17-1

CHAPTER 17

PROCESS COSTING

17-1 Industries using process costing in their manufacturing area include chemical processing,

17-2 Process costing systems separate costs into cost categories according to the timing of

when costs are introduced into the process. Often, only two cost classifications, direct materials

17-3 Equivalent units is a derived amount of output units that takes the quantity of each input

(factor of production) in units completed or in incomplete units in work in process, and converts

17-4 The accuracy of the estimates of completion depends on the care and skill of the

17-5 The five key steps in process costing follow:

Step 1: Summarize the flow of physical units of output.

17-6 Three inventory methods associated with process costing are:

17-7 The weighted-average process-costing method calculates the equivalent-unit cost of all

17-2

17-8 FIFO computations are distinctive because they assign the cost of the previous

accounting period’s equivalent units in beginning work–in-process inventory to the first units

17-9 FIFO should be called a modified or departmental FIFO method because the goods

17-10 A major advantage of FIFO is that managers can judge the performance in the current

period independently from the performance in the preceding period.

17-11 The journal entries in process costing are basically similar to those made in job-costing

17-12 Standard-cost procedures are particularly appropriate to process-costing systems where

there are various combinations of materials and operations used to make a wide variety of similar

17-13 There are two reasons why the accountant should distinguish between transferred-in

costs and additional direct materials costs for a particular department:

17-14 No. Transferred-in costs or previous department costs are costs incurred in a previous

period.

17-15 Materials are only one cost item. Other items (often included in a conversion costs pool)

include labor, energy, and maintenance. If the costs of these items vary over time, this variability

17-3

17-16 (25 min.) Equivalent units, zero beginning inventory.

1. Direct materials cost per unit ($750,000 ÷ 10,000) $ 75.00

Conversion cost per unit ($798,000 ÷ 10,000) 79.80

Assembly Department cost per unit $154.80

3. The difference in the Assembly Department cost per unit calculated in requirements 1 and

2 arises because the costs incurred in January and February are the same but fewer equivalent

units of work are done in February relative to January. In January, all 10,000 units introduced are

fully completed resulting in 10,000 equivalent units of work done with respect to direct materials

and conversion costs. In February, of the 10,000 units introduced, 10,000 equivalent units of

17-4

SOLUTION EXHIBIT 17-16B

Compute Cost per Equivalent Unit,

Assembly Department of Nihon, Inc. for February 2012.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Costs added during February

$1,548,000

$750,000

$798,000

Divide by equivalent units of work done

in current period (Solution Exhibit 17-l6A)

10,000

9,500

Cost per equivalent unit

$ 75

$ 84

1. Work in Process––Assembly 750,000

Accounts Payable 750,000

2. Work in Process––Assembly 798,000

Various accounts 798,000

3. Work in Process––Testing 1,431,000

Work in Process––Assembly 1,431,000

To record 9,000 units completed and

1. Direct materials 750,000 Work in Process––Testing 1,431,000

17-5

1. Solution Exhibit 17-18A shows equivalent units of work done in the current period of

Chemical P, 50,000; Chemical Q, 35,000; Conversion costs, 45,000.

2. Solution Exhibit 17-18B summarizes the total Mixing Department costs for July 2012,

calculates cost per equivalent unit of work done in the current period for Chemical P, Chemical

Q, and Conversion costs, and assigns these costs to units completed (and transferred out) and to

units in ending work in process.

SOLUTION EXHIBIT 17-18A

17-6

SOLUTION EXHIBIT 17-18B

Steps 3, 4, and 5: Summarize Total Costs to Account For, Compute Cost per Equivalent Unit,

and Assign Total Costs to Units Completed and to Units in Ending Work in Process;

Mixing Department of Roary Chemicals for July 2012.

Total

Production

Costs

Chemical P

Chemical Q

Conversion

Costs

(Step 3) Costs added during July

$455,000

$250,000

$70,000

$135,000

Total costs to account for

$455,000

$250,000

$70,000

$135,000

(Step 4) Costs added in current period

$250,000

$70,000

$135,000

Divide by equivalent units of work

done in current period

(Solution Exhibit 17-l8A)

50,000

35,000

45,000

Cost per equivalent unit

$ 5

$ 2

$ 3

(Step 5) Assignment of costs:

Completed and transferred out

(35,000 units)

$350,000

(35,000* $5) + (35,000* $2) + (35,000* $3)

Work in process, ending

(15,000 units)

105,000

(15,000† $5) + (0† $2) + (10,000† $3)

Total costs accounted for

$455,000

$250,000 + $70,000 + $135,000

*Equivalent units completed and transferred out from Solution Exhibit 17-18A, Step 2.

†Equivalent units in ending work in process from Solution Exhibit 17-18A, Step 2.

17-19 (15 min.) Weighted-average method, equivalent units.

Under the weighted-average method, equivalent units are calculated as the equivalent units of

May 2012.

(Step 2)

(Step 1) Equivalent Units

Physical Direct Conversion

17-7

17-20 (20 min.) Weighted-average method, assigning costs (continuation of 17-19).

Solution Exhibit 17-20 summarizes total costs to account for, calculates cost per equivalent unit

May 2012.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given)

$ 584,400

$ 493,360

$ 91,040

Costs added in current period (given)

4,612,000

3,220,000

1,392,000

Total costs to account for

$5,196,400

$3,713,360

$1,483,040

(Step 4) Costs incurred to date

$3,713,360

$1,483,040

Divide by equivalent units of work done to date

(Solution Exhibit 17-19)

532

496

Cost per equivalent unit of work done to date

$ 6,980

$ 2,990

(Step 5) Assignment of costs:

Completed and transferred out (460 units)

$4,586,200

(460* $6,980) + (460* $2,990)

Work in process, ending (120 units)

610,200

(72† $6,980) + (36† $2,990)

Total costs accounted for

$5,196,400

$3,713,360 + $1,483,040

*Equivalent units completed and transferred out from Solution Exhibit 17-19, Step 2.

† Equivalent units in work in process, ending from Solution Exhibit 17-19, Step 2.

17-8

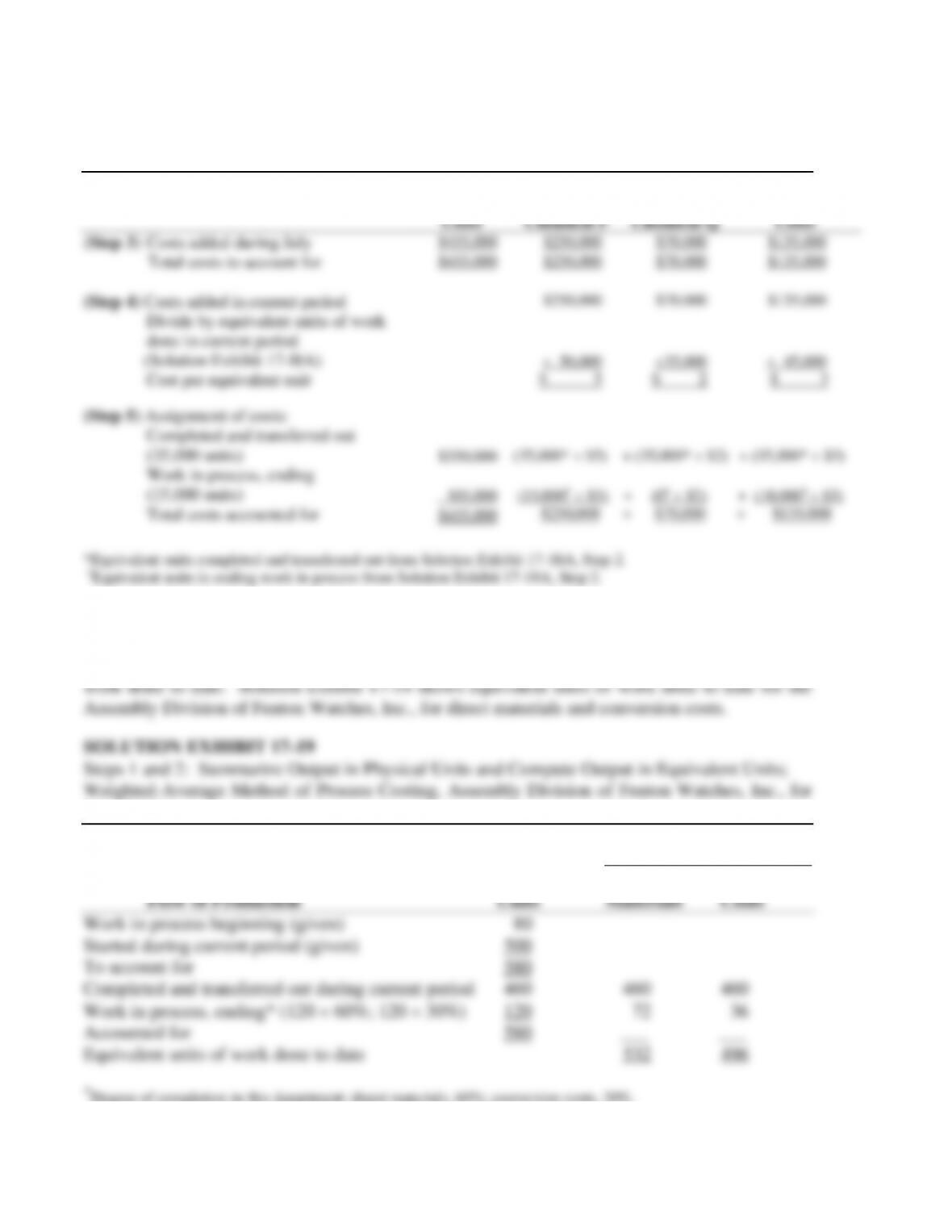

17-21 (15 min.) FIFO method, equivalent units.

Under the FIFO method, equivalent units are calculated as the equivalent units of work done in

the current period only. Solution Exhibit 17-21 shows equivalent units of work done in May

2012 in the Assembly Division of Fenton Watches, Inc., for direct materials and conversion

costs.

SOLUTION EXHIBIT 17-21

17-22 (20 min.) FIFO method, assigning costs (continuation of 17-21).

Solution Exhibit 17-22 summarizes total costs to account for, calculates cost per equivalent unit

of work done in May 2012 in the Assembly Division of Fenton Watches, Inc., and assigns total

costs to units completed and to units in ending work-in–process inventory.

SOLUTION EXHIBIT 17-22

17-10

1. To obtain the conversion-cost rates, divide the budgeted cost of each operation by the number

of packages that are expected to go through that operation.

Budgeted

Conversion

Cost

Budgeted

number of

packages

Conversion

Cost per

Package

Mixing

$ 9,040

11,300

$0.80

Shaping

1,625

6,500

0.25

Cutting

720

4,800

0.15

Baking

7,345

11,300

0.65

Slicing

650

6,500

0.10

Packaging

8,475

11,300

0.75

2.

Work Order

Work Order

#215

#216

Bread type:

Dinner Roll

Multigrain Loaves

Quantity:

1,200

1,400

Direct Materials

$ 660

$1,260

Mixing

960

1,120

Shaping

0

350

Cutting

180

0

Baking

780

910

Slicing

0

140

Packaging

900

1,050

Total

$3,480

$4,830

The direct materials costs per unit vary based on the type of bread ($2,640 ÷ 4,800 = $0.55 for

the dinner rolls, and $5,850 ÷ 6,500 = $0.90 for the multi-grain loaves). Conversion costs are

charged using the rates computed in part (1), taking into account the specific operations that each

type of bread actually goes through.

3. Work order #215 (Dinner rolls): Work order #216 (Mulit-grain loaves):

Total cost $3,480 Total cost: $4,830