11-32 (20 min.) Opportunity costs.

1. The opportunity cost to Wild Boar of producing the 3,500 units of Orangebo is the

contribution margin lost on the 3,500 units of Rosebo that would have to be forgone, as

computed below:

Selling price

Variable costs per unit:

Direct materials

Direct manufacturing labor

Variable manufacturing overhead

Variable marketing costs

Contribution margin per unit

Contribution margin for 3,500 units ($14 3,500 units)

$ 26

$ 5

1

4

2 12

$ 14

$49,000

The opportunity cost is $49,000. Opportunity cost is the maximum contribution to

operating income that is forgone (rejected) by not using a limited resource in its next-best

alternative use.

2. Contribution margin from manufacturing 3,500 units of Orangebo and purchasing 3,500

units of Rosebo from Buckeye is $52,500, as follows:

Manufacture

Orangebo

Purchase

Rosebo

Total

Selling price

Variable costs per unit:

Purchase costs

Direct materials

Direct manufacturing labor

Variable manufacturing costs

Variable marketing overhead

Variable costs per unit

Contribution margin per unit

Contribution margin from selling 3,500 units

of Orangebo and 3,500 units of Rosebo

($9 3,500 units; $6 3,500 units)

$ 20

–

5

1

4

1

11

$ 9

$31,500

$ 26

18

2

20

$ 6

$21,000

$52,500

As calculated in requirement 1, Wild Boar’s contribution margin from continuing to

manufacture 3,500 units of Rosebo is $49,000. Accepting the Miami Company and Buckeye

offer will benefit Wild Boar by $3,500 ($52,500 – $49,000). Hence, Wild Boar should accept the

Miami Company and Buckeye Corporation’s offers.

11-22

11-33 (30–40 min.) Product mix, relevant costs.

1. R3 HP6

Selling price $100 $150

machine)regular (the resource dconstraine theofhour per margin on Contributi

1

0.5

Total contribution margin from selling

only R3 or only HP6

R3: $25 50,000; HP6: $30 50,000 $1,250,000 $1,500,000

Less Lease costs of high-precision machine

2. If capacity of the regular machines is increased by 15,000 machine-hours to 65,000

machine-hours (50,000 originally + 15,000 new), the net relevant benefit from producing R3 and

HP6 is as follows:

R3 HP6

Total contribution margin from selling only

11-23

Investing in the additional capacity increases Pendleton’s operating income by $250,000

($1,500,000 calculated in requirement 2 minus $1,250,000 calculated in requirement 1), so

3. R3 HP6 S3

Selling price $100 $150 $120

Variable manufacturing costs per unit 60 100 70

machine)regular (the resource dconstraine theofhour per margin on Contributi

1

5.0

1

The first step is to compare the operating profits that Pendleton could earn if it accepted

the Carter Corporation offer for 20,000 units with the operating profits Pendleton is

currently earning. S3 has the highest contribution margin per hour on the regular machine

and requires no additional investment such as leasing a high-precision machine. To

produce the 20,000 units of S3 requested by Carter Corporation, Pendleton would require

11-24

11-34 (35–40 min.) Dropping a product line, selling more units.

1. The incremental revenue losses and incremental savings in cost by discontinuing the

Tables product line follows:

Difference:

Incremental

(Loss in Revenues)

and Savings in Costs

from Dropping

Tables Line

Revenues

Direct materials and direct manufacturing labor

Depreciation on equipment

Marketing and distribution

General administration

Corporate office costs

Total costs

Operating income (loss)

$(500,000)

300,000

0

70,000

0

0

370,000

$(130,000)

Dropping the Tables product line results in revenue losses of $500,000 and cost savings

of $370,000. Hence, Grossman Corporation’s operating income will be $130,000 lower if it

drops the Tables line.

Note that, by dropping the Tables product line, Home Furnishings will save none of the

depreciation on equipment, general administration costs, and corporate office costs, but it will

save variable manufacturing costs and all marketing and distribution costs on the Tables product

line.

2. Grossman’s will generate incremental operating income of $128,000 from selling 4,000

additional tables and, hence, should try to increase table sales. The calculations follow:

Incremental Revenues

(Costs) and Operating Income

Revenues $500,000

3. Solution Exhibit 11-34, Column 1, presents the relevant loss of revenues and the relevant

savings in costs from closing the Northern Division. As the calculations show, Grossman’s

operating income would decrease by $140,000 if it shut down the Northern Division (loss in

4. Solution Exhibit 11-34, Column 2, presents the relevant revenues and relevant costs of

opening the Southern Division (a division whose revenues and costs are expected to be identical

to the revenues and costs of the Northern Division). Grossman should open the Southern

Division because it would increase operating income by $40,000 (increase in relevant revenues

of $1,500,000 and increase in relevant costs of $1,460,000). The relevant costs include direct

11-26

1. The variable costs required to manufacture 150,000 starter assemblies are

Direct materials $200,000

Direct manufacturing labor 150,000

Variable manufacturing overhead 100,000

Total variable costs $450,000

11-27

2. The information on the storage cost, which is avoidable if self-manufacture is

discontinued, is relevant; these storage charges represent current outlays that are avoidable if

self-manufacture is discontinued. Assume these $50,000 charges are represented as an

opportunity cost of the make alternative. The costs of internal manufacture that incorporate this

$50,000 opportunity cost are

11-28

11-36 (30 min.) Make versus buy, activity-based costing, opportunity costs.

1. Relevant costs under buy alternative:

Purchases, 40,000 $9.25 $370,000

Relevant costs under make alternative:

Direct materials $200,000

2. Relevant costs under the make alternative:

Relevant costs (as computed in requirement 1) $362,000

Relevant costs under the buy alternative:

3. In this requirement, the decision on making the rotisserie attachments is irrelevant to the

analysis because the rotisserie attachments increase operating income and they will be

made whether the burners are purchased or made.

11-29

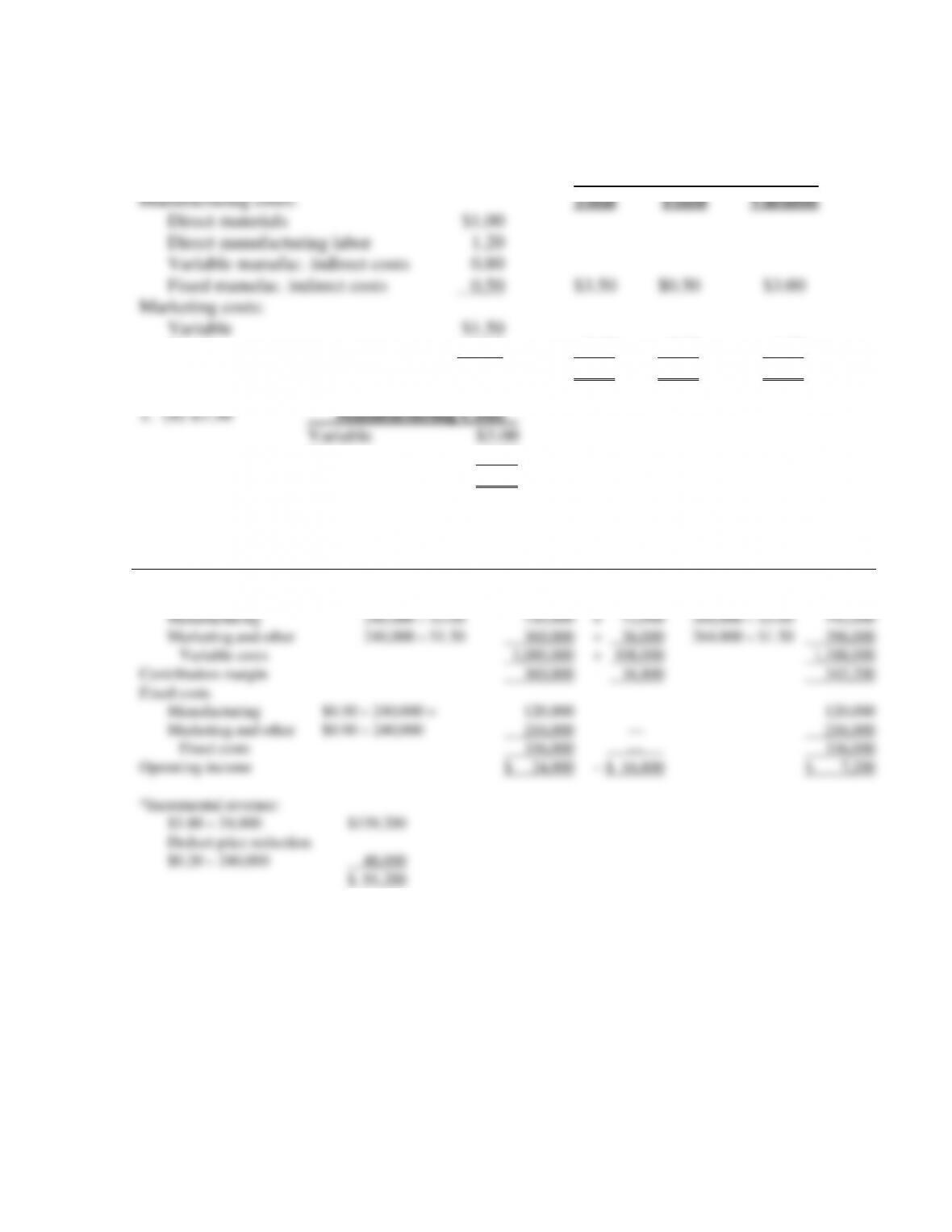

11-37 (60 min.) Multiple choice, comprehensive problem on relevant costs.

You may wish to assign only some of the parts.

Per Unit

Fixed 0.90 2.40 0.90 1.50

$5.90 $1.40 $4.50

Fixed 0.50

Total $3.50

2. (e) None of the above. Decrease in operating income is $16,800.

Old

Differential

New

Revenues 240,000 $6.00 $1,440,000 + $ 91,200* 264,000 $5.80 $1,531,200

Variable costs

11-30

3. (c) $3,500

If this order were not landed, fixed manufacturing overhead would be underallocated by

$2,500, $0.50 per unit 5,000 units. Therefore, taking the order increases operating income by

4. (a) $4,000 less ($7,500 – $3,500)

Alternative B: 5,000 units sold Alternative A: 5,000 units

under Government Contract sold to Regular Customers

5. (b) $4.15

Differential costs:

6. (e) $1.50, the variable marketing costs. The other costs are past costs and therefore, are

irrelevant.