The change in operating income between 2010 and 2011 can be analyzed as follows:

Income

Statement

Amounts

in 2010

(1)

Revenue and

Cost Effects

of Growth

Component

in 2011

(2)

Revenue and

Cost Effects of

Price-Recovery

Component

in 2011

(3)

Cost Effect of

Productivity

Component

in 2011

(4)

Income

Statement

Amounts

in 2011

(5) =

(1) + (2) + (3) + (4)

Revenues

$3,000,000

$500,000 F

$140,000 U

−−

$3,360,000

Costs

2,160,000

300,000 U

114,000 U

$189,000 F

2,385,000

Operating income

$ 840,000

$200,000 F

$254,000 U

$189,000 F

$ 975,000

$135,000 F

Change in operating income

3. The analysis of operating income indicates that a significant amount of the increase in

operating income resulted from Westlake’s productivity improvements in 2011. The company

13-22

13-28 (25 min.) Analysis of growth, price-recovery, and productivity components

(continuation of 13-27).

Effect of industry-market-size factor on operating income

Of the 10-unit increase in sales from 60 to 70 units, 5% or 3 units (5% 60) are due to growth in

market size, and 7 (10 − 3) units are due to an increase in market share.

income.

13-23

13-29 (20 min.) Identifying and managing unused capacity (continuation of 13-26).

1. The amount and cost of unused capacity at the beginning of year 2011 based on work

done in year 2011 follows:

2. Westlake can reduce software implementation support capacity from 90 jobs to

75 (90 − 15) jobs. Westlake will save 15 $4,100 = $61,500. This is the maximum amount of

3. Westlake may have chosen not to downsize because it projects sales increases in the near

term that would lead to greater demand for and utilization of capacity. Westlake may have also

13-24

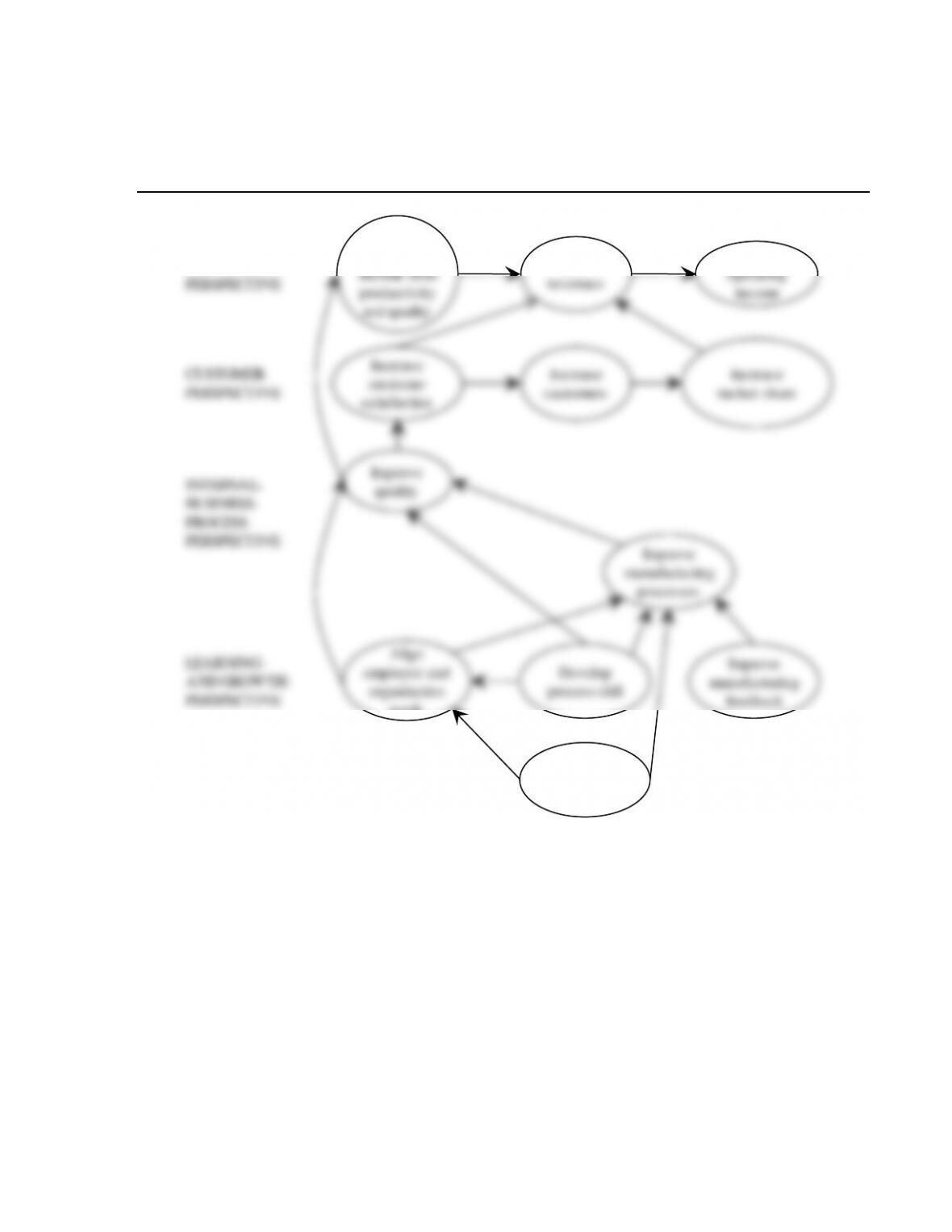

13-30 (30 min.) Balanced scorecard and strategy.

1. Solution Exhibit 13-30A shows the customer preference map for MP3 players for Music

Master Company and Vantage Manufacturing on price, storage capacity, and quality.

SOLUTION EXHIBIT 13-30A

13-25

3. Solution Exhibit 13-30B presents Music Master’s strategy map explaining cause-and-effect

relationships in its balanced scorecard.

SOLUTION EXHIBIT 13-30B

Strategy Map for Music Master Company

FINANCIAL

PERSPECTIVE

CUSTOMER

PERSPECTIVE

INTERNAL–

BUSINESS-

PROCESS

PERSPECTIVE

LEARNING-

AND GROWTH-

Increase

operating

income from

productivity

and quality

Grow

revenues

Improve

manufacturing

processes

Develop

Increase

market share

Grow

operating

income

Increase

customer

satisfaction

Increase

customers

Improve

quality

Align

employee and

Improve

4. In the internal-business-process perspective, Music Master needs to set targets for decreasing

the percentage of defective products sold and then identify measures that would be leading

indicators of achieving this goal. For example, in the learning and growth perspective, Music

Master may want to measure the percentage of employees trained in quality management and the

percentage of manufacturing processes with real-time feedback. The logic is that improvements

13-31 (25-30 min.) Strategic analysis of operating income (continuation of 13-30)

1. Operating income for each year is as follows:

2010 2011

Revenue ($45 8,000; $43 9,000) $360,000 $387,000

Costs

2. The Growth Component

Revenue effect

of growth

=

Actual units of Actual units of Selling

output sold output sold price

in 2011 in 2010 in 2010

−

13-28

The Price-Recovery Component

Revenue effect of

price-recovery

()

Actual units

Selling price Selling price

= of output

in 2011 in 2010 sold in 2011

−

variable costs

2011 2010

produce 2011

output in 2010

Cost effect of

price-recovery for

fixed costs

=

Price per Price per

unit of unit of

capacity capacity

in 2011 in 2010

−

×

Actual units of capacity in

2010 because adequate

capacity exists to produce

2011 output in 2010

The Productivity Component

Cost effect of

productivity for

variable costs

=

Actual units of Units of input

input used required to

to produce produce 2011

2011 output ouput in 2010

−

Input

price

in 2011

Cost effect of

Actual Actual units of capacity in

units of 2010 because adequate

Price per

unit of

Cost effect of

price-recovery for

The change in operating income between 2010 and 2011 can be analyzed as follows:

Income

Statement

Amounts

in 2010

(1)

Revenue and

Cost Effects

of Growth

Component

in 2011

(2)

Revenue and

Cost Effects of

Price-Recovery

Component

in 2011

(3)

Cost Effect

of

Productivity

Component

in 2011

(4)

Income

Statement

Amounts

in 2011

(5) =

(1) + (2) + (3) + (4)

Revenues

$360,000

$45,000 F

$18,000 U

−−

$387,000

Costs

313,000

14,000 U

4,500 U

$23,500 F

308,000

Operating income

$ 47,000

$31,000 F

$22,500 U

$23,500 F

$ 79,000

$32,000 F

Change in operating income

3. The analysis of operating income indicates that a significant amount of the increase in

operating income resulted from Music Master’s cost leadership strategy. The company was able

.

13-30

13-32 (20 min.) Analysis of growth, price-recovery, and productivity components

(continuation of 13-31)

Effect of the industry-market-size factor on operating income

Of the 1,000-unit increase in sales from 8,000 to 9,000 units, 3% or 240 (3% 8,000)

units are due to growth in market size, and 760 (1,000 − 240) units are due to an increase in