4-39

1. Adjusting entry for 12/31 payroll.

(a) Work-in–Process Control 3,850

Manufacturing Department Overhead Control 950

problem.

2. a-e An effective approach to this problem is to draw T-accounts and insert all the known

figures. Then, working with T-account relationships, solve for the unknown figures. Entries (a)

and (b) are posted into the T-accounts that follow.

Materials Control

Beginning balance 12/1

Purchases

1,200

65,400

59,000a

Materials requisitioned

Balance 12/30

7,600

a $1,200 + $65,400 – $7,600 = $59,000

(a) Direct materials requisitioned into work in process during December equals $59,000

because no materials are requisitioned on December 31.

Work-in–Process Control

Beginning balance 12/1

Direct materials $59,000

Direct manf. labor 76,500b

Manf. overhead

allocated 91,800b

5,800

227,300

225,000

Cost of goods manufactured

Balance 12/30

8,100

(a) Direct manuf. labor 12/31 payroll

3,850

(b) Manuf. overhead allocated 12/31

4,620c

Ending balance 12/31

16,570

b Direct manufacturing labor and manufacturing overhead allocated are unknown. Let x = Direct

manufacturing labor up to 12/30 payroll, then manufacturing overhead allocated up to 12/30

payroll = 1.20x

Use the T-account equation and solve for x:

$5,800 + $59,000 + x + 1.20x – $225,000 = $8,100

2.20x = $8,100 – $5,800 – $59,000 + $225,000 = $168,300

$168,300 $76,500

Total direct manufacturing labor for December = $80,350

Total manufacturing overhead allocated in December = 1.20 $80,350 = $96,420

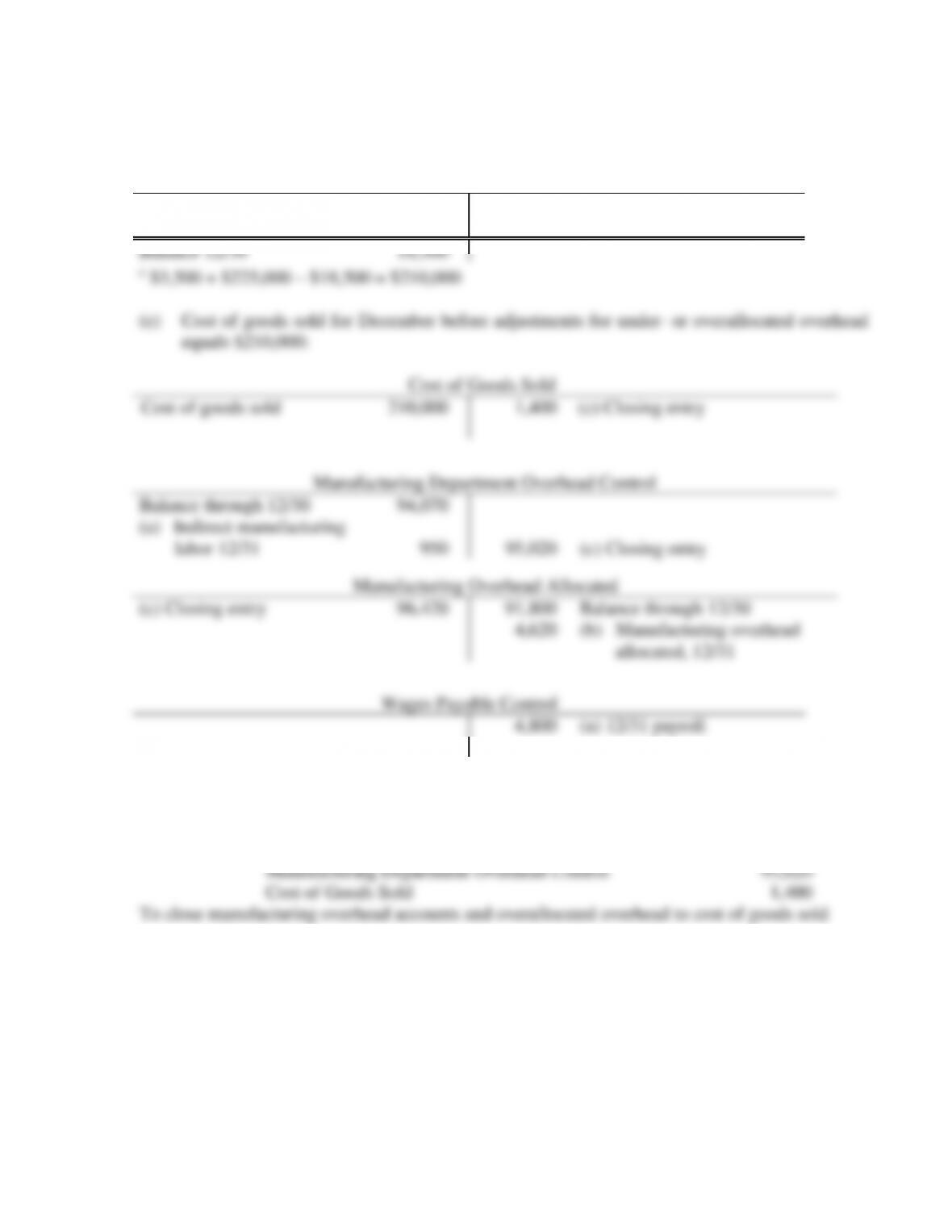

Finished Goods Control

Beginning balance 12/1

Cost of goods manufactured

3,500

225,000

210,000c

Cost of goods sold

Balance 12/30

18,500

(c) Closing entry

(c) Closing entry

1. Budgeted overhead rate = Budgeted overhead costs ÷ Budgeted labor costs

= $180,000 ÷ $150,000 = 120% of labor cost

2. Ending work in process

Job 1

Job 2

Total

Direct material costs

$ 3,620

$ 6,830

$10,450

Direct labor costs

4,500

7,250

11,750

Overhead

(1.20 × Direct labor costs)

5,400

8,700

14,100

Total costs

$13,520

$22,780

$36,300

3. Overhead allocated = 1.20

$148,750 = $178,500

4.a. All overallocated overhead is written off to cost of goods sold.

WIP inventory remains unchanged.

Account

(1)

Dec. 31, 2010

Account Balance

(Before Proration)

(2)

Write-off of $2,500

Overallocated

overhead

(3)

Dec. 31, 2010

Account Balance

(After Proration)

(4) = (2) + (3)

Work in Process

$ 36,300

$ 0

$ 36,300

Cost of goods sold

417,450

(2,500)

414,950

$453,750

$(2,500)

$451,250

4b. Overallocated overhead prorated based on ending balances

Account

(1)

Dec. 31, 2010

Balance

(Before Proration)

(2)

Balance as a

Percent of Total

(3) = (2) ÷ $453,750

Proration of $2,500

Overallocated

Overhead

(4) = (3)

$2,500

Dec. 31, 2010

Balance

(After Proration)

(5) = (2) + (4)

Work in Process

$ 36,300

0.08

$ (200)

$ 36,100

Cost of Goods Sold

417,450

0.92

(2,300)

415,150

$453,750

1.00

$(2,500)

$451,250

5. Writing off all of the overallocated overhead to Cost of Goods Sold (CGS) is warranted

4-40 (20 min.) Job costing, contracting, ethics.

1.

Direct manufacturing costs:

Direct materials ($8,000 x 150 huts)

Direct manufacturing labor ($600 150 huts)

Manufacturing overhead ($3 90,000)

Total costs

Markup (15% $1,560,000)

Total bid price

$1,200,000

90,000

270,000

$1,560,000

234,000

$1,794,000

2.

Direct manufacturing costs:

Direct materials

Direct manufacturing labor

Production labor

Inspection labor

Setup labor

Manufacturing overhead

Total costs

Markup (15% of $1,795,200)

Total bid price

$84,000

9,000

10,800

$1,380,000

103,800

311,400

$1,795,200

269,280

$2,064,480

Direct materials = ($1,840,000/200) 150 = $1,380,000

Direct labor = production labor + inspection labor + setup labor

Production labor = 28 hours 150 $20 = $84,000

Inspection labor = 4 hours x 150 $15 = $9,000

Setup labor = 6 hours x 150 $12 = $10,800

Alternatively, Direct manufacturing labor

$138,400 150 huts = $103,800

200 huts

=

Manufacturing overhead = (3 $103,800) = $311,400

3. The main discrepancies in costs (before the mark up) in requirements 1 and 2 are as follows:

a. Materials are marked up by 15% in the Sept. 15, 2005 invoice

4. According to the IMA Standards of Ethical Conduct for Practitioners of Management

Accounting and Financial Management, the following principles should guide your decision

I would go to my boss with the bid in requirement 1 after checking

(a) If any direct material savings is possible and

(b) If direct manufacturing labor can be reduced to 28 hours from 30 hours.

4-41 (35 min.) Job costing-service industry.

Author

Materials

(1)

Direct

Labor

(2)

Overhead

(3) = 80% × (2)

Total

(4)

Asher ($425 + $90; $750 + $225)

$ 515

$ 975

$ 780

$2,270

Brown ($200 + $320; $550 + $450)

520

1,000

800

2,320

Sherman

150

200

160

510

Total

$1,185

$2,175

$1,740

$5,100

2. Cost of Completed Signings (CCS) in April 2010

Author

Materials

(1)

Direct

Labor

(2)

Overhead

(3) = 80% × (2)

Total

(4)

Bucknell ($710 + $150; $575 + $75)

$ 860

$ 650

$ 520

$2,030

King

650

400

320

1,370

Total

$1,510

$1,050

$ 840

$3,400

3. Overhead allocated = 0.80 × 1,350a = $1,080

Underallocated overhead = Actual overhead – Allocated overhead

= $1,980 – 1,080 = $900 underallocated

Account

April 30, 2010

Balance

(Before Proration)

(1)

Proration of

$900

Underallocated

Overhead

(2)

April 30, 2010

Balance

(After

Proration)

(3) = (1) + (2)

SIP

$5,100

$ 0

$5,100

CCS

3,400

900

4,300

$8,500

$900

$9,400

4b. Underallocated overhead prorated based on ending balances

Account

April 30, 2010

Balance

(Before Proration)

(1)

Balance as a

Percent of Total

(2) = (1) ÷ $8,500

Proration of $900

Underallocated

Overhead

(3) = (2)

$900

April 30, 2010

Balance

(After Proration)

(4) = (1) + (3)

SIP

$5,100

0.60

0.60

$900 = $540

$5,640

CCS

3,400

0.40

0.40

$900 = 360

3,760

$8,500

1.00

$900

$9,400

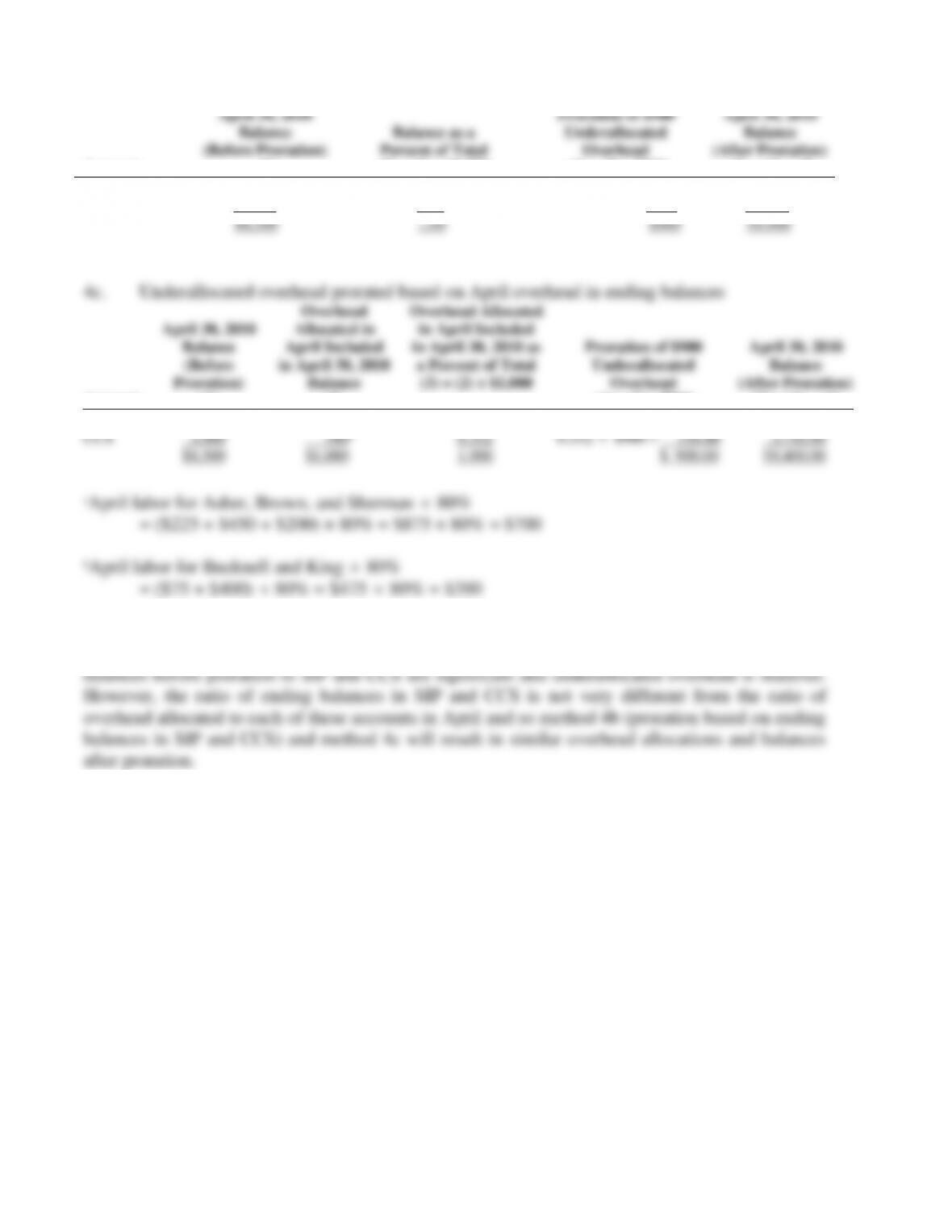

4c. Underallocated overhead prorated based on April overhead in ending balances

Account

April 30, 2010

Balance

(Before

Proration)

(1)

Overhead

Allocated in

April Included

in April 30, 2010

Balance

(2)

Overhead Allocated

in April Included

in April 30, 2010 as

a Percent of Total

(3) = (2) ÷ $1,080

Proration of $900

Underallocated

Overhead

(4) = (3)

$900

April 30, 2010

Balance

(After Proration)

(5) = (1) + (4)

SIP

$5,100

$ 700a

0.648

0.648

$900 = $ 583.20

$5,683.20

CCS

3,400

380b

0.352

0.352

$900 = 316.80

3,716.80

$8,500

$1,080

1.000

$ 900.00

$9,400.00

aApril labor for Asher, Brown, and Sherman

5. I would choose the method in 4c (proration based on overhead allocated) because this

method results in account balances based on actual overhead allocation rates. The account