7-31

2.

Direct Materials Price Variance (time of purchase = time of use)

Direct Materials Control

10,640

Direct Materials Price Variance

304

Accounts Payable Control or Cash

10,336

Direct Materials Efficiency Variance

Work in Process Control

9,870

Direct Materials Efficiency Variance

770

Direct Materials Control

10,640

Direct Manufacturing Labor Variances

Work in Process Control

9,400

Direct Mfg. Labor Price Variance

370

Direct Mfg. Labor Efficiency Variance

150

Wages Payable or Cash

9,620

3. Plausible explanations for the above variances include:

Shayna paid a little less for the wool, but the wool was lower quality (more knots in the yarn that

7-32

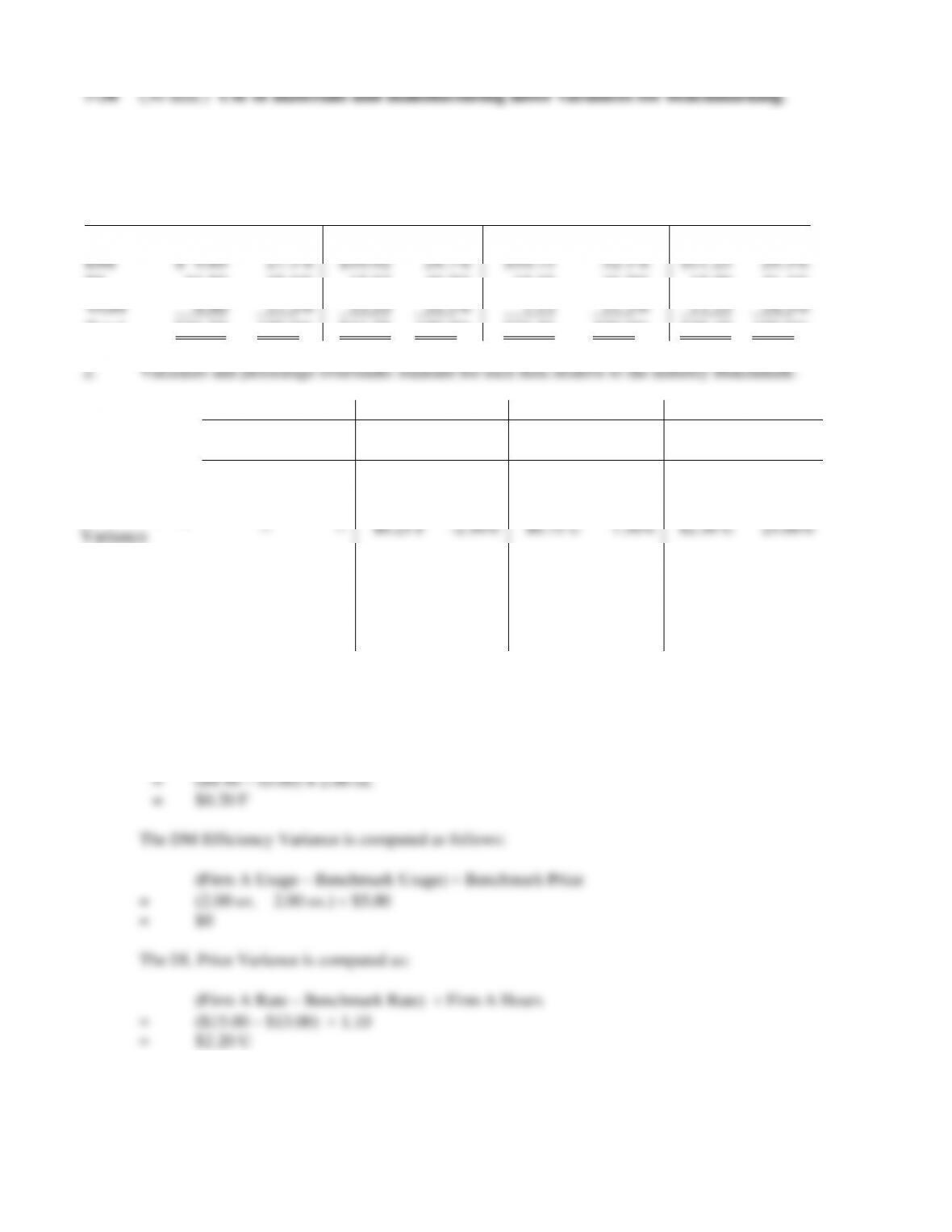

1. Unit variable cost (dollars) and component percentages for each firm:

Firm A

Firm B

Firm C

Firm D

DM

$ 9.80

27.1%

$10.92

24.7%

$10.75

32.1%

$11.25

29.3%

DL

16.50

45.6%

17.83

40.2%

15.68

46.7%

15.90

41.4%

VOH

9.90

27.3%

15.53

35.1%

7.13

21.2%

11.25

29.3%

Total

$36.20

100.0%

$44.28

100.0%

$33.56

100.0%

$38.40

100.0%

Firm A

Firm B

Firm C

Firm D

Variance

% over

standard

Variance

% over

standard

Variance

% over

standard

Variance

% over

standard

DM Price

Variance

$0.20 F

-2.00%

$1.17 U

12.00%

—

—

$1.25 F

-10.00%

DM Efficiency

Variance

—

—

$0.25 F

-2.50%

$0.75 U

7.50%

$2.50 U

25.00%

DL Price

Variance

$2.20 U

15.38%

$2.88 U

19.23%

$3.33 U

26.92%

$2.90 U

22.31%

DL Efficiency

Variance

$1.30 U

10.00%

$1.95 U

15.00%

$0.65 F

-5.00%

—

—

We illustrate these calculations for Firm A.

The DM Price Variance is computed as:

(Firm A Price – Benchmark Price) × Firm A Usage

7-33

The DL Efficiency Variance is computed as follows:

(Firm A Usage – Benchmark Usage) Benchmark Rate

= (1.10 hrs. – 1.00 hrs.) $13.00

3.

To: Boss

From: Junior Accountant

Re: Benchmarking & productivity improvements

Date: March 15, 2011

Benchmarking advantages

7-34

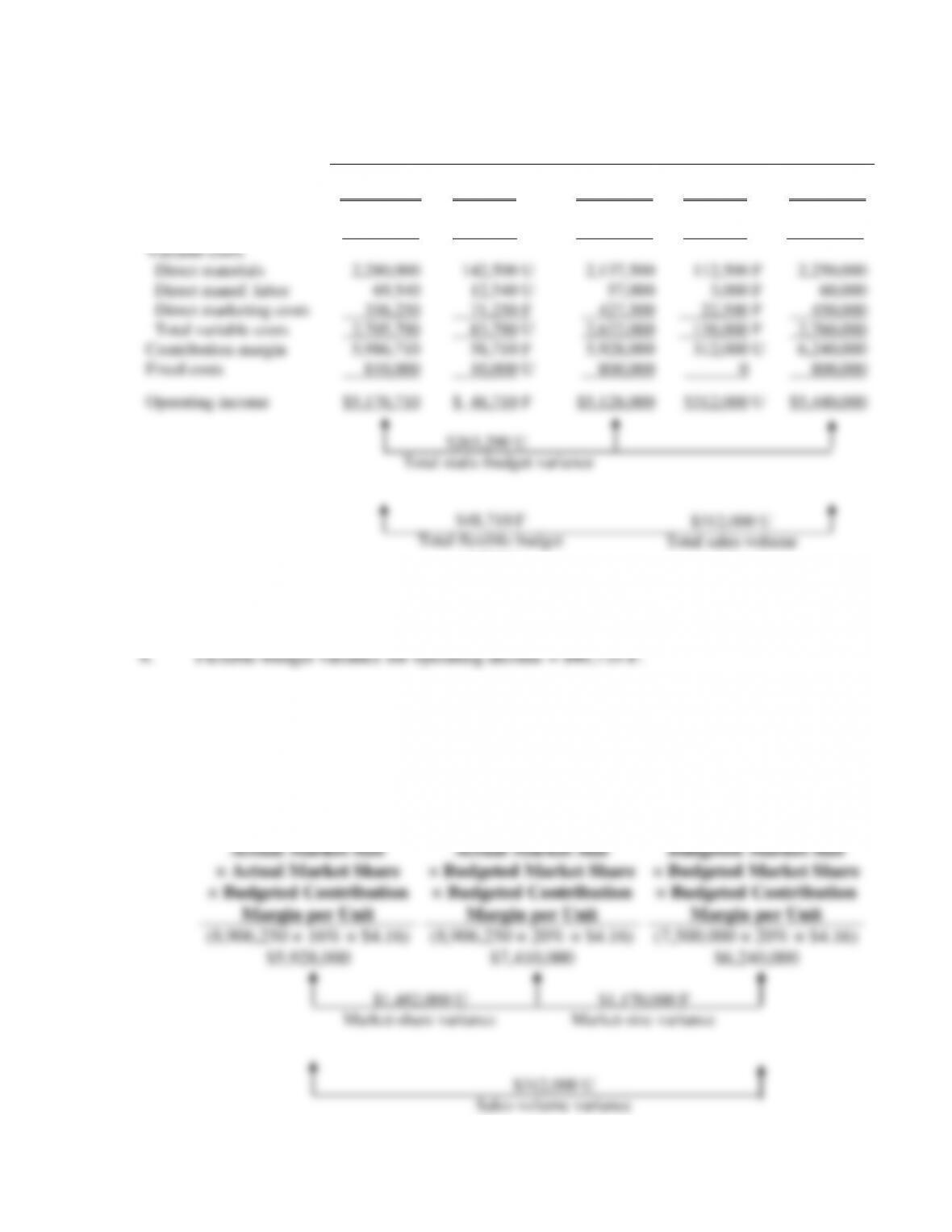

7-39 (60 min.) Comprehensive variance analysis review.

Actual Results

Units sold (95% × 1,500,000) 1,425,000

Selling price per unit $ 6.10

Revenues (1,425,000 × $6.10) $8,692,500

Total direct marketing costs (1,425,000 × $0.25) $ 356,250

Fixed overhead costs ($800,000 + $10,000) $ 810,000

Static Budgeted Amounts

Units sold 1,500,000

Selling price per unit $ 6.00

1. Actual Static-Budget

Results Amounts

Revenues $8,692,500 $9,000,000

2. Actual operating income $5,176,710

Flexible-budget-based variance analysis for Sonnet, Inc. for March 2011

Actual

Results

Flexible-Budget

Variances

Flexible

Budget

Sales-

Volume

Variances

Static

Budget

Units (diskettes) sold

1,425,000

0

1,425,000

75,000

1,500,000

Revenues

Variable costs

Direct materials

Direct manuf. labor

Direct marketing costs

Total variable costs

$8,692,500

2,280,000

69,540

356,250

2,705,790

$142,500 F

142,500 U

12,540 U

71,250 F

83,790 U

$8,550,000

2,137,500

57,000

427,500

2,622,000

$450,000 U

112,500 F

3,000 F

22,500 F

138,000 F

$9,000,000

2,250,000

60,000

450,000

2,760,000

Contribution margin

5,986,710

58,710 F

5,928,000

312,000 U

6,240,000

Fixed costs

810,000

10,000 U

800,000

0

800,000

Operating income

$5,176,710

$ 48,710 F

$5,128,000

$312,000 U

$5,440,000

3. Flexible-budget operating income = $5,128,000.

5. Sales-volume variance for operating income = $312,000 U.

6. Budgeted market share = 1,500,000 ÷ 7,500,000 = 20%

Actual market share = 1,425,000 ÷ 8,906,250 = 16%

Budgeted contribution margin per unit = $6,240,000 ÷ 1,500,000 = $4.16 per unit

Actual Market Size

× Actual Market Share

× Budgeted Contribution

Margin per Unit

Actual Market Size

× Budgeted Market Share

× Budgeted Contribution

Margin per Unit

Static Budget:

Budgeted Market Size

× Budgeted Market Share

× Budgeted Contribution

Margin per Unit

(8,906,250 × 16% × $4.16)

$5,928,000

(8,906,250 × 20% × $4.16)

$7,410,000

(7,500,000 × 20% × $4.16)

$6,240,000

$1,482,000 U $1,170,000 F

Market-share variance Market-size variance

$312,000 U

Total sales-volume

variance

$48,710 F

Total flexible-budget

variance

$263,290 U

Total static-budget variance

$312,000 U

Sales-volume variance

7-36

Analysis of direct mfg. labor flexible-budget variance for Sonnet, Inc. for March 2011

Actual Costs

Incurred

(Actual Input

Quantity

× Actual Price)

Actual Input

Quantity

× Budgeted Price

Flexible Budget

(Budgeted Input

Quantity Allowed

for Actual Output

× Budgeted Price)

Direct.

Mfg. Labor

(5,700 × $12.20)

$69,540

(5,700 × $12.00)

$68,400

(*4,750 × $12.00)

$57,000

$1,140 U $11,400 U

Price variance Efficiency variance

* 1,425,000 units ÷ 300 direct manufacturing labor standard productivity rate per hour.

8. DML flexible-budget variance = $12,540U

$12,540 U

Flexible-budget variance