4-21

The posting of entries to T-accounts is as follows:

Materials Control

Work-in–Process Control

Bal 12

(2) 145

Bal. 2

(2) 145

(4) 90

(8) 63

(9) 294

(1) 150

(3) 10

Bal. 7

Bal. 6

Finished Goods Control

Cost of Goods Sold

Bal. 6

(9) 294

(10a) 292

(10a) 292

(11) 5

Bal. 8

Manufacturing Department

Overhead Control

Manufacturing Overhead Allocated

(3) 10

(5) 30

(6) 19

(7) 9

(11) 68

(11) 63

(8) 63

Accounts Payable Control

Wages Payable Control

(1) 150

(4) 90

(5) 30

Accumulated Depreciation

Various Liabilities

(6) 19

(7) 9

Accounts Receivable Control

Revenues

(10b) 400

(10b) 400

3. (11) Manufacturing Overhead Allocated 63

4-22

4-27 (15 min.) Job costing, unit cost, ending work in progress.

1.

Direct manufacturing labor rate per hour

$26

Manufacturing overhead cost allocated

per manufacturing labor-hour

$20

Job M1

Job M2

Direct manufacturing labor costs

$273,000

$208,000

Direct manufacturing labor hours

($273,000

$26; $208,000

$26)

10,500

8,000

Manufacturing overhead cost allocated

(10,500

$20; 8,000

$20)

$210,000

$160,000

Job Costs May 2011

Job M1

Job M2

Direct materials

$ 78,000

$ 51,000

Direct manufacturing labor

273,000

208,000

Manufacturing overhead allocated

210,000

160,000

Total costs

$561,000

$419,000

2.

Number of pipes produced for Job M1

1,100

Cost per pipe ($561,000

1,100)

$510

3.

Finished Goods Control 561,000

Work-in–Process Control 561,000

4. Rafael Company began May 2011 with no work-in-process inventory. During May, it started

4-28 (20−30 min.) Job costing; actual, normal, and variation from normal costing.

1. Actual direct cost rate for professional labor = $59 per professional labor-hour

Actual indirect cost rate =

$735,000

17,500 hours

= $42 per professional labor-hour

Budgeted direct cost rate

$990,000

18,000 hours

4-24

Although not required, the following overview diagram summarizes Chico’s job-costing

system.

Audit

Support

Professional

Labor-Hours

Indirect Costs

Direct Costs

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

COST OBJECT:

JOB FOR

AUDITING

PIERRE

& CO.

DIRECT

COST

Professional

Labor

4-29 (20−30 min.) Job costing; actual, normal, and variation from normal costing.

1. Actual direct cost rate for architectural labor = $92 per architectural labor-hour

Actual indirect cost rate =

$1,729,500

34,590

= $50 per architectural labor-hour

Budgeted direct cost rate

$2,880,000

$1,728,000

4-30 (30 min.) Proration of overhead.

overhead rate

1. Budgeted manufacturing

=

Budgeted manufacturing overhead cost

Budgeted direct manufacturing labor cost

$250,000

2. Overhead allocated = 50%

Actual direct manufacturing labor cost

= 50%

$228,000 = $114,000

Underallocated

manufacturing

overhead

=

Actual

manufacturing

overhead costs

–

Allocated plant

overhead costs

= $117,000 – $114,000 = $3,000

Underallocated manufacturing overhead = $3,000

3a. All underallocated manufacturing overhead is written off to cost of goods sold.

Both work in process (WIP) and finished goods inventory remain unchanged.

Account

Dec. 31, 2011

Balance

(Before Proration)

(1)

Proration of $3,000

Underallocated

Manuf. Overhead

(2)

Dec. 31, 2011

Balance

(After Proration)

(3) = (1) + (2)

WIP

$ 50,700

$ 0

$ 50,700

Finished Goods

245,050

0

245,050

Cost of Goods Sold

549,250

3,000

552,250

Total

$845,000

$3,000

$848,000

Account

Dec. 31, 2011

Account Balance

(Before Proration)

(1)

Account

Balance as a

Percent of Total

(2) = (1) ÷ $845,000

Proration of $3,000

Underallocated

Manuf. Overhead

(3) = (2)

$3,000

Dec. 31, 2011

Account Balance

(After Proration)

(4) = (1) + (3)

WIP

$ 50,700

0.06

0.06

$3,000 = $ 180

$ 50,880

Finished Goods

245,050

0.29

0.29

$3,000 = 870

245,920

Cost of Goods Sold

549,250

0.65

0.65

$3,000 = 1,950

551,200

Total

$845,000

1.00

$3,000

$848,000

3c. Underallocated manufacturing overhead prorated based on 2011 overhead in ending

balances:

Account

Dec. 31, 2011

Account

Balance

(Before

Proration)

(1)

Allocated

Manuf.

Overhead in

Dec. 31, 2011

Balance

(Before

Proration)

(2)

Allocated Manuf.

Overhead in

Dec. 31, 2011

Balance as a

Percent of Total

(3) = (2) ÷ $114,000

Proration of $3,000

Underallocated

Manuf. Overhead

(4) = (3)

$3,000

Dec. 31, 2011

Account

Balance

(After

Proration)

(5) = (1) + (4)

WIP

$ 50,700

$ 10,260a

0.09

0.09

$3,000 = $ 270

$ 50,970

Finished Goods

245,050

29,640b

0.26

0.26

$3,000 = 780

245,830

Cost of Goods Sold

549,250

74,100c

0.65

0.65

$3,000 = 1,950

551,200

Total

$845,000

$114,000

1.00

$3,000

$848,000

a,b,c Overhead allocated = Direct manuf. labor cost

50% = $20,520; $59,280; $148,200

50%

4. Writing off all of the underallocated manufacturing overhead to Cost of Goods Sold (CGS) is

usually warranted when CGS is large relative to Work-in–Process and Finished Goods Inventory

4-31 (20−30 min) Job costing, accounting for manufacturing overhead, budgeted rates.

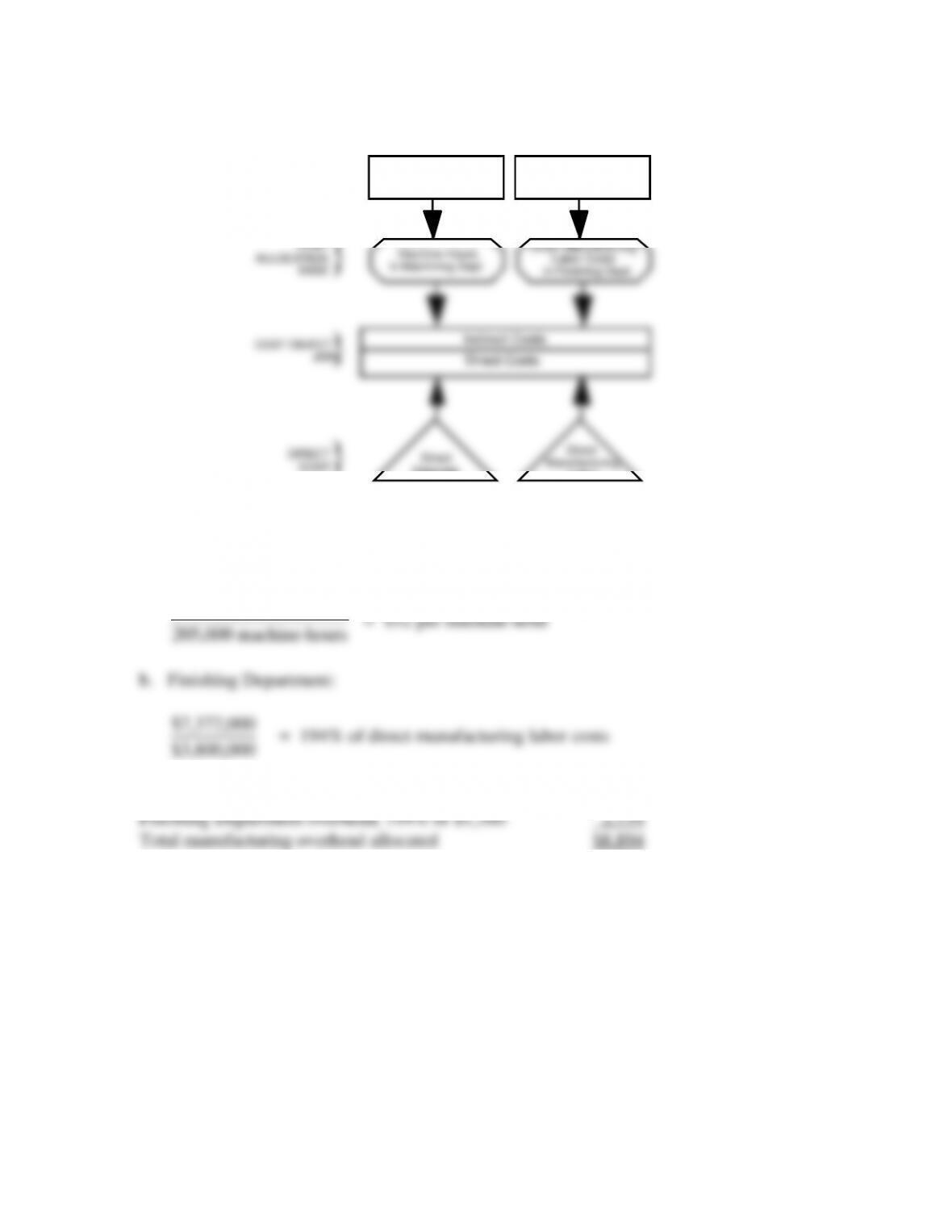

1. An overview of the job-costing system is:

COST OBJECT:

PRODUCT

COST

ALLOCATION

BASE

DIRECT

COST

Machining Department

Manufacturing Overhead

Machine-Hours

in Machining Dept.

Direct

Materials

INDIRECT

COST

POOL

Direct

Manufacturing

Labor

Indirect Costs

Direct Costs

Finishing Department

Manufacturing Overhead

Direct Manufacturing

Labor Costs

in Finishing Dept.

2. Budgeted manufacturing overhead divided by allocation base:

a. Machining Department:

$10,660,000

205,000 machine-hours

= $52 per machine-hour

b. Finishing Department:

$7,372,000

$3,800,000

= 194% of direct manufacturing labor costs

3. Machining Department overhead, $52 130 machine-hours $6,760

COST OBJECT:

JOB

4-29

4. Total costs of Job 431:

Direct costs:

Direct materials––Machining Department $15,500

––Finishing Department 5,000

rate.

5.

Machining Finishing

Manufacturing overhead incurred (actual) $11,070,000 $8,236,000

6. A homogeneous cost pool is one where all costs have the same or a similar cause-and–

effect or benefits-received relationship with the cost-allocation base. Fasano likely assumes that

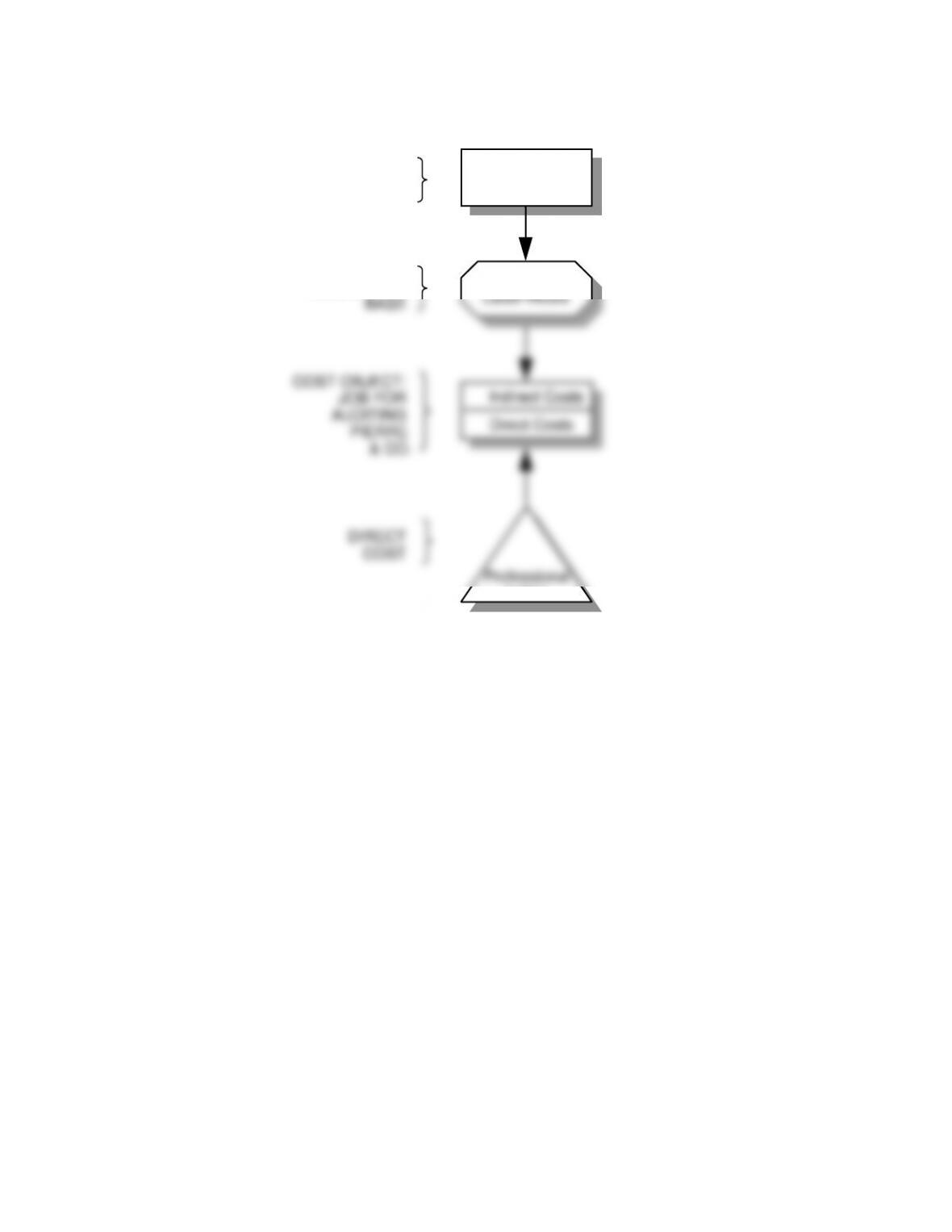

1.

Professional

Labor-Hours

Legal

Support

COST OBJECT:

JOB FOR

CLIENT

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

}

DIRECT

COST

Indirect Costs

Direct Costs

Professional

Labor

2.

Budgeted professional

labor-hour direct cost rate

=

Budgeted direct labor compensation per professional

Budgeted direct labor-hours per professional

=

$104,000

1,600 hours

Budgeted indirect

cost rate

=

Budgeted total costs in indirect cost pool

Budgeted total professional labor-hours

$2,200,000

4.

Richardson

Punch

Direct costs:

Professional labor, $65 100; $65 150

Indirect costs:

Legal support, $55 100; $55 150

$ 6,500

5,500

$12,000

$ 9,750

8,250

$18,000

3.