4-11

1.

Quarter

1

2

3

4

Annual

(1) Pools sold

700

500

150

150

1,500

(2) Direct manufacturing

labor hours (0.5 Row 1)

350

250

75

75

750

(3) Fixed manufacturing

overhead costs

$10,500

$10,500

$10,500

$10,500

$42,000

(4) Budgeted fixed

manufacturing overhead

rate per direct

manufacturing labor hour

($10,500 Row 2)

$30

$42

$140

$140

$56

Budgeted Costs Based on

Quarterly Manufacturing

Overhead Rate

2nd Quarter

3rd Quarter

Direct material costs ($7.50 500 pools; 150 pools)

$ 3,750

$ 1,125

Direct manufacturing labor costs

($16 250 hours; 75 hours)

4,000

1,200

Variable manufacturing overhead costs

($12 250 hours; 75 hours)

3,000

900

Fixed manufacturing overhead costs

($42 250 hours; $140 × 75 hours)

10,500

10,500

Total manufacturing costs

$21,250

$13,725

Divided by pools manufactured each quarter

÷ 500

÷ 150

Manufacturing cost per pool

$ 42.50

$ 91.50

2.

Budgeted Costs Based on

Annual Manufacturing

Overhead Rate

2nd Quarter

3rd Quarter

Direct material costs ($7.50 500 pools; 150 pools)

$ 3,750

$1,125

Direct manufacturing labor costs

($16 250 hours; 75 hours)

4,000

1,200

Variable manufacturing overhead costs

($12 250 hours; 75 hours)

3,000

900

Fixed manufacturing overhead costs

($56 250 hours; 75 hours)

14,000

4,200

Total manufacturing costs

$24,750

$7,425

Divided by pools manufactured each quarter

500

150

Manufacturing cost per pool

$ 49.50

$49.50

4-12

3.

2nd Quarter

3rd Quarter

Prices based on quarterly budgeted manufacturing

overhead rates calculated in requirement 1

($42.50 130%; $91.50 130%)

$55.25

$118.95

Price based on annual budgeted manufacturing overhead

rates calculated in requirement 2

($49.50 130%; $49.50 130%)

$64.35

$64.35

Splash should use the budgeted annual manufacturing overhead rate because capacity decisions

4-13

4-23 (10–15 min.) Accounting for manufacturing overhead.

1. Budgeted manufacturing overhead rate =

$7,500,000

250,000 machine–hours

2. Work-in–Process Control 7,350,000

3. $7,350,000– $7,300,000 = $50,000 overallocated,

an insignificant amount of actual manufacturing overhead

4-14

4-24 (35−45 min.) Job costing, journal entries.

1. An overview of the product costing system is:

COST

DIRECT

COST

Manufacturing Overhead

Direct

Materials

INDIRECT

COST

POOL

Direct

Manuf

.

Labor

Direct Costs

4-15

2. & 3.

2.

(1) Materials Control

Accounts Payable Control

800

800

(2) Work-in-Process Control

Materials Control

710

710

(3) Manufacturing Overhead Control

Materials Control

100

100

(4) Work-in-Process Control

Manufacturing Overhead Control

Wages Payable Control

1,300

900

2,200

(5) Manufacturing Overhead Control

Accumulated Depreciation––buildings and

manufacturing equipment

400

400

(6) Manufacturing Overhead Control

Miscellaneous accounts

550

550

(7) Work-in-Process Control

Manufacturing Overhead Allocated

(1.60 $1,300 = $2,080)

2,080

2,080

(8) Finished Goods Control

Work-in-Process Control

4,120

4,120

(9) Accounts Receivable Control (or Cash)

Revenues

8,000

8,000

(10) Cost of Goods Sold

Finished Goods Control

4,020

4,020

(11) Manufacturing Overhead Allocated

Manufacturing Overhead Control

Cost of Goods Sold

2,080

1,950

130

3.

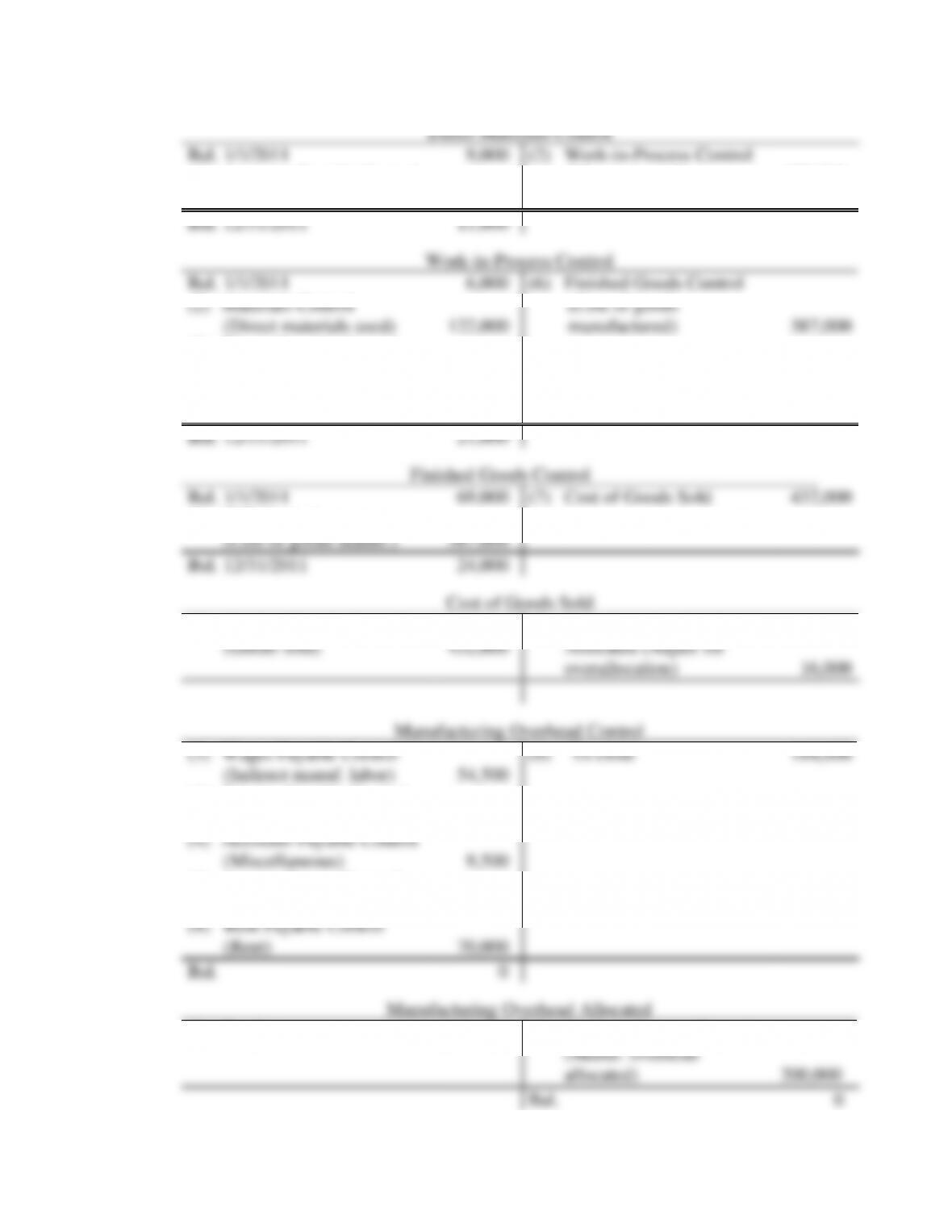

Materials Control

Bal. 1/1/2011

(1) Accounts Payable

Control (Purchases)

100

800

(2) Work-in-Process Control

(Materials used)

(3) Manufacturing Overhead

Control (Materials used)

710

100

Bal. 12/31/2011

90

Work-in-Process Control

Bal. 1/1/2011

(2) Materials Control

(Direct materials)

(4) Wages Payable

Control (Direct

manuf. labor)

(7) Manuf. Overhead

Allocated

60

710

1,300

2,080

(8) Finished Goods Control

(Goods completed)

4,120

Bal. 12/31/2011

30

Finished Goods Control

Bal. 1/1/2011

(8) WIP Control

(Goods completed)

500

4,120

(10) Cost of Goods Sold

4,020

Bal. 12/31/2011

600

Cost of Goods Sold

(10) Finished Goods

Control (Goods sold)

4,020

(11) Manufacturing Overhead

Allocated (Adjust for

overallocation)

130

Bal. 12/31/2011

3,890

Manufacturing Overhead Control

(3) Materials Control

(Indirect materials)

(4) Wages Payable Control

(Indirect manuf. labor)

(5) Accum. Deprn. Control

(Depreciation)

(6) Accounts Payable Control

(Miscellaneous)

100

900

400

550

(11) To close

1,950

Bal.

0

Manufacturing Overhead Allocated

(11) To close

2,080

(7) Work-in-Process Control

(Manuf. overhead allocated)

2,080

Bal.

0

4-17

1. i. Direct Materials Control 124,000

Accounts Payable Control 124,000

Source Document: Purchase Invoice, Receiving Report

Subsidiary Ledger: Direct Materials Record, Accounts Payable

ii. Work in Process Control a 122,000

Salaries Payable Control 20,000

Accounts Payable Control 9,500

Accumulated Depreciation Control 30,000

Rent Payable Control 70,000

Source Document: Depreciation Schedule, Rent Schedule, Maintenance wages due, Invoices

Subsidiary Ledger: Work-in-Process Inventory Records by Jobs, Finished Goods Inventory

Records by Jobs

vii. Cost of Goods Sold c 432,000

Finished Goods Control 432,000

Source Document: Sales Invoice, Completed Job Cost Record

4-18

viii. Manufacturing Overhead Allocated 200,000

Manufacturing Overhead Control

($129,500 + $54,500) 184,000

Cost of Goods Sold 16,000

Source Document: Prior Journal Entries

2. T-accounts

Direct Materials Control

Bal. 1/1/2011

(1) Accounts Payable Control

(Purchases)

9,000

124,000

(2) Work-in-Process Control

(Materials used)

122,000

Bal. 12/31/2011

11,000

Work-in–Process Control

Bal. 1/1/2011

(2) Materials Control

(Direct materials used)

(3) Wages Payable Control

(Direct manuf. labor)

(5) Manuf. Overhead

Allocated

6,000

122,000

80,000

200,000

(6) Finished Goods Control

(Cost of goods

manufactured)

387,000

Bal. 12/31/2011

21,000

Finished Goods Control

Bal. 1/1/2011

(6) WIP Control

(Cost of goods manuf.)

69,000

387,000

(7) Cost of Goods Sold

432,000

Bal. 12/31/2011

24,000

Cost of Goods Sold

(7) Finished Goods Control

(Goods sold)

432,000

(8) Manufacturing Overhead

Allocated (Adjust for

overallocation)

16,000

Manufacturing Overhead Control

(3) Wages Payable Control

(Indirect manuf. labor)

(4) Salaries Payable Control

(Maintenance)

(4) Accounts Payable Control

(Miscellaneous)

(4) Accum. Deprn. Control

(Depreciation)

(4) Rent Payable Control

(Rent)

54,500

20,000

9,500

30,000

70,000

(8) To close

184,000

Bal.

0

Manufacturing Overhead Allocated

(8) To close

200,000

(5) Work-in–Process Control

(Manuf. overhead

allocated)

200,000

4-26 (45 min.) Job costing, journal entries.

1. An overview of the product-costing system is

(1) Materials Control

Accounts Payable Control

150

150

(2) Work-in–Process Control

Materials Control

145

145

(3) Manufacturing Department Overhead Control

Materials Control

10

10

(4) Work-in–Process Control

Wages Payable Control

90

90

(5) Manufacturing Department Overhead Control

Wages Payable Control

30

30

(6) Manufacturing Department Overhead Control

Accumulated Depreciation

19

19

(7) Manufacturing Department Overhead Control

Various liabilities

9

9

(8) Work-in–Process Control

Manufacturing Overhead Allocated

63

63

(9) Finished Goods Control

Work-in–Process Control

294

294

(10a) Cost of Goods Sold

Finished Goods Control

292

292

(10b) Accounts Receivable Control (or Cash )

400

Manufacturing

Overhead

Machine-Hours

Indirect Costs

Direct Costs

Direct

Materials Direct

Manuf. Labor

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

COST OBJECT

PRODUCT

DIRECT

COSTS

Revenues

400