20-18

SOLUTION EXHIBIT 20-30

Annual Relevant Costs of Current Purchasing Policy and JIT Purchasing Policy

for Margro Corporation

Relevant

Costs under

Current

Purchasing

Policy

Relevant

Costs under

JIT

Purchasing

Policy

Required return on investment

20% per year

$600,000 of average inventory per year

$120,000

20% per year

$0 inventory per year

$ 0

Annual insurance and property tax costs

14,000

0

Warehouse rent

60,000

(13,500)a

Overtime costs

No overtime

0

Overtime premium

40,000

Stockout costs

No stockouts

0

$6.50b contribution margin per unit

20,000 units

130,000

Total incremental costs

$194,000

$156,500

Difference in favor of JIT purchasing $37,500

a$(13,500) = Warehouse rental revenues, [(75%

12,000)

$1.50].

20-19

20-31 (25 min.) Supply chain effects on total relevant inventory costs.

1. The relevant costs of purchasing from Maji and Induk are:

Cost Category

Maji

Induk

Purchase costs

10,000 boards × $93 per board

10,000 boards × $90 per board

$930,000

900,000

Ordering costs

50 orders × $10 per order

50 orders × $8 per order

500

400

Inspection costs

10,000 boards × 5% × $5 per board

10,000 boards × 25% × $5 per board

2,500

12,500

Required annual return on investment

100 boards × $93 per board × 10%

100 boards × $90 per board × 10%

930

900

Stockout costs

100 boards × $5 per board

300 boards × $8 per board

500

2,400

Return costs

50 boards × $25 per board

500 boards × $25 per board

1,250

12,500

Other carrying costs

100 boards × $2.50 per board per year

100 boards × $2.50 per board per year

250

250

Total Cost

$935,930

$928,950

2. While Induk will save Cow Spot $6,980 ($935,930 − $928,950), Cow Spot may still choose

to use Maji for the following reasons:

a. The savings are less than 1% of the total cost of the mother boards.

20-20

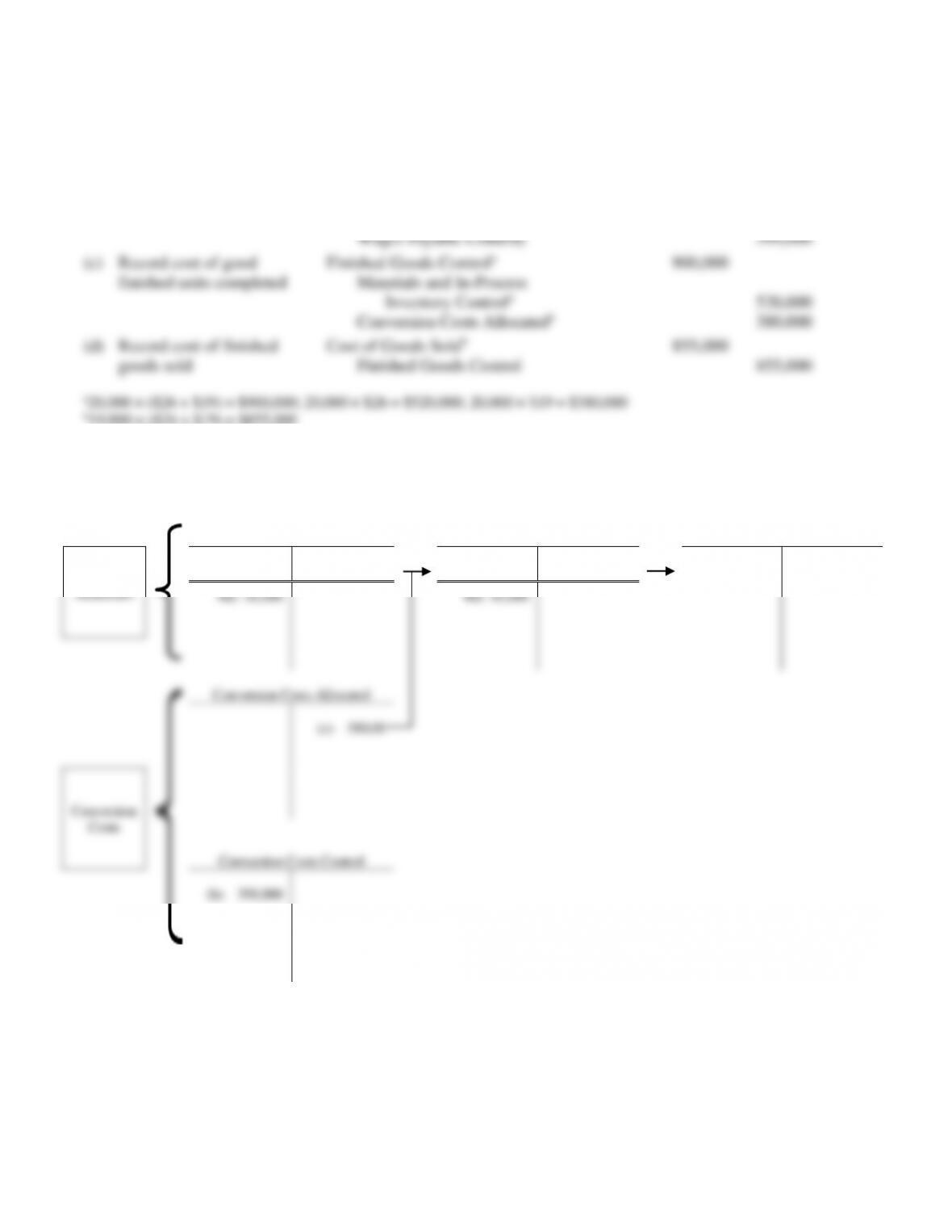

20-32 (20 min.) Blackflush costing and JIT production.

1.

(a) Record purchases of

direct materials

Materials and In-Process Inventory Control

Accounts Payable Control

546,000

546,000

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

399,000

Wages Payable Control)

399,000

(c) Record cost of good

finished units completed

Finished Goods Controla

Materials and In-Process

900,000

Inventory Controla

520,000

Conversion Costs Allocateda

380,000

(d) Record cost of finished

goods sold

Cost of Goods Soldb

Finished Goods Control

855,000

855,000

2.

Materials and In-Process

Inventory Control

Finished Goods Control

Cost of Goods Sold

Direct

Materials

(a) 546,000

(c) 520,000

(c) 900,000

(d) 855,000

(d) 855,000

Bal. 26,000

Bal. 45,000

Conversion Costs Allocated

(c) 380,00

Conversion

Costs

Conversion Costs Control

(b) 399,000

20-21

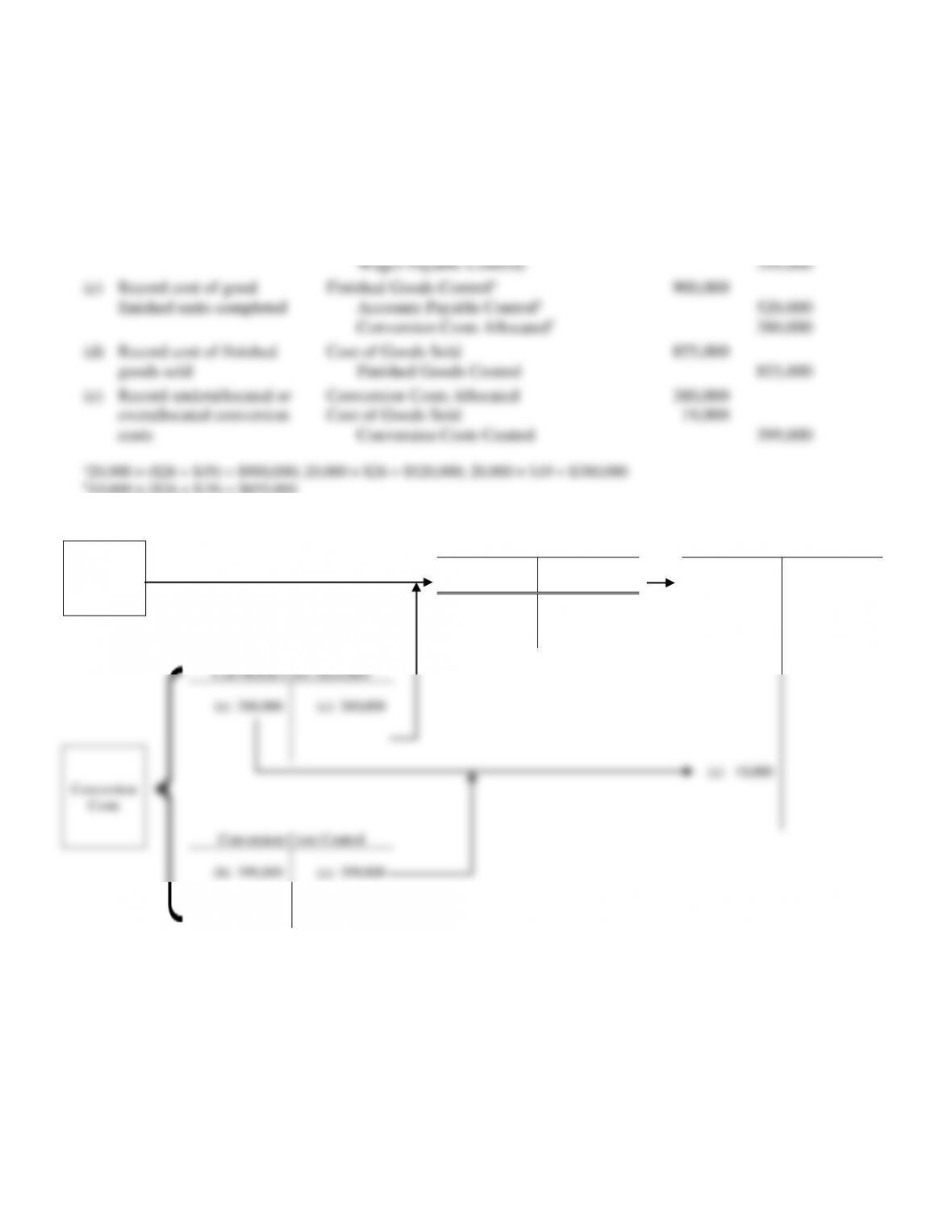

20-33 (20 min.) Backflush, two trigger points, materials purchase and sale

(continuation of 20-32).

1.

(a) Record purchases of

direct materials

Inventory Control

Accounts Payable Control

546,000

546,000

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

399,000

Wages Payable Control)

399,000

(c) Record cost of good

finished units completed

No entry

(d) Record cost of finished

goods sold

Cost of Goods Solda

Inventory Controla

855,000

494,000

Conversion Costs Allocateda

361,000

(e) Record underallocated or

overallocated conversion

costs

Conversion Costs Allocated

Cost of Goods Sold

Conversion Costs Control

361,000

38,000

399,000

2.

Inventory Control

Cost of Goods Sold

Direct

Materials

(a) 546,000

(d) 494,000

(d) 855,000

Bal. 52,000

Conversion Costs Allocated

(e) 361,000

(d) 361,000

Conversion

Costs

(e) 38,000

Conversion Costs Control

(b) 399,000

(e) 399,000

20-22

20-34 (20 min.) Backflush, two trigger points, completion of production and sale

(continuation of 20-32).

1.

(a) Record purchases of

direct materials

No Entry

(b) Record conversion costs

incurred

Conversion Costs Control

Various Accounts (such as

399,000

Wages Payable Control)

399,000

(c) Record cost of good

finished units completed

Finished Goods Controla

Accounts Payable Controla

900,000

520,000

Conversion Costs Allocateda

380,000

(d) Record cost of finished

goods sold

Cost of Goods Sold

Finished Goods Control

855,000

855,000

(e) Record underallocated or

overallocated conversion

costs

Conversion Costs Allocated

Cost of Goods Sold

Conversion Costs Control

380,000

19,000

399,000

a20,000 × ($26 + $19) = $900,000; 20,000 × $26 = $520,000; 20,000 × $19 = $380,000

b19,000 × ($26 + $19) = $855,000

2.

Finished Goods Control

Cost of Goods Sold

Direct

Materials

(c) 900,000

(d) 855,000

(d) 855,000

Bal. 45,000

Conversion Costs Allocated

(e) 380,000

(c) 380,000

Conversion

Costs

(e) 19,000

Conversion Costs Control

(b) 399,000

(e) 399,000

20-23

20-35 (20 min.) Lean accounting.

1. The cost object in lean accounting is the value stream, not the individual product. FSD

has identified two distinct value streams: Mechanical Devices and Electronic Devices. All direct

2. Operating income under lean accounting are the following (in thousands of dollars):

Mechanical

Devices

Electronic

Devices

Sales ($700 + $500; $900 + $450)

$1,200

$1,350

Costs

Direct materials purchased

($210 + $120; $250 + $90)

330

340

Direct manufacturing labor

($150 + $75; $200 + $60)

225

260

Equipment costs

($90 + $120; $200 + $95)

210

295

Design and marketing costs

($95 + $50; $105 + $42)

145

147

Plant facility costs

($200,000 × 40%)

($200,000 × 50%)

80

100

Value stream operating income

$ 210

$ 208

In addition to the differences discussed in Requirement 1, FSD’s lean accounting system

accounts for direct materials as expenses in the period the materials are purchased. The

following factors explain the differences between traditional operating income and lean

accounting income for the two value streams (in thousands of dollars):

Mechanical

Devices

Electronic

Devices

Traditional operating income

($100 + $105; $45 + $140)

$205

$185

Additional cost of direct materials purchased

over direct materials used

($330 − $200 – $100; $340 − $250 – $75)

(30)

(15)

Decrease in allocated plant-level overhead

($50 + $40 – $80; $80 + $30 – $100)

10

10

Add back allocated corporate overhead costs

($15 + $10; $20 + $8)

25

28

Value stream operating income

$210

$208

20-24

20-36 (20 min.) JIT production, relevant benefits, relevant costs, ethics.

2. As part of the IMA’s Standards of Ethical Professional Practice, Sue Winston, the

company controller has an obligation under the competence standard to “provide decision

3. It is understandable that Jim Ingram the company’s operations manager would be

concerned about potential layoffs in his department and the resulting morale issues.

However, recommendations could include 1) fully engage the production staff in the

upcoming changes to minimize negative morale issues 2) retrain existing staff to manage

the new JIT production and purchasing system, so as to avoid as many potential layoffs, as