1. a. Stand-alone method for the BegM + RCC package

DVD

Separate

Revenue

Percentage

Joint

Revenue

Allocation

1. b. Incremental method

i)

Allocated Revenue

Revenue Remaining

(BegM first)

To Allocate

15-22

2. c. Shapley method. (assuming each DVD is demanded in equal proportion)

3. For each DVD package, the stand-alone method and the Shapley method give

approximately the same allocation to each DVD. These methods are fair if the demand for

15-23

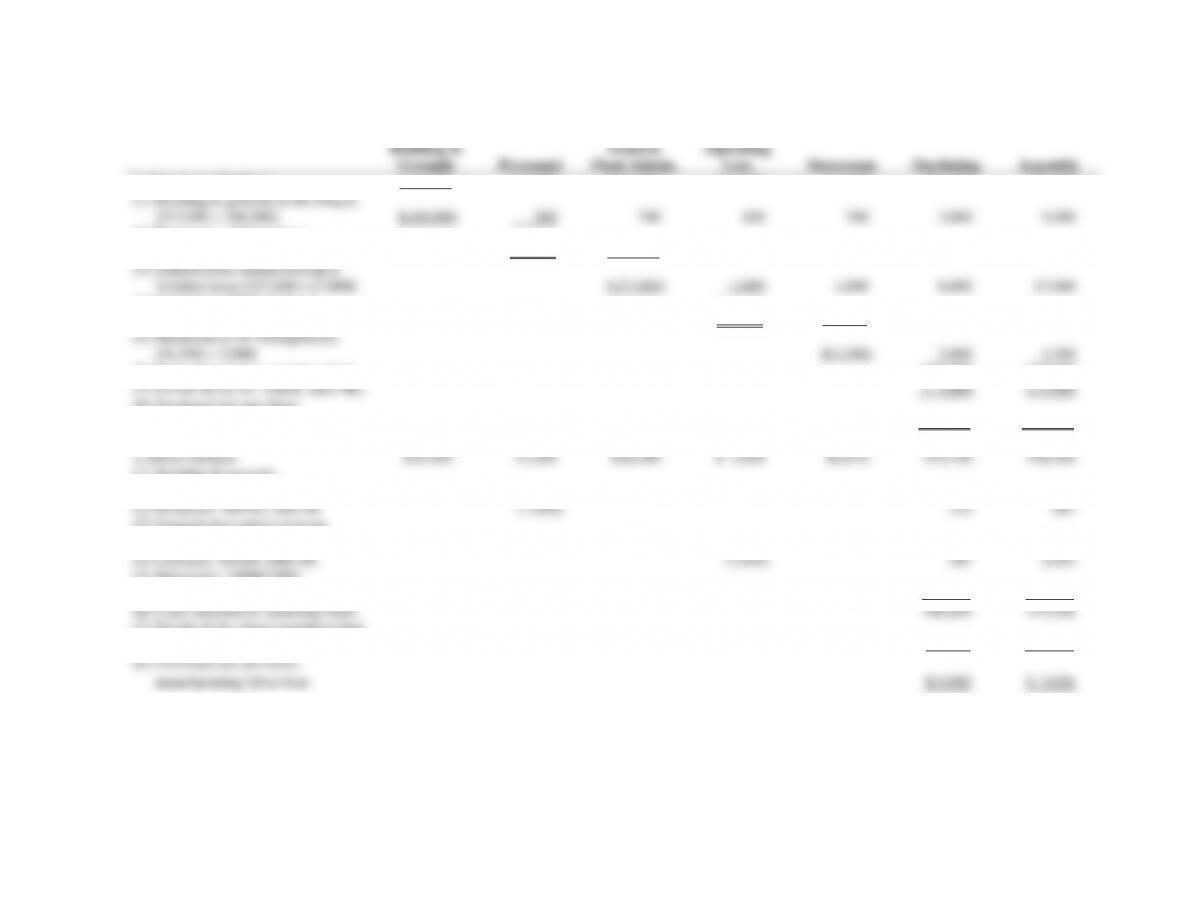

15-29 (20 min.) Fixed cost allocation

1. i) Allocation using actual usage.

Department

Actual

Usage

Percentage of

Total Usage

Allocation

% × 1,500,000a

Executive

16,250

0.25

$ 375,000

Accounting

26,000

0.40

600,000

Human Resources

22,750

0.35

525,000

Total

65,000

$1,500,000

a$30,000,000 building cost/20 years straight-line depreciation = $1,500,000 annual depreciation

expense related to building.

ii) Allocation using planned usage.

Department

Planned

Usage

Percentage of

Total Usage

Allocation

% × 1,500,000

Executive

12,400

0.20

$ 300,000

Accounting

26,040

0.42

630,000

Human Resources

23,560

0.38

570,000

Total

62,000

$1,500,000

iii) Allocation using practical capacity.

Department

Practical

Capacity

Percentage of

Total Usage

Allocation

% × 1,500,000

Executive

18,000

0.24

$ 360,000

Accounting

33,000

0.44

660,000

Human Resources

24,000

0.32

480,000

Total

75,000

$1,500,000

2.

Usage of Space

% of Total

Building Space

% of Total Annual

Building Cost

Office Space (occupied)

52%

$ 780,000

Vacant Office Space

8%

120,000

Common Meeting Space

25%

375,000

Workout Room

5%

75,000

Cafeteria

10%

150,000

Total 100% $1,500,000

a) $120,000 of Vacant Office Space cost will not be allocated to the departments, but will

be absorbed by the university’s central administration.

b) Allocation of Office Space (occupied) costs ($780,000) using actual usage.

Department

Actual

Usage

Percentage of

Total Usage

Allocation

% × 780,000

Executive

16,250

0.25

$195,000

Accounting

26,000

0.40

312,000

Human Resources

22,750

0.35

273,000

Total

65,000

$780,000

Percentage of

Allocation

0.24

$144,000

Accounting

0.44

264,000

0.32

$600,000

15-25

15-30 (45 min.) Allocating costs of support departments; step-down and direct methods.

Building &

Grounds

Personnel

General

Plant Admin.

Cafeteria

Operating

Loss

Storeroom

Machining

Assembly

1. Step-down Method:

$ 10,000

$ 1,000

$ 26,090

$ 1,640

$ 2,670

$34,700

$48,900

(1) Building & grounds at $0.10/sq.ft.

($10,000 ÷ 100,000)

$(10,000)

200

700

400

700

3,000

5,000

(2) Personnel at $6/employee

($1,200 ÷ 200)

$(1,200)

210

60

30

300

600

(3) General plant administration at

$1/labor-hour ($27,000 ÷ 27,000)

$(27,000)

1,000

1,000

8,000

17,000

(4) Cafeteria at $20/empoloyee

($3,100 ÷ 155)

$(3,100)

100

1,000

2,000

(5) Storeroom at $1.50/requisition

($4,500 ÷ 3,000)

$(4,500)

3,000

1,500

(6) Costs allocated to operating depts.

$50,000

$75,000

(7) Divide (6) by dir. manuf. labor-hrs.

÷ 5,000

÷15,000

(8) Overhead rate per direct

manuf. labor-hour

$ 10

$ 5

2. Direct method:

$10,000

$1,000

$26,090

$ 1,640

$2,670

$34,700

$48,900

(1) Building & grounds,

30,000/80,000; 50,000/80,000

(10,000)

3,750

6,250

(2) Personnel, 50/150; 100/150

(1,000)

333

667

(3) General plant administration,

8,000/25,000; 17,000/25,000

(26,090)

8,349

17,741

(4) Cafeteria, 50/150; 100/150

(1,640)

547

1,093

(5) Storeroom: 2,000/3,000;

1,000/3,000

(2,670)

1,780

890

(6) Costs allocated to operating depts.

$49,459

$75,541

(7) Divide (6) by direct manufacturing

labor-hours

÷ 5,000

÷15,000

(8) Overhead rate per direct

manufacturing labor-hour

$ 9.892

$ 5.036

15-26

3. Comparison of Methods:

Step-down method: Job 88: Machining 18 × $10 $ 180

Assembly 2 × $ 5 10 $190.00

4. The manager of Machining Department would prefer the direct method. The direct

15-27

15-31 (40–60 min.) Support-department cost allocations; single-department cost pools;

1.

Direct method: To X To Y

A 250/400 $100,000 = $62,500 150/400 $100,000 = $37,500

B 100/500 $ 40,000 = 8,000 400/500 $ 40,000 = 32,000

Total $70,500 $69,500

Step-down method, allocating A first:

A

B

X

Y

A

B

X

Y

0.9 A = $120,000

A = $133,333

Substituting in (2): B = $40,000 + 0.2($133,333)

15-28

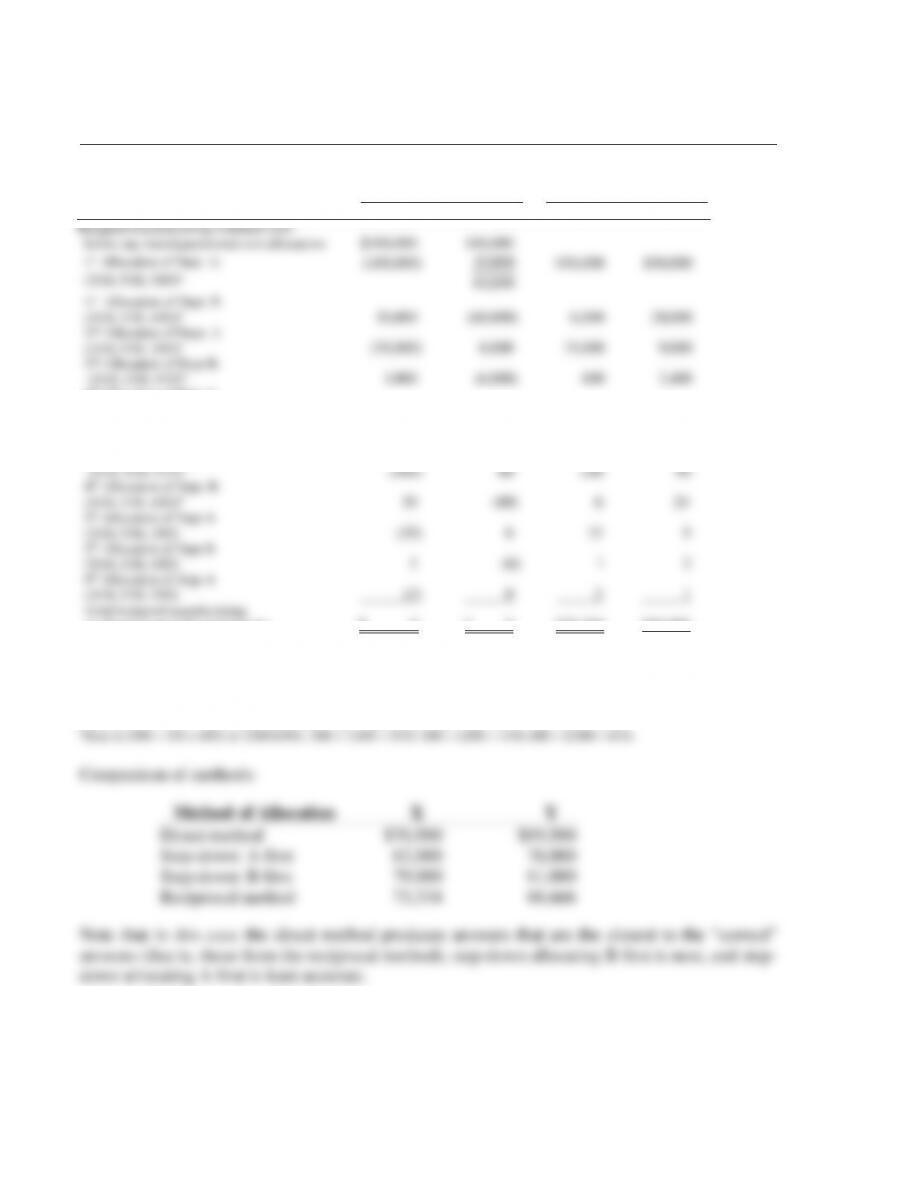

SOLUTION EXHIBIT 15-31

Reciprocal Method of Allocating Support Department Costs for Manes Company Using

Repeated Iterations.

Support Departments

Operating

Departments

A B X Y

Budgeted manufacturing overhead costs

before any interdepartmental cost allocations

$100,000

$40,000

1st Allocation of Dept. A:

(2/10, 5/10, 3/10)a

(100,000)

00060

00020

,

,

$50,000

$30,000

1st Allocation of Dept. B

(5/10, 1/10, 4/10)b

30,000

(60,000)

6,000

24,000

2nd Allocation of Dept. A

(2/10, 5/10, 3/10)a

(30,000)

6,000

15,000

9,000

2nd Allocation of Dept B:

(5/10, 1/10, 4/10)b

3,000

(6,000)

600

2,400

3rd Allocation of Dept A:

(2/10, 5/10, 3/10)a

(3,000)

600

1,500

900

3rd Allocation of Dept. B:

(5/10, 1/10, 4/10)b

300

(600)

60

240

4th Allocation of Dept. A

(2/10, 5/10, 3/10)a

(300)

60

150

90

4th Allocation of Dept. B

(5/10, 1/10, 4/10)b

30

(60)

6

24

5th Allocation of Dept A

(2/10, 5/10, 3/10)

(30)

6

15

9

5th Allocation of Dept B

(5/10, 1/10, 4/10)

3

(6)

1

2

6th Allocation of Dept A

(2/10, 5/10, 3/10)

(3)

0

2

1

Total budgeted manufacturing

overhead of operating departments

$ 0

$ 0

$73,334

$66,666

Total accounts allocated and reallocated (the numbers in parentheses in first two columns)

Dept A; Materials Handling: $100,000 + $30,000 + $3,000 + $300 + $30 + $3 = $133,333

Dept B; Power Generation: $60,000 + $6,000 + $600 + $60 + $6 = $66,666

aBase is (100 + 250 +150) or 500 labor-hours; 100 ÷ 500 = 2/10, 250 ÷ 500 = 5/10, 150 ÷ 500 = 3/10.

2. At first glance, it appears that the cost of power is $40 per unit plus the material

handling costs. If so, Manes would be better off by purchasing from the power company.

However, the decision should be influenced by the effects of the interdependencies and the fixed

costs. Note that the power needs would be less (students frequently miss this) if they were

purchased from the outside:

Outside

Power Units

Needed

X 100

Y 400

A (500 units minus 20% of 500 units,

because there is no need to service

the nonexistent power department) 400

Total units 900

Total costs, 900 $40 = $36,000

In contrast, the total costs that would be saved by not producing the power inside would depend

on the effects of the decision on various costs:

Avoidable Costs of

1,000 Units of Power

Produced Inside

Variable indirect labor and indirect material costs

Supervision in power department

Materials handling, 20% of $70,000*

Probable minimum cost savings

Possible additional savings:

a. Can any supervision in materials handling be saved

because of overseeing less volume?

Minimum savings is probably zero; the maximum is

probably 20% of $10,000 or $2,000.

b. Is any depreciation a truly variable, wear-and-tear type of

cost?

Total savings by not producing 1,000 units of power

$10,000

10,000

14,000

$34,000

?

?

______

$34,000 + ?

* Materials handling costs are higher because the power department uses

20% of materials handling. Therefore, materials-handling costs will decrease

by 20%.

In the short run (at least until a capital investment in equipment is necessary), the data suggest

continuing to produce internally because the costs eliminated would probably be less than the

15-30

15-32 (25 min.) Common costs.

1. Stand-alone cost-allocation method.

Wright Inc. =

(800 $50) (1,000 $42)

(800 $50) (200 $50)

+

$40,000 $42,000

2. With Wright Inc. as the primary party:

Party

Costs Allocated

Cumulative Costs

Allocated

Wright

$40,000

$40,000

Brown

2,000 ($42,000 – $40,000)

$42,000

Total

$42,000

With Brown Inc. as the primary party:

Party

Costs Allocated

Cumulative Costs

Allocated

Brown

$10,000

$10,000

Wright

32,000 ($42,000 – $10,000)

$42,000

Total

$42,000

$10,000 $42,000