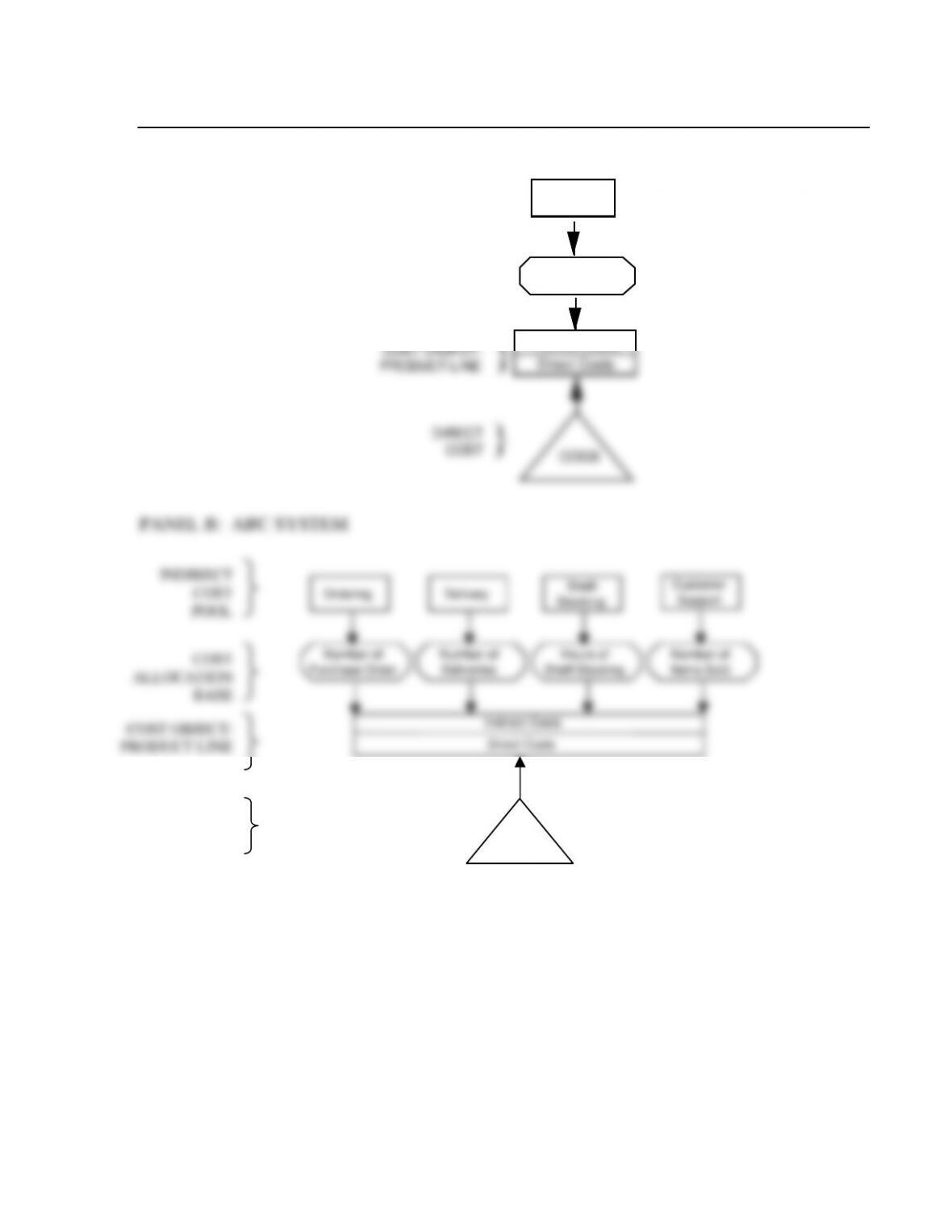

SOLUTION EXHIBIT 5-24

Product-Costing Overviews of Family Supermarkets

PANEL A: SIMPLE COSTING SYSTEM

COST OBJECT:

PRODUCT LINE

Indirect Costs

Direct Costs

Store

Support

COGS

COGS

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

DIRECT

COST

PANEL B: ABC SYSTEM

Ordering Delivery Shelf-

Stocking

Customer

Support

Number of

Purchase Order

Number of

Deliveries

Hours of

Shelf-Stocking

Number of

Items Sold

Indirect Costs

Direct Costs

COGS

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

COST OBJECT:

PRODUCT LINE

DIRECT

COST

5-22

5-25 (15–20 min.) ABC, wholesale, customer profitability.

Chain

1 2 3 4

Gross sales $55,000 $25,000 $100,000 $75,000

Sales returns 11,000 3,500 7,000 6,500

Net sales 44,000 21,500 93,000 68,500

(21.6%) to 23.15%. Immediate attention to Chain 2 is required which is currently showing a loss

contribution. The chain has a disproportionate number of both regular orders and rush orders.

improved.

5-23

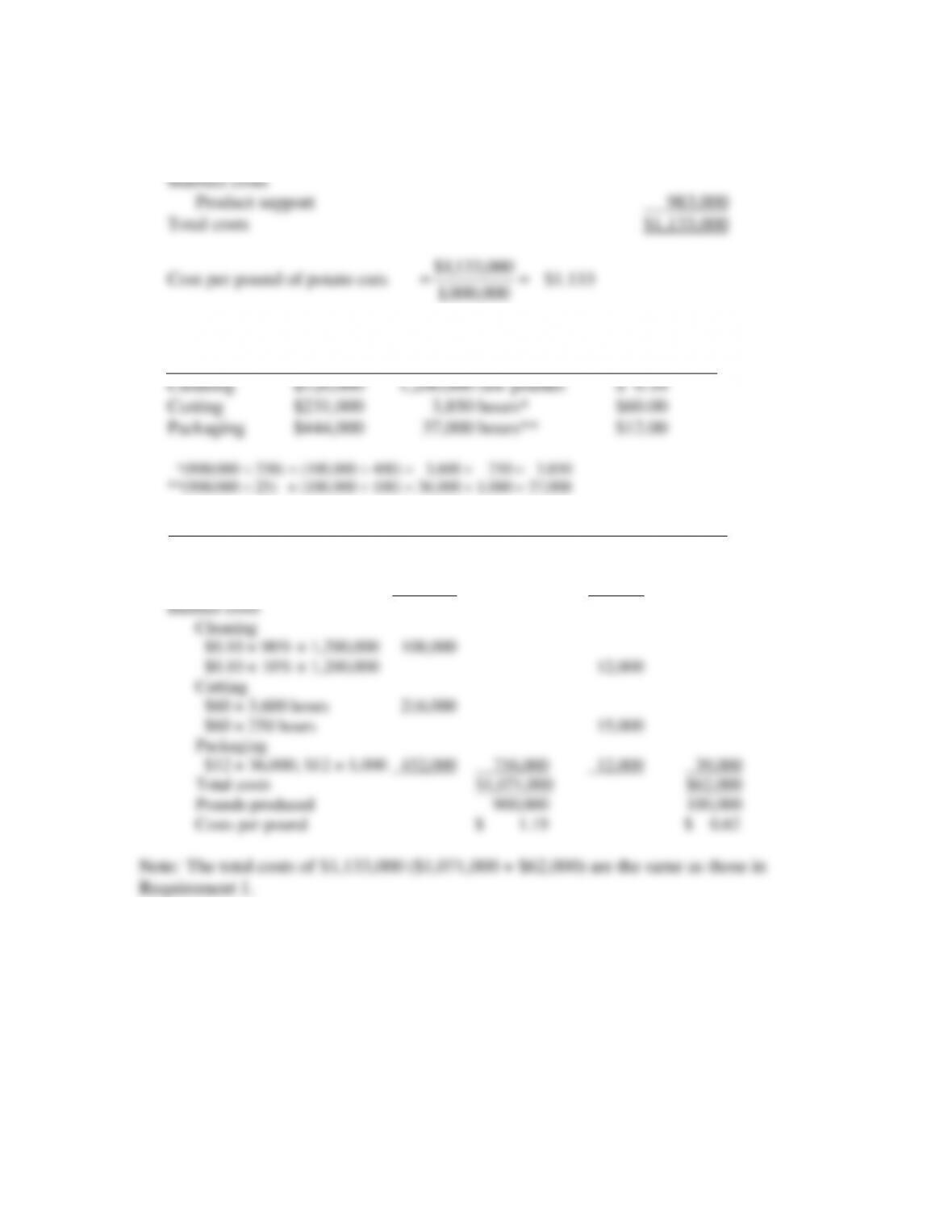

5-26 (50 min.) ABC, activity area cost-driver rates, product cross-subsidization.

1. Direct costs

Direct materials $ 150,000

000,000,1

2. Cost Costs in Number of Costs per

Pool Pool Driver Units Driver Unit

3. Retail Potato Cuts Institutional Potato Cuts

Direct costs

Direct materials $135,000 $15,000

Packaging 180,000 $ 315,000 8,000 $23,000

5-24

4. There is much evidence of product-cost cross-subsidization.

Cost per Pound Retail Institutional

Simple costing system $1.133 $1.133

ABC system $1.190 $0.620

Assuming the ABC numbers are more accurate, potato cuts sold to the retail market are

Cutting 93.5 6.5 100.0

Packaging 97.3 2.7 100.0

Units produced 90.0% 10.0% 100.0%

Idaho can use the revised cost information for a variety of purposes:

a. Pricing/product emphasis decisions. The sizable drop in the reported cost of potatoes

Packaging 16.8 12.90

Indirect costs

Cleaning 10.1 19.35

Cutting 20.2 24.20

Packaging 40.3 19.35

5-25

1. Overhead allocation using a simple job-costing system, where overhead is allocated based

on machine hours:

2. Overhead allocation using an activity-based job-costing system:

Budgeted

Overhead

(1)

Activity Driver

(2)

Budgeted

Activity Driver

(3)

Activity Rate

(4) = (1) (3)

Purchasing

$ 70,000

Purchase orders

processed

2,000

$35.00

Material handling

$ 87,500

Material moves

5,000

$17.50

Machine maintenance

$ 237,300

Machine hours

10,500

$22.60

Product inspection

$ 18,900

Inspections

1,200

$15.75

Packaging

$ 39,900

Units produced

3,800

$10.50

$ 453,600

Job 215

Job 325

Overhead allocated

Purchasing ($35 25; 8 orders)

$ 875.00

$ 280.00

Material handling ($17.50 10; 4 moves)

175.00

70.00

Machine maintenance ($22.60 40; 60 hours)

904.00

1,356.00

Product inspection ($15.75 9; 3 inspections)

141.75

47.25

Packaging ($10.50 15; 6 units)

157.50

63.00

Total

$2,253.25

$1,816.25

3. The manufacturing manager likely would find the ABC job-costing system more useful in

cost management. Unlike direct manufacturing labor costs, the five indirect cost pools are

systematically linked to the activity areas at the plant. The result is more accurate product

5-28 (30 min.) ABC, product-costing at banks, cross-subsidization.

1.

Holt

Turner

Graham

Total

Revenues

Spread revenue on annual basis

(3% ; $1,100, $700, $24,600)

Monthly fee charges

($22 ; 0, 12, 0)

Total revenues

$ 33.00

0.00

33.00

$ 21.00

264.00

285.00

$738.00

0.00

738.00

$ 792.00

264.00

1,056.00

Costs

Deposit/withdrawal with teller

$2.30

42; 48; 5

Deposit/withdrawal with ATM

$0.70

7; 19; 17

Deposit/withdrawal on prearranged basis

$0.40

0; 13; 62

Bank checks written

$8.40

11; 1; 3

Foreign currency drafts

$12.40

4; 2; 6

Inquiries

$1.40

12; 20; 9

Total costs

Operating income (loss)

96.60

4.90

0.00

92.40

49.60

16.80

260.30

$(227.30)

110.40

13.30

5.20

8.40

24.80

28.00

190.10

$ 94.90

11.50

11.90

24.80

25.20

74.40

12.60

160.40

$577.60

218.50

30.10

30.00

126.00

148.80

57.40

610.80

$ 445.20

The assumption that the Holt and Graham accounts exceed $1,000 every month and the

Turner account is less than $1,000 each month means the monthly charges apply only to Turner.

One student with a banking background noted that in this solution 100% of the spread is

attributed to the “depositor side of the bank.” He noted that often the spread is divided between

the “depositor side” and the “lending side” of the bank.

2. Cross-subsidization across individual Premier Accounts occurs when profits made on

some accounts are offset by losses on other accounts. The aggregate profitability on the three

customers is $445.20. The Graham account is highly profitable, $577.60, while the Holt account

is sizably unprofitable. The Turner account shows a small profit but only because of the $264

5-27

3. Possible changes NSB could make are:

a. Offer higher interest rates on high-balance accounts to increase NSB’s

competitiveness in attracting and retaining these accounts.

firm.

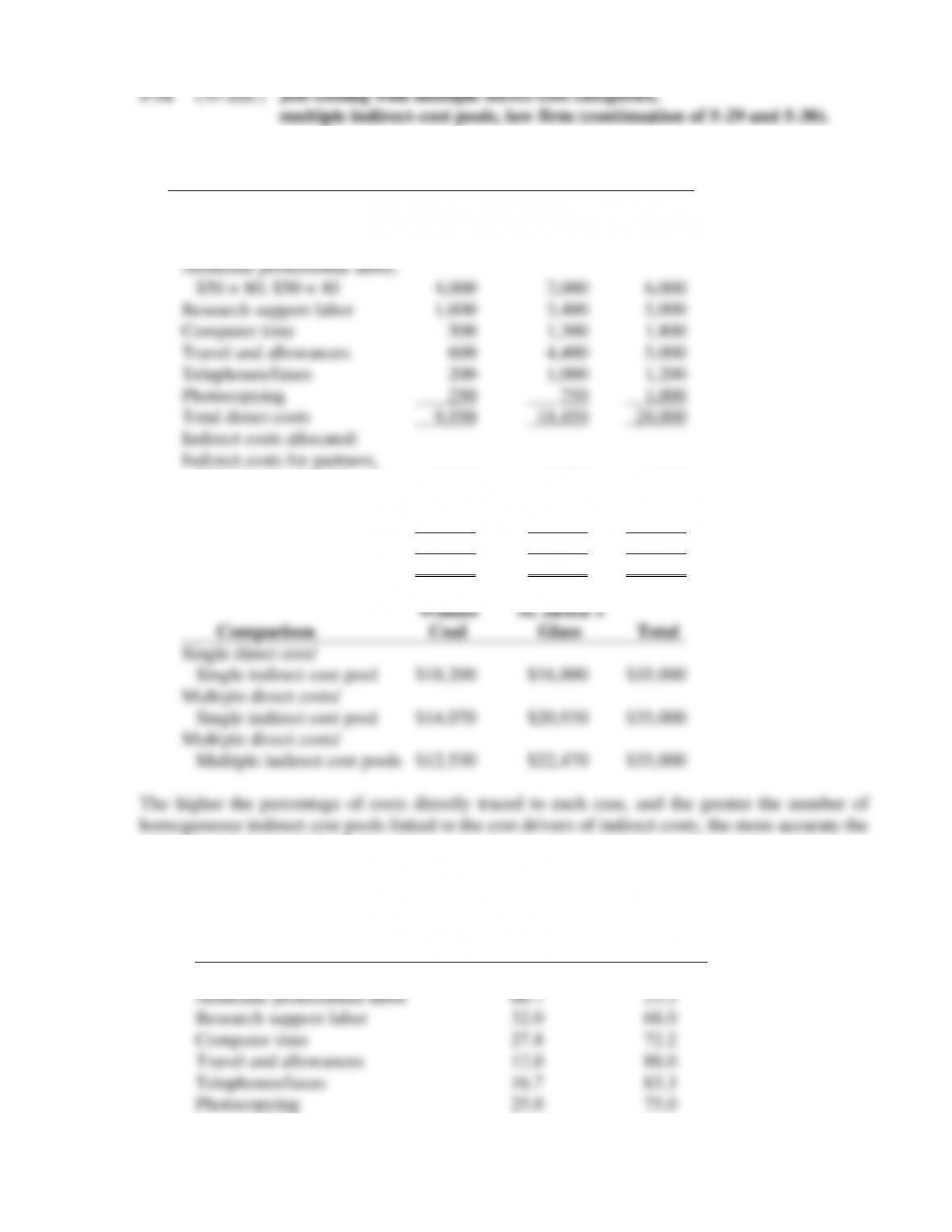

1. Pricing decisions at Wigan Associates are heavily influenced by reported cost numbers.

Suppose Wigan is bidding against another firm for a client with a job similar to that of Widnes

2. Widnes St. Helen’s

Coal Glass Total

5-28

1. Indirect costs = $7,000

2. Widnes St. Helen’s

Coal Glass Total

Direct costs:

Direct professional labor,

3.

Widnes St. Helen’s

Coal Glass Total

Problem 5-30 14,070 20,930 35,000

The Problem 5-30 approach directly traces $14,000 of general support costs to the individual

5-29

1. Widnes St. Helen’s

Coal Glass Total

Direct costs:

Partner professional labor,

$100 × 24; $100 × 56 $ 2,400 $ 5,600 $ 8,000

$57.50 × 24; $57.50 × 56 1,380 3,220 4,600

Indirect costs for associates,

$20 × 80; $20 × 40 1,600 800 2,400

Total indirect costs 2,980 4,020 7,000

Total costs to be billed $12,530 $22,470 $35,000

product cost of each individual case.

The Widnes and St. Helen’s cases differ in how they use “resource areas” of Wigan Associates:

Widnes St. Helen’s

Coal Glass

Partner professional labor 30.0% 70.0%

5-30

The Widnes Coal case makes relatively low use of the higher-cost partners but relatively higher

use of the lower-cost associates than does St. Helen’s Glass. As a result, it also uses less of the

2. The specific areas where the multiple direct/multiple indirect (MD/MI) approach can

provide better information for decisions at Wigan Associates include:

Pricing and product (case) emphasis decisions. In a bidding situation using single direct/single

indirect (SD/SI) or multiple direct/single indirect (MD/SI) data, Wigan may win bids for legal

cases on which it will subsequently lose money. It may also not win bids on which it would