3-31

Sales revenue 5,000

1.20

$60 $360,000

Variable costs 5,000

1.20

$25 × (1 – 0.20) 120,000

1. CMU (SP – VCU = $30 – $21) $ 9.00

a. Breakeven units (FC

CMU = $360,000

$9 per unit) 40,000

2. Pairs sold 35,000

Revenues, 35,000

$30 $1,050,000

Total cost of shoes, 35,000

$19.50 682,500

3. Unit variable data (per pair of shoes)

Selling price $ 30.00

Cost of shoes 19.50

Sales commissions 0

3-32

4. Unit variable data (per pair of shoes)

Selling price $ 30.00

Cost of shoes 19.50

5. Pairs sold 50,000

Revenues (50,000 pairs

$30 per pair) $1,500,000

Total cost of shoes (50,000 pairs

$19.50 per pair) $ 975,000

Sales commissions on first 40,000 pairs (40,000 pairs

$1.50 per pair) 60,000

3-33

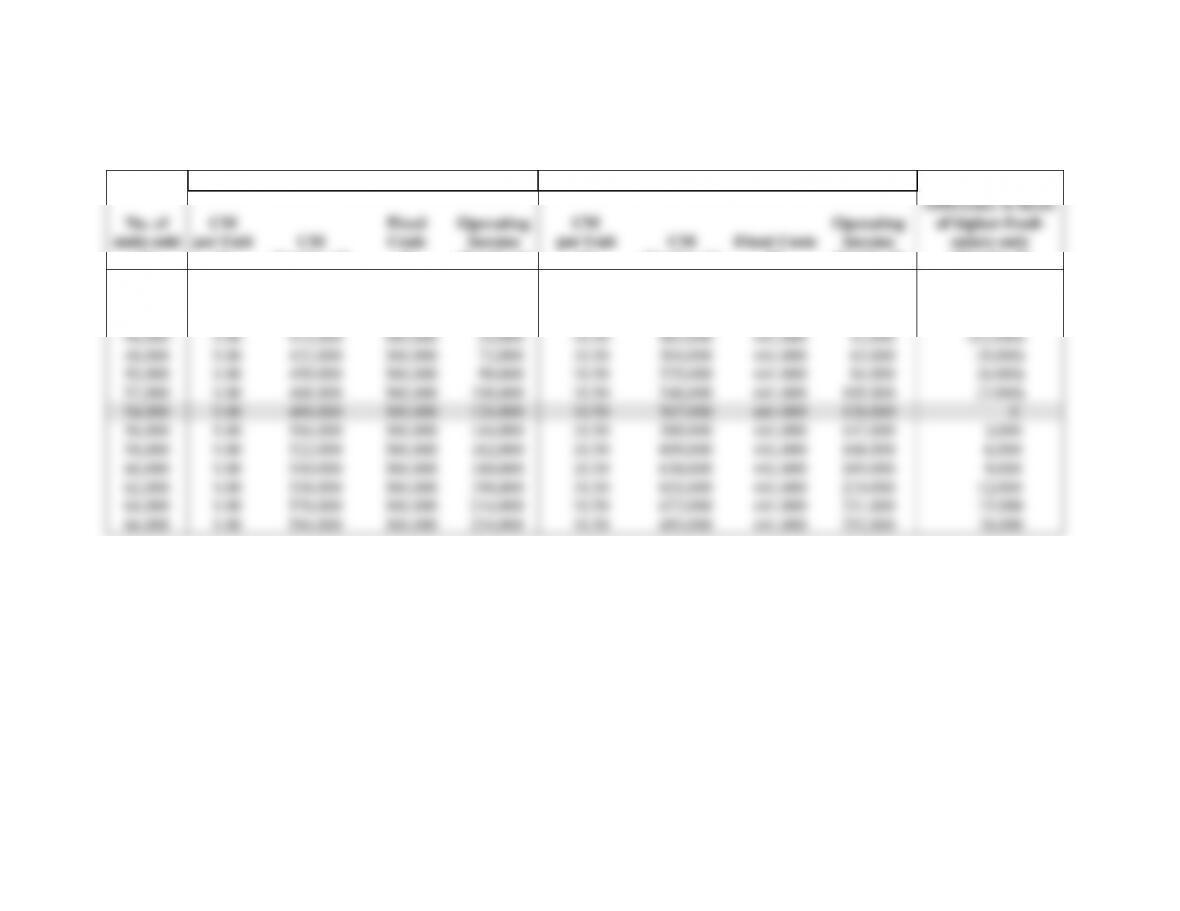

3-39 (30 min.) CVP analysis, shoe stores (continuation of 3-38).

Salaries + Commission Plan

Higher Fixed Salaries Only

No. of

units sold

CM

per Unit

CM

Fixed

Costs

Operating

Income

CM

per Unit

CM

Fixed Costs

Operating

Income

Difference in favor

of higher-fixed-

salary-only

(1)

(2)

(3)=(1)

(2)

(4)

(5)=(3)–(4)

(6)

(7)=(1)

(6)

(8)

(9)=(7)–(8)

(10)=(9)–(5)

40,000

$9.00

$360,000

$360,000

0

$10.50

$420,000

$441,000

$ (21,000)

$(21,000)

42,000

9.00

378,000

360,000

18,000

10.50

441,000

441,000

0

(18,000)

44,000

9.00

396,000

360,000

36,000

10.50

462,000

441,000

21,000

(15,000)

46,000

9.00

414,000

360,000

54,000

10.50

483,000

441,000

42,000

(12,000)

48,000

9.00

432,000

360,000

72,000

10.50

504,000

441,000

63,000

(9,000)

50,000

9.00

450,000

360,000

90,000

10.50

525,000

441,000

84,000

(6,000)

52,000

9.00

468,000

360,000

108,000

10.50

546,000

441,000

105,000

(3,000)

54,000

9.00

486,000

360,000

126,000

10.50

567,000

441,000

126,000

0

56,000

9.00

504,000

360,000

144,000

10.50

588,000

441,000

147,000

3,000

58,000

9.00

522,000

360,000

162,000

10.50

609,000

441,000

168,000

6,000

60,000

9.00

540,000

360,000

180,000

10.50

630,000

441,000

189,000

9,000

62,000

9.00

558,000

360,000

198,000

10.50

651,000

441,000

210,000

12,000

64,000

9.00

576,000

360,000

216,000

10.50

672,000

441,000

231,000

15,000

66,000

9.00

594,000

360,000

234,000

10.50

693,000

441,000

252,000

18,000

3-34

1. See preceding table. The new store will have the same operating income under either

compensation plan when the volume of sales is 54,000 pairs of shoes. This can also be calculated

2. When sales volume is above 54,000 pairs, the higher-fixed-salaries plan results in lower

costs and higher operating incomes than the salary-plus-commission plan. So, for an expected

3. Let TQ = Target number of units

For the salary-only plan,

$30.00TQ – $19.50TQ – $441,000 = $168,000

$10.50TQ = $609,000

4. WalkRite Shoe Company

Operating Income Statement, 2011

3-35

1. Contribution margin per

page assuming current

fixed leasing agreement

= $0.15 – $0.03 – $0.04 = $0.08 per page

Fixed costs = $1,000

Fixed costs $1,000 12,500 pages

2. Let

x

denote the number of pages Stylewise must sell for it to be indifferent between the

x

$0.15

x

– $0.03

x

– $0.04

x

– $1,000 = $0.15

x

– $0.02

x

– $0.03

x

– $.04

x

x

x

$0.02

x

= $1,000

x

= $1,000 ÷ $0.02 = 50,000 pages

x

x

x

3. Fixed leasing agreement

Pages

Sold

(1)

Revenue

(2)

Variable

Costs

(3)

Fixed

Costs

(4)

Operating

Income

(Loss)

(5)=(2)–(3)–(4)

Probability

(6)

Expected

Operating

Income

(7)=(5)

(6)

20,000

20,000

$.15=$ 3,000

20,000

$.07=$1,400

$1,000

$ 600

0.20

$ 120

40,000

40,000

$.15=$ 6,000

40,000

$.07=$2,800

$1,000

$2,200

0.20

440

60,000

60,000

$.15=$ 9,000

60,000

$.07=$4,200

$1,000

$3,800

0.20

760

80,000

80,000

$.15=$12,000

80,000

$.07=$5,600

$1,000

$5,400

0.20

1,080

100,000

100,000

$.15=$15,000

100,000

$.07=$7,000

$1,000

$7,000

0.20

1,400

Expected value of fixed leasing agreement

$3,800

3-37

1. Variable cost per computer = $100 + ($15

10) + $50 = $300

Contribution margin per computer = Selling price –Variable cost per computer

2. Target number of computers =

Fixed costs + Target operating income

Contribution margin per computer

$200 =

3. Contribution margin per computer = Selling price – Variable cost per computer

= $500 – $200 – $50 = $250

Contribution margin per computer $250

4. Let

x

be the number of computers for which PC Planet is indifferent between paying

a monthly rental fee for the retail space and paying a 20% commission on sales. PC

Planet will be indifferent when the profits under the two alternatives are equal.

$500

x

x

x

x

x

3-38

3-42 (30 min.) CVP analysis, income taxes, sensitivity.

1a.To breakeven, Agro Engine Company must sell 1,200 units. This amount represents the point

where revenues equal total costs.

Let Q denote the quantity of engines sold.

Revenue = Variable costs + Fixed costs

2. To achieve its net income objective, Agro Engine Company should select alternative c,

where fixed costs are reduced by 20% and selling price is reduced by 10% resulting in 1,700

additional units being sold through the end of the year. This alternative results in the highest net

3-39

Alternative b

Revenues = ($3,000 300) + ($2,750c 1,800) = $5,850,000

Variable costs = ($500 300) + ($450d 1,800) = $960,000

Operating income = $5,850,000 − $960,000 − $3,000,000 = $1,890,000

1. We can recast Marston’s income statement to emphasize contribution margin, and then use it

to compute the required CVP parameters.

Marston Corporation

Income Statement

For the Year Ended December 31, 2011

Using Sales Agents

Using Own Sales Force

Revenues

$26,000,000

$26,000,000

Variable Costs

Cost of goods sold—variable

$11,700,000

$11,700,000

Marketing commissions

4,680,000

16,380,000

2,600,000

14,300,000

Contribution margin

9,620,000

11,700,000

Fixed Costs

Cost of goods sold—fixed

2,870,000

2,870,000

Marketing—fixed

3,420,000

6,290,000

5,500,000

8,370,000

Operating income

$ 3,330,000

$ 3,330,000

Contribution margin percentage

($9,620,000

26,000,000;

$11,700,000

$26,000,000)

37%

45%

Breakeven revenues

($6,290,000

0.37;

$8,370,000

0.45)

$17,000,000

$18,600,000

Degree of operating leverage

($9,620,000

$3,330,000;

$11,700,000

$3,330,000)

2.89

3.51

2. The calculations indicate that at sales of $26,000,000, a percentage change in sales and

contribution margin will result in 2.89 times that percentage change in operating income if

Marston continues to use sales agents and 3.51 times that percentage change in operating income

3. Variable costs of marketing = 15% of Revenues

Fixed marketing costs = $5,500,000

Variable

Fixed

Variable

Fixed