22-1

CHAPTER 22

22-1 A management control system is a means of gathering and using information to aid and

22-2 To be effective, management control systems should be (a) closely aligned to an

22-3 Motivation combines goal congruence and effort. Motivation is the desire to attain a

1. Creates greater responsiveness to local needs

3. Increases motivation of subunit managers

5. Sharpens the focus of subunit managers

The chapter cites four costs of decentralization:

2. Focuses managers’ attention on the subunit rather than the company as a whole

4. Results in duplication of activities

22-5 No. Organizations typically compare the benefits and costs of decentralization on a

22-6 No. A transfer price is the price one subunit of an organization charges for a product or

service supplied to another subunit of the same organization. The two segments can be cost

1. Market-based transfer prices

3. Hybrid transfer prices

22-2

22-8 Transfer prices should have the following properties. They should

2. be useful for evaluating subunit performance,

4. preserve a high level of subunit autonomy in decision making.

22-10 Transferring products or services at market prices generally leads to optimal decisions

when (a) the market for the intermediate product market is perfectly competitive, (b)

22-11 One potential limitation of full-cost-based transfer prices is that they can lead to

suboptimal decisions for the company as a whole. An example of a conflict between divisional

action and overall company profitability resulting from an inappropriate transfer-pricing policy is

buying products or services outside the company when it is beneficial to overall company

22-12 Reasons why a dual-pricing approach to transfer pricing is not widely used in practice

include:

2. This approach does not provide clear signals to division managers about the level of

decentralization top management wants.

4. It leads to problems in computing the taxable income of subunits located in different tax

jurisdictions.

22-13 Disagree. Cost and price information are often useful starting points in the negotiation

process. Costs, particularly variable costs of the selling division, serve as a “floor” below which

22-3

22-14 Yes. The general transfer-pricing guideline specifies that the minimum transfer price

equals the incremental cost per unit incurred up to the point of transfer plus the opportunity cost

22-15 Alternative transfer-pricing methods can result in sizable differences in the reported

22-16 (15 min.) Evaluating management control systems, balanced scorecard.

1. Correct answers may include any of the following:

Financial perspective – stock price, net income, return on investment, cash flow from operations,

cost per visitor, gross margin percentage in retail venues

2. Each manager would be concerned with management controls related specifically to

their level of responsibility. Within the financial perspective, for example, the souvenir shop

22-4

22-17 (25 min.) Cost centers, profit centers, decentralization.

1. The Glass Department sends its product to the Wood and Metal Departments for

3. A centralized department can be a profit center. Centralization relates to the degree of

autonomy that a department has for decision making. This concept is independent of the

4. a) With these changes, Fenster will be moving toward a more decentralized environment

because each department will have more local decision-making authority, such as the

22-5

1. Health Source has a centralized structure. Individual managers have little autonomy in

decision-making.

2. Harvest Moon has a decentralized structure. Store managers have significant autonomy.

They are able to customize product offerings, negotiate purchases with local farmers, and can

even influence store expansion decisions.

3. The stores in the Health Source chain would be considered profit centers. Store

managers are responsible for store revenues and costs, and as such, would be evaluated based on

4. Jackson must be attentive to the fact that Harvest Moon managers have enjoyed

significant freedom to make decisions about their own stores. Jackson will need to carefully

22-6

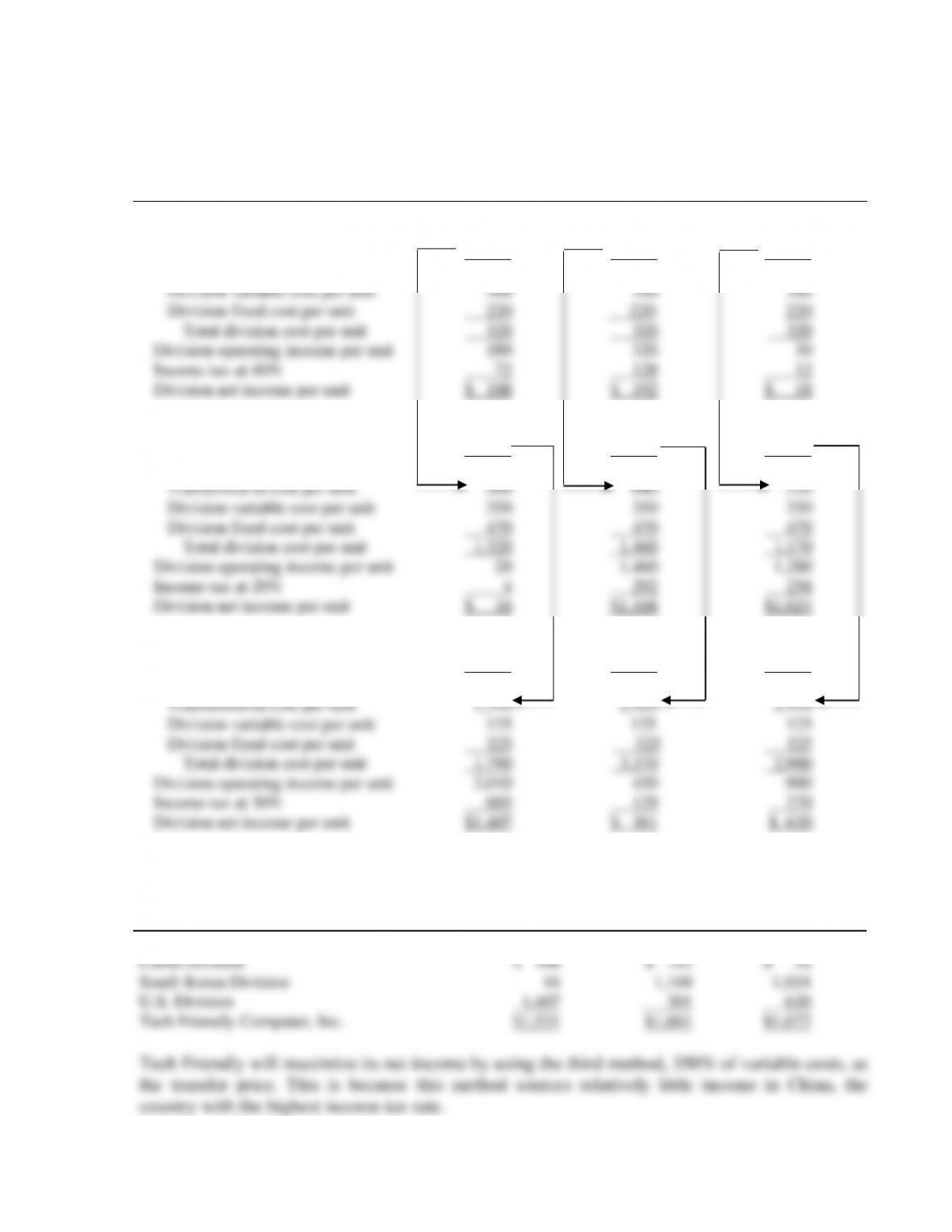

22-19 (35 min.) Multinational transfer pricing, effect of alternative transfer-pricing

methods, global income tax minimization.

1. This is a three-country, three-division transfer-pricing problem with three alternative

transfer-pricing methods. Summary data in U.S. dollars are:

China Plant

Variable costs: 900 Yuan ÷ 9 Yuan per $ = $100 per subunit

Fixed costs: 1,980 Yuan ÷ 9 Yuan per $ = $220 per subunit

2.0 ($640 + $350 + $470) = $2,920 per unit

3.5 $100 = $350 per subunit

• South Korea to U.S. Plant

Method A

Method B

Method C

Internal

Transfers

at Market

Price

Internal

Transfers

at 200% of

Full Costs

Internal

Transfers

at 350% of

Variable Costs

1. China Division

Division revenue per unit

Cost per unit:

Division variable cost per unit

Division fixed cost per unit

Total division cost per unit

Division operating income per unit

Income tax at 40%

Division net income per unit

2. South Korea Division

Division revenue per unit

Cost per unit:

Transferred-in cost per unit

Division variable cost per unit

Division fixed cost per unit

Total division cost per unit

Division operating income per unit

Income tax at 20%

Division net income per unit

3. United States Division

Division revenue per unit

Division operating income per unit

Income tax at 30%

Division net income per unit

$ 500

100

220

320

180

72

$ 108

$1,340

500

350

470

1,320

20

4

$ 16

$3,800

2,010

603

$1,407

$ 640

100

220

320

320

128

$ 192

$2,920

640

350

470

1,460

1,460

292

$1,168

$3,800

430

129

$ 301

$ 350

100

220

320

30

12

$ 18

$2,450

350

350

470

1,170

1,280

256

$1,024

$3,800

900

270

$ 630

U.S. Division

Tech Friendly Computer, Inc.

1,407

$1,531

301

$1,661

630

$1,672

Tech Friendly will maximize its net income by using the third method, 350% of variable costs, as

22-20 (30 min.) Transfer-pricing methods, goal congruence.

1. Alternative 1: Sell as raw lumber for $200 per 100 board feet:

Revenue $200

Variable costs 100

Contribution margin $100 per 100 board feet

2. Transfer price at 110% of variable costs:

= $100 + ($100 0.10)

= $110 per 100 board feet

Sell as

Raw Lumber

Sell as

Finished Lumber

Raw Lumber Division

Division revenues

Division variable costs

Division operating income

Finished Lumber Division

Division revenues

Transferred-in costs

Division variable costs

Division operating income

$200

100

$100

$ 0

—

$ 0

$110

100

$ 10

$275

110

125

$ 40

The Raw Lumber Division will maximize reported division operating income by selling

raw lumber, which is the action preferred by the company as a whole. The Finished Lumber

3. Transfer price at market price = $200 per 100 board feet.

Sell as

Raw Lumber

Sell as

Finished Lumber

Raw Lumber Division

Division revenues

Division variable costs

Division operating income

Finished Lumber Division

Division revenues

Transferred-in costs

Division variable costs

Division operating income

$200

100

$100

$ 0

—

—

$ 0

$200

100

$100

$275

200

125

$ (50)

Since the Raw Lumber Division will be indifferent between selling the lumber in raw or finished

form, it would be willing to maximize division operating income by selling raw lumber, which is

the action preferred by the company as a whole. The Finished Lumber Division will maximize

division operating income by not further processing raw lumber and this is preferred by the

company as a whole. Thus, transfer at market price will result in division actions that are also in

the best interest of the company as a whole.

22-10

22-21 (30 min.) Effect of alternative transfer-pricing methods on division operating income.

Method A

Internal Transfers

at Market Prices

Method B

Internal Transfers at

110% of Full Costs

1. Mining Division

Revenues:

$90, $661 200,000 units

$18,000,000

$13,200,000

Costs:

Division variable costs:

$522 200,000 units

10,400,000

10,400,000

Division fixed costs:

$83 200,000 units

1,600,000

1,600,000

Total division costs

12,000,000

12,000,000

Division operating income

$ 6,000,000

$ 1,200,000

Metals Division

Revenues:

$150 200,000 units

$30,000,000

$30,000,000

Costs:

Transferred-in costs:

$90, $66 200,000 units

18,000,000

13,200,000

Division variable costs:

$364 200,000 units

7,200,000

7,200,000

Division fixed costs:

$155 200,000 units

3,000,000

3,000,000

Total division costs

28,200,000

23,400,000

Division operating income

$ 1,800,000

$ 6,600,000

1$66 = Full manufacturing cost per unit in the Mining Division, $60 110%

2Variable cost per unit in Mining Division = Direct materials + Direct manufacturing labor + 75% of manufacturing

overhead = $12 + $16 + (75% $32) = $52

3Fixed cost per unit = 25% of manufacturing overhead = 25% $32 = $8

4Variable cost per unit in Metals Division = Direct materials + Direct manufacturing labor + 40% of manufacturing

overhead = $6 + $20 + (40% $25) = $36

5Fixed cost per unit in Metals Division = 60% of manufacturing overhead = 60% $25 = $15