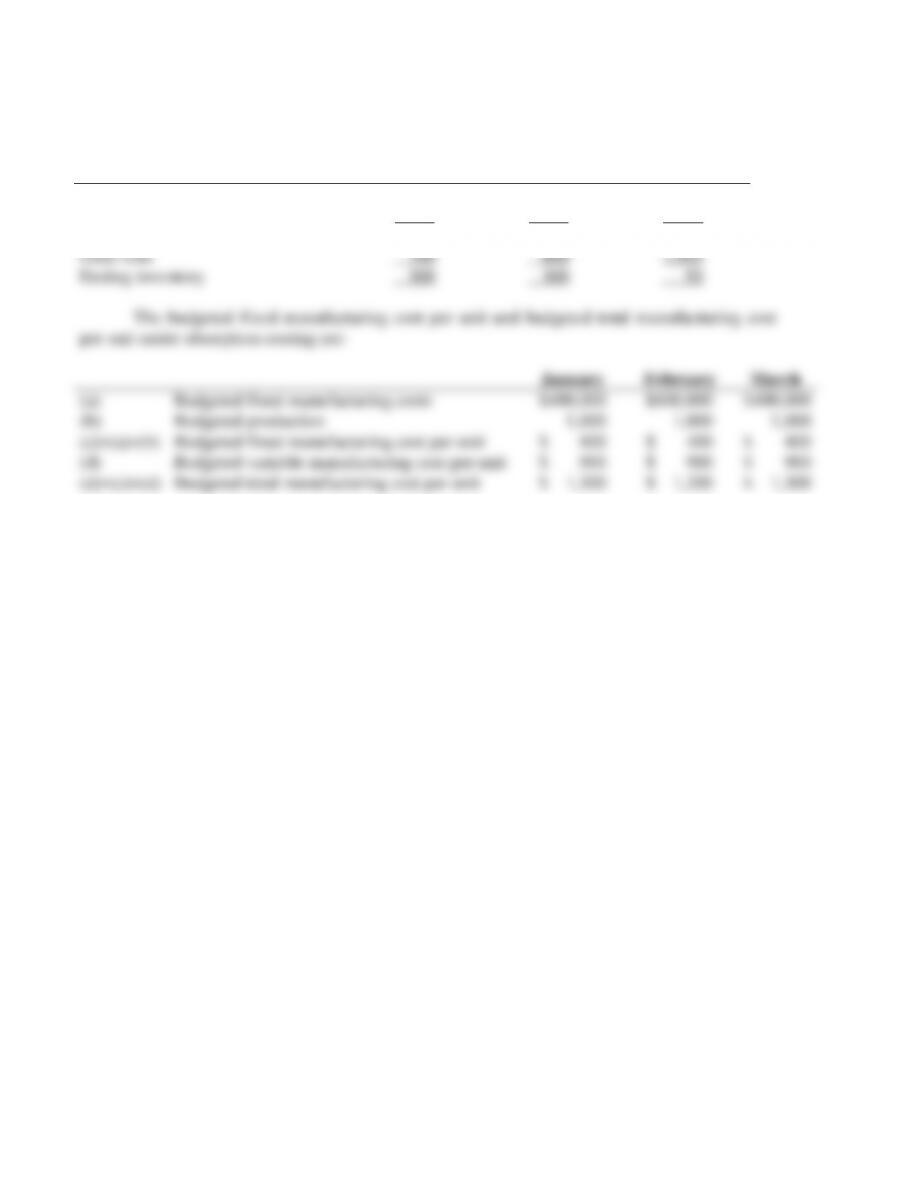

1. Key inputs for income statement computations are

April

May

Beginning inventory

Production

Goods available for sale

Units sold

Ending inventory

0

500

500

350

150

150

400

550

520

30

The budgeted fixed cost per unit and budgeted total manufacturing cost per unit under absorption

costing are

April

May

(a) Budgeted fixed manufacturing costs

(b) Budgeted production

(c)=(a)÷(b) Budgeted fixed manufacturing cost per unit

(d) Budgeted variable manufacturing cost per unit

(e)=(c)+(d) Budgeted total manufacturing cost per unit

$2,000,000

500

$4,000

$10,000

$14,000

$2,000,000

500

$4,000

$10,000

$14,000

(a) Variable costing

April 2011

May 2011

Revenuesa

$8,400,000

$12,480,000

Variable costs

Beginning inventory

$ 0

$1,500,000

Variable manufacturing costsb

5,000,000

4,000,000

Cost of goods available for sale

5,000,000

5,500,000

Deduct ending inventoryc

(1,500,000)

(300,000)

Variable cost of goods sold

3,500,000

5,200,000

Variable operating costsd

1,050,000

1,560,000

Total variable costs

4,550,000

6,760,000

Contribution margin

3,850,000

5,720,000

Fixed costs

Fixed manufacturing costs

2,000,000

2,000,000

Fixed operating costs

600,000

600,000

Total fixed costs

2,600,000

2,600,000

Operating income

$1,250,000

$3,120,000

a $24,000 × 350; $24,000 × 520 c $10,000 × 150; $10,000 × 30

b $10,000 × 500; $10,000 × 400 d $3,000 × 350; $3,000 × 520

9-4

(b) Absorption costing

April 2011

May 2011

Revenuesa

$8,400,000

$12,480,000

Cost of goods sold

Beginning inventory

$ 0

$2,100,000

Variable manufacturing costsb

5,000,000

4,000,000

Allocated fixed manufacturing costsc

2,000,000

1,600,000

Cost of goods available for sale

7,000,000

7,700,000

Deduct ending inventoryd

(2,100,000)

(420,000)

Adjustment for prod.-vol. variancee

0

400,000 U

Cost of goods sold

4,900,000

7,680,000

Gross margin

3,500,000

4,800,000

Operating costs

Variable operating costsf

1,050,000

1,560,000

Fixed operating costs

600,000

600,000

Total operating costs

1,650,000

2,160,000

Operating income

$1,850,000

$ 2,640,000

2.

Absorption-costing

operating income

–

Variable-costing

operating income

=

Fixed manufacturing costs

in ending inventory

–

Fixed manufacturing costs

in beginning inventory

April:

$1,850,000 – $1,250,000 = ($4,000 × 150) – ($0)

$600,000 = $600,000

May:

9-5

9-17 (20 min.) Throughput costing (continuation of Exercise 9-16).

1.

April 2011

May 2011

Revenuesa

$8,400,000

$12,480,000

Direct material cost of goods sold

Beginning inventory

Direct materials in goods

manufacturedb

$ 0

3,350,000

$1,005,000

2,680,000

Cost of goods available for sale

Deduct ending inventoryc

3,350,000

(1,005,000)

3,685,000

(201,000)

Total direct material cost of goods sold

Throughput margin

Other costs

2,345,000

6,055,000

3,484,000

8,996,000

Manufacturing costs

3,650,000d

3,320,000e

Other operating costs

1,650,000f

2,160,000g

Total other costs

Operating income

5,300,000

$ 755,000

5,480,000

$ 3,516,000

2. Operating income under:

April

May

Variable costing

Absorption costing

Throughput costing

$1,250,000

1,850,000

755,000

$3,120,000

2,640,000

3,516,000

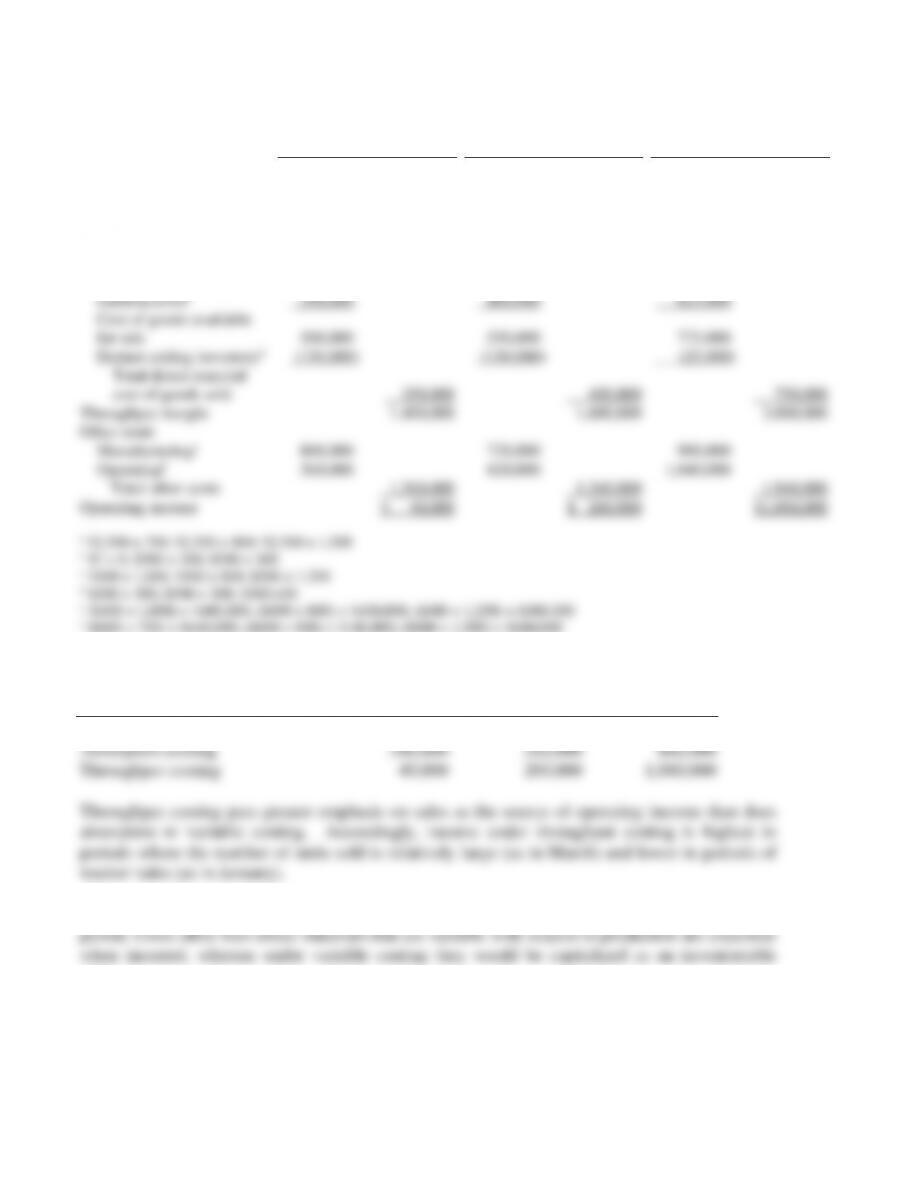

In April, throughput costing has the lowest operating income, whereas in May throughput

costing has the highest operating income. Throughput costing puts greater emphasis on sales as

the source of operating income than does either absorption or variable costing.

3. Throughput costing puts a penalty on production without a corresponding sale in the

same period. Costs other than direct materials that are variable with respect to production are

9-6

9-18 (40 min.) Variable and absorption costing, explaining operating-income differences.

1. Key inputs for income statement computations are:

January

February

March

Beginning inventory

Production

Goods available for sale

Units sold

Ending inventory

0

1,000

1,000

700

300

300

800

1,100

800

300

300

1,250

1,550

1,500

50

The budgeted fixed manufacturing cost per unit and budgeted total manufacturing cost

per unit under absorption costing are:

January

February

March

(a) Budgeted fixed manufacturing costs

(b) Budgeted production

(c)=(a)÷(b) Budgeted fixed manufacturing cost per unit

(d) Budgeted variable manufacturing cost per unit

(e)=(c)+(d) Budgeted total manufacturing cost per unit

$400,000

1,000

$ 400

$ 900

$ 1,300

$400,000

1,000

$ 400

$ 900

$ 1,300

$400,000

1,000

$ 400

$ 900

$ 1,300

9-7

(a) Variable Costing

January 2012

February 2012

March 2012

Revenuesa

$1,750,000

$2,000,000

$3,750,000

Variable costs

Beginning inventoryb

$ 0

$270,000

$ 270,000

Variable manufacturing costsc

900,000

720,000

1,125,000

Cost of goods available for sale

Deduct ending inventoryd

900,000

(270,000)

990,000

(270,000)

1,395,000

(45,000)

Variable cost of goods sold

Variable operating costse

Total variable costs

630,000

420,000

1,050,000

720,000

480,000

1,200,000

1,350,000

900,000

2,250,000

Contribution margin

Fixed costs

Fixed manufacturing costs

Fixed operating costs

Total fixed costs

Operating income

400,000

140,000

700,000

540,000

$ 160,000

400,000

140,000

800,000

540,000

$ 260,000

400,000

140,000

1,500,000

540,000

$ 960,000

a $2,500 × 700; $2,500 × 800; $2,500 × 1,500

b $? × 0; $900 × 300; $900 × 300

c $900 × 1,000; $900 × 800; $900 × 1,250

d $900 × 300; $900 × 300; $900 × 50

e $600 × 700; $600 × 800; $600 × 1,500

9-8

(b) Absorption Costing

January 2012

February 2012

March 2012

Revenuesa

Cost of goods sold

Beginning inventoryb

$ 0

$1,750,000

$ 390,000

$2,000,000

$ 390,000

$3,750,000

Variable manufacturing costsc

900,000

720,000

1,125,000

Allocated fixed manufacturing

costsd

400,000

320,000

500,000

Cost of goods available for sale

1,300,000

1,430,000

2,015,000

Deduct ending inventorye

(390,000)

(390,000)

(65,000)

Adjustment for prod. vol. var.f

0

80,000 U

(100,000) F

Cost of goods sold

910,000

1,120,000

1,850,000

Gross margin

840,000

880,000

1,900,000

Operating costs

Variable operating costsg

420,000

480,000

900,000

Fixed operating costs

140,000

140,000

140,000

Total operating costs

560,000

620,000

1,040,000

Operating income

$ 280,000

$ 260,000

$ 860,000

9-9

2.

Absorption-costing Variable costing Fixed manufacturing Fixed manufacturing

operating operating costs in costs in

income income ending inventory beginning inventory

− = −

9-19 (20–30 min.) Throughput costing (continuation of Exercise 9-18).

1.

January

February

March

Revenuesa

Direct material cost of

goods sold

Beginning inventoryb

$ 0

$1,750,000

$150,000

$2,000,000

$ 150,000

$3,750,000

Direct materials in goods

manufacturedc

Cost of goods available

for sale

Deduct ending inventoryd

Total direct material

cost of goods sold

500,000

500,000

(150,000)

350,000

400,000

550,000

(150,000)

400,000

625,000

775,000

(25,000)

750,000

Throughput margin

1,400,000

1,600,000

3,000,000

Other costs

Manufacturinge

Operatingf

Total other costs

Operating income

800,000

560,000

1,360,000

$ 40,000

720,000

620,000

1,340,000

$ 260,000

900,000

1,040,000

1,940,000

$1,060,000

a $2,500 × 700; $2,500 × 800; $2,500 × 1,500

b $? × 0; $500 × 300; $500 × 300

c $500 × 1,000; $500 × 800; $500 × 1,250

d $500 × 300; $500 × 300; $500 ×50

e ($400 × 1,000) + $400,000; ($400 × 800) + $400,000; ($400 × 1,250) + $400,000

f ($600 × 700) + $140,000; ($600 × 800) + $140,000; ($600 × 1,500) + $140,000

2. Operating income under:

January

February

March

Variable costing

Absorption costing

Throughput costing

$160,000

280,000

40,000

$260,000

260,000

260,000

$ 960,000

860,000

1,060,000

Throughput costing puts greater emphasis on sales as the source of operating income than does

absorption or variable costing. Accordingly, income under throughput costing is highest in

periods where the number of units sold is relatively large (as in March) and lower in periods of

weaker sales (as in January).

3. Throughput costing puts a penalty on producing without a corresponding sale in the same

cost.