6-21

4. Scarborough Corporation

Direct Materials Purchases Budget (in dollars) for 2012

Budgeted

Expected

Purchases

Purchase

(Units)

Price per unit

Total

Direct material A

469,000

$12

$5,628,000

Direct material B

256,000

5

1,280,000

Direct material C

42,000

3

126,000

Budgeted purchases

$7,034,000

5. Scarborough Corporation

Direct Manufacturing Labor Budget (in dollars) for 2012

Direct

Budgeted

Manufacturing

Rate

Production

Labor-Hours

Total

per

(Units)

per Unit

Hours

Hour

Total

Thingone

65,000

2

130,000

$12

$1,560,000

Thingtwo

41,000

3

123,000

16

1,968,000

Total

$3,528,000

6. Scarborough Corporation

Budgeted Finished Goods Inventory

at December 31, 2012

Thingone:

Direct materials costs:

6-22

6-31 (30 min.) Budgeted income statement.

Easecom Company

Budgeted Income Statement for 2012

(in thousands)

Revenues

6-32 (15 min.) Responsibility of purchasing agent.

The cost of the biscuits is usually the responsibility of the purchasing agent, and usually

controllable by the Central Warehouse. However, in this scenario, Janet the cook has taken the

responsibility for the cost of the replacement biscuits from the purchasing agent by making a

1.

Revenue Budget

For the Month of April

Units

Selling Price

Total Revenues

Cat-allac

580

$190

$ 110,200

Dog-eriffic

240

275

66,000

Total

$176,200

2.

Production Budget

For the Month of April

Product

Cat-allac

Dog-eriffic

Budgeted unit sales

580

240

Add target ending finished goods inventory

45

25

Total required units

625

265

Deduct beginning finished goods inventory

25

40

Units of finished goods to be produced

600

225

Total

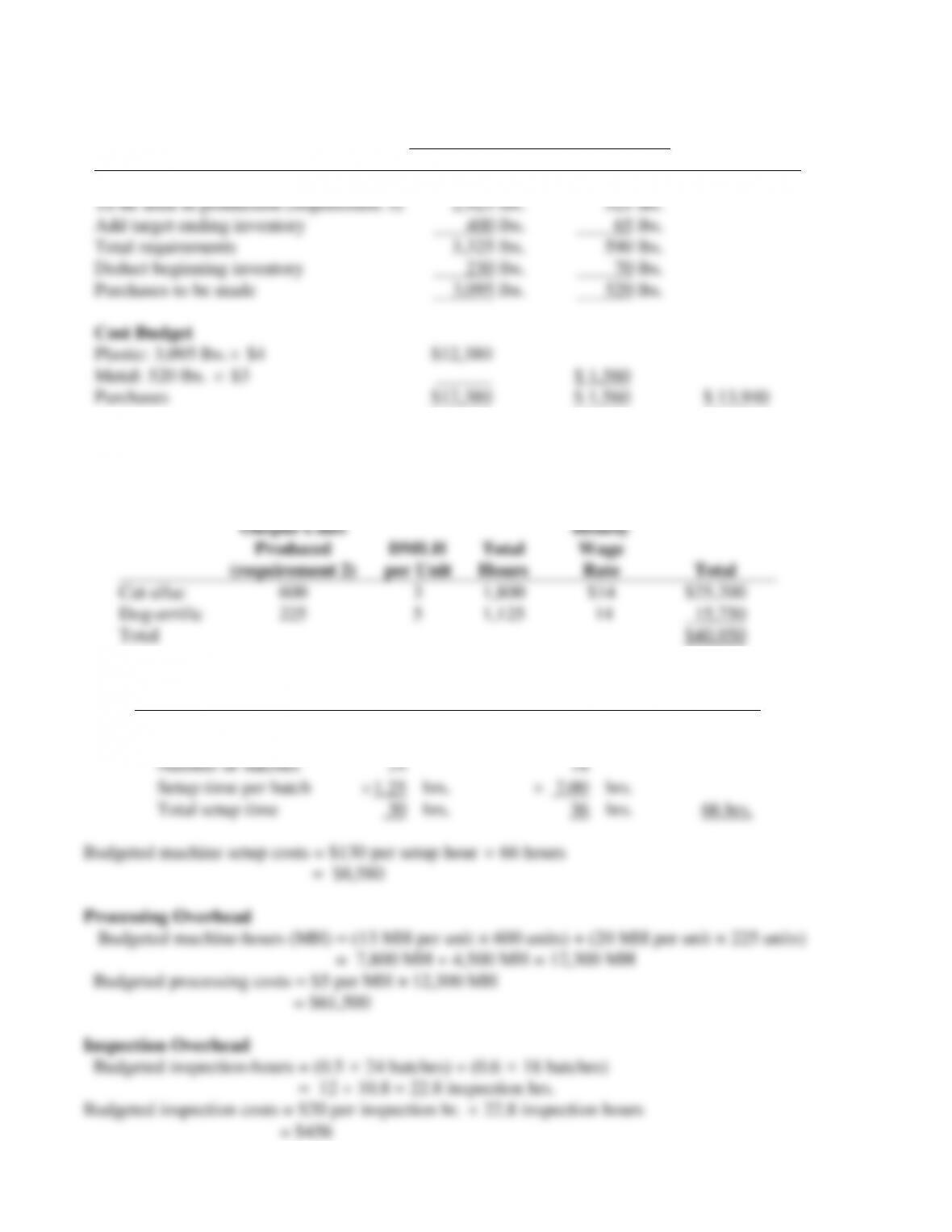

Direct materials required for

Cat-allac (600 units × 3 lbs. and 0.5 lb.)

Dog-errific (225 units × 5 lbs. and 1 lb.)

Available from beginning direct materials inventory

(under a FIFO cost-flow assumption)

Plastic: 230 lbs. × $3.80 per lb.

Metal: 70 lbs. × $3.20 per lb.

To be purchased this period

Plastic: (2,925 – 230) lbs.

Metal: (525 – 70) lbs.

6-24

Direct Material Purchases Budget

For the Month of April

Material

Plastic

Metal

Total

Physical Units Budget

To be used in production (requirement 3)

2,925 lbs.

525 lbs.

Add target ending inventory

400 lbs.

65 lbs.

Total requirements

3,325 lbs.

590 lbs.

Deduct beginning inventory

230 lbs.

70 lbs.

Purchases to be made

3,095 lbs.

520 lbs.

Cost Budget

Plastic: 3,095 lbs.

$4

$12,380

Metal: 520 lbs.

$3

______

$ 1,560

Purchases

$12,380

$ 1,560

$ 13,940

4.

Direct Manufacturing Labor Costs Budget

For the Month of April

Output Units

Produced

DMLH

Total

Hourly

Wage

(requirement 2)

per Unit

Hours

Rate

Total

Cat-allac

600

3

1,800

$14

$25,200

Dog-errific

225

5

1,125

14

15,750

Total

$40,950

5. Machine Setup Overhead

Cat-allac

Dog-errific

Total

Units to be produced

600

225

Units per batch

÷ 25

÷13

Number of batches

24

18

Setup time per batch

1.25

hrs.

2.00

hrs.

Total setup time

30

hrs.

36

hrs.

66 hrs.

6-25

Manufacturing Overhead Budget

For the Month of April

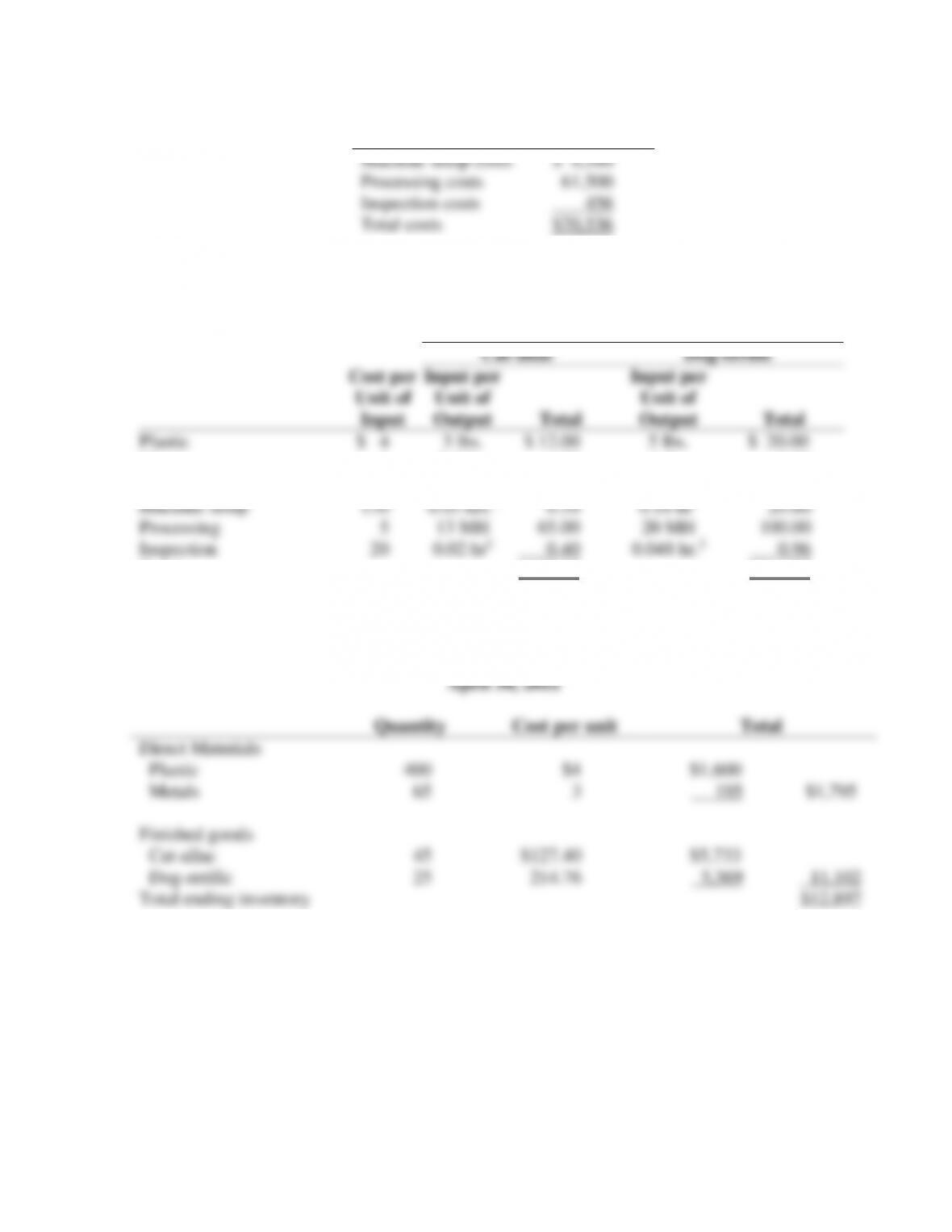

Machine setup costs

$ 8,580

Processing costs

61,500

Inspection costs

456

Total costs

$70,536

6.

Unit Costs of Ending Finished Goods Inventory

April 30, 20xx

Product

Cat-allac

Dog-errific

Cost per

Input per

Input per

Unit of

Input

Unit of

Output

Total

Unit of

Output

Total

Plastic

$ 4

3 lbs.

$ 12.00

5 lbs.

$ 20.00

Metal

3

0.5 lbs.

1.50

1 lb.

3.00

Direct manufacturing labor

14

3 hrs.

42.00

5 hrs.

70.00

Machine setup

130

0.05 hrs. 1

6.50

0.16 hr1

20.80

Processing

5

13 MH

65.00

20 MH

100.00

Inspection

20

0.02 hr2

0.40

0.048 hr.2

0.96

Total

$127.40

$214.76

1 30 setup-hours ÷ 600 units = 0.05 hours per unit; 36 setup-hours ÷ 225 units = 0.16 hours per unit

2 12 inspection hours ÷ 600 units = 0.02 hours per unit; 10.8 inspection hours ÷ 225 units = 0.048 hours per unit

Ending Inventories Budget

April 30, 20xx

Quantity

Cost per unit

Total

Direct Materials

Plastic

400

$4

$1,600

Metals

65

3

195

$1,795

Finished goods

Cat-allac

45

$127.40

$5,733

Dog-errific

25

214.76

5,369

11,102

Total ending inventory

$12,897

6-26

7.

Cost of Goods Sold Budget

For the Month of April, 20xx

Beginning finished goods inventory, April, 1 ($2,500 + $7,440)

$ 9,940

Direct materials used (requirement 3)

$13,243

Direct manufacturing labor (requirement 4)

40,950

Manufacturing overhead (requirement 5)

70,536

Cost of goods manufactured

124,729

Cost of goods available for sale

134,669

Deduct: Ending finished goods inventory, April 30 (reqmt. 6)

11,102

Cost of goods sold

$123,567

8.

Nonmanufacturing Costs Budget

For the Month of April, 20xx

Salaries ($32,000 ÷ 2

1.05)

$16,800

Other fixed costs ($32,000 ÷ 2)

16,000

Sales commissions ($176,200

1%)

1,762

Total nonmanufacturing costs

$34,562

9.

Budgeted Income Statement

For the Month of April, 20xx

Revenues

$176,200

Cost of goods sold

123,567

Gross margin

52,633

Operating (nonmanufacturing) costs

34,562

Operating income

$ 18,071

6-27

6-34 (25 min.) (Continuation of 6-33) Cash budget (Appendix)

Cash Budget

April 30, 20xx

Cash balance, April 1, 20xx

$ 5,200

Add receipts

Cash sales ($176,200 × 10%)

17,620

Credit card sales ($176,200 × 90% × 98%)

155,408

Total cash available for needs (x)

$178,228

Deduct cash disbursements

Direct materials ($8,400 + $13,940 × 50%)

$ 15,370

Direct manufacturing labor

40,950

Manufacturing overhead ($70,536 ─ $22,500 depreciation)

48,036

Nonmanufacturing salaries

16,800

Sales commissions

1,762

Other nonmanufacturing fixed costs ($16,000 ─ $12,500 deprn)

3,500

Machinery purchase

13,800

Income taxes

5,400

Total disbursements (y)

$145,618

Financing

Repayment of loan

$ 2,600

Interest at 24% ($2,600

24%

1

12

)

52

Total effects of financing (z)

$ 2,652

Ending cash balance, April 30 (x) ─ (y) ─ (z)

$ 29,958

6-28

1. Schedule 1: Revenues Budget for the Year Ended December 31, 2012

2. Schedule 2: Production Budget (in Units) for the Year Ended December 31, 2012

Snowboards

3. Schedule 3A: Direct Materials Usage Budget for the Year Ended December 31, 2012

Wood Fiberglass Total

Physical Units Budget

Wood: 1,100 × 5.00 b.f. 5,500

Fiberglass: 1,100 × 6.00 yards 6,600

6-29

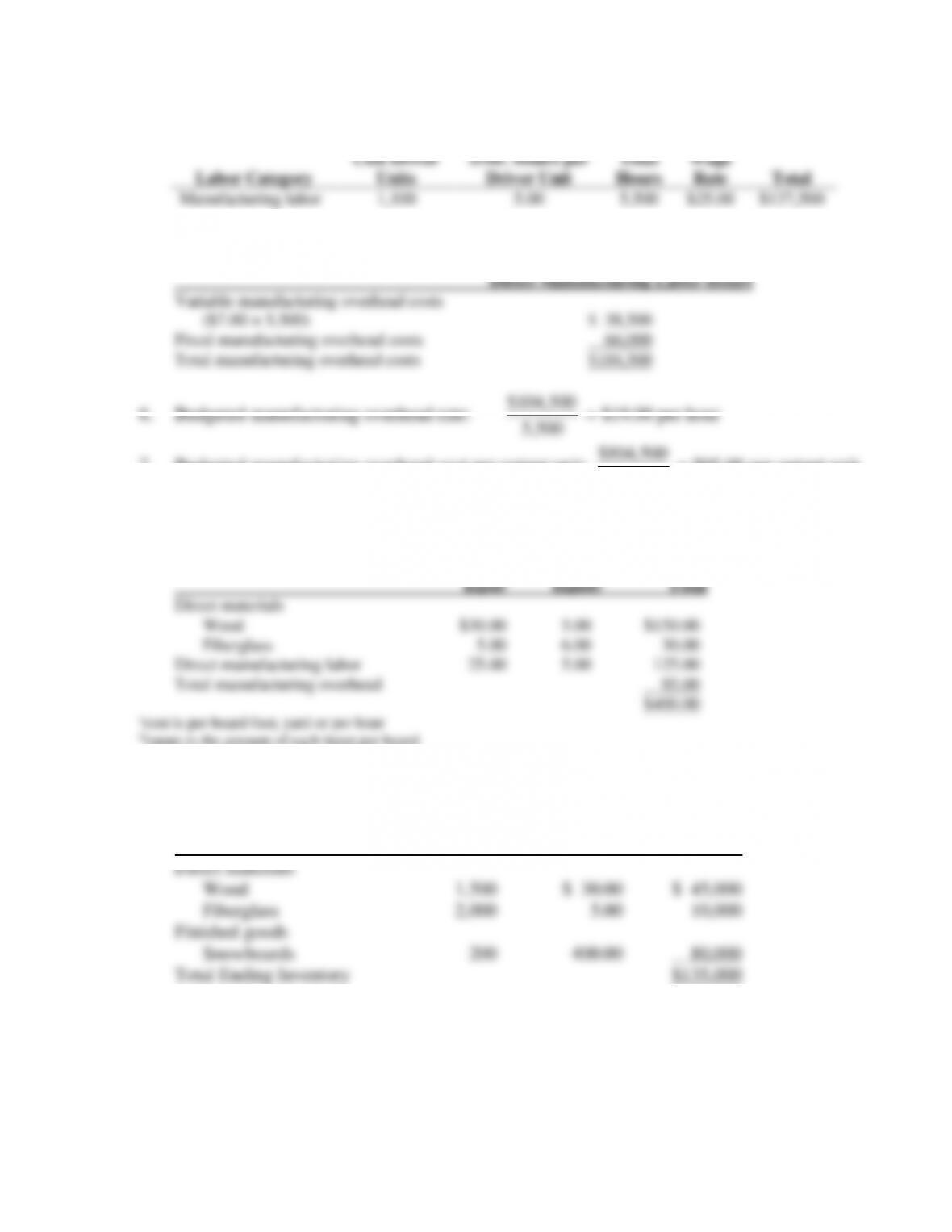

4. Schedule 4: Direct Manufacturing Labor Budget for the Year Ended December 31, 2012

Labor Category

Cost Driver

Units

DML Hours per

Driver Unit

Total

Hours

Wage

Rate

Total

Manufacturing labor

1,100

5.00

5,500

$25.00

$137,500

5. Schedule 5: Manufacturing Overhead Budget for the Year Ended December 31, 2012

At Budgeted Level of 5,500

5,500

7. Budgeted manufacturing overhead cost per output unit:

1,100

$104,500

= $95.00 per output unit

8. Schedule 6A: Computation of Unit Costs of Manufacturing Finished Goods in 2012

Cost per

Unit of

9. Schedule 6B: Ending Inventories Budget, December 31, 2012

Cost per

Units Unit Total

6-30

10. Schedule 7: Cost of Goods Sold Budget for the Year Ended December 31, 2012

From

Schedule Total

Beginning finished goods inventory

11. Budgeted Income Statement for Slopes for the Year Ended December 31, 2012

Revenues Schedule 1 $450,000

12. Budgeted Balance Sheet for Slopes as of December 31, 2012

Cash $ 10,000

Inventory Schedule 6B 135,000