4-1

CHAPTER 4

JOB COSTING

4-1 Cost pool––a grouping of individual indirect cost items.

Cost tracing––the assigning of direct costs to the chosen cost object.

4-2 In a job-costing system, costs are assigned to a distinct unit, batch, or lot of a product or

4-3 An advertising campaign for Pepsi is likely to be very specific to that individual client.

4-4 The seven steps in job costing are: (1) identify the job that is the chosen cost object, (2)

(5) compute the rate per unit of each cost–allocation base used to allocate indirect costs to the

4-5 Major cost objects that managers focus on in companies using job costing are a product

4-6 Three major source documents used in job-costing systems are (1) job cost record or job

cost sheet, a document that records and accumulates all costs assigned to a specific job, starting

4-7 The main advantages of using computerized source documents for job cost records are

4-8 Two reasons for using an annual budget period are

a. The numerator reason––the longer the time period, the less the influence of seasonal

4-2

4-9 Actual costing and normal costing differ in their use of actual or budgeted indirect cost

rates:

Actual

Costing

Normal

Costing

Direct-cost rates

Indirect-cost rates

Actual rates

Actual rates

Actual rates

Budgeted rates

Each costing method uses the actual quantity of the direct-cost input and the actual quantity of

the cost-allocation base.

4-10 A house construction firm can use job cost information (a) to determine the profitability

4-11 The statement is false. In a normal costing system, the Manufacturing Overhead Control

account will not, in general, equal the amounts in the Manufacturing Overhead Allocated

account. The Manufacturing Overhead Control account aggregates the actual overhead costs

4-12 Debit entries to Work-in-Process Control represent increases in work in process.

4-13 Alternative ways to make end-of-period adjustments to dispose of underallocated or

overallocated overhead are as follows:

(i) Proration based on the total amount of indirect costs allocated (before proration) in

4-14 A company might use budgeted costs rather than actual costs to compute direct labor

4-15 Modern technology of electronic data interchange (EDI) is helpful to managers because it

4-3

4-16 (10 min) Job order costing, process costing.

a. Job costing l. Job costing

b. Process costing m. Process costing

4-4

4-17 (20 min.) Actual costing, normal costing, accounting for manufacturing overhead.

1.

Budgeted manufacturing

overhead rate

=

costslabor ingmanufacturdirect Budgeted

costs overhead ingmanufactur Budgeted

=

$2,700,000

$1,500,000

= 1.80 or 180%

costs overhead ingmanufactur Actual

=

$2,755,000

$1,450,000

= 1.9 or 190%

2. Costs of Job 626 under actual and normal costing follow:

Actual Normal

Costing Costing

3.

Total manufacturing overhead

allocated under normal costing

=

Actual manufacturing

labor costs

Budgeted

overhead rate

= $1,450,000 1.80

Actual manufacturing

overhead.

4-18 (20 -30 min.) Job costing, normal and actual costing.

1.

Budgeted indirect-

cost rate

=

Budgeted indirect costs (assembly support)

Budgeted direct labor-hours

=

$8,300,000

166,000 hours

= $50 per direct labor–hour

Actual indirect-

cost rate

=

Actual indirect costs (assembly support)

Actual direct labor-hours

=

$6,520,000

163,000 hours

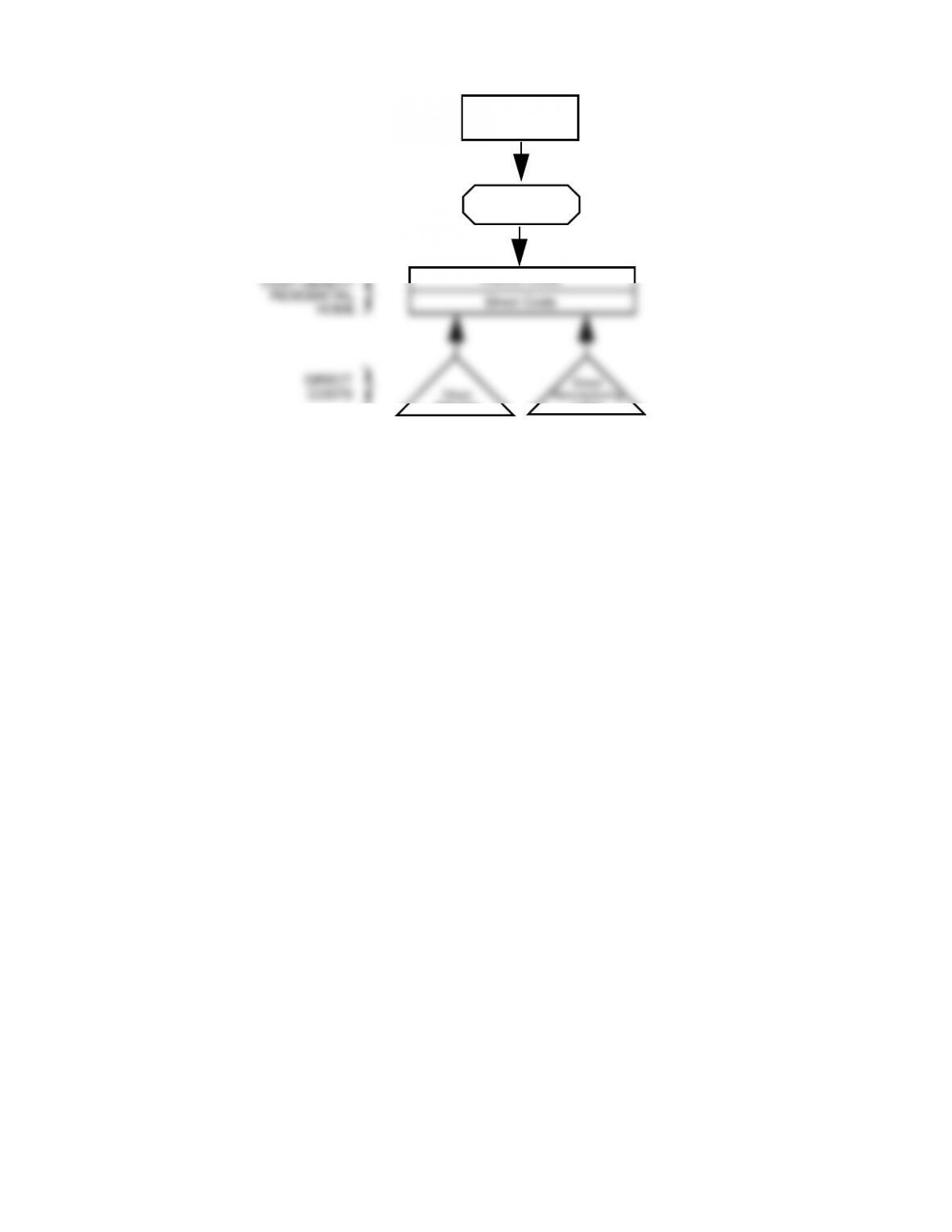

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

Direct

Materials

COST OBJECT:

RESIDENTIAL

HOME

DIRECT

COSTS

Direct

Manufacturing

Labor

Indirect Costs

Direct Costs

Assembly

Support

Direct

Labor-Hours

4-7

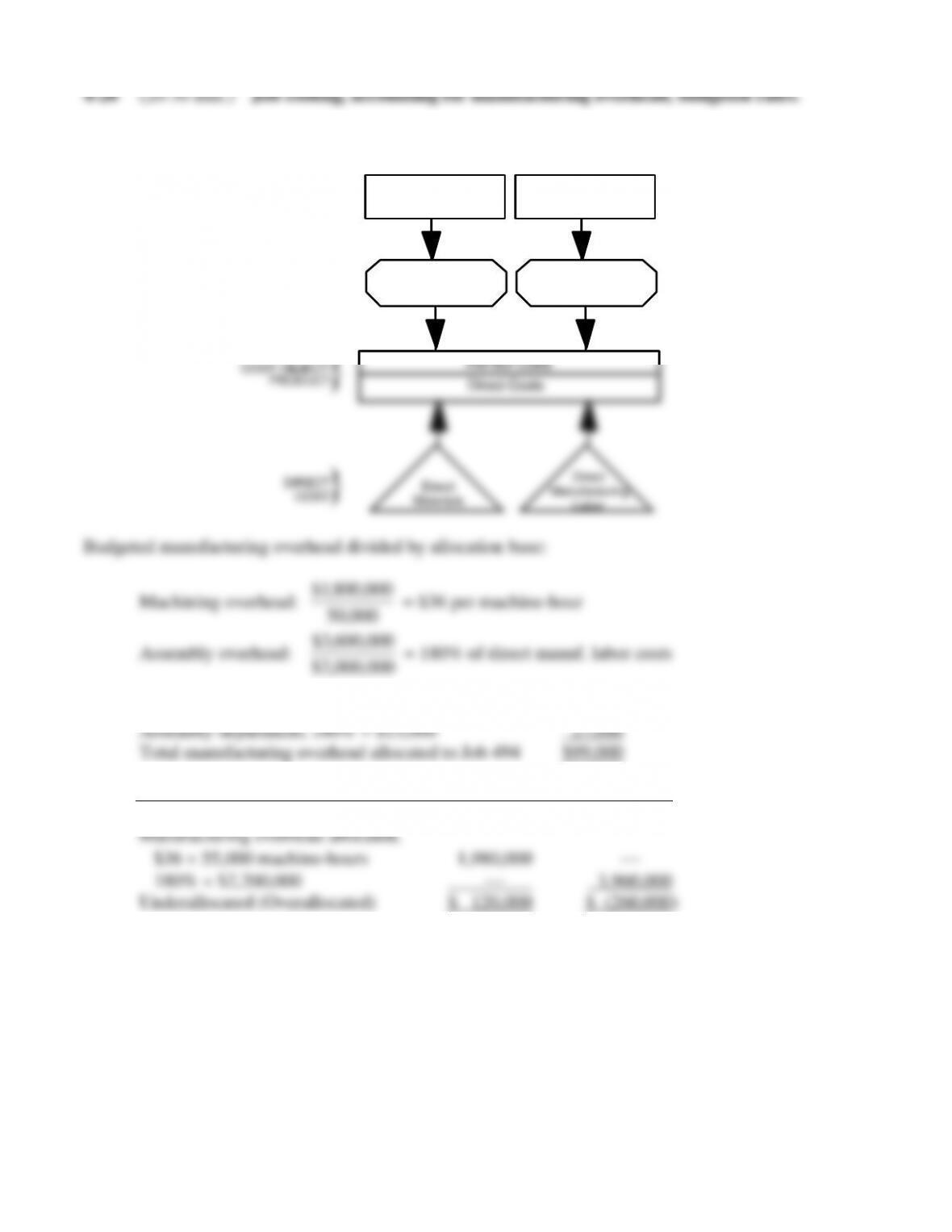

1. Budgeted manufacturing overhead rate =

Budgeted manufacturing overhead

Budgeted machine hours

$4,200,000

175,000 machine-hours

2.

Manufacturing

overhead

allocated

=

Actual

machine-hours

Budgeted

manufacturing

overhead rate

= 170,000 × $24 = $4,080,000

3. Since manufacturing overhead allocated is greater than the actual manufacturing overhead

costs, Gammaro overallocated manufacturing overhead:

4-8

1. An overview of the product costing system is

COST OBJECT:

PRODUCT

COST

ALLOCATION

BASE

DIRECT

COST

Machining Department

Manufacturing Overhead

Machine-Hours

Direct

Materials

INDIRECT

COST

POOL

Direct

Manufacturing

Labor

Indirect Costs

Direct Costs

Assembly Department

Manufacturing Overhead

Direct Manuf.

Labor Cost

000,000,2$

2. Machining department, 2,000 hours $36 $72,000

3. Machining Assembly

Actual manufacturing overhead $2,100,000 $ 3,700,000

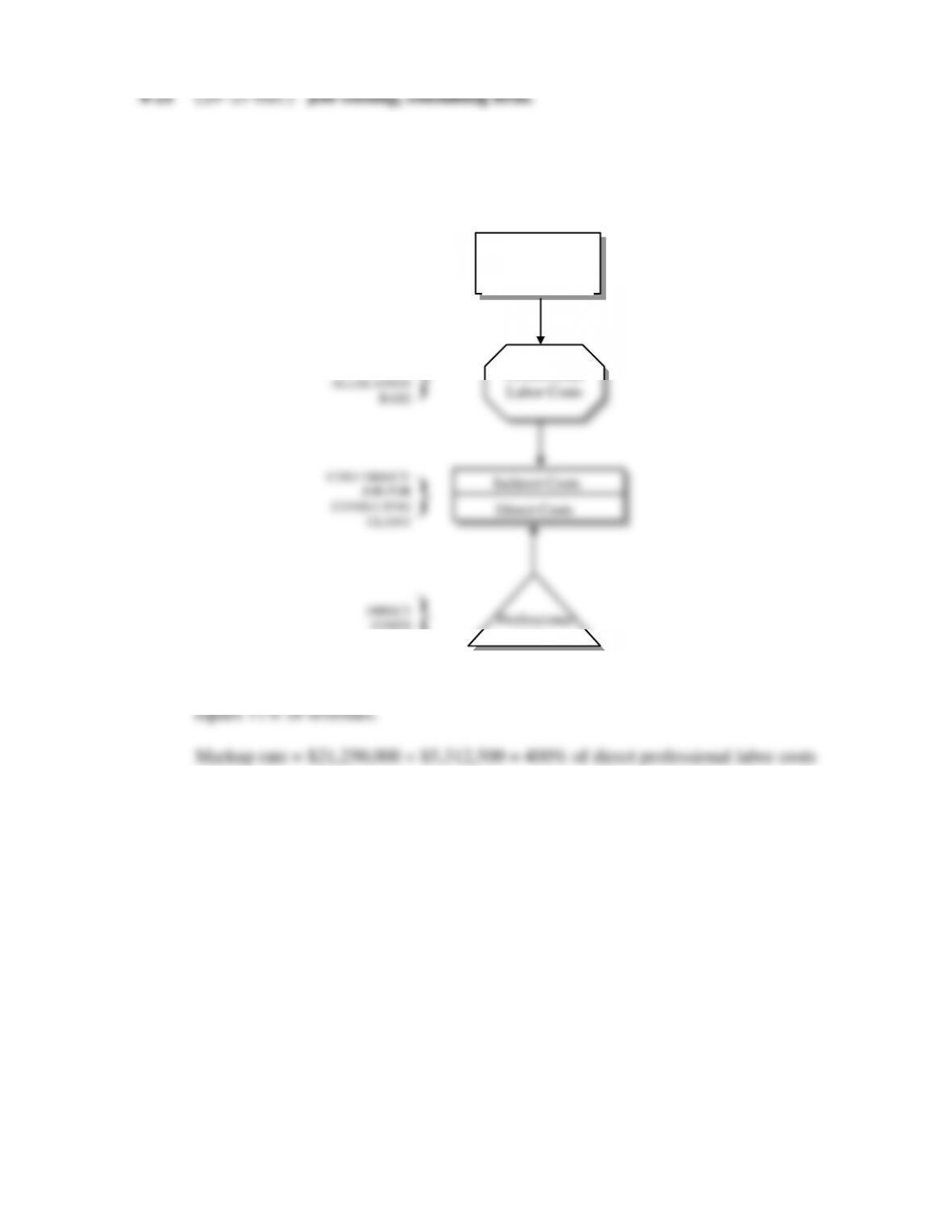

1. Budgeted indirect-cost rate for client support can be calculated as follows:

Budgeted indirect-cost rate = $13,600,000 ÷ $5,312,500 = 256% of professional labor costs

2. At the budgeted revenues of $21,250,000 Taylor’s operating income of $2,337,500

COST

ALLOCATION

BASE

Consulting

Support

Consulting

Support

COST OBJECT:

JOB FOR

CONSULTING

CLIENT

DIRECT

COSTS

Indirect Costs

Direct Costs

INDIRECT

COST

POOL

Professional

Labor Costs

Professional

Labor Costs

Professional

Labor

Client

Support

4-10

3. Budgeted costs

Direct costs:

Director, $198 4 $ 792

Partner, $101 17 1,717

0.89R = $35,867

R = $35,867 ÷ 0.89 = $40,300

Or