9-30 (30–35 min.) Comparison of variable costing and absorption costing.

1. Since production volume variance is unfavorable, the budgeted fixed manufacturing

overhead must be larger than the fixed manufacturing overhead allocated.

Production-volume

variance

=

Budgeted fixed

manufacturing overhead

–

Fixed manufacturing

overhead allocated

$400,000 = $1,200,000 – Allocated

Allocated = $800,000, which is 67% of $1,200,000

If 67% of the budgeted fixed costs were allocated, the plant must have been operating at 67% of

denominator level in 2012.

2. The problem provides the beginning and ending inventory balances under both, variable

and absorption costing. Under variable costing, all fixed costs are written off as period costs, i.e.,

they are not inventoried. Under absorption costing, inventories include variable and fixed costs.

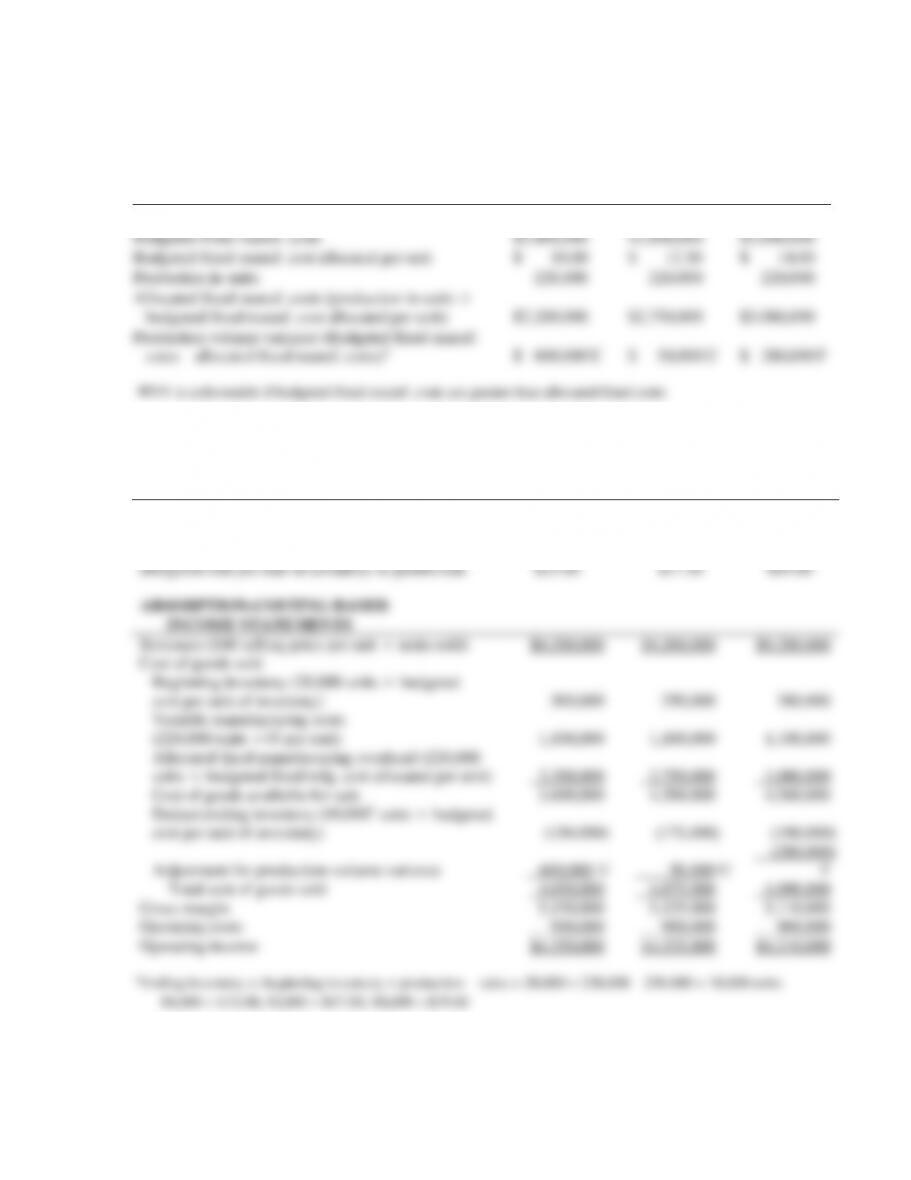

9-32

Absorption costing,

Fixed manuf. costs in cost of goods sold

($5,860,000 − $4,680,000)

$1,180,000

Production-volume variance

400,000

1,580,000

Variable costing, fixed manuf. costs charged to expense

(1,200,000)

Difference in operating income explained

$ 380,000

4. Under absorption costing, operating income is a function of both sales and production

(i.e., change in inventory levels). During 2012, Hinkle experienced a severe decline in inventory

1.

20,000

books

24,000

books

30,000

Books

Revenues

$1,600,000

$1,600,000

$1,600,000

Cost of goods sold

1,400,000a

1,400,000

1,400,000

Production volume —

*variance

0b

(80,000)c

(200,000)d

Net cost of goods sold

1,400,000

1,320,000

1,200,000

Gross Margin

$ 200,000

$ 280,000

$ 400,000

a cost per unit = ($50 + $400,000/20,000 books sold) = $70 per book

CGS = $70 20,000 = $1,400,000

b volume variance = Budgeted fixed cost – fixed overhead rate production

$400,000 – ($20 20,000 books) = $0

c volume variance = Budgeted fixed cost – fixed overhead rate production

$400,000 – ($20 24,000 books) = $80,000

d volume variance = Budgeted fixed cost – fixed overhead rate production

$400,000 – ($20 30,000 books) = $200,000

2.

20,000

Books

24,000

books

30,000

books

Beginning inventory 0 0 0

+ Production 20,000 books 24,000 books 30,000 books

20,000 24,000 30,000

9-32 (25–30 min.) Alternative denominator-level capacity concepts, effect on operating income.

1.

Budgeted Fixed

Budgeted Fixed

Days of

Hours of

Budgeted

Manufacturing

Denominator-Level

Capacity Concept

Manuf. Overhead

per Period

Production

per Period

Production

per Day

Barrels

per Hour

Denominator Level

(Barrels)

Overhead Rate

per Barrel

(1)

(2)

(3)

(4)

(5) = (2)

(3)

(4)

(6) = (1)

(5)

Theoretical capacity

$28,000,000

360

24

540

4,665,600

$ 6.00

Practical capacity

28,000,000

350

20

500

3,500,000

8.00

Normal capacity utilization

28,000,000

350

20

400

2,800,000

10.00

Master-budget utilization

(a) January-June 2012

14,000,000

175

20

320

1,120,000

12.50

(b) July-December 2012

14,000,000

175

20

480

1,680,000

8.33

2. Using column (6) from above,

Per Barrel

Denominator-Level

Capacity Concept

Budgeted

Fixed Mfg.

Overhead

Rate per Barrel

(6)

Budgeted

Variable

Mfg.

Cost Rate

(7)

Budgeted

Total Mfg

Cost Rate

(8) =

(6) + (7)

Fixed Mfg.

Overhead

Costs Allocated

(9) =

2,600,000

(6)

Fixed

Mfg. Overhead

Variance

(10) =

$27,088,000 – (9)

Theoretical capacity

$6.00

$30.20a

$36.20

$15,600,000

$11,488,000

U

Practical capacity

8.00

30.20

38.20

20,800,000

6,288,000

U

Normal capacity utilization

10.00

30.20

40.20

26,000,000

1,088,000

U

a$78,520,000

2,600,000 barrels

9-35

Absorption-Costing Income Statement

Theoretical

Capacity

Practical

Capacity

Normal

Capacity

Utilization

Revenues (2,400,000 bbls.

$45 per bbl.)

$108,000,000

$108,000,000

$108,000,000

Cost of goods sold

Beginning inventory

0

0

0

Variable mfg. costs

78,520,000

78,520,000

78,520,000

Fixed mfg. overhead costs allocated

(2,600,000 units

$6.00; $8.00; $10.00 per unit)

15,600,000

20,800,000

26,000,000

Cost of goods available for sale

94,120,000

99,320,000

104,520,000

Deduct ending inventory

(200,000 units

$36.20; $38.20; $40.20 per unit)

(7,240,000)

(7,640,000)

(8,040,000)

Adjustment for variances (add: all unfavorable)

11,488,000U

6,288,000U

1,088,000U

Cost of goods sold

98,368,000

97,968,000

97,568,000

Gross margin

9,632,000

10,032,000

10,432,000

Other costs

0

0

0

Operating income

$ 9,632,000

$ 10,032,000

$ 10,432,000

9-36

9-33 (20 min.) Motivational considerations in denominator-level capacity selection

(continuation of 9-32).

1. If the plant manager gets a bonus based on operating income, he/she will prefer the

denominator-level capacity to be based on normal capacity utilization (or master-budget

utilization). In times of rising inventories, as in 2012, this denominator level will maximize the

2. Given the data in this question, the theoretical capacity concept reports the lowest

3. The IRS may restrict the flexibility of a company in several ways:

a. Restrict the denominator-level concept choice (to say, practical capacity).

9-37

9-34 (25 min.) Denominator-level choices, changes in inventory levels, effect on

operating income.

1.

Normal

Theoretical

Practical

Capacity

Capacity

Capacity

Utilization

Denominator level in units

280,000

224,000

200,000

Budgeted fixed manuf. costs

$2,800,000

$2,800,000

$2,800,000

Budgeted fixed manuf. cost allocated per unit

$ 10.00

$ 12.50

$ 14.00

Production in units

220,000

220,000

220,000

Allocated fixed manuf. costs (production in units

budgeted fixed manuf. cost allocated per unit)

$2,200,000

$2,750,000

$3,080,000

Production volume variance (Budgeted fixed manuf.

costs – allocated fixed manuf. costs)a

$ 600,000

U

$ 50,000

U

$ 280,000

F

2.

Normal

Theoretical

Practical

Capacity

Capacity

Capacity

Utilization

Units sold

230,000

230,000

230,000

Budgeted fixed mfg. cost allocated per unit

$10.00

$12.50

$14.00

Budgeted var. mfg. cost per unit

$ 5.00

$ 5.00

$ 5.00

Budgeted cost per unit of inventory or production

$15.00

$17.50

$19.00

ABSORPTION-COSTING BASED

INCOME STATEMENTS

Revenues ($40 selling price per unit

units sold)

$9,200,000

$9,200,000

$9,200,000

Cost of goods sold

Beginning inventory (20,000 units

budgeted

cost per unit of inventory)

300,000

350,000

380,000

Variable manufacturing costs

(220,000 units

$5 per unit)

1,100,000

1,100,000

1,100,000

Allocated fixed manufacturing overhead (220,000

units

budgeted fixed mfg. cost allocated per unit)

2,200,000

2,750,000

3,080,000

Cost of goods available for sale

3,600,000

4,200,000

4,560,000

Deduct ending inventory (10,000b units

budgeted

cost per unit of inventory)

(150,000)

(175,000)

(190,000)

Adjustment for production-volume variance

600,000 U

50,000 U

(280,000)

F

Total cost of goods sold

4,050,000

4,075,000

4,090,000

Gross margin

5,150,000

5,125,000

5,110,000

Operating costs

900,000

900,000

900,000

Operating income

$4,250,000

$4,225,000

$4,210,000

9-38

3. Koshu’s 2011 beginning inventory was 20,000 units; its ending inventory was 10,000

units. So, during 2011, there was a drop of 10,000 units in inventory levels (matching the 10,000

4.

Reconciliation

Theoretical Capacity Operating Income –

Practical Capacity Operating Income

$25,000

Decrease in inventory level during 2011

10,000

Fixed mfg cost allocated per unit under

practical capacity – fixed mfg. cost allocated

per unit under theoretical capacity ($12.50 – $10)

$2.50

Additional allocated fixed cost included in COGS

under practical capacity = 10,000 units

$2.50 per unit =

$25,000

income.

1. Normal capacity utilization. Givens denoted*

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(4)

$90,600

$96,600*

$96,600*

37,680 hrs.* × $2.50a

= $94,200

2. Practical capacity. Givens denoted*

Actual Costs

Incurred

(1)

Same Lump Sum

(as in Static Budget)

Regardless of

Budgeted Output

Level

(2)

Flexible Budget:

Same Lump Sum

(as in Static Budget)

Regardless of

Budgeted Output

Level

(3)

Allocated:

Budgeted Input

Allowed for

Actual Output

× Budgeted Rate

(4)

$90,600

$96,600*

$96,600*

37,680* × $2.24a

= $84,400

3. To maximize operating income, the executive vice president would favor using normal

capacity utilization rather than practical capacity. Why? Because normal capacity utilization is a