3-1

CHAPTER 3

COST-VOLUME-PROFIT ANALYSIS

3-1 Cost-volume-profit (CVP) analysis examines the behavior of total revenues, total costs,

3-2 The assumptions underlying the CVP analysis outlined in Chapter 3 are

2. Total costs can be separated into a fixed component that does not vary with the units sold

and a variable component that changes with respect to the units sold.

period.

4. The selling price, variable cost per unit, and fixed costs are known and constant.

3-3 Operating income is total revenues from operations for the accounting period minus cost

of goods sold and operating costs (excluding income taxes):

3-4 Contribution margin is the difference between total revenues and total variable costs.

3-5 Three methods to express CVP relationships are the equation method, the contribution

3-2

3-6 Breakeven analysis denotes the study of the breakeven point, which is often only an

3-7 CVP certainly is simple, with its assumption of output as the only revenue and cost

driver, and linear revenue and cost relationships. Whether these assumptions make it simplistic

expanded.

3-8 An increase in the income tax rate does not affect the breakeven point. Operating income

at the breakeven point is zero, and no income taxes are paid at this point.

3-9 Sensitivity analysis is a “what–if” technique that managers use to examine how an

outcome will change if the original predicted data are not achieved or if an underlying

3-10 Examples include:

Manufacturing––substituting a robotic machine for hourly wage workers.

3-11 Examples include:

Manufacturing––subcontracting a component to a supplier on a per-unit basis to avoid

3-12 Operating leverage describes the effects that fixed costs have on changes in operating

3-13 CVP analysis is always conducted for a specified time horizon. One extreme is a very

variable.

3-3

CVP itself is not made any less relevant when the time horizon lengthens. What happens

3-15 Yes, gross margin calculations emphasize the distinction between manufacturing and

nonmanufacturing costs (gross margins are calculated after subtracting variable and fixed

3-16 (10 min.) CVP computations.

Variable

Fixed

Total

Operating

Contribution

Contribution

Revenues

Costs

Costs

Costs

Income

Margin

Margin %

a.

$2,000

$ 500

$300

$ 800

$1,200

$1,500

75.0%

b.

2,000

1,500

300

1,800

200

500

25.0%

c.

1,000

700

300

1,000

0

300

30.0%

d.

1,500

900

300

1,200

300

600

40.0%

3-17 (10–15 min.) CVP computations.

1a. Sales ($68 per unit × 410,000 units) $27,880,000

Variable costs ($60 per unit × 410,000 units) 24,600,000

Contribution margin $ 3,280,000

3. Operating income is expected to decrease by $1,230,000 ($1,640,000 − $410,000) if Ms.

Schoenen’s proposal is accepted.

3-18 (35–40 min.) CVP analysis, changing revenues and costs.

1a. SP = 6% × $1,500 = $90 per ticket

VCU = $43 per ticket

CMU = $90 – $43 = $47 per ticket

FC = $23,500 a month

Q =

CMU

FC

=

per ticket $47

$23,500

per ticket $47

$40,500

CMU

FC

per ticket $50

$23,500

per ticket $50

$40,500

CMU

FC

3-5

3b. Q =

CMU

TOI FC +

=

per ticket $20

$17,000 $23,500+

=

per ticket $20

$40,500

= 2,025 tickets

CMU

per ticket $25

TOI FC +

$17,000 $23,500+

3-6

3-19 (20 min.) CVP exercises.

Revenues

Variable

Costs

Contribution

Margin

Fixed

Costs

Budgeted

Operating

Income

Orig.

$10,000,000G

$8,000,000G

$2,000,000

$1,800,000G

$200,000

1.

10,000,000

7,800,000

2,200,000a

1,800,000

400,000

2.

10,000,000

8,200,000

1,800,000b

1,800,000

0

3.

10,000,000

8,000,000

2,000,000

1,890,000c

110,000

4.

10,000,000

8,000,000

2,000,000

1,710,000d

290,000

5.

10,800,000e

8,640,000f

2,160,000

1,800,000

360,000

6.

9,200,000g

7,360,000h

1,840,000

1,800,000

40,000

7.

11,000,000i

8,800,000j

2,200,000

1,980,000k

220,000

8.

10,000,000

7,600,000l

2,400,000

1,890,000m

510,000

Gstands for given.

3-20 (20 min.) CVP exercises.

1a. [Units sold (Selling price – Variable costs)] – Fixed costs = Operating income

[5,000,000 ($0.50 – $0.30)] – $900,000 = $100,000

price Selling

=

$0.50

$0.30 – $0.50

= 0.40

2.

5,000,000 ($0.50 – $0.34) – $900,000

=

$ (100,000)

3.

[5,000,000 (1.1) ($0.50 – $0.30)] – [$900,000 (1.1)]

=

$ 110,000

4.

[5,000,000 (1.4) ($0.40 – $0.27)] – [$900,000 (0.8)]

=

$ 190,000

5.

$900,000 (1.1) ÷ ($0.50 – $0.30)

=

4,950,000 units

6.

($900,000 + $20,000) ÷ ($0.55 – $0.30)

=

3,680,000 units

3-7

3-21 (10 min.) CVP analysis, income taxes.

1. Monthly fixed costs = $48,200 + $68,000 + $13,000 = $129,200

Contribution margin per unit = $27,000 – $23,000 – $600 = $ 3,400

Monthly fixed costs

Contribution margin per unit

$129,200

$3,400 per car

2. Tax rate 40%

Target net income $51,000

Target net income $51,000 $51,000

1 – tax rate (1 0.40) 0.60

−

Quantity of output units

required to be sold

=

Fixed costs + Target operating income $129,200 $85,000

Contribution margin per unit $3,400

+

==

63 cars

1. Variable cost percentage is $3.40 $8.50 = 40%

30.01

−

0.60R = $459,000 + $153,000

R = $612,000 0.60

R = $1,020,000

Fixed costs + Target operating income

Target net income $107,100

Fixed costs + $459,000

1 Tax rate 1 0.30

Target revenues $1,020,000

Contribution margin percentage 0.60

+

−−

= = =

Proof: Revenues $1,020,000

Variable costs (at 40%) 408,000

Contribution margin 612,000

Fixed costs 459,000

Operating income 153,000

Income taxes (at 30%) 45,900

Net income $ 107,100

2.a. Customers needed to break even:

Contribution margin per customer = $8.50 – $3.40 = $5.10

3-8

2.b. Customers needed to earn net income of $107,100:

3. Using the shortcut approach:

Change in net income =

( )

Change in Unit

number of contribution 1 Tax rate

customers margin

−

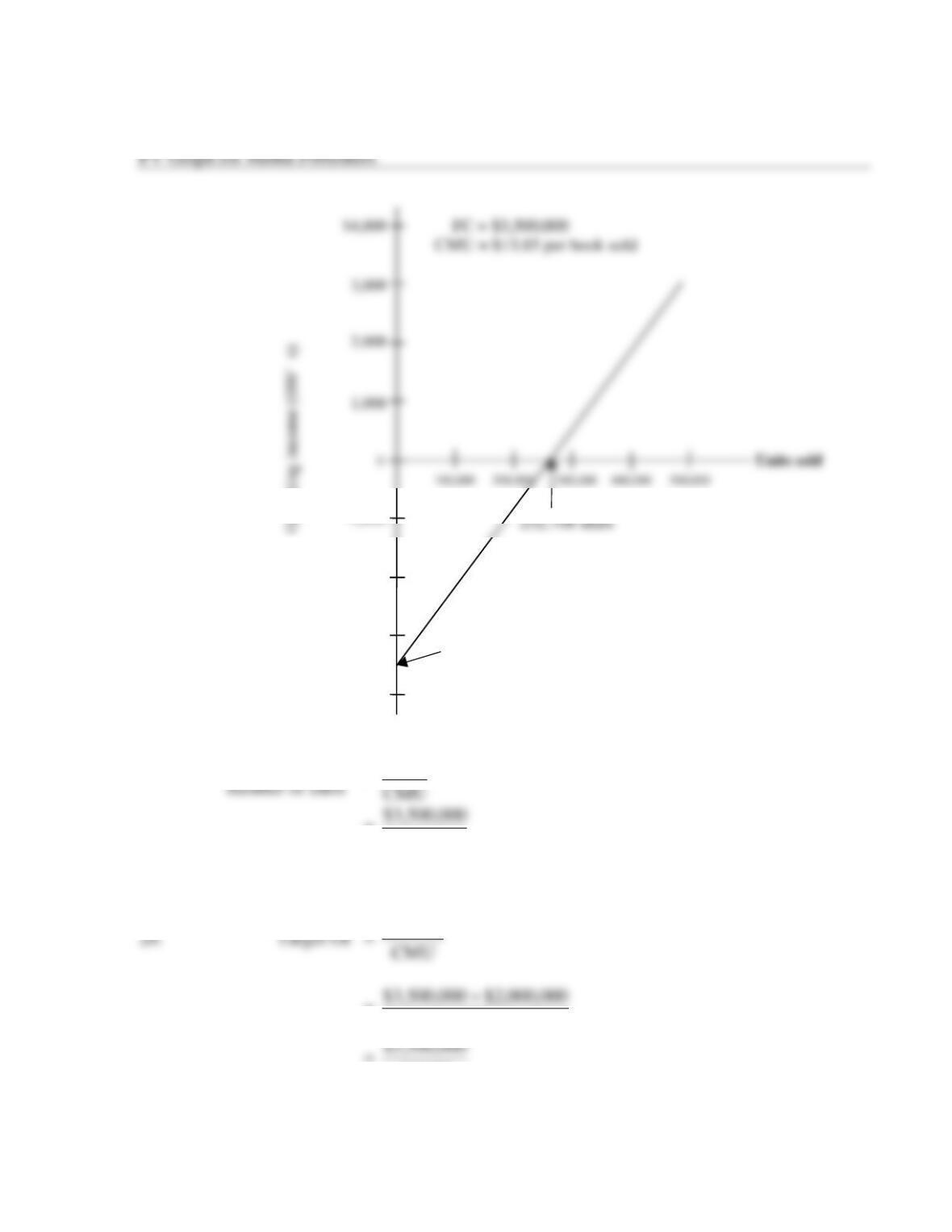

3-23 (30 min.) CVP analysis, sensitivity analysis.

1. SP = $30.00 (1 – 0.30 margin to bookstore)

3.15 variable author royalty cost (0.15 $21.00)

$ 7.15

Solution Exhibit 3-23A shows the PV graph.

SOLUTION EXHIBIT 3-23A

$4,000

3,000

2,000

1,000

2a.

Breakeven

FC

$3.5 million

252,708 units

-1,000

-2,000

-3,000

-4,000

100,000

200,000

300,000

400,000

500,000

3-10

3a. Decreasing the normal bookstore margin to 20% of the listed bookstore price of $30 has the

following effects:

SP = $30.00 (1 – 0.20)

$16.40

= 213,415 copies sold (rounded up)

The breakeven point decreases from 252,708 copies in requirement 2 to 213,415 copies.

3b. Increasing the listed bookstore price to $40 while keeping the bookstore margin at 30%

has the following effects:

$19.80

= 176,768 copies sold (rounded up)

The breakeven point decreases from 252,708 copies in requirement 2 to 176,768 copies.