8-31

8-31 (30−40 min.) Graphs and overhead variances.

1. Variable Manufacturing Overhead Costs

Total

Variable

Manuf.

Overhead

Costs

$17,000,000

$8,500,000

Graph for planning

and control and inventory

costing

purposes at $10

per machine-hour

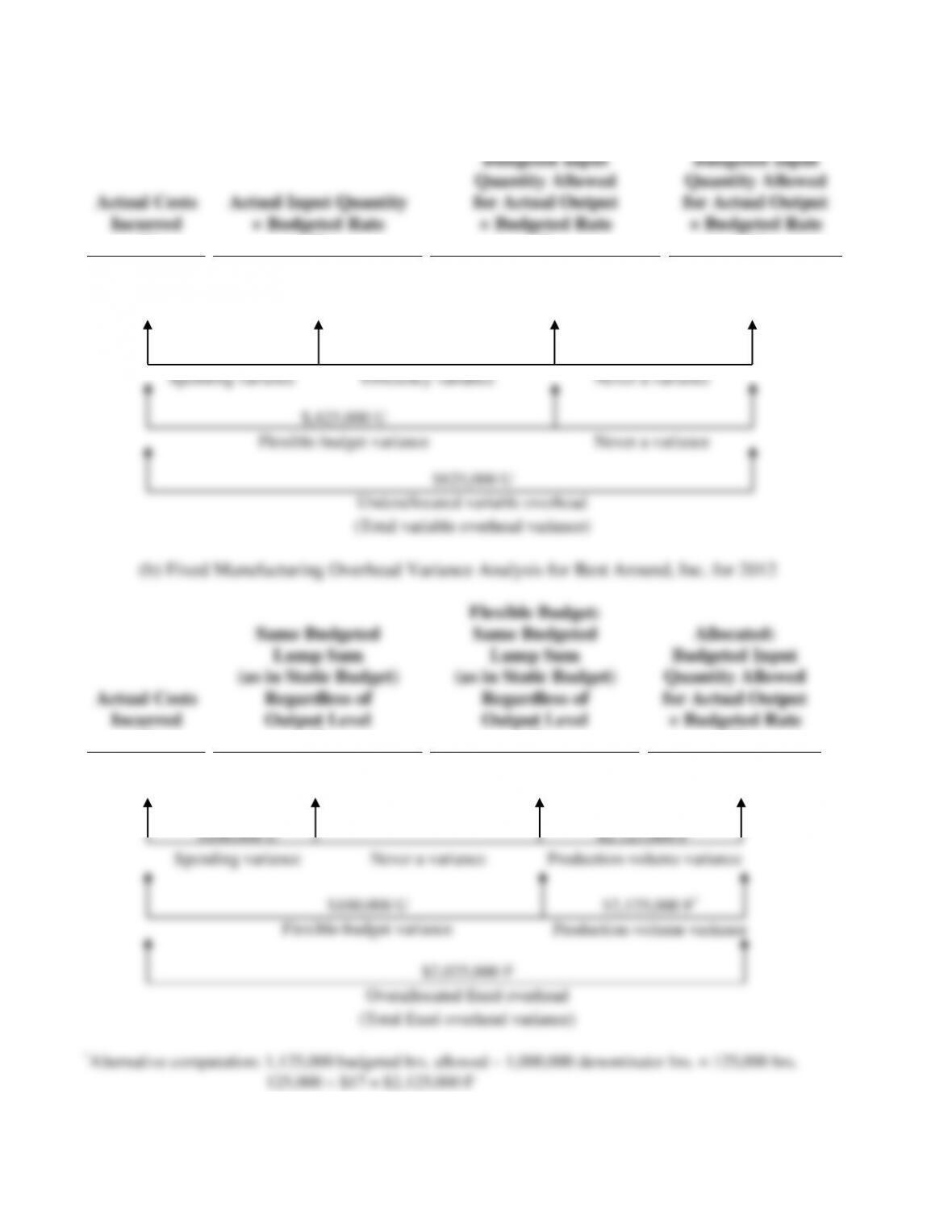

2. (a) Variable Manufacturing Overhead Variance Analysis for Best Around, Inc. for 2012

Actual Costs

Incurred

(1)

Actual Input Quantity

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(4)

$12,075,000

(1,150,000 $10)

$11,500,000

(1,125,000 $10)

$11,250,000

(1,125,000 $10)

$11,250,000

$575,000 U

$250,000 U

8-33

3. The underallocated variable manufacturing overhead was $825,000 and overallocated

fixed overhead was $2,025,000. The flexible-budget variance and underallocated overhead are

4. The choice of the denominator level will affect inventory costs. The new fixed

manufacturing overhead rate would be $17,000,000 ÷ 1,360,000 = $12.50 per machine-hour. In

turn, the allocated amount of fixed manufacturing overhead and the production-volume variance

would change as seen below:

Actual

Budget

Allocated

$17,100,000

$17,000,000

1,125,000 × $12.50 =

$14,062,500

$100,000 U $2,937,500 U*

Flexible-budget variance Prodn. volume variance

$3,037,500 U

Total fixed overhead variance

*Alternate computation: (1,360,000 – 1,125,000) × $12.50 = $2,937,500 U

The major point of this requirement is that inventory costs (and, hence, income determination)

can be heavily affected by the choice of the denominator level used for setting the fixed

manufacturing overhead rate.

8-34

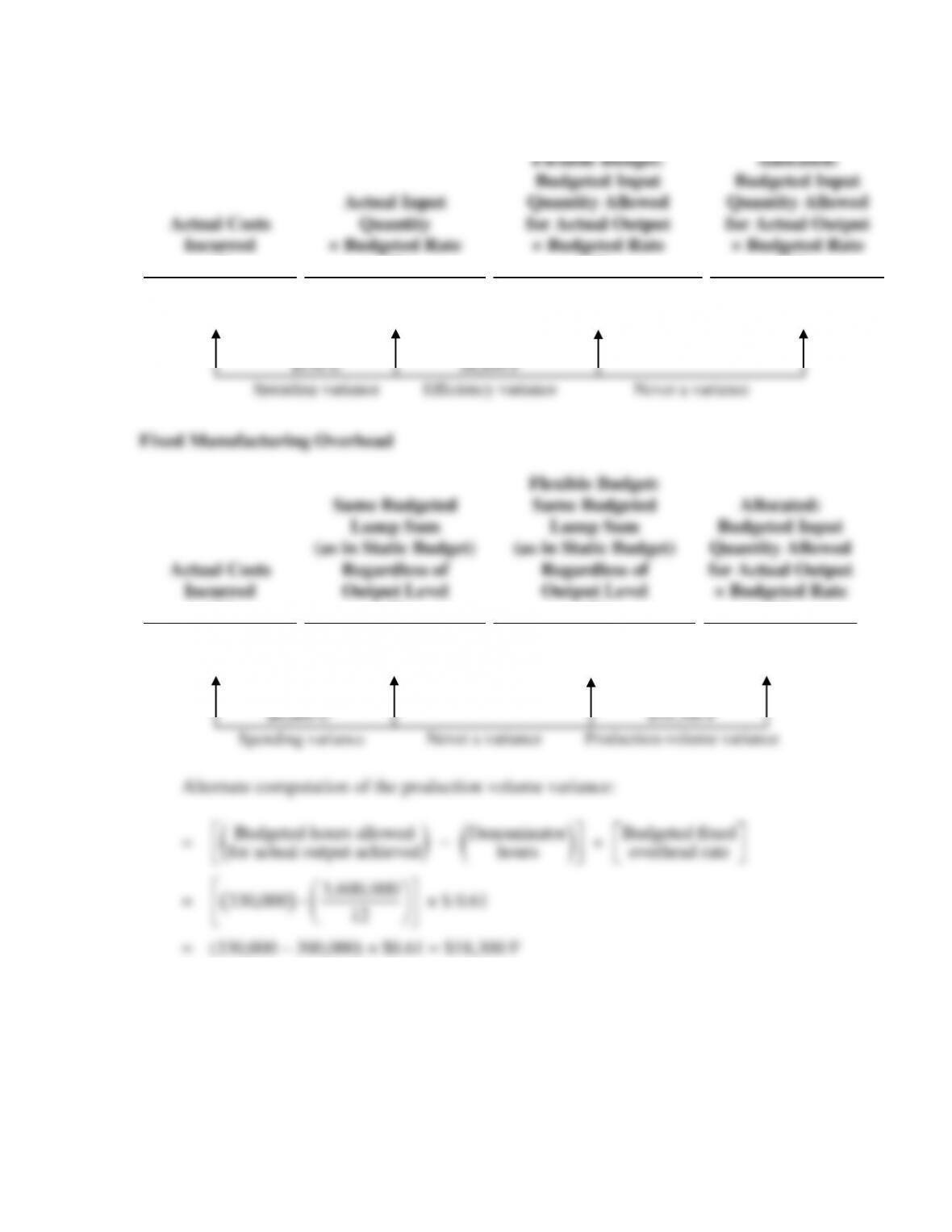

8-32 (30 min.) 4-variance analysis, find the unknowns.

Known figures denoted by an *

Case A:

Actual Costs

Incurred

Actual Input

Quantity

× Budgeted Rate

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

Allocated:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

Variable

Manufacturing

Overhead

$120,000*

(6,230 × $20)

$124,600

(6,200* × $20)

$124,000*

(6,200* × $20)

$124,000*

Fixed

Manufacturing

Overhead

$84,920*

(Lump sum)

$88,200*

(Lump sum)

$88,200*

(6,200* × $14a)

$86,800*

Total budgeted manufacturing overhead = $124,000 + $88,200 = $212,200

Case B:

Actual Costs

Incurred

Actual Input

Quantity

× Budgeted Rate

Flexible Budget:

Budgeted Input

Quantity

Allowed for

Actual Output

× Budgeted Rate

Allocated:

Budgeted Input

Quantity

Allowed for

Actual Output

× Budgeted Rate

Variable

Manufacturing

Overhead

$45,640

(1,141 $42.00*)

$47,922

(1,200 $42.00*)

$50,400b

(1,200 $42.00*)

$50,400

Never a variance

$600 U

Efficiency variance

$4,600* F

Spending variance

$1,400 U

Production-volume

variance

Never a variance

$3,280 F

Spending variance

Never a variance

$2,478 F*

Efficiency variance

$2,282 F*

Spending variance

8-35

Fixed

Manufacturing

Overhead

$23,180*

(Lump sum)

$20,000*

(Lump sum)

$20,000*

$24,000c

$4,000 F*

Production-volume

Never a variance

$3,180 U

Spending variance

8-33 (15−25 min.) Flexible budgets, 4-variance analysis.

1. Budgeted hours allowed

per unit of output = Budgeted DLH

Budgeted actual output

=

3,600,000

720,000

= 5 hours per unit

Budgeted DLH allowed for May output = 66,000 units 5 hrs./unit = 330,000 hrs.

Allocated total MOH = 330,000 Total MOH rate per hour

SOLUTION EXHIBIT 8-33

Variable Manufacturing Overhead

Actual Costs

Incurred

(1)

Actual Input

Quantity

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(4)

$186,000

(315,000 $0.59)

$185,850

(330,000 $0.59)

$194,700

(330,000 $0.59)

$194,700

$150 U

$8,850 F

8-38

8-34 (20 min.) Direct Manufacturing Labor and Variable Manufacturing

Overhead Variances

1. Direct Manufacturing Labor variance analysis for Sarah Beth’s Art Supply Company

Actual Costs

Incurred

Actual Input Quantity

Budgeted Rate

Flexible Budget:

Budgeted Input Quantity

Allowed for Actual Output

Budgeted Price

29,000 × 2.3 × 10.4

29,000 × 2.3 × 10

29,000 × 2 × 10.0

$693,680

$667,000

$580,000

$26,680 U $87,000 U

Price variance Efficiency variance

2. Variable Manufacturing Overhead variance analysis for Sarah Beth’s Art Supply Company

Actual Costs

Incurred

Actual Input Quantity

Budgeted Rate

Flexible Budget:

Budgeted Input Quantity

Allowed for Actual Output

Budgeted Rate

29,000 × 2.3 × 18.95

29,000 × 2.3 × 20.0

29,000 × 2 × 20.0

$1,263,965

$1,334,000

$1,160,000

$70,035 F $174,000 U

Spending variance Efficiency variance

3. The favorable spending variance for variable manufacturing overhead suggests that less costly

items were used, which could have a negative impact on labor efficiency. But note that the

4. If the variable overhead consisted only of costs that were related to direct manufacturing

labor, then Sarah is correct—both the labor efficiency variance and the variable overhead

8-39

8-35 (20 min.) Activity-based costing, batch-level variance analysis

1. Static budget number of crates = Budgeted pairs shipped / Budgeted pairs per crate

2. Flexible budget number of crates = Actual pairs shipped / Budgeted pairs per crate

3. Actual number of crates shipped = Actual pairs shipped / Actual pairs per box

4. Static budget number of hours = Static budget number of crates × budgeted hours per box

= 25,000 × 1.1 = 27,500 hours

5. Variable Direct Variance Analysis for Pointe’s Fleet Feet, Inc. for 2011

Actual Actual Hours Budgeted Hours Allowed for

6. Fixed Overhead Variance Analysis for Pointe’s Fleet Feet, Inc. for 2011

Actual Static Budget Budgeted Hours Allowed for

8-40

8-36 (30 min.) Activity-based costing, batch-level variance analysis

2. Flexible budget number of setups = Actual books produced / Budgeted books per setup

= 324,000 ÷ 500 = 648 setups

4. Static budget number of hours = Static budget # of setups × Budgeted hours per setup

5. Budgeted direct variable cost of a setup

= Budgeted variable cost per setup-hour × Budgeted number of setup-hours

= $40 × 8 = $320.

6. Direct Variable Variance Analysis for Jo Nathan Publishing Company for 2012

Actual Actual Hours Standard Hours