2-26 (20 min.) Total costs and unit costs

1.

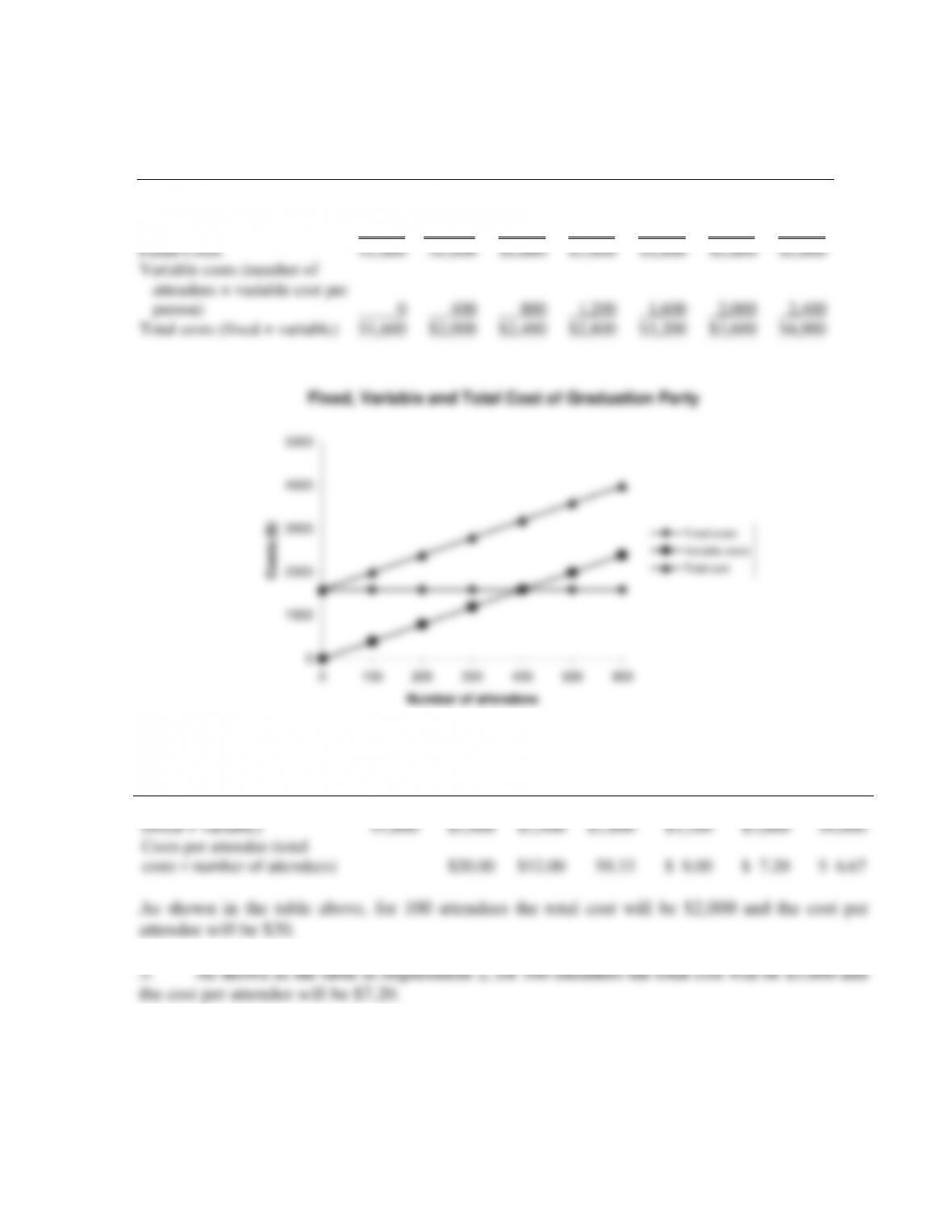

Number of attendees 0 100 200 300 400 500 600

Variable cost per person

($9 caterer charge –

$5 student door fee) $4 $4 $4 $4 $4 $4 $4

Fixed Costs $1,600 $1,600 $1,600 $1,600 $1,600 $1,600 $1,600

Variable costs (number of

attendees × variable cost per

person) 0 400 800 1,200 1,600 2,000 2,400

Total costs (fixed + variable) $1,600 $2,000 $2,400 $2,800 $3,200 $3,600 $4,000

2-12

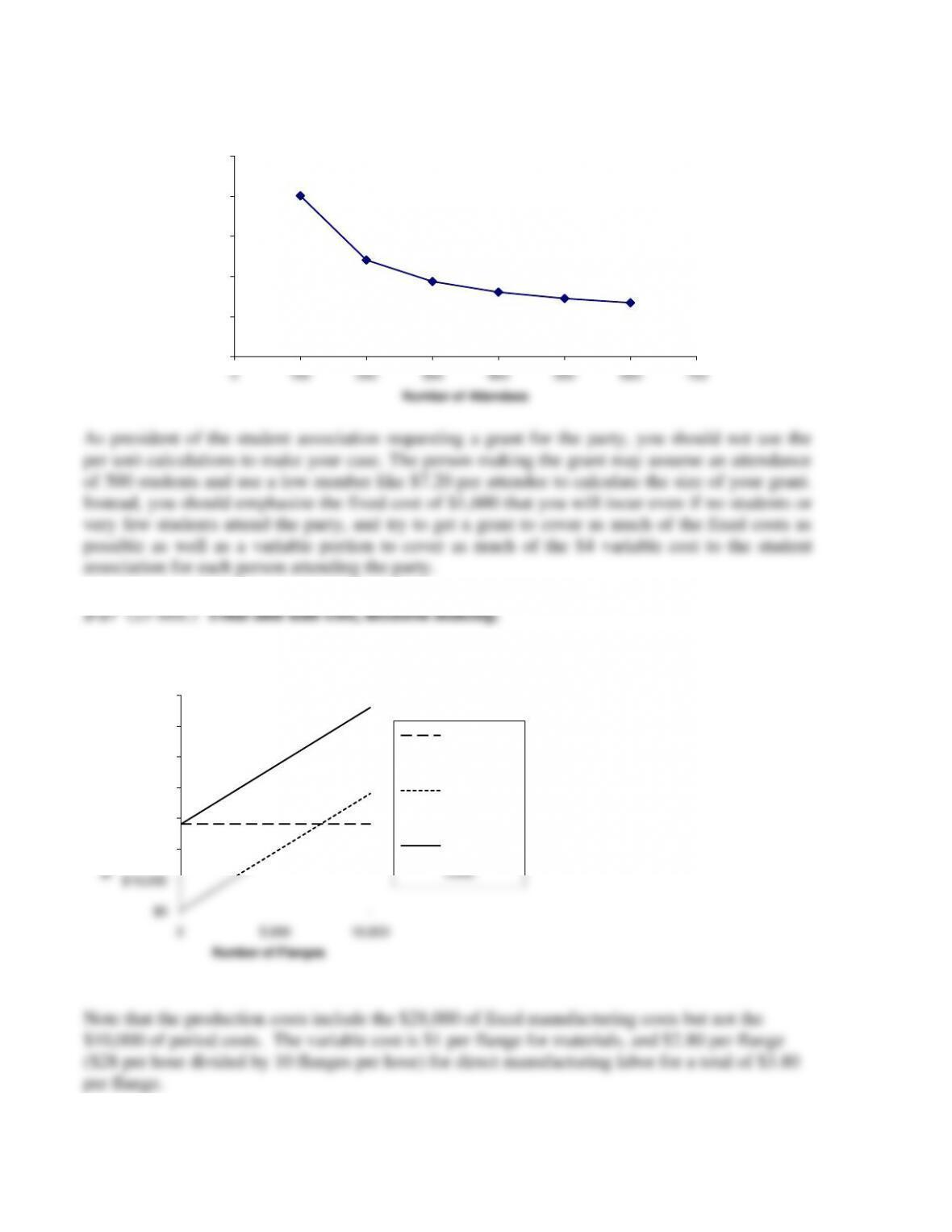

4. Using the calculations shown in the table in requirement 2, we can construct the cost-per-

attendee graph shown below:

0

5

10

15

20

25

0100 200 300 400 500 600 700

Number of Attendees

Cost per Attendee ($)

1.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

0

5,000

10,000

Total Manufacturing Costs

Number of Flanges

Fixed Costs

Variable Costs

Total

Manufacturing

Costs

Note that the production costs include the $28,000 of fixed manufacturing costs but not the

$10,000 of period costs. The variable cost is $1 per flange for materials, and $2.80 per flange

($28 per hour divided by 10 flanges per hour) for direct manufacturing labor for a total of $3.80

per flange.

2-13

$3.80 × 5,000 + $28,000 = $47,000

Average (unit) cost = $47,000 ÷ 5,000 units = $9.40 per unit.

This is below Flora’s selling price of $10 per flange. However, in order to make a profit,

Gayle’s Glassworks also needs to cover the period (non-manufacturing) costs of $10,000, or

3. If Gayle’s Glassworks produces 10,000 units, then total inventoriable cost will be:

Variable cost ($3.80 × 10,000) + fixed manufacturing costs, $28,000 = total manufacturing

costs, $66,000.

Average (unit) inventoriable (manufacturing) cost will be $66,000 ÷ 10,000 units = $6.60 per flange

Unit total cost including both inventoriable and period costs will be

2-14

1. Manufacturing–sector companies purchase materials and components and convert them

into different finished goods.

2. Inventoriable costs are all costs of a product that are regarded as an asset when they are

incurred and then become cost of goods sold when the product is sold. These costs for a

3. (a) Perrier mineral water purchased for resale by Safeway—inventoriable cost of a

merchandising company. It becomes part of cost of goods sold when the mineral water is sold.

(b) Electricity used for lighting at GE refrigerator assembly plant—inventoriable cost of

a manufacturing company. It is part of the manufacturing overhead that is included in the

manufacturing cost of a refrigerator finished good.

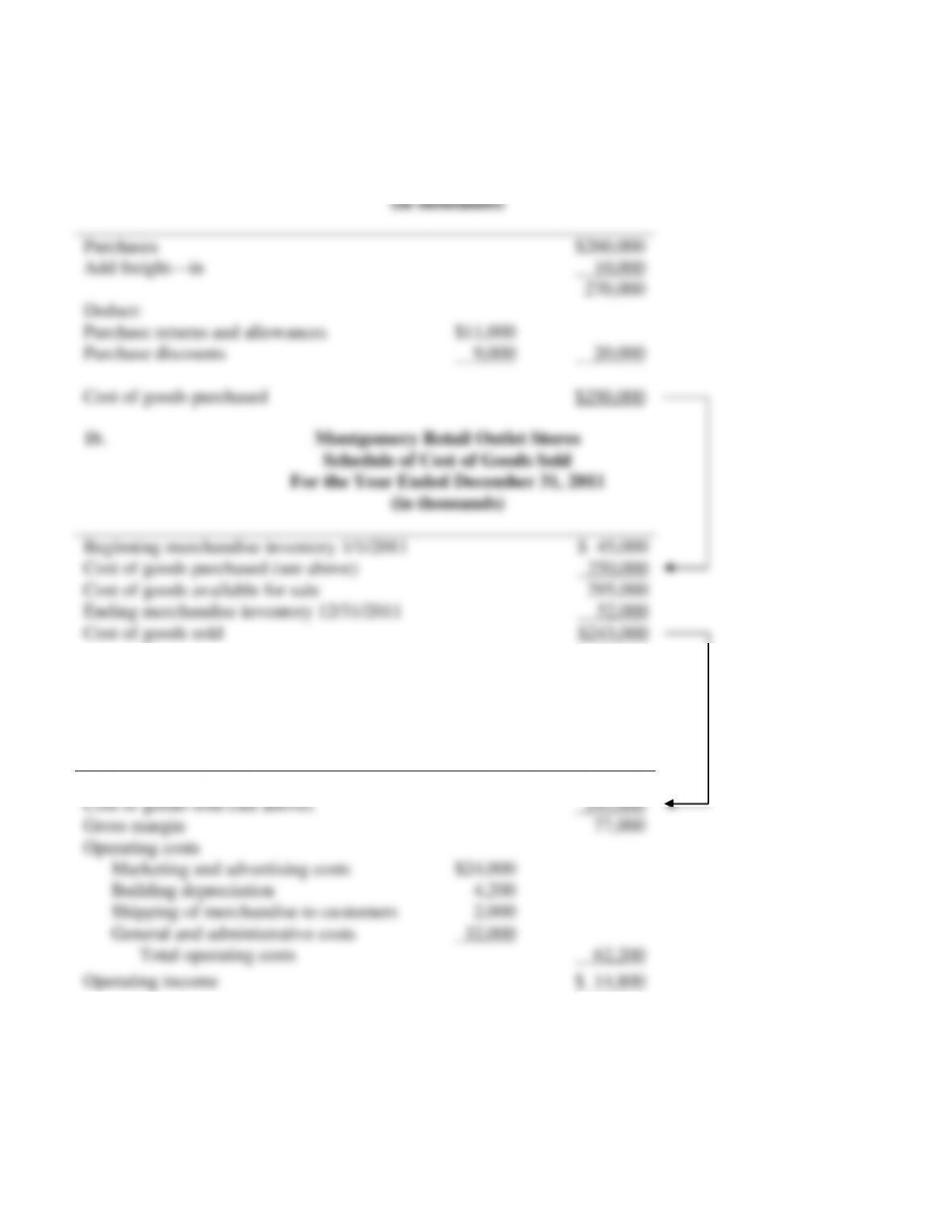

2-29 (20 min.) Computing cost of goods purchased and cost of goods sold.

1a. Marvin Department Store

Schedule of Cost of Goods Purchased

For the Year Ended December 31, 2011

2-30 (20 min.) Cost of goods purchased, cost of goods sold, and income statement.

1a. Montgomery Retail Outlet Stores

Schedule of Cost of Goods Purchased

For the Year Ended December 31, 2011

2-17

1.

Direct materials inventory 10/1/2011 $ 105

Direct materials purchased 365

2.

Total manufacturing overhead costs $ 450

3.

Total manufacturing costs $ 1,610

4.

Work–in–process inventory 10/1/2011 $ 230

Total manufacturing costs 1,610

5.

Finished goods inventory 10/1/2011 $ 130

6.

Finished goods available for sale in October 2011

2-18

1. Canseco Company

Schedule of Cost of Goods Manufactured

Year Ended December 31, 2011

(in thousands)

Direct materials cost

2. Canseco Company

Income Statement

Year Ended December 31, 2011

(in thousands)

2-19

2-33 (30–40 min.) Cost of goods manufactured, income statement, manufacturing

company.

Piedmont Corporation

Schedule of Cost of Goods Manufactured

Year Ended December 31, 2011

(in thousands)

Plant insurance 2,000

Depreciation—plant building & equipment 21,000

Plant utilities 12,000

Repairs and maintenance—plant 8,000

Equipment lease costs 32,000

Revenues $600,000

Cost of goods sold:

Beginning finished goods, January 1, 2011 $123,000

Cost of goods manufactured 413,000

Cost of goods available for sale 536,000

2-20

2-34 (25–30 min.) Income statement and schedule of cost of goods manufactured.

Howell Corporation

Income Statement for the Year Ended December 31, 2011

(in millions)

Revenues $950

for the Year Ended December 31, 2011

(in millions)

Direct materials costs

Beginning inventory, Jan. 1, 2011 $ 15

Purchases of direct materials 325

Miscellaneous plant overhead 35 220

Manufacturing costs incurred during 2011 640

Add beginning work–in–process inventory, Jan. 1, 2011 10

Total manufacturing costs to account for 650

Deduct ending work-in-process, Dec. 31, 2011 5