17-31

SOLUTION EXHIBIT 17-34B

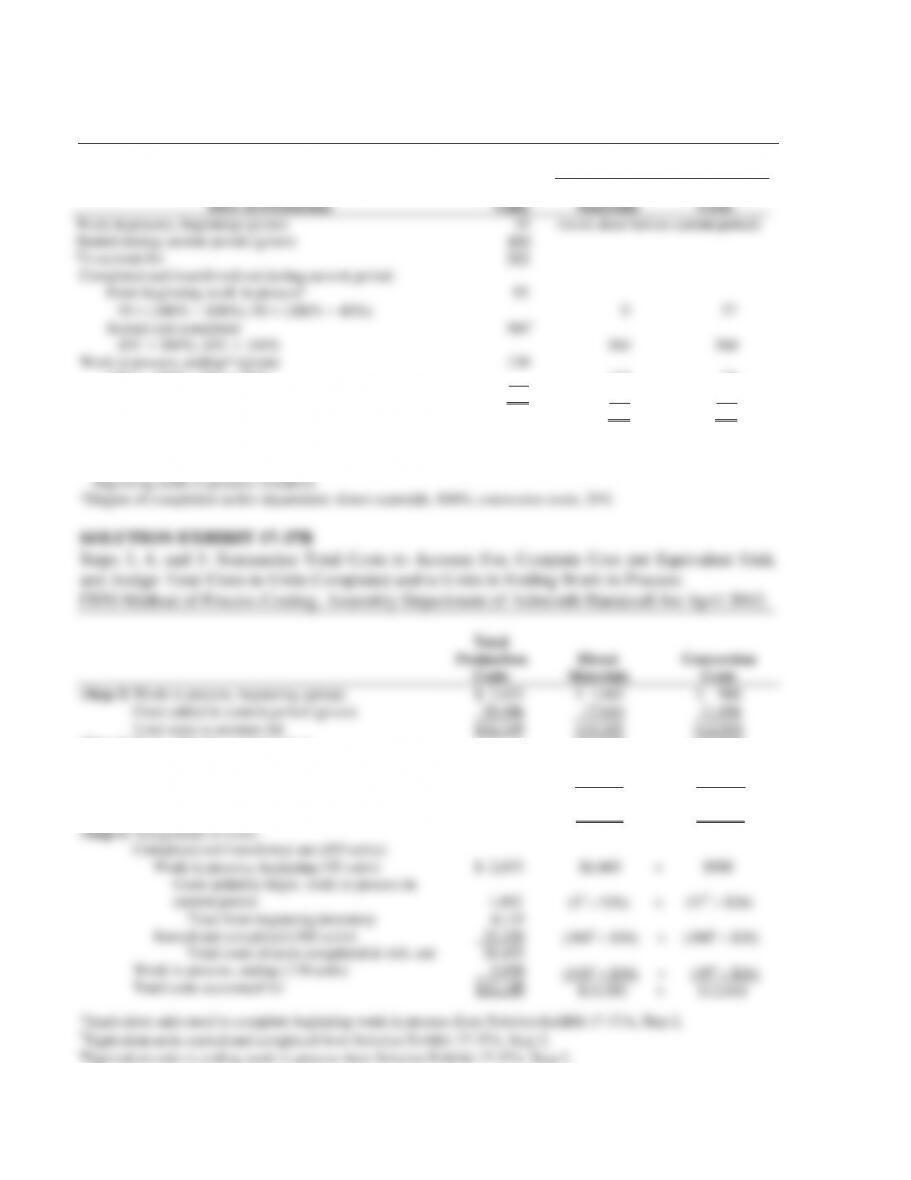

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to

Units Completed and to Units in Ending Work in Process;

FIFO Method of Process Costing,

Testing Department of Larsen Company for October 2012.

Total

Production

Costs

Transferred-in

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

$ 3,717,335

$ 2,881,875

$ 0

$ 835,460

Costs added in current period (given)

21,395,850

7,735,250

9,704,700

3,955,900

Total costs to account for

$25,113,185

$10,617,125

$9,704,700

$4,791,360

(Step 4) Costs added in current period

$ 7,735,250

$9,704,700

$3,955,900

Divide by equivalent units of work done in

current period (Solution Exhibit 17–34A)

22,500

26,300

23,270

Cost per equiv. unit of work done in current period

$ 343.79

$ 369.00

$ 170.00

(Step 5) Assignment of costs:

Completed and transferred out (26,300 units):

Work in process, beginning (7,500 units)

Costs added to beg. work in process in current period

$ 3,717,335

3,150,000

$2,881,875 + $0 + $835,460

(0* $343.79) + (7,500* $369.00) + (2,250* $170.00)

Total from beginning inventory

Started and completed (18,800 units)

Total costs of units completed & transferred out

Work in process, ending (3,700 units)

6,867,335

16,596,431

23,463,766

1,649,419

(18,800† $343.79) + (18,800† $369.00) + (18,800† $170.00)

(3,700# $343.79) + (0# $369.00) + (2,220# $170.00)

Total costs accounted for

$25,113,185

$10,617,125

+ $9,704,700

+ $4,791,360

*Equivalent units used to complete beginning work in process from Solution Exhibit 17-34A, Step 2.

†Equivalent units started and completed from Solution Exhibit 17-34A, Step 2.

#Equivalent units in ending work in process from Solution Exhibit 17-34A, Step 2.

17-32

17-35 (25 min.) Weighted-average method.

Solution Exhibit 17-35A shows equivalent units of work done to date of:

Direct materials 625 equivalent units

Conversion costs 525 equivalent units

Note that direct materials are added when the Assembly Department process is 10%

17-33

SOLUTION EXHIBIT 17-35B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit,

and Assign Total Costs to Units Completed and to Units in Ending Work in Process;

Weighted-Average Method of Process Costing, Assembly Department of Ashworth, April 2012.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

$ 2,653

$ 1,665

$ 988

Costs added in current period (given)

29,496

17,640

11,856

Total costs to account for

$32,149

$19,305

$12,844

(Step 4) Costs incurred to date

$19,305

$12,844

Divide by equivalent units of work done to

date (Solution Exhibit 17-35A)

585

494

Cost per equivalent unit of work done to date

$ 33

$ 26

(Step 5) Assignment of costs:

Completed and transferred out (455 units)

$26,845

(455* $33) + (455* $26)

Work in process, ending (130 units)

5,304

(130† $33) + (39† $26)

Total costs accounted for

$32,149

$19,305

+ $12,844

*Equivalent units completed and transferred out from Solution Exhibit 17-35A, Step 2.

†Equivalent units in ending work in process from Solution Exhibit 17-35A, Step 2.

17-34

1. Work in Process–– Assembly Department 17,640

2. Work in Process–– Assembly Department 11,856

3. Work in Process––Finishing Department 26,845

Work in Process–– Assembly Department 26,845

1. Direct materials 17,640 Work in Process––Finishing 26,845

17-37 (20 min.) FIFO method (continuation of 17-35).

The equivalent units of work done in April 2012 in the Assembly Department for direct materials

and conversion costs are shown in Solution Exhibit 17-37A.

Solution Exhibit 17-37B summarizes the total Assembly Department costs for April 2012,

SOLUTION EXHIBIT 17-37A

Steps 1 and 2: Summarize Output in Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing, Assembly Department of Ashworth Handcraft for April 2012.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

To account for

95

490

585

(work done before current period)

Completed and transferred out during current period:

From beginning work in process§

95

(100% − 100%); 95

(100% − 40%)

95

0

57

Started and completed

455

100%; 455

100%

360†

360

360

Work in process, ending* (given)

130

100%; 130

30%

130

130

39

Accounted for

585

Equivalent units of work done in current period

490

456

§Degree of completion in this department: direct materials, 100%; conversion costs, 40%.

†455 physical units completed and transferred out minus 95 physical units completed and transferred out from

$ 988

Costs added in current period (given)

11,856

Total costs to account for

$11,856

period

$ 26

Completed and transferred out (455 units):

1. Solution Exhibit 17–38A computes the equivalent units of work done to date in the

Binding Department for transferred-in costs, direct materials, and conversion costs.

method.

2. Journal entries:

a. Work in Process–– Binding Department 129,600

Work in Process––Printing Department 129,600

Cost of goods completed and transferred out

during April from the Printing Department

SOLUTION EXHIBIT 17-38B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit, and Assign Total Costs to

Units Completed and to Units in Ending Work in Process;

Weighted-Average Method of Process Costing,

1. Solution Exhibit 17-39A calculates the equivalent units of work done in April 2012 in the

Binding Department for transferred-in costs, direct materials, and conversion costs.

Solution Exhibit 17-39B summarizes total Binding Department costs for April 2012,

calculates the cost per equivalent unit of work done in April 2012 in the Binding Department for

2. The equivalent units of work done in beginning inventory is: Transferred-in costs, 1,050

100% = 1,050; direct materials, 1,050 0% = 0; and conversion costs, 1,050 50% = 525. The