16-11

16-21 (30 min.) Joint-cost allocation, process further.

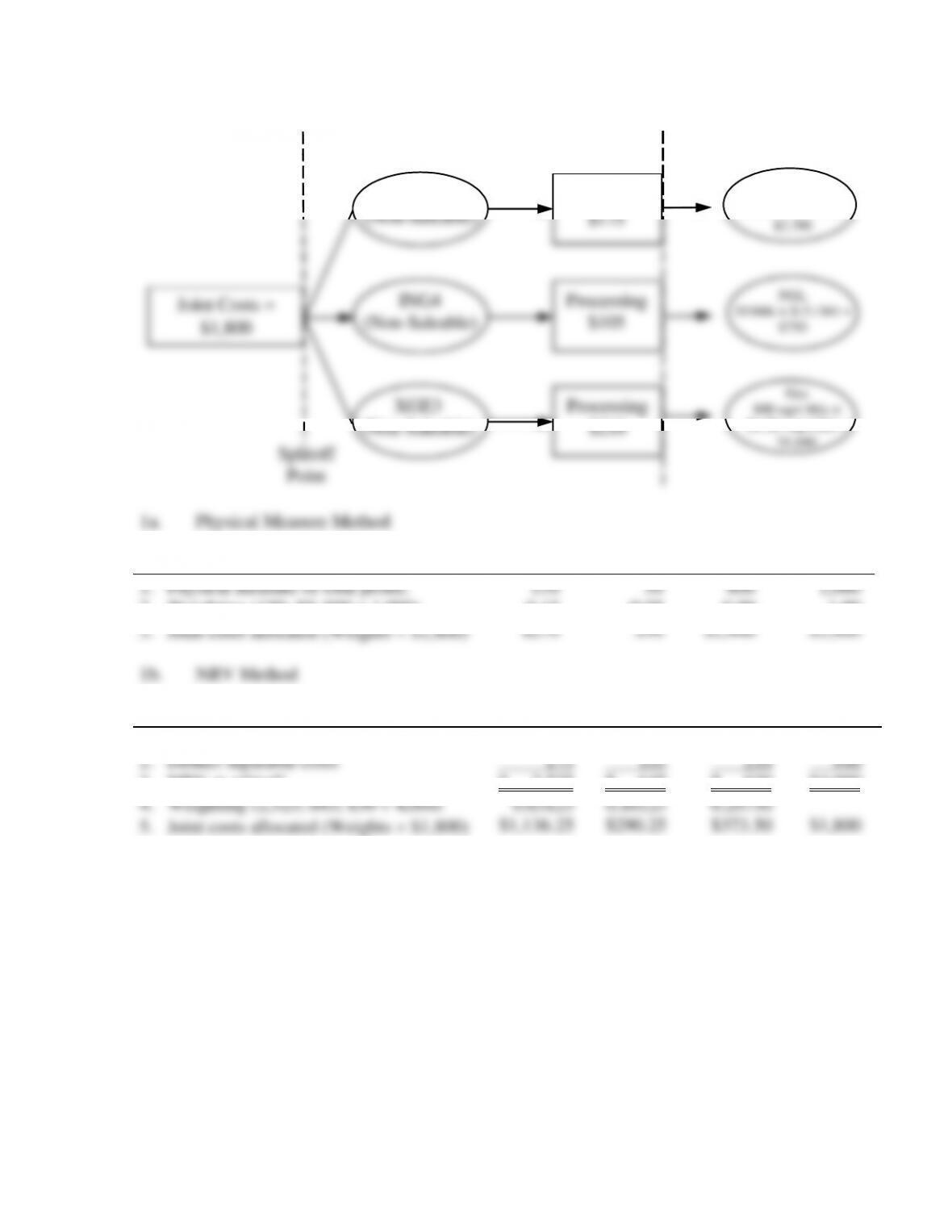

Joint Costs =

$1800

ICR8

(Non-Saleable)

ING4

(Non-Saleable)

XGE3

(Non-Saleable)

Processing

$175

Processing

$210

Processing

$105

Crude Oil

150 bbls × $18 / bbl =

$2700

NGL

50 bbls × $15 / bbl =

$750

Gas

800 eqvt bbls ×

$1.30 / eqvt bbl =

$1040

Splitoff

Point

1a. Physical Measure Method

Crude Oil

NGL

Gas

Total

1. Physical measure of total prodn.

2. Weighting (150; 50; 800 ÷ 1,000)

3. Joint costs allocated (Weights $1,800)

150

0.15

$270

50

0.05

$90

800

0.80

$1,440

1,000

1.00

$1,800

1b. NRV Method

Crude Oil

NGL

Gas

Total

1. Final sales value of total production

2. Deduct separable costs

3. NRV at splitoff

4. Weighting (2,525; 645; 830 ÷ 4,000)

5. Joint costs allocated (Weights $1,800)

$ 2,700

175

$ 2,525

0.63125

$1,136.25

$ 750

105

$ 645

0.16125

$290.25

$ 1,040

210

$ 830

0.20750

$373.50

$4,490

490

$4,000

$1,800

2. The operating-income amounts for each product using each method is:

(a) Physical Measure Method

Crude Oil

NGL

Gas

Total

Revenues

Cost of goods sold

Joint costs

Separable costs

Total cost of goods sold

Gross margin

$2,700

270

175

445

$2,255

$750

90

105

195

$555

$1,040

1,440

210

1,650

$ (610)

$4,490

1,800

490

2,290

$2,200

(b) NRV Method

Crude Oil

NGL

Gas

Total

Revenues

Cost of goods sold

Joint costs

Separable costs

Total cost of goods sold

Gross margin

$2,700.00

1,136.25

175.00

1,311.25

$1,388.75

$750.00

290.25

105.00

395.25

$354.75

$1,040.00

373.50

210.00

583.50

$ 456.50

$4,490.00

1,800.00

490.00

2,290.00

$2,200.00

3. Neither method should be used for product emphasis decisions. It is inappropriate to use

joint-cost-allocated data to make decisions regarding dropping individual products, or pushing

4. Since crude oil is the only product subject to taxation, it is clearly in Sinclair’s best

interest to use the NRV method since it leads to a lower profit for crude oil and, consequently, a

16-13

16-22 (30 min.) Joint-cost allocation, sales value, physical measure, NRV methods.

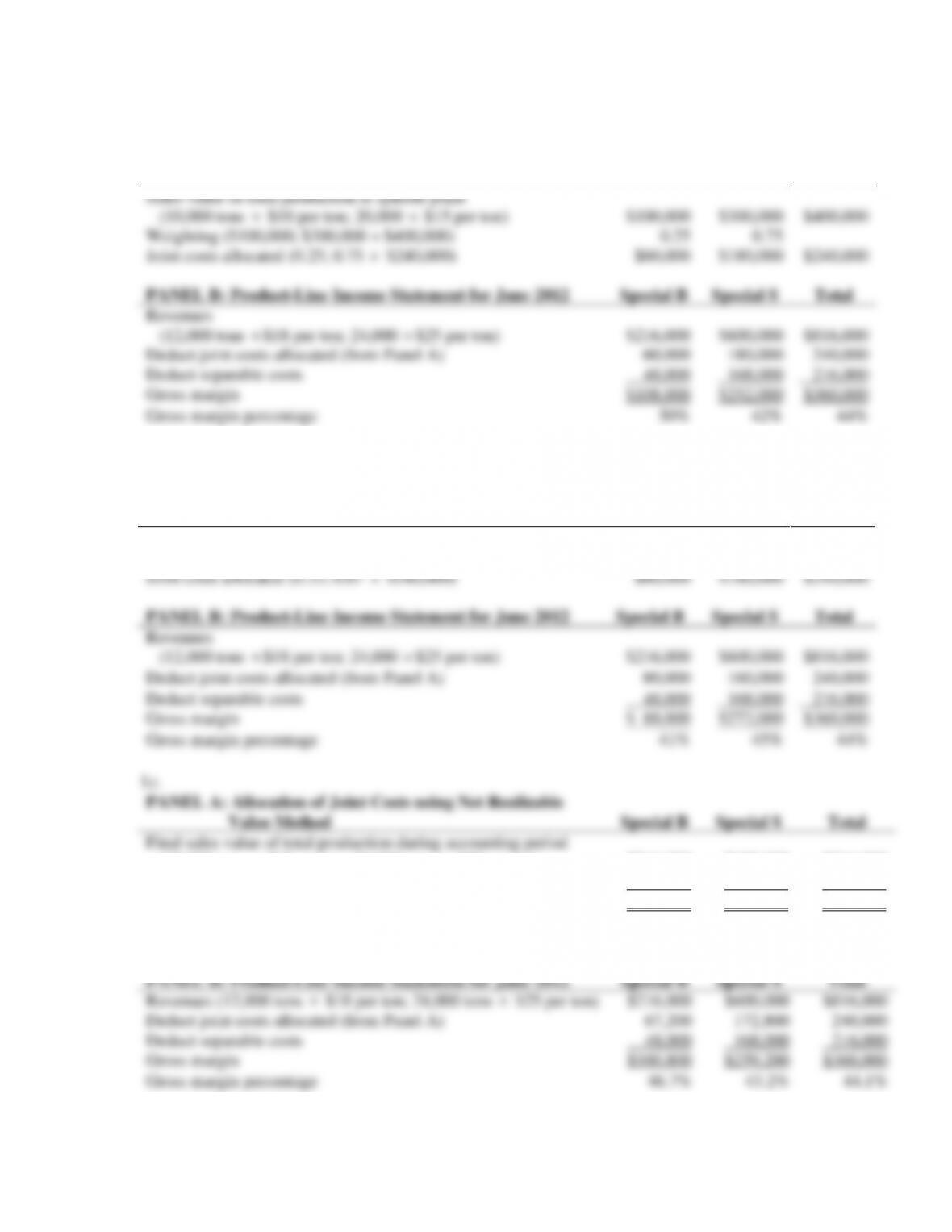

1a.

PANEL A: Allocation of Joint Costs using Sales Value at

Splitoff Method

Special B/

Beef

Ramen

Special S/

Shrimp

Ramen

Total

Sales value of total production at splitoff point

(10,000 tons

$10 per ton; 20,000

$15 per ton)

$100,000

$300,000

$400,000

Weighting ($100,000; $300,000 ÷ $400,000)

0.25

0.75

Joint costs allocated (0.25; 0.75

$240,000)

$60,000

$180,000

$240,000

PANEL B: Product-Line Income Statement for June 2012

Special B

Special S

Total

Revenues

(12,000 tons

$18 per ton; 24,000

$25 per ton)

$216,000

$600,000

$816,000

Deduct joint costs allocated (from Panel A)

60,000

180,000

240,000

Deduct separable costs

48,000

168,000

216,000

Gross margin

$108,000

$252,000

$360,000

Gross margin percentage

50%

42%

44%

1b.

PANEL A: Allocation of Joint Costs using Physical-Measure

Method

Special B/

Beef

Ramen

Special S/

Shrimp

Ramen

Total

Physical measure of total production (tons)

10,000

20,000

30,000

Weighting (10,000 tons; 20,000 tons ÷ 30,000 tons)

33%

67%

Joint costs allocated (0.33; 0.67

$240,000)

$80,000

$160,000

$240,000

PANEL B: Product-Line Income Statement for June 2012

Special B

Special S

Total

Revenues

(12,000 tons

$18 per ton; 24,000

$25 per ton)

$216,000

$600,000

$816,000

Deduct joint costs allocated (from Panel A)

80,000

160,000

240,000

Deduct separable costs

48,000

168,000

216,000

Gross margin

$ 88,000

$272,000

$360,000

Gross margin percentage

41%

45%

44%

1c.

PANEL A: Allocation of Joint Costs using Net Realizable

Value Method

Special B

Special S

Total

Final sales value of total production during accounting period

(12,000 tons

$18 per ton; 24,000 tons

$25 per ton)

$216,000

$600,000

$816,000

Deduct separable costs

48,000

168,000

216,000

Net realizable value at splitoff point

$168,000

$432,000

$600,000

Weighting ($168,000; $432,000 ÷ $600,000)

28%

72%

Joint costs allocated (0.28; 0.72

$240,000)

$67,200

$172,800

$240,000

PANEL B: Product-Line Income Statement for June 2012

Special B

Special S

Total

Revenues (12,000 tons

$18 per ton; 24,000 tons

$25 per ton)

$216,000

$600,000

$816,000

Deduct joint costs allocated (from Panel A)

67,200

172,800

240,000

Deduct separable costs

48,000

168,000

216,000

Gross margin

$100,800

$259,200

$360,000

Gross margin percentage

46.7%

43.2%

44.1%

16-14

2. Sherrie Dong probably performed the analysis shown below to arrive at the net loss of

$2,228 from marketing the stock:

PANEL A: Allocation of Joint Costs using

Sales Value at Splitoff

Special B/

Beef

Ramen

Special S/

Shrimp

Ramen

Stock

Total

Sales value of total production at splitoff point

(10,000 tons

$10 per ton; 20,000

$15 per

ton; 4,000

$5 per ton)

$100,000

$300,000

$20,000

$420,000

Weighting

($100,000; $300,000; $20,000 ÷ $420,000)

23.8095%

71.4286%

4.7619%

100%

Joint costs allocated

(0.238095; 0.714286; 0.047619

$240,000)

$57,143

$171,429

$11,428

$240,000

PANEL B: Product-Line Income Statement

for June 2012

Special B

Special S

Stock

Total

Revenues

(12,000 tons

$18 per ton; 24,000

$25 per ton;

4,000

$5 per ton)

$216,000

$600,000

$20,000

$836,000

Separable processing costs

48,000

168,000

0

216,000

Joint costs allocated (from Panel A)

57,143

171,429

11,428

240,000

Gross margin

$110,857

$260,571

8,572

380,000

Deduct marketing costs

10,800

10,800

Operating income

$ (2,228)

$369,200

In this (misleading) analysis, the $240,000 of joint costs are re-allocated between Special B,

Special S, and the stock. Irrespective of the method of allocation, this analysis is wrong. Joint

costs are always irrelevant in a process-further decision. Only incremental costs and revenues

past the splitoff point are relevant. In this case, the correct analysis is much simpler: the

incremental revenues from selling the stock are $20,000, and the incremental costs are the

marketing costs of $10,800. So, Instant Foods should sell the stock—this will increase its

operating income by $9,200 ($20,000 – $10,800).

16-15

1.

a. Sales value at splitoff method:

Cookies/

Soymeal

Soyola/

Soy Oil

Total

Sales value of total production at splitoff,

500lbs × $1; 100 gallons × $4

$ 500

$ 400

$900

Weighting, $500; $400

$900

0.556

0.444

Joint costs allocated,

0.556; 0.444 $500

$ 278

$ 222

$500

b. Net realizable value method:

Cookies

Soyola

Total

Final sales value of total production,

600lbs × $2; 400qts × $1.25

$1,200

$ 500

$1,700

Deduct separable costs

300

200

500

Net realizable value

$ 900

$ 300

$1,200

Weighting, $900; $300

$1,200

0.75

0.25

Joint costs allocated,

0.75; 0.25 $500

$375

$125

$500

2.

Cookies/Soy Meal

Soyola/Soy Oil

Revenue if sold at splitoff

$500a

$ 400 b

Process further NRV

900 c

300 d

Profit (Loss) from processing further

$400

$(100)

a 500 lbs × $ 1 = $500

b 100 gal × $ 4 = $400

c 600 lbs × $ 2 – $300 = $900

d 400 qts × $1.25 – $200 = $300

ISP should process the soy meal into cookies because it increases profit by $400 (900-500).

However, they should sell the soy oil as is, without processing it into the form of Soyola, because

profit will be $100 (400-300) higher if they do. Since the total joint cost is the same under both

allocation methods, it is not a relevant cost to the decision to sell at splitoff or process further.

16-24 (30 min.) Accounting for a main product and a byproduct.

Production

Method

Sales

Method

1.

Revenues

Main product

$682,240a

$682,240

Byproduct

––__

65,000d

Total revenues

682,240

747,240

Cost of goods sold

Total manufacturing costs

500,000

500,000

Deduct value of byproduct production

85,000b

0

Net manufacturing costs

415,000

500,000

Deduct main product inventory

74,700c

90,000e

Cost of goods sold

340,300

410,000

Gross margin

$341,940

$337,240

2.

Main Product

$74,700

Byproduct

16-17

16-25 (35-45 min.) Joint costs and byproducts.

1. Computing byproduct deduction to joint costs:

Revenues from C, 16,000 $6 $ 96,000

Deduct:

Gross margin, 10% of revenues 9,600

Marketing costs, 20% of revenues 19,200

16-18

2. If all three products are treated as joint products:

Quantity

Unit

Sales

Price

Final

Sales

Value

Deduct

Separable

Processing

Cost

Net

Realizable

Value at

Splitoff

Weighting

Allocation

of

$180,000

Joint

Costs

A

12,000

$12

$144,000

$27,000

$117,000

117 ÷ 376.8

$ 55,892

B

65,000

3

195,000

─

195,000

195 ÷ 376.8

93,153

C

16,000

6

96,000

31,200

64,800

64.8 ÷ 376.8

30,955

Totals

$435,000

$58,200

$376,800

$180,000

Add Separable

Joint Costs Processing

Allocation Costs Total Costs Units Unit Cost

A $ 55,892 $27,000 $ 82,892 12,000 $6.91

B 93,153 –– 93,153 65,000 1.43

C 30,955 12,000 42,955 16,000 2.68

Totals $180,000 $39,000 $219,000 93,000

Call the attention of students to the different unit “costs” resulting from the two assumptions

about the relative importance of Product C. The point is that costs of individual products depend

heavily on which assumptions are made and which accounting methods and techniques are used.

16-19

1. Byproduct recognized at time of production:

Joint cost = $7,200

Joint cost to be charged to main product = Joint Cost – NRV of Byproduct = $7,200 – (900 lbs. × $2)

= $5,400

$5400

1500×2

Inventoriable cost of byproduct = NRV = $2.00 per pound

Gross Margin Calculation under Production Method

Revenues

Main product: Juice (2800 half-gallons × $2.50)

$7,000

Byproduct: Pulp and peel

0

7,000

Cost of goods sold

Main product: Juice (2800 half-gallons × $1.80)

5,040

Gross margin

$1,960

Gross-margin percentage ($1,960 ÷ $7,000)

28.00%

2. Byproduct recognized at time of sale:

Joint cost to be charged to main product = Total joint cost = $7,200

Inventoriable cost of main product =

$7,200

1,500×2

= $2.40 per half-gallon

Inventoriable cost of byproduct = $0

Gross Margin Calculation under Sales Method

Revenues

Main product: Juice (2800 half-gallons × $2.50)

$7,000

Byproduct: Pulp and peel (860 pounds × $2.00)

1,720

8,720

Cost of goods sold

Main product: Juice (2800 half-gallons × $2.40)

6,720

Gross margin

$2,000

Gross-margin percentage ($2,000 ÷ $8,720)

22.94%

Inventoriable costs (end of period):

Main product: Juice (200 half-gallons × $2.40) = $480

Byproduct: Pulp and peel (40 pounds × $ 0) = $ 0

3. The production method recognizes the byproduct cost as inventory in the period it is

produced. This method sets the cost of the byproduct inventory equal to its net realizable

1. Computation of joint-cost allocation proportions:

a. Sales Value of

Total Production Allocation of $96,000

at Splitoff Weighting Joint Costs

A $ 84,000 84 ÷ 240 = 0.35 $33,600