8-41

7. Fixed Setup Overhead Variance Analysis for Jo Nathan Publishing Company for 2012

Actual Static Budget Standard Hours

8. Rejecting an order may have implications for future orders (i.e., professors would be

reluctant to order books from this publisher again). Jo Nathan should consider factors

such as prior history with the customer and potential future sales.

8-42

1. and 2. Fixed Overhead Variance Analysis for Dawn Floral Creations, Inc. for February

Actual Fixed Static Budget Standard Hours

Overhead Fixed Overhead × Budgeted Rate

3. An unfavorable production-volume variance measures the cost of unused capacity. Production

at capacity would result in a production-volume variance of 0 since the fixed overhead rate is

based upon expected hours at capacity production. However, the existence of an unfavorable

volume variance does not necessarily imply that management is doing a poor job or incurring

unnecessary costs. Using the suggestions in the problem, two reasons can be identified.

8-43

4. The static-budget operating income for February is:

Revenues $55 × 1,000 $55,000

Variable costs $25 × 1,000 25,000

Fixed overhead costs 9,000

Static-budget operating income $21,000

Equivalently, the sales-volume variance captures the fact that when Dawn sells 600 units instead

of the budgeted 1,000, only the revenue and the variable costs are affected. Fixed costs remain

unchanged. Therefore, the shortfall in profit is equal to the budgeted contribution margin per

unit times the shortfall in output relative to budget.

Sales-volume

variable cost

units sold relative to the

8-44

The $3,600 U production-volume variance explains the difference between operating income

based on the budgeted profit per unit and the flexible-budget operating income:

Operating income based on budgeted profit per unit $12,600

Production-volume variance 3,600 U

Flexible-budget operating income $ 9,000

8-45

8-38 (30−40 min.) Comprehensive review of Chapters 7 and 8, working backward from

given variances.

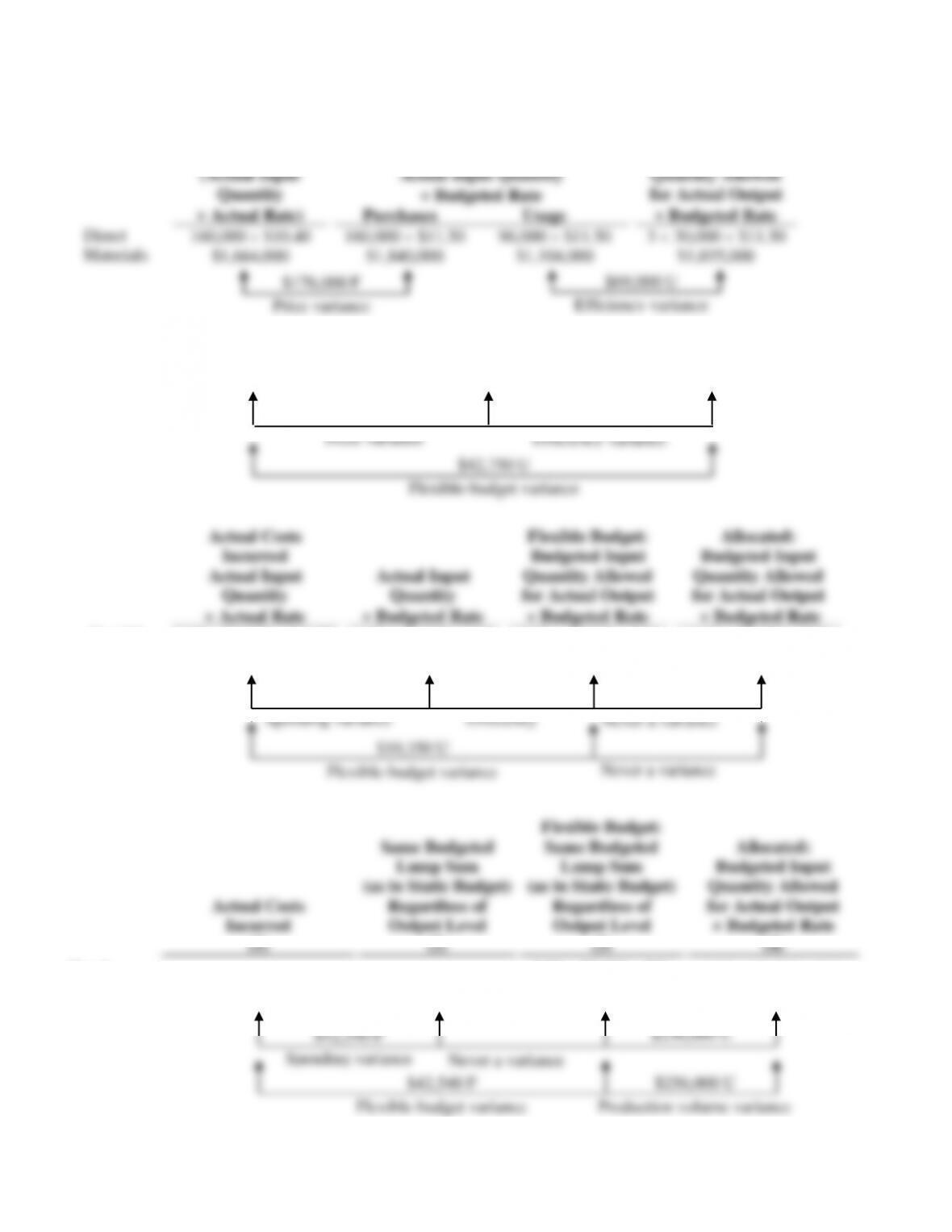

1. Solution Exhibit 8-38 outlines the Chapter 7 and 8 framework underlying this solution.

a. Pounds of direct materials purchased = $176,000 ÷ $1.10 = 160,000 pounds

b. Pounds of excess direct materials used = $69,000 ÷ $11.50 = 6,000 pounds

c. Variable manufacturing overhead spending variance = $10,350 – $18,000 = $7,650 F

2. The control of variable manufacturing overhead requires the identification of the cost drivers

for such items as energy, supplies, and repairs. Control often entails monitoring nonfinancial

measures that affect each cost item, one by one. Examples are kilowatts used, quantities of

SOLUTION EXHIBIT 8-38

Actual Costs

Incurred

(Actual Input

Quantity

Actual Rate)

Actual Input Quantity

Budgeted Rate

Purchases Usage

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

Budgeted Rate

Direct

Materials

160,000 $10.40

$1,664,000

160,000 $11.50

$1,840,000

96,000 $11.50

$1,104,000

3 30,000 $11.50

$1,035,000

Direct

Manuf.

Labor

0.85 30,000 $20.50

$522,750

0.85 30,000 $20

$510,000

0.80 30,000 $20

$480,000

$176,000 F

Price variance

$69,000 U

Efficiency variance

$12,750 U

Price variance

$30,000 U

Efficiency variance

Quantity

Budgeted Rate

Variable

0.80 30,000 $12

8-47

8-39 (30−50 min.) Review of Chapters 7 and 8, 3-variance analysis.

1. Total standard production costs are based on 7,800 units of output.

Direct materials, 7,800 $15.00

7,800 3 lbs. $5.00 (or 23,400 lbs. $5.00) $ 117,000

Direct manufacturing labor, 7,800 $75.00

2. Solution Exhibit 8-39 presents a columnar presentation of the variances. An overview of

the 3-variance analysis using the block format of the text is:

3-Variance

Analysis

Spending

Variance

Efficiency

Variance

Production

Volume Variance

Total Manufacturing

Overhead

$39,400 U

$6,600 U

$8,000 U