1. This problem has two major purposes: (a) to give experience with data allocated on a total

overhead basis instead of on separate variable and fixed bases and (b) to reinforce distinctions

between actual hours of input, budgeted (standard) hours allowed for actual output, and

denominator level.

An analysis of direct manufacturing labor will provide the data for actual hours of input

Let D = denominator level in input units

Budgeted fixed

overhead rate

per input unit

= Budgeted fixed overhead costs

Denominator level in input units

8-23

1. In the columnar presentation of variable overhead variance analysis, all numbers shown in

bold are calculated from the given information, in the order (a) – (e).

VARIABLE MANUFACTURING OVERHEAD

Flexible Budget:

Budgeted Input

Actual Costs

Incurred

Actual Input Quantity

Budgeted Rate

Quantity Allowed Budgeted

for Actual Output

Rate

(b)

(a)

(c)

15,000

$6.00

14,850

$6.00

mach. hrs.

per mach. hr.

mach. hrs.

per mach. hr.

$89,625

$90,000

$89,100

$375 F $900 U (d)

Spending variance Efficiency variance

$525 U (e)

Flexible-budget variance

a. 15,000 machine-hours

$6 per machine-hour = $90,000

b. Actual VMOH = $90,000 – $375F (VOH spending variance) = $89,625

c. 14,850 machine-hours

$6 per machine-hour = $89,100

d. VOH efficiency variance = $90,000 – $89,100 = $900 U

e. VOH flexible budget variance = $900U – $375F = $525 U

Allocated variable overhead will be the same as the flexible budget variable overhead of

$89,100. The actual variable overhead cost is $89,625. Therefore, variable overhead is

underallocated by $525.

8-24

2. In the columnar presentation of fixed overhead variance analysis, all numbers shown in

bold are calculated from the given information, in the order (a) – (e).

FIXED MANUFACTURING OVERHEAD

Flexible Budget:

Allocated:

Actual Costs

Static Budget Lump Sum

Regardless of Output

Budgeted Input

Quantity Allowed

Budgeted

Incurred

Level

for Actual Output

Rate

(a)

(b)

14,850

$1.60* (c)

mach. hrs.

per mach. hr.

$30,375

$28,800

$23,760

$1,575 U $5,040 U (d)

Spending variance Production-volume variance

$1,575 U (e)

Flexible-budget variance

a. Actual FOH costs = $120,000 total overhead costs – $89,625 VOH costs = $30,375

b. Static budget FOH lump sum = $30,375 – $1,575 spending variance = $28,800

c. *FOH allocation rate = $28,800 FOH static-budget lump sum

18,000 static-budget machine-hours

= $1.60 per machine-hour

Allocated FOH = 14,850 machine-hours

$1.60 per machine-hour = $23,760

d. PVV = $28,800 – $23,760 = $5,040 U

e. FOH flexible budget variance = FOH spending variance = $1,575 U

Allocated fixed overhead is $23,760. The actual fixed overhead cost is $30,375. Therefore, fixed

overhead is underallocated by $6,615.

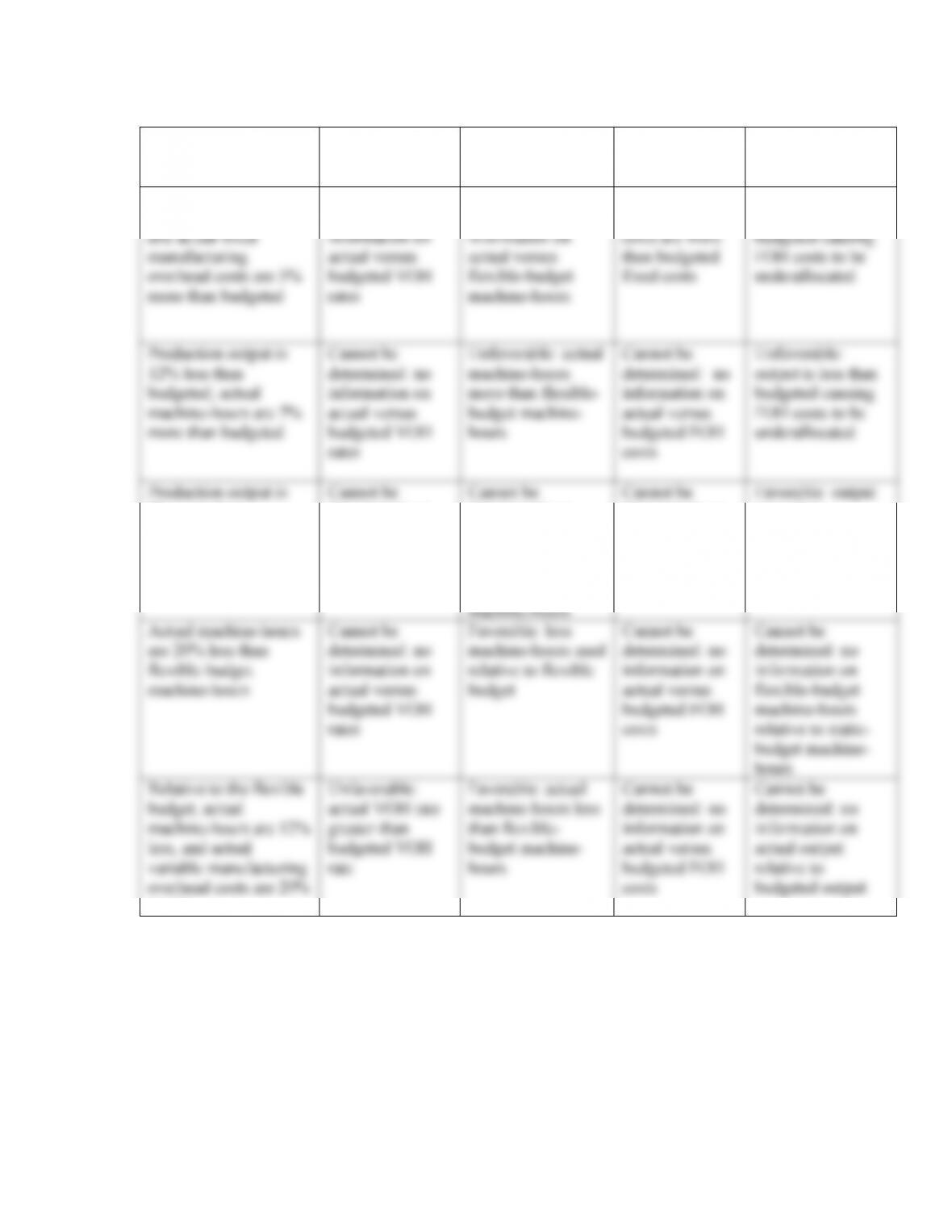

8-27 (15 min.) Identifying favorable and unfavorable variances.

Scenario

VOH

Spending

Variance

VOH

Efficiency

Variance

FOH

Spending

Variance

FOH

Production-

Volume Variance

Production output is

4% less than budgeted,

and actual fixed

manufacturing

overhead costs are 5%

more than budgeted

Cannot be

determined: no

information on

actual versus

budgeted VOH

rates

Cannot be

determined: no

information on

actual versus

flexible-budget

machine-hours

Unfavorable:

actual fixed

costs are more

than budgeted

fixed costs

Unfavorable:

output is less than

budgeted causing

FOH costs to be

underallocated

Production output is

12% less than

budgeted; actual

machine-hours are 7%

more than budgeted

Cannot be

determined: no

information on

actual versus

budgeted VOH

rates

Unfavorable: actual

machine-hours

more than flexible-

budget machine-

hours

Cannot be

determined: no

information on

actual versus

budgeted FOH

costs

Unfavorable:

output is less than

budgeted causing

FOH costs to be

underallocated

Production output is

9% more than

budgeted

Cannot be

determined: no

information on

actual versus

budgeted VOH

rates

Cannot be

determined: no

information on

actual machine-

hours versus

flexible-budget

machine-hours

Cannot be

determined: no

information on

actual versus

budgeted FOH

costs

Favorable: output

more than

budgeted will

cause FOH costs to

be overallocated

Actual machine-hours

are 20% less than

flexible-budget

machine-hours

Cannot be

determined: no

information on

actual versus

budgeted VOH

rates

Favorable: less

machine-hours used

relative to flexible

budget

Cannot be

determined: no

information on

actual versus

budgeted FOH

costs

Cannot be

determined: no

information on

flexible-budget

machine-hours

relative to static-

budget machine-

hours

Relative to the flexible

budget, actual

machine-hours are 12%

less, and actual

variable manufacturing

overhead costs are 20%

greater

Unfavorable:

actual VOH rate

greater than

budgeted VOH

rate

Favorable: actual

machine-hours less

than flexible-

budget machine-

hours

Cannot be

determined: no

information on

actual versus

budgeted FOH

costs

Cannot be

determined: no

information on

actual output

relative to

budgeted output

8-26

1. Solution Exhibit 8-28 contains a columnar presentation of the variances for Doorknob Design

Company (DDC) for April 2012.

SOLUTION EXHIBIT 8-28

Actual Costs

Incurred:

Actual Input Quantity

Actual Input Quantity

Budgeted Price

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Actual Rate

Purchases

Usage

× Budgeted Price

Direct

Materials

(12,000 $11)

$132,000

(12,000 $10)

$120,000

(10,450 $10)

$104,500

(10,500 $10)

$105,000

$12,000 U $500 F

a. Price variance b. Efficiency variance

Direct

Manufacturing

Labor

$808,500

(38,500 $20)

$770,000

(42,000 $20)

$840,000

$38,500 U $70,000 F

c. Price variance d. Efficiency variance

Actual Costs

Incurred

Actual Input Quantity

Budgeted Rate

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

Budgeted Rate

Allocated:

(Budgeted Input

Quantity Allowed

for Actual Output

Budgeted Rate)

Variable

Manufacturing

Overhead

$64,150

(10,450 $6)

$62,700

(10,500 $6)

$63,000

(10,500 $6)

$63,000

$1,450U $300 F

e. Spending variance f. Efficiency variance Never a variance

Fixed

Manufacturing

Overhead

$152,000

$150,000*

$150,000

(10,500 $15)

$157,500

$2,000 U $7,500 F

h. Spending variance Never a variance g. Production volume variance

*Denominator level (Annual) in pounds of material: 400,000 .3 = 120,000 pounds

Annual Budgeted Fixed Overhead: 120,000 $15/lb = $1,800,000

Monthly budgeted FOH: $1,800,000 / 12 = $150,000

8-27

2. The direct materials price variance indicates that DDC paid more for brass than they had

planned. If this is because they purchased a higher quality of brass, it may explain why they

used less brass than expected (leading to a favorable material efficiency variance). In turn, since

8-28

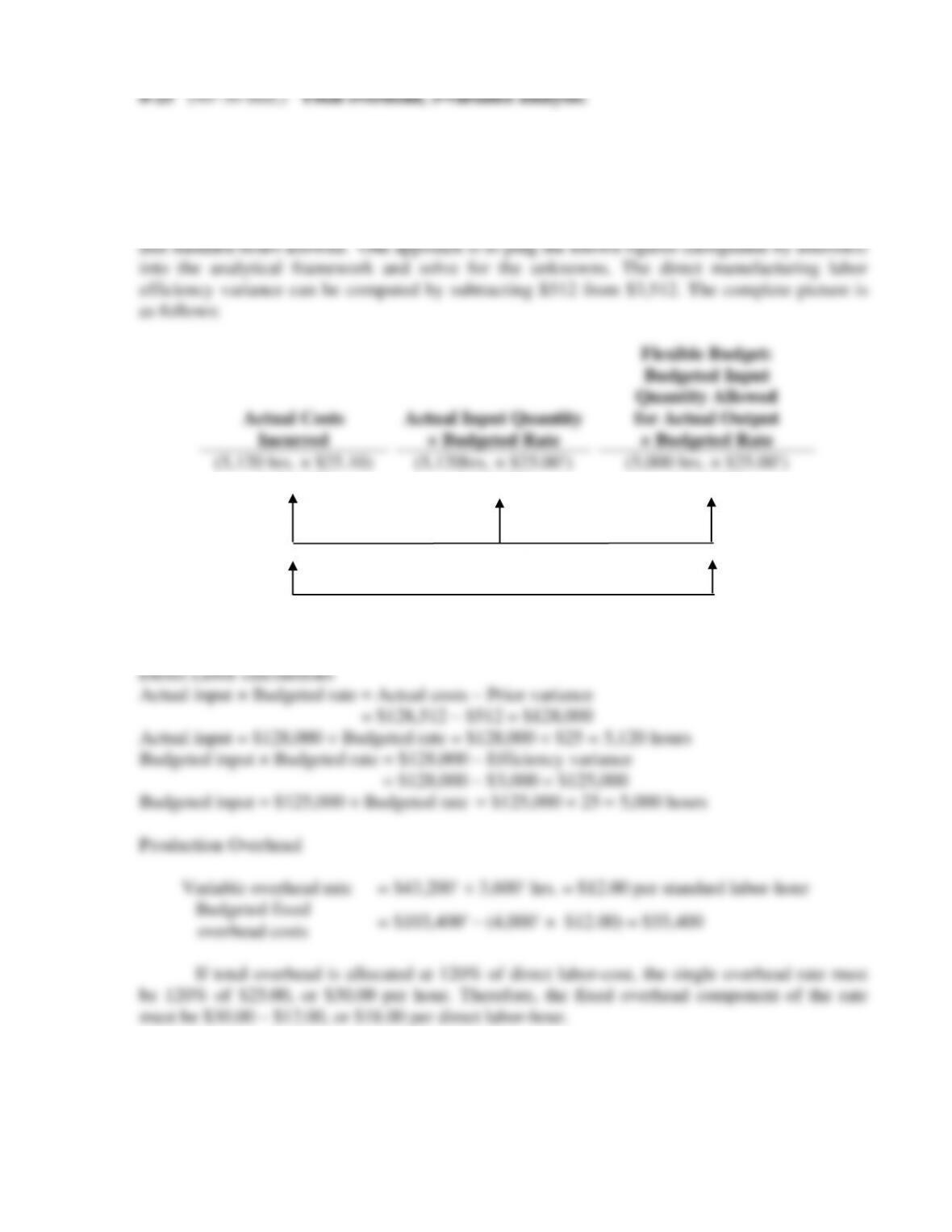

8-29 (30 min.) Comprehensive variance analysis.

1. Budgeted number of machine-hours planned can be calculated by multiplying the number

2. Budgeted fixed MOH costs per machine-hour can be computed by dividing the flexible

3. Budgeted variable MOH costs per machine-hour are calculated as budgeted variable

4. Budgeted number of machine-hours allowed for actual output achieved can be calculated

5. The actual number of output units is the budgeted number of machine-hours allowed for

6. The actual number of machine-hours used per output unit is the actual number of

8-29

8-30 (60 min.) Journal entries (continuation of 8-29).

Actual

Results

Flexible-Budget

Amount

Static-Budget

Amount

1. Output units (food processors)

960

960

888

2. Machine-hours

1,824

1,920

1,776

3. Machine-hours per output unit

1.90

2.00

2.00

4. Variable MOH costs

$ 76,608

$ 76,800

$ 71,040

5. Variable MOH costs per machine-

hour (Row 4 ÷ Row 2)

$ 42.00

$ 40.00

$ 40.00

6. Variable MOH costs per unit

(Row 4 ÷ Row 1)

$ 79.80

$ 80.00

$ 80.00

7. Fixed MOH costs

$350,208

$348,096

$348,096

8. Fixed MOH costs per machine-

hour (Row 7 ÷ Row 2)

$ 192.00

$ 181.30

$ 196.00

9. Fixed MOH costs per unit (7 ÷ 1)

$ 364.80

$ 362.60

$ 392.00

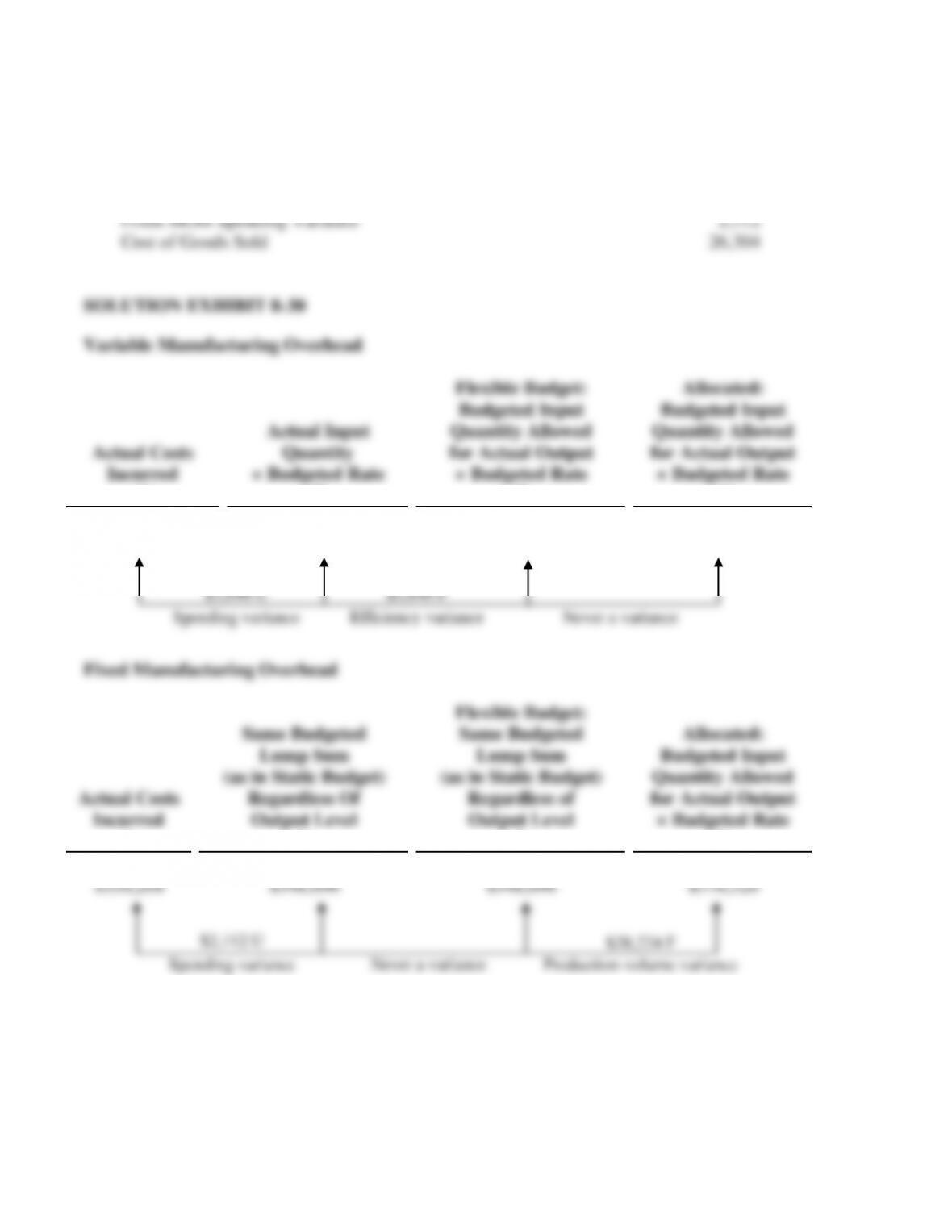

Solution Exhibit 8-30 shows the computation of the variances.

Journal entries for variable MOH, year ended December 31, 2012:

Variable MOH Control

76,608

Accounts Payable Control and Other Accounts

76,608

Work-in-Process Control

76,800

Variable MOH Allocated

76,800

Variable MOH Allocated

76,800

Variable MOH Spending Variance

3,648

Variable MOH Control

76,608

Variable MOH Efficiency Variance

3,840

Journal entries for fixed MOH, year ended December 31, 2012:

Fixed MOH Control

350,208

Wages Payable, Accumulated Depreciation, etc.

350,208

Work-in-Process Control

376,320

Fixed MOH Allocated

376,320

Fixed MOH Allocated

376,320

Fixed MOH Spending Variance

2,112

Fixed MOH Control

350,208

Fixed MOH Production-Volume Variance

28,224

2. Adjustment of COGS

Variable MOH Efficiency Variance

3,840

Fixed MOH Production-Volume Variance

28,224

Variable MOH Spending Variance

3,648

Fixed MOH Spending Variance

2,112

Cost of Goods Sold

26,304

SOLUTION EXHIBIT 8-30

Variable Manufacturing Overhead

Actual Costs

Incurred

(1)

Actual Input

Quantity

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Rate

(4)

(1,824 $42)

$76,608

(1,824 $40)

$72,960

(1,920 $40)

$76,800

(1,920 $40)

$76,800

Allocated:

Budgeted Input

(1,920 × $196)

$3,648 U

$3,840 F