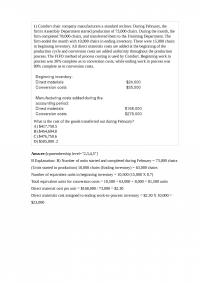

Archives

978-0133428704 Chapter 1 Solution Manual Part 1

1- 1 CHAPTER 1 THE MANAGER AND MANAGEMENT ACCOUNTING See the front matter of this Solutions Manual for suggestions regarding your choices of assignment material for each chapter. 1-1 Management accounting measures, analyzes, and reports financial and nonfinancial information that […]

978-0133428704 Chapter 1 Solution Manual Part 2

1-27 (15 min.) Planning and control decisions, Internet company. PostNews.com offers its subscribers several services, such as an annotated TV guide and local– area information on weather, restaurants, and movie theaters. Its main revenue sources are fees for banner advertisements […]

978-0133428704 Chapter 10 Solution Manual Part 1

10-1 CHAPTER 10 DETERMINING HOW COSTS BEHAVE 10-1 The two assumptions are 1. Variations in the level of a single activity (the cost driver) explain the variations in the related total costs. 2. Cost behavior is approximated by a linear […]

978-0133428704 Chapter 10 Solution Manual Part 2

10-1 SOLUTION 1. Manufacturing cost classification for 2014: Account Total Costs (1) % of Total Costs That is Variable (2) Variable Costs (3) = (1) (2) Fixed Costs (4) = (1) – (3) Variable Cost per Unit (5) = […]

978-0133428704 Chapter 10 Solution Manual Part 3

10-1 SOLUTION 1. Solution Exhibit 10-26 plots the relationship between labor-hours and overhead costs and shows the regression line. y = $96,541 + $3.93 X Economic plausibility. Labor-hours appears to be an economically plausible driver of overhead costs for a […]

978-0133428704 Chapter 10 Solution Manual Part 4

10-1 SOLUTION EXHIBIT 10-30 Plot and High-Low Line of Maintenance Costs as a Function of Machine-Hours $100,000 $120,000 $140,000 $160,000 $180,000 $200,000 $220,000 $240,000 $260,000 $280,000 $300,000 90,000 100,000 110,000 120,000 130,000 140,000 150,000 Maintenance Costs Machine-Hours 10-2 Solution Exhibit […]

978-0133428704 Chapter 10 Solution Manual Part 5

10-1 Inspection costs using units inspected = $98.79 + ($2.02 × 1,500) = $3,128.79 Inspection costs using inspection labor-hours = $3.89 + ($20.06 × 160) = $3,213.49 If Sharon uses inspection-labor-hours she will estimate inspection costs to be $3,213.49, $84.70 […]

978-0133428704 Chapter 10 Solution Manual Part 6

10-1 SOLUTION 1. Cost to produce the second through the seventh boats: Direct materials, 6 $201,000 $1,206,000 Direct manufacturing labor (DML), 76,0621 $43 3,270,666 Variable manufacturing overhead, 76,062 $24 1,825,4888 Other manufacturing overhead, 15% of DML costs […]

978-0133428704 Chapter 10 Solution Manual Part 7

3. Multicollinearity is an issue that can arise with multiple regression but not simple regression analysis. Multicollinearity means that the independent variables are highly correlated. The correlation feature in Excel’s Data Analysis reveals a coefficient of correlation of 0.61 between […]

978-0133428704 Chapter 10 Solution Manual Part 8

3. Here is the summary output for the regression of monthly Sales Revenue on the prior month’s Online Advertising Expense: SUMMARY OUTPUT Regression Statistics Multiple R 0.808588 R Square 0.653815 Adjusted R Square 0.61535 Standard Error 7393.922 Observations 11 ANOVA […]

978-0133428704 Chapter 11 Solution Manual Part 1

11- 1 CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION 11-1 The five steps in the decision process outlined in Exhibit 11-1 of the text are 1. Identify the problem and uncertainties. 2. Obtain information. 3. Make predictions about the future. […]

978-0133428704 Chapter 11 Solution Manual Part 2

11-21 (10 min.) Inventory decision, opportunity costs. Best Trim, a manufacturer of lawn mowers, predicts that it will purchase 204,000 spark plugs next year. Best Trim estimates that 17,000 spark plugs will be required each month. A supplier quotes a […]

978-0133428704 Chapter 11 Solution Manual Part 3

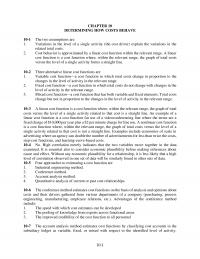

11-1 11-27 (20 min.) Relevance of equipment costs. Papa’s Pizza is considering replacement of its pizza oven with a new, more energy-efficient model. Information related to the old and new pizza ovens follows: The old oven had been purchased a […]

978-0133428704 Chapter 11 Solution Manual Part 4

11-1 SOLUTION 1. Easyspread 2.0 has a higher relevant operating income than Easyspread 1.0. Based on this analysis, Easyspread 2.0 should be introduced immediately: Easyspread 1.0 Easyspread 2.0 Relevant revenues $165 $215 Relevant costs: Manuals, diskettes, compact discs $ 0 […]

978-0133428704 Chapter 11 Solution Manual Part 5

SOLUTION 1. 11-1 A110 B382 C657 Selling price $168 $ 112 $140 Variable costs: Direct materials (DM) 48 30 18 Labor and other costs 56 54 80 Total variable costs 104 84 98 Contribution margin $ 64 $ 28 $ […]

978-0133428704 Chapter 11 Solution Manual Part 6

SOLUTION 1. and 2. Division A Division B Sales $504,000 $948,000 Variable costs of goods sold ($440,000 0.90; $930,000 0.80) 396,000 744,000 Variable S,G & A ($96,000 0.50; $202,500 0.50) 48,000 101,250 Total variable costs 444,000 […]

978-0133428704 Chapter 11 Solution Manual Part 7

SOLUTION 1. Let D represent the batches of Della’s Delight made and sold. Let B represent the batches of Bonny’s Bourbon made and sold. The contribution margin per batch of Della’s Delight is $300. The contribution margin per batch of […]

978-0133428704 Chapter 12 Solution Manual Part 1

12- 1 CHAPTER 12 STRATEGY, BALANCED SCORECARD, AND STRATEGIC PROFITABILITY ANALYSIS 12-1 Strategy specifies how an organization matches its own capabilities with the opportunities in the marketplace to accomplish its objectives. 12-2 The five key forces to consider in industry […]

978-0133428704 Chapter 12 Solution Manual Part 2

SOLUTION Effect of the industry-market-size factor on operating income Of the 28,000-unit (233,000 – 205,000) increase in sales between 2012 and 2013, 20,500 (10% 205,000) units are due to growth in market size, and 7,500 (28,000 – 20,500) units […]

978-0133428704 Chapter 12 Solution Manual Part 3

The Productivity Component Cost effect of productivity for variable costs = Actual units of Units of input input used required to to produce produce 2013 2013 output ouput in 2012 − Input price in 2013 […]

978-0133428704 Chapter 12 Solution Manual Part 4

SOLUTION Effect of the industry-market-size factor on operating income Of the 3,000-unit increase in sales from 8,000 to 11,000 units, 10% or 800 (10% 8,000) units are due to growth in market size, and 2,2000 (3,000 − 800) units […]

978-0133428704 Chapter 12 Solution Manual Part 5

Required: 1. Was Cerebral successful in implementing its strategy in 2013? Explain your answer. 2. Would you have included some measure of customer satisfaction in the customer perspective? Are these objectives critical to Cerebral for implementing its strategy? Why or […]

978-0133428704 Chapter 13 Solution Manual Part 1

13-1 CHAPTER 13 PRICING DECISIONS AND COST MANAGEMENT 13-1 The three major influences on pricing decisions are 1. Customers 2. Competitors 3. Costs 13-2 Not necessarily. For a one-time-only special order, the relevant costs are only those costs that will […]

978-0133428704 Chapter 13 Solution Manual Part 2

SOLUTION 1. and 2. Manufacturing costs of HJ6 in 2012 and 2013 are as follows: 2012 2013 Per Unit Per Unit Total (2) = Total (4) = (1) (1) ÷ 2,700 (3) (3) ÷ 4,600 Direct materials, $1,400 × 2,700; […]

978-0133428704 Chapter 13 Solution Manual Part 3

13-24 (25 min.) Considerations other than cost in pricing decisions. Fun Stay Express operates a 100-room hotel near a busy amusement park. During June, a 30-day month, Fun Stay Express experienced a 65% occupancy rate from Monday evening through Thursday […]

978-0133428704 Chapter 13 Solution Manual Part 4

13-28 (25 min.) Cost-plus, target return on investment pricing. Zoom-o-licious makes candy bars for vending machines and sells them to vendors in cases of 30 bars. Although Zoom-o-licious makes a variety of candy, the cost differences are insignificant, and the […]

978-0133428704 Chapter 13 Solution Manual Part 5

13-33 (30 min.) Airline pricing, considerations other than cost in pricing. Northern Airways is about to introduce a daily round-trip flight from New York to Los Angeles and is determining how to price its round- trip tickets. The market research […]

978-0133428704 Chapter 14 Solution Manual Part 1

14-1 N CHAPTER 14 COST ALLOCATION, CUSTOMER-PROFITABILITY ANALYSIS, AND SALES-VARIANCE ANALYSIS 14-1 Disagree. Cost accounting data plays a key role in many management planning and control decisions. The division president will be able to make better operating and strategy decisions […]

978-0133428704 Chapter 14 Solution Manual Part 2

14-19 (20−25 min.) Customer profitability, distribution. Best Drugs is a distributor of pharmaceutical products. Its ABC system has five activities: Rick Flair, the controller of Best Drugs, wants to use this ABC system to examine individual customer profitability within each […]

978-0133428704 Chapter 14 Solution Manual Part 3

SOLUTION Note: In some editions of the book, the revenues for the Pulp division has a zero missing at the end. It is shown as $9,800,00 instead of $9,800,000. Percentages for various allocation bases (old and new): Pulp Paper Fibers […]

978-0133428704 Chapter 14 Solution Manual Part 4

SOLUTION Actual Budgeted Western region 12.3 million 10 million Soda King 1.23 million 1.25 million Market share 10% 12.5% Average budgeted contribution margin per unit = $3.90 ($4,875,000 ÷ 1,250,000). Solution Exhibit 14-26 presents the sales-quantity variance, market-size variance, and […]

978-0133428704 Chapter 14 Solution Manual Part 5

14-31 (30 min.) Customer-cost hierarchy, customer profitability. Denise Nelson operates Interiors by Denise, an interior design consulting and window treatment fabrication business. Her business is made up of two different distribution channels, a consulting business in which Denise serves two […]

978-0133428704 Chapter 14 Solution Manual Part 6

SOLUTION 1. Customer A Customer B Customer C Others Division Revenue $1,054,826 $1,544,680 $2,210,162 $480,33 2 $5,290,000 Customer-level costs 675,378 951,669 1,517,895 266,058 3,411,000 Customer-level operating income 379,448 593,011 692,267 214,274 1,879,000 Wholesale channel costs1 149,437 233,543 272,633 84,387 740,000 […]

978-0133428704 Chapter 14 Solution Manual Part 7

SOLUTION EXHIBIT 14-37 Market-Share and Market-Size Variance Analysis of Houston Infonautics for the Third Quarter 2014. Static Budget: Actual Market Size Actual Market Size Budgeted Market Size Actual Market Share Budgeted Market Share Budgeted Market Share […]

978-0133428704 Chapter 15 Solution Manual Part 1

15-1 CHAPTER 15 ALLOCATION OF SUPPORT-DEPARTMENT COSTS, COMMON COSTS, AND REVENUES 15-1 The single-rate (cost-allocation) method makes no distinction between fixed costs and variable costs in the cost pool. It allocates costs in each cost pool to cost objects using […]

978-0133428704 Chapter 15 Solution Manual Part 2

SOLUTION 1a. 15-1 Support Departments Operating Departments AS I S Govt. Corp. Costs $600,000 $2,400,000 Alloc. of AS costs (0.25, 0.40, 0.35) (861,538) 215,385 $ 344,615 $ 301,538 Alloc. of IS costs (0.10, 0.30, 0.60) 261,538 (2,615,385) 784,616 1,569,231 $ […]

978-0133428704 Chapter 15 Solution Manual Part 3

15-1 SOLUTION In some print editions of the book, requirement 1 states the airfare to be $1,600. The airfare in requirement 1 should be $1,200 instead of $1,600. 1. Alternative approaches for the allocation of the $1,200 airfare include the […]

978-0133428704 Chapter 15 Solution Manual Part 4

978-0133428704 Chapter 15 Solution Manual Part 5

15-1 15-28 (20 min.) Revenue allocation Yang Inc. produces and sells DVDs to business people and students who are planning extended stays in China. It has been very successful with two DVDs: Beginning Mandarin and Conversational Mandarin. It is introducing […]

978-0133428704 Chapter 15 Solution Manual Part 6

3. Comparison of Methods: Step-down method: Job 88: Machining 17 × $7.686 $130.66 Assembly 7 × $3.584 25.09 $155.75 Job 89: Machining 9 × $7.686 $ 69.17 Assembly 20 × $3.584 71.68 $140.85 Direct method: Job 88: Machining 17 × […]

978-0133428704 Chapter 15 Solution Manual Part 7

SOLUTION 1. Stand-alone cost-allocation method. Taylor Inc. = (600 $60) (1,000 $54) (600 $60) (400 $60) + = $36,000 $54,000 ($36,000 $24,000) + = $32,400 Victor Inc. = (400 $60) (1,000 $54) (600 $60) (400 $60) […]

978-0133428704 Chapter 15 Solution Manual Part 8

Collaborative Learning Problem 15-35 (20–25 min.) Revenue allocation, bundled products. Premier Resorts (PR) operates a five-star hotel with a championship golf course. PR has a decentralized management structure, with three divisions: ▪ Lodging (rooms, conference facilities) ▪ Food (restaurants and […]

978-0133428704 Chapter 16 Solution Manual Part 1

16-1 CHAPTER 16 COST ALLOCATION: JOINT PRODUCTS AND BYPRODUCTS 16-1 Exhibit 16-1 presents many examples of joint products from four different general industries. These include: Industry Separable Products at the Splitoff Point Food Processing: • Lamb • Lamb cuts, tripe, […]

978-0133428704 Chapter 16 Solution Manual Part 2

16-1 SOLUTION EXHIBIT 16-19 Joint Costs Separable Costs Processing $120000 for 10000 gallons Processing $2 per gallon Processing $3 per gallon 7500 gallons 2500 gallons Methanol: 2500 gallons at $21 per gallon Turpentine: 7500 gallons at $14 per gallon Splitoff […]

978-0133428704 Chapter 16 Solution Manual Part 3

SOLUTION 1a. PANEL A: Allocation of Joint Costs using Sales Value at Splitoff Method Special B/ Beef Ramen Special S/ Shrimp Ramen Total Sales value of total production at splitoff point (20,000 tons $5 per ton; 28,000 $20 […]

978-0133428704 Chapter 16 Solution Manual Part 4

SOLUTION 1. Net realizable value of human product: (2,000 gallons × $585) – $120,000 = $1,050,000 Net realizable value of veterinarian product: 500 gallons × ($410 – $10) = $200,000 Joint costs: $60,000 + $90,000 = $150,000 Joint costs charged […]

978-0133428704 Chapter 16 Solution Manual Part 5

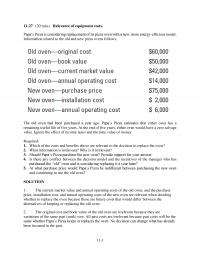

3. Further processing of chocolate-powder liquor base into chocolate powder: Incremental revenue, $81,900 – $14,000 ($20 × 700) $67,900 Incremental costs 50,100 Incremental operating income from further processing $17,800 Further processing of milk-chocolate liquor base into milk chocolate: Incremental revenue, […]

978-0133428704 Chapter 16 Solution Manual Part 6

SOLUTION 1. Byproduct—production method journal entries i) At time of production: Work-in–process Inventory 600,000 Accounts Payable, etc. 600,000 For Byproduct: Finished Goods Inv – Shreds 35,000 Work-in-process Inventory 35,000 For Joint Products Finished Goods Inv – Floor 226,000 Finished Goods […]

978-0133428704 Chapter 17 Solution Manual Part 1

17- 1 CHAPTER 17 PROCESS COSTING 17-1 Industries using process costing in their manufacturing areas include chemical processing, oil refining, pharmaceuticals, plastics, brick and tile manufacturing, semiconductor chips, beverages, and breakfast cereals. 17-2 Process costing systems separate costs into cost […]

978-0133428704 Chapter 17 Solution Manual Part 2

17- 1 17-23 (20-25 min.) Operation costing. Whole Goodness Bakery needs to determine the cost of two work orders for the month of June. Work order 215 is for 2,400 packages of dinner rolls, and work order 216 is for […]

978-0133428704 Chapter 17 Solution Manual Part 3

17-27 (35–40 min.) Transferred-in costs, FIFO method. Refer to the information in Exercise 17-26. Suppose that Trendy uses the FIFO method instead of the weighted-average method in all of its departments. The only changes to Exercise 17-26 under the FIFO […]

978-0133428704 Chapter 17 Solution Manual Part 4

SOLUTION 1. Because direct materials are added at the beginning of the assembly process, the units in this department must be 100% complete with respect to direct materials. Solution Exhibit 17-31A shows equivalent units of work done to date: Direct […]

978-0133428704 Chapter 17 Solution Manual Part 5

17-35 (30 min.) Transferred-in costs, FIFO method (continuation of 17-34). Refer to the information in Problem 17-34. Suppose that Larsen Company uses the FIFO method instead of the weighted-average method in all of its departments. The only changes to Problem […]

978-0133428704 Chapter 17 Solution Manual Part 6

SOLUTION 1. & 2. The equivalent units of work done in April 2014 in the Assembly Department for direct materials and conversion costs are shown in Solution Exhibit 17-37A. Solution Exhibit 17-37B summarizes the total Assembly Department costs for April […]

978-0133428704 Chapter 17 Solution Manual Part 7

SOLUTION EXHIBIT 17-39A Summarize the Flow of Physical Units and Compute Output in Equivalent Units; FIFO Method of Process Costing, Binding Department of Publishers, Inc., for April 2014. (Step 1) (Step 2) Equivalent Units Flow of Production Physical Units Transferred-in […]

978-0133428704 Chapter 17 Solution Manual Part 8

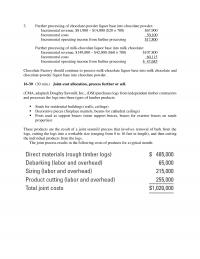

17-41 (25 min.) Multiple processes or operations, costing. The Sedona Company is dedicated to making products that meet the needs of customers in a sustainable manner. Sedona is best known for its KLN water bottle, which is a BPA-free, dishwasher-safe, […]

978-0133428704 Chapter 18 Solution Manual Part 1

18- 1 CHAPTER 18 SPOILAGE, REWORK, AND SCRAP 18-1 Managers have found that improved quality and intolerance for high spoilage have lowered overall costs and increased sales. 18-2 Spoilage—units of production that do not meet the standards required by customers […]

978-0133428704 Chapter 18 Solution Manual Part 2

SOLUTION Spoilage represents the amount of resources that go into the process but do not result in finished product. A simple way to account for spoilage in process costing is to calculate the amount of direct material that was spoiled. […]

978-0133428704 Chapter 18 Solution Manual Part 3

18-30 (25 min.) Scrap, job costing. The Russell Company has an extensive job-costing facility that uses a variety of metals. Consider each requirement independently. Required: 1. Job 372 uses a particular metal alloy that is not used for any other […]

978-0133428704 Chapter 18 Solution Manual Part 4

SOLUTION 1. Inspection Inspection Inspection at 30% at 60% at 100% Work in process, beginning (40%)* Started during November To account for 2,400 12,000 14,400 2,400 12,000 14,400 2,400 12,000 14,400 Good units completed and transferred out Normal spoilage 9,000a […]

978-0133428704 Chapter 19 Solution Manual Part 1

19- 1 CHAPTER 19 BALANCED SCORECARD: QUALITY, TIME, AND THE THEORY OF CONSTRAINTS 19-1 Quality costs (including the opportunity cost of lost sales because of poor quality) can be as much as 10% to 20% of sales revenues of many […]

978-0133428704 Chapter 19 Solution Manual Part 2

SOLUTION 1. Cell Design’s managers plan to increase spending on CAD design improvement improving machine calibrations to achieve product specifications. These are prevention activities. Cell Design’s managers plan to increase prevention costs to improve quality. This is consistent with much […]

978-0133428704 Chapter 19 Solution Manual Part 3

19-24 (25 min.) Waiting time, cost considerations, and customer satisfaction (continued from 19-23). Refer to the information presented in Exercise 19-23. The head of the registration advisors at SMU has decided that the advisors must finish their advising in 2 […]

978-0133428704 Chapter 19 Solution Manual Part 4

SOLUTION EXHIBIT 19-28A Quality improvement, Pareto diagram, cause-and-effect diagram 2. Prevention activities that could reduce failures in Pauli’s Pizza deliveries could include the following: a. Better staff training b. Improved technology for order processing c. Additional time for delivery personnel […]

978-0133428704 Chapter 19 Solution Manual Part 5

3. Delays occur in the processing of B7 and A3 because of (a) uncertainty about how many orders Brandt will actually receive (Brandt expects to receive 125 orders of B7 and 10 orders of A3), and (b) uncertainty about the […]

978-0133428704 Chapter 2 Solution Manual Part 1

2-1 CHAPTER 2 AN INTRODUCTION TO COST TERMS AND PURPOSES 2-1 A cost object is anything for which a separate measurement of costs is desired. Examples include a product, a service, a project, a customer, a brand category, an activity, […]

978-0133428704 Chapter 2 Solution Manual Part 2

SOLUTION 1. Variable manufacturing cost per vehicle Steel $1,500 per Surfer Tires 625 per Surfer Direct manufacturing labor 700 per Surfer Total $2,825 per Surfer Fixed manufacturing costs per month Plant management costs ($1,200,000 ÷ 12) $ 100,000 Cost of […]

978-0133428704 Chapter 2 Solution Manual Part 3

2-28 (20–30 min.) Inventoriable costs versus period costs. Each of the following cost items pertains to one of these companies: Star Market (a merchandising– sector company), Maytag (a manufacturing-sector company), and Yahoo! (a service-sector company): a. Cost of lettuce and […]

978-0133428704 Chapter 2 Solution Manual Part 4

SOLUTION Shaler Corporation Schedule of Cost of Goods Manufactured Year Ended December 31, 2014 (in thousands) Direct materials costs Beginning inventory, January 1, 2014 $130,000 Purchases of direct materials 256,000 Cost of direct materials available for use 386,000 Ending inventory, […]

978-0133428704 Chapter 2 Solution Manual Part 5

SOLUTION 1.(a) Total cost of hours worked at regular rates 48 hours × $20 per hour $ 960 44 hours × $20 per hour 880 43 hours × $20 per hour 860 46 hours × $20 per hour 920 3,620 […]

978-0133428704 Chapter 20 Solution Manual Part 1

20-1 CHAPTER 20 INVENTORY MANAGEMENT, JUST-IN-TIME, AND SIMPLIFIED COSTING METHODS 20-1 Cost of goods sold (in retail organizations) or direct materials costs (in organizations with a manufacturing function) as a percentage of sales frequently exceeds net income as a percentage […]

978-0133428704 Chapter 20 Solution Manual Part 2

20-1 SOLUTION EXHIBIT 20-21 Annual Relevant Costs of Current Production System and JIT Production System for Colonial Hardware Company Relevant Items Relevant Costs under Current Production System Relevant Costs under JIT Production System Annual tooling costs – $200,000 Required return […]

978-0133428704 Chapter 20 Solution Manual Part 3

SOLUTION 1. 2 DP 2 10,400 $100 EOQ C $13 == EOQ = 400 steering wheels 2. Average weekly demand = 10,400 ÷ 52 weeks = 200 steering wheels per week Purchasing lead time = 1.5 weeks Reorder point […]

978-0133428704 Chapter 20 Solution Manual Part 4

SOLUTION 1. (a) Record purchases of direct materials Materials and In-Process Inventory Control Accounts Payable Control 550,000 550,000 (b) Record conversion costs incurred Conversion Costs Control Various Accounts (such as 440,000 Wages Payable Control) 440,000 (c) Record cost of good […]

978-0133428704 Chapter 21 Solution Manual Part 1

21-1 CHAPTER 21 CAPITAL BUDGETING AND COST ANALYSIS 21-1 No. Capital budgeting focuses on an individual investment project throughout its life, recognizing the time value of money. The life of a project is often longer than a year. Accrual accounting […]

978-0133428704 Chapter 21 Solution Manual Part 2

SOLUTION 1. Present value of annuity of savings in cash operating costs ($31,250 per year for 8 years at 14%): $31,250 4.639 $144,969 Present value of $37,500 terminal disposal price of machine at end of year 8: $37,500 […]

978-0133428704 Chapter 21 Solution Manual Part 3

21-1 SOLUTION 1. The after-tax cash inflow per year is $24,400 ($19,600 + $4,800), as shown below: Annual cash flow from operations ($43,000 – $15,000) $28,000 Deduct income tax payments (0.30 $28,000) 8,400 Annual after-tax cash flow from operations […]

978-0133428704 Chapter 21 Solution Manual Part 4

21-1 1. Modernizing alternative: Present Value Discount Factors Net Cash Present Year At 10% Flow Value Jan. 1, 2015 1.000 $(36,800000) $(36,800,000) Dec. 31, 2015 0.909 10,432,500 9,483,143 Dec. 31, 2016 0.826 11,700000 9,664,200 Dec. 31, 2017 0.751 12,967,500 9,738,593 […]

978-0133428704 Chapter 21 Solution Manual Part 5

21-1 Difference in after-tax cash flow from terminal disposal of machines: $23,020 – $14,720 = $8,300 (in favor of new machine) 2. The Frooty Company should retain the old equipment because the net present value of the incremental cash flows […]

978-0133428704 Chapter 22 Solution Manual Part 1

22- CHAPTER 22 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, AND MULTINATIONAL CONSIDERATIONS 22-1 A management control system is a means of gathering and using information to aid and coordinate the planning and control decisions throughout an organization and to guide the […]

978-0133428704 Chapter 22 Solution Manual Part 2

22-21 (30 min.) Effect of alternative transfer-pricing methods on division operating income. (CMA, adapted) Ajax Corporation has two divisions. The mining division makes toldine, which is then transferred to the metals division. The toldine is further processed by the metals […]

978-0133428704 Chapter 22 Solution Manual Part 3

SOLUTION 1. The minimum transfer price that the SD would demand from the AD is the net price it could obtain from selling its screens on the outside market: $100 minus $8 marketing and distribution cost per screen, or $92 […]

978-0133428704 Chapter 22 Solution Manual Part 4

22-30 (25 min.) Goal congruence problems with cost-plus transfer-pricing methods, dual pricing system (continuation of 22-29). Assume that Pat Borges, CEO of Cranergy, had mandated a transfer price equal to 150% of full cost. Now he decides to decentralize some […]

978-0133428704 Chapter 22 Solution Manual Part 5

22–33 (30–40 min.) International transfer pricing, taxes, goal congruence. Castor, a division of Gemini Corporation, is located in the United States. Its effective income tax rate is 30%. Another division of Gemini, Pollux, is located in Canada, where the income […]

978-0133428704 Chapter 22 Solution Manual Part 6

22-35 (25 min.) Transfer pricing, goal congruence. The Croydon Division of CC Industries supplies the Hauser Division with 100,000 units per month of an infrared LED that Hauser uses in a remote control device it sells. The transfer price of […]

978-0133428704 Chapter 23 Solution Manual Part 1

23- 1 CHAPTER 23 PERFORMANCE MEASUREMENT, COMPENSATION, AND MULTINATIONAL CONSIDERATIONS 23-1 Examples of financial and nonfinancial measures of performance are Financial: ROI, residual income, economic value added, and return on sales Nonfinancial: Customer perspective: Market share, customer satisfaction Internal-business-processes perspective: […]

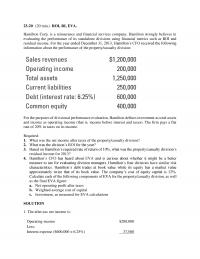

978-0133428704 Chapter 23 Solution Manual Part 2

23-20 (20 min.) ROI, RI, EVA. Hamilton Corp. is a reinsurance and financial services company. Hamilton strongly believes in evaluating the performance of its standalone divisions using financial metrics such as ROI and residual income. For the year ended December […]

978-0133428704 Chapter 23 Solution Manual Part 3

SOLUTION 1. ROI and residual income: Clothing Cosmetics Operating income after tax $ 800,000 $ 1,800,000 Net assets $3,200,000 $7,500,000 ROI ($800,000 ÷ $3,200,000; $1,800,000 ÷ $7,500,000) 25.00% 24.00% RI ($800,000 − 11% × 3,200,000; $1,800,000 − 11% × $7,500,000) […]

978-0133428704 Chapter 23 Solution Manual Part 4

SOLUTION 1. ROI = Operating income ÷ Net book value of total assets St. Louis ROI = $1,446,000 ÷ ($9,000,000 – $6,600,000 + 1,999,600) = $1,446,000 ÷ $4,399,600 = 32.87% Memphis ROI = $1,008,000 ÷ ($7,500,000 – $3,500,000 + 1,536,400) […]

978-0133428704 Chapter 23 Solution Manual Part 5

23-34 (30 min.) Financial and nonfinancial performance measures, goal congruence. (CMA, adapted) Precision Equipment specializes in the manufacture of medical equipment, a field that has become increasingly competitive. Approximately 2 years ago, Pedro Mendez, president of Precision, decided to revise […]

978-0133428704 Chapter 3 Solution Manual Part 1

3- 1 CHAPTER 3 COST–VOLUME–PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1 Cost-volume-profit (CVP) analysis examines the behavior of […]

978-0133428704 Chapter 3 Solution Manual Part 2

3- 1 SOLUTION 1. Variable cost percentage is $3.80 $9.50 = 40% Let R = Revenues needed to obtain target net income R – 0.40R – $456,000 = $159,600 1 0.30− 0.60R = $456,000 + $228,000 R = $684,000 […]

978-0133428704 Chapter 3 Solution Manual Part 3

SOLUTION 1. Sales of A, B, and C are in ratio 24,000 : 96,000 : 48,000. So for every 1 unit of A, 4 (96,000 ÷ 24,000) units of B are sold, and 2 (48,000 ÷ 24,000) units of C […]

978-0133428704 Chapter 3 Solution Manual Part 4

SOLUTION 1. Monthly Number of Orders Cost of Current System 300,000 $1,000,000 + $45(300,000) = $14,500,000 400,000 $1,000,000 + $45(400,000) = $19,000,000 500,000 $1,000,000 + $45(500,000) = $23,500,000 600,000 $1,000,000 + $45(600,000) = $28,000,000 700,000 $1,000,000 + $45(700,000) = $32,500,000 […]

978-0133428704 Chapter 3 Solution Manual Part 5

SOLUTION 1. CMU (SP – VCU = $60 – $40) $ 20.00 a. Breakeven units (FC CMU = $180,000 $20 per unit) 9,000 b. Breakeven revenues (Breakeven units SP = 9,000 units $60 per unit) $540,000 […]

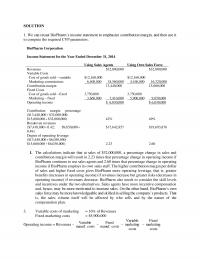

978-0133428704 Chapter 3 Solution Manual Part 6

SOLUTION 1. We can recast BioPharm’s income statement to emphasize contribution margin, and then use it to compute the required CVP parameters. BioPharm Corporation Income Statement for the Year Ended December 31, 2014 Using Sales Agents Using Own Sales Force […]

978-0133428704 Chapter 3 Solution Manual Part 7

SOLUTION 1. Sales of standard and deluxe carriers are in the ratio of 187,500 : 62,500. So for every 1 unit of deluxe, 3 (187,500 ÷ 62,500) units of standard are sold. Contribution margin of the bundle = 3 […]

978-0133428704 Chapter 4 Solution Manual Part 1

CHAPTER 4 JOB COSTING 4-1 Cost pool––a grouping of individual indirect cost items. Cost tracing––the assigning of direct costs to the chosen cost object. Cost allocation––the assigning of indirect costs to the chosen cost object. Cost-allocation base––a factor that links […]

978-0133428704 Chapter 4 Solution Manual Part 2

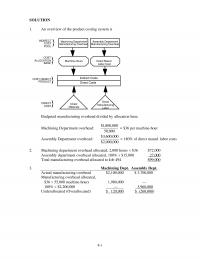

4-1 SOLUTION 1. An overview of the product costing system is COST OBJECT: PRODUCT COST ALLOCATION BASE DIRECT COST Machining Department Manufacturing Overhead Machine-Hours Direct Materials INDIRECT COST POOL Direct Manufacturing Labor Indirect Costs Direct Costs […]

978-0133428704 Chapter 4 Solution Manual Part 3

SOLUTION Some instructors may also want to assign Exercise 4-25. It demonstrates the relationships of the general ledger to the underlying subsidiary ledgers and source documents. 1. An overview of the product costing system is: 2. & 3. This answer […]

978-0133428704 Chapter 4 Solution Manual Part 4

SOLUTION Some instructors may wish to assign Problem 4-25. It demonstrates the relationships of journal entries, general ledger, subsidiary ledgers, and source documents. 1. An overview of the product-costing system is 2. Amounts in millions. (1) Materials Control Accounts Payable […]

978-0133428704 Chapter 4 Solution Manual Part 5

SOLUTION overhead rate 1. Budgeted manufacturing = Budgeted manufacturing overhead cost Budgeted direct manufacturing labor cost $125,000 50% of direct manufacturing labor cost $250,000 == 2. Overhead allocated = 50% Actual direct manufacturing labor cost = 50% $228,000 […]

978-0133428704 Chapter 4 Solution Manual Part 6

SOLUTION Although not required, the following overview diagram is helpful to understand Kidman’s job– costing system. 1. Professional Partner Labor Professional Associate Labor Budgeted compensation per professional Divided by budgeted hours of billable time per professional Budgeted direct-cost rate $ […]

978-0133428704 Chapter 4 Solution Manual Part 7

4-38 (40−55 min.) Overview of general ledger relationships. Brandon Company uses normal costing in its job-costing system. The company produces custom bikes for toddlers. The beginning balances (December 1) and ending balances (as of December 30) in their inventory accounts […]

978-0133428704 Chapter 5 Solution Manual Part 1

5-1 CHAPTER 5 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT 5-1 Broad averaging (or “peanut–butter costing”) describes a costing approach that uses broad averages for assigning (or spreading, as in spreading peanut butter) the cost of resources uniformly to cost objects when […]

978-0133428704 Chapter 5 Solution Manual Part 2

SOLUTION 1. Actual plantwide variable MOH rate based on machine hours, $308,600 4,000 $77.15 per machine hour United Motors Holden Motors Leland Auto Total Variable manufacturing overhead, allocated based on machine hours ($77.15 120; $77.15 2,800; $77.15 […]

978-0133428704 Chapter 5 Solution Manual Part 3

SOLUTION Note: The cost driver for engineering is number of engineering-hours, not number of engineers. This change does not, however, affect the solution itself. 1. Using the simple costing system, total overhead costs are equally allocated to projects. There were […]

978-0133428704 Chapter 5 Solution Manual Part 4

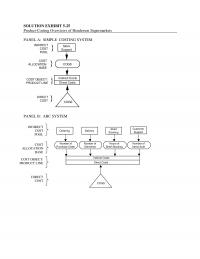

SOLUTION EXHIBIT 5-25 Product-Costing Overviews of Henderson Supermarkets PANEL A: SIMPLE COSTING SYSTEM COST OBJECT: PRODUCT LINE Indirect Costs Direct Costs Store Support COGS COGS INDIRECT COST POOL COST ALLOCATION BASE DIRECT COST PANEL B: ABC […]

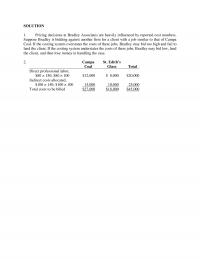

978-0133428704 Chapter 5 Solution Manual Part 5

SOLUTION 1. Pricing decisions at Bradley Associates are heavily influenced by reported cost numbers. Suppose Bradley is bidding against another firm for a client with a job similar to that of Campa Coal. If the costing system overstates the costs […]

978-0133428704 Chapter 5 Solution Manual Part 6

5-36 (30–40 min.) Activity-based costing, merchandising. Pharmahelp, Inc., a distributor of special pharmaceutical products, operates at capacity and has three main market segments: a. General supermarket chains b. Drugstore chains c. Mom-and-pop single-store pharmacies Rick Flair, the new controller of […]

978-0133428704 Chapter 5 Solution Manual Part 7

5-40 (30 min.) Unused capacity, activity-based costing, activity-based management. Whitewater Adventures manufactures two models of kayaks, Basic and Deluxe, using a combination of machining and hand finishing. Machine setup costs are driven by the number of setups. Indirect manufacturing labor […]

978-0133428704 Chapter 6 Solution Manual Part 1

6-1 CHAPTER 6 MASTER BUDGET AND RESPONSIBILITY ACCOUNTING 6-1 The budgeting cycle includes the following elements: a. Planning the performance of the company as a whole as well as planning the performance of its subunits. Management agrees on what is […]

978-0133428704 Chapter 6 Solution Manual Part 2

6-1 6-23 (45 min.) Budgeting: service company. Sunshine Window Washers (SWW) provides window-washing services to commercial clients. The company has enjoyed considerable growth in recent years due to a successful marketing campaign and favorable reviews on service-rating Web sites. Sunshine […]

978-0133428704 Chapter 6 Solution Manual Part 3

6-1 1. When the office manager receives calls from potential customers, she is instructed to handle the contracts herself. Recently, however, the number of contracts written up by the office manager has declined. At the same time, one of the […]

978-0133428704 Chapter 6 Solution Manual Part 4

6-1 SOLUTION 1. Increase in Costs for the Year Assume Trendy uses New Dye Units to dye 60,000 Cost differential ($1.25 – $0.40) per ounce × 3 ounces × $2.55 Increase in costs $153,000 Because the fine is only $120,000, […]

978-0133428704 Chapter 6 Solution Manual Part 5

6-1 SOLUTION 1. Revenue Budget For the Month of April Units Selling Price Total Revenues Cat-allac 530 $205 $108,650 Dog-eriffic 225 310 69,750 Total $178,400 2. Production Budget For the Month of April Product Cat-allac Dog-eriffic Budgeted unit sales 530 […]

978-0133428704 Chapter 6 Solution Manual Part 6

6-1 6-38 (30 min.) Cash budgeting, chapter appendix. Retail outlets purchase snowboards from Skulas, Inc., throughout the year. However, in anticipation of late summer and early fall purchases, outlets ramp up inventories from May through August. Outlets are billed when […]

978-0133428704 Chapter 6 Solution Manual Part 7

5. Direct Material Usage Budget in Quantity and Dollars For the Year Ending December 31, 2015 Material Plastic Bristles Total Physical Units Budget Direct materials required for Combs (12,600 units × 5 oz and 0 bunches) 63,000 oz. Brushes (14,200 […]

978-0133428704 Chapter 6 Solution Manual Part 8

Required: 1. Prepare each of the following for June: a. Revenues budget b. Production budget in units c. Direct material usage budget and direct material purchases budget in both units and dollars; round to dollars d. Direct manufacturing labor cost […]

978-0133428704 Chapter 7 Solution Manual Part 1

7-1 CHAPTER 7 FLEXIBLE BUDGETS, DIRECT-COST VARIANCES, AND MANAGEMENT CONTROL 7-1 Management by exception is the practice of concentrating on areas not operating as expected and giving less attention to areas operating as expected. Variance analysis helps managers identify areas […]

978-0133428704 Chapter 7 Solution Manual Part 2

SOLUTION 1. The key information items are: Actual Budgeted Output units (scones) Input units (pounds of pumpkin) Cost per input unit 60,800 16,000 $ 0.82 60,000 15,000 $ 0.89 Peterson budgets to obtain four pumpkin scones from each pound of […]

978-0133428704 Chapter 7 Solution Manual Part 3

SOLUTION For requirement 1 from Exercise 7-25: a. Direct Materials Control 18,500 Direct Materials Price Variance 370 Accounts Payable Control 18,870 To record purchase of direct materials. b. Work-in–Process Control 20,000 Direct Materials Efficiency Variance 1,500 Direct Materials Control 18,500 […]

978-0133428704 Chapter 7 Solution Manual Part 4

7-30 (30 min.) Variance analysis, nonmanufacturing setting. Marcus McQueen has run In-A-Flash Car Detailing for the past 10 years. His static budget and actual results for June 2014 are provided next. Marcus has one employee who has been with him […]

978-0133428704 Chapter 7 Solution Manual Part 5

SOLUTION 1. Materials Variances Actual Costs Incurred (Actual Input Qty. × Actual Price) Actual Input Qty. × Budgeted Price Flexible Budget (Budgeted Input Qty. Allowed for Actual Output × Budgeted Price) Direct Materials (5,200 × $17a) $88,400 Purchases Usage (5,200 […]

978-0133428704 Chapter 7 Solution Manual Part 6

SOLUTION 1. Direct Materials: Actual Costs Incurred (Actual Input Qty. × Actual Price) Actual Input Qty. × Budgeted Price Flexible Budget (Budgeted Input Qty. Allowed for Actual Output × Budgeted Price) Wool (given) $9,000 3,500 $3.40 $11,900 200 […]

978-0133428704 Chapter 7 Solution Manual Part 7

SOLUTION 1. Computing unit selling prices and unit costs of inputs: Actual selling price = $3,626,700 ÷ 462,000 = $7.85 Budgeting selling price = $3,360,000 ÷ 420,000 = $8.00 Selling-price variance = Actual selling price […]

978-0133428704 Chapter 8 Solution Manual Part 1

8- 1 CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities that add value for customers using the product or service, and […]

978-0133428704 Chapter 8 Solution Manual Part 2

Fixed Manufacturing Costs and Variances a. Fixed Manufacturing Overhead Control 12,180 Salaries Payable, Acc. Depreciation, various other accounts 12,180 To record actual fixed manufacturing overhead costs incurred. b. Work–in–Process Control 22,050 Fixed Manufacturing Overhead Allocated 22,050 To record fixed manufacturing […]

978-0133428704 Chapter 8 Solution Manual Part 3

SOLUTION 1. Easy Meals Now (May 2014) Actual Results Flexible Budget Static Budget Output units (number of deliveries) 8,600 8,600 12,000 Hours per delivery 0.66a 0.70 0.70 Hours of delivery time 5,660 6,020b 8,400c Variable overhead costs per delivery hour […]

978-0133428704 Chapter 8 Solution Manual Part 4

Required: 1. For the month of April, compute the following variances, indicating whether each is favorable (F) or unfavorable (U): a. Direct materials price variance (based on purchases) b. Direct materials efficiency variance c. Direct manufacturing labor price variance d. […]

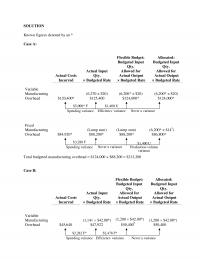

978-0133428704 Chapter 8 Solution Manual Part 5

SOLUTION Known figures denoted by an * Case A: Actual Costs Incurred Actual Input Qty. × Budgeted Rate Flexible Budget: Budgeted Input Qty. Allowed for Actual Output × Budgeted Rate Allocated: Budgeted Input Qty. Allowed for Actual Output × Budgeted […]

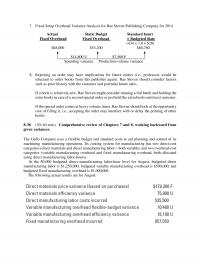

978-0133428704 Chapter 8 Solution Manual Part 6

7. Fixed Setup Overhead Variance Analysis for Rae Steven Publishing Company for 2014 Actual Static Budget Standard hours Fixed Overhead Fixed Overhead × Budgeted Rate (434 × 7.0 × $20) $68,000 $53,200 $60,760 $14,800 U $7,560 F Spending variance Production-volume […]

978-0133428704 Chapter 8 Solution Manual Part 7

SOLUTION 1. In the columnar presentation of variable overhead variance analysis, all numbers shown in bold are calculated from the given information, in the order (a)–(e). VARIABLE MANUFACTURING OVERHEAD Flexible Budget: Budgeted Input Qty. Actual Costs Incurred Actual Input Qty. […]

978-0133428704 Chapter 9 Solution Manual Part 1

9-1 CHAPTER 9 INVENTORY COSTING AND CAPACITY ANALYSIS 9-1 No. Differences in operating income between variable costing and absorption costing are due to accounting for fixed manufacturing costs. Under variable costing, only variable manufacturing costs are included as inventoriable costs. […]

978-0133428704 Chapter 9 Solution Manual Part 2

Absorption-costing Variable costing Fixed manufacturing Fixed manufacturing 2. operating income – operating income = costs in ending inventory – costs in beginning […]

978-0133428704 Chapter 9 Solution Manual Part 3

9-23 (40 min.) Variable and absorption costing, sales, and operating-income changes. Smart Safety, a three- year-old company, has been producing and selling a single type of bicycle helmet. Smart Safety uses standard costing. After reviewing the income statements for the […]

978-0133428704 Chapter 9 Solution Manual Part 4

SOLUTION This problem always generates active classroom discussion. 1. The treatment of fixed manufacturing overhead in absorption costing is affected primarily by what denominator level is selected as a base for allocating fixed manufacturing costs to units produced. In this […]

978-0133428704 Chapter 9 Solution Manual Part 6

SOLUTION 1. Fixed manufacturing overhead rate = $576,000/24,000 units = $24 per unit Manufacturing cost per unit: $20 direct materials + $35 direct mfg. labor + $9 var. mfg. OH + $24 fixed mfg. OH = $88 Selling price: $88 […]

978-0133428704 Chapter 9 Solution Manual Part 7

9-40 (20 min.) Cost allocation, responsibility accounting, ethics (continuation of 9-39). In 2015, only 740,000 Topman meals were produced and sold to the hospitals. Smith suspects that hospital controllers had systematically inflated their 2015 meal estimates. Required: 1. Recall that […]

AC 109

1) The return on investment is usually considered the most popular approach to measure performance because ________. A) it blends all the ingredients of profitability into a single percentage B) once determined, there is no need to use it with […]

AC 117 Homework

1) ________ is also called lean production. A) Economic order quantity production B) Just-in-time production C) Materials requirements planning production D) Push-through system 2) Financial accounting provides a historical perspective, whereas management accounting emphasizes ________. A) the future B) past […]

AC 202

1) An efficient management accounting system traces direct costs and allocates indirect costs to products. 2) Absorption costing enables managers to increase operating income by increasing the unit level of sales, as well as by producing more units. Answer: TRUE […]

AC 205 Quiz 1

1) When the operating budget is used as a control device, managers are less likely to be motivated to budget higher sales than actually anticipated. 2) Bottom-up budgets entrusts senior managers to prepare budgets and lower-level managers to execute them. […]

AC 250 Quiz 1

1) In markets with little or no competition, the key factor affecting price is the cost of production to the company. 2) One of the steps in planning is evaluating the performance and taking corrective measures. Answer: FALSE 3) The […]

AC 271 Quiz 1

1) In a combined 3-variance analysis, the total spending variance would be ________. A) $20,500 F B) $22,500 U C) $20,500 U D) $37,500 F 2) The gross margin for April was: A) $1,465,600 B) $3,960,400 C) $1,017,600 D) $600,400 […]

AC 468

1) Investing in a new equipment, such as flexible manufacturing systems that can be programmed to switch quickly from producing one product to producing another can decrease capacity as it would incur excess overhead costs. 2) Companies seek to minimize […]

AC 565 Homework

1) Ruben intends to sell his customers a special round-trip airline ticket package. He is able to purchase the package from the airline carrier for $150 each. The round-trip tickets will be sold for $200 each and the airline intends […]

AC 575 Quiz 3

1) Fixed costs are sometimes allocated to individual products as part of the standard costing system. When this is the case, they should be treated as variable costs for purposes of future cost estimation. 2) A composite unit is a […]

AC 609 1 Which of the following is an

1) Which of the following is an example of division-sustaining costs? A) research and development cost B) corporate administration costs C) corporate brand advertising D) shipment costs 2) Beta Corp reported the following: Required: a.Compute contribution margin. b.Compute gross margin. […]

AC 668

1) Longer manufacturing cycle times increase the inventory carrying costs and decrease revenues. 2) The DuPont method recognizes the two basic ingredients in profit making: increasing the income per dollar of revenues and using assets to generate more revenues. Answer: […]

AC 687 Test 2

1) An Enterprise Resource Planning System can best be described as ________. A) a collection of programs that use a variety of unconnected databases B) a single database that collects data and feeds it into applications that support each of […]

AC 767 Final

1) Hammond and Jarrett provide tax consulting for estates and trusts. Their job-costing system has a single direct-cost category (professional labor) and a single indirect-cost pool (research support). The indirect-cost pool contains all the costs except direct personnel costs. All […]

AC 822 Quiz 3

1) Quality-inspection costs is an example of batch-level costs. 2) Identifying and minimizing the sources of non-value-added manufacturing time increases a firm’s responsiveness to its customers and reduces its costs. Answer: TRUE 3) Simple regression analysis estimates the relationship between […]

AC 838 Quiz 2

1) All other things being equal, the longer the time horizon the more likely a cost will be fixed. 2) The full cost plus a markup transfer-pricing method can sometimes lead to goal incongruence. Answer: TRUE 3) The cost used […]

AC 887 Midterm 1

1) If one of five distribution channels is discontinued, corporate-sustaining costs such as general administration costs will most likely be reduced by 20%. 2) Management accountants must promote fact-based analysis and make tough-minded, critical judgments without being adversarial. Answer: TRUE […]

Acc 113 Quiz

1) Which of the following costs can be classified into both value-added and non-value-added costs? A) production control costs B) machine breakdown costs C) rework costs D) direct material costs 2) The cost components of a heater include $30 for […]

ACC 137

1) Which of the following is true of the Work-in-Process Control account? A) It tracks all direct material purchases. B) Its balance is the sum of amounts from all in-process individual job-cost records. C) It is an expense account. D) […]

ACC 151 Homework

1) Pearl Manufacturing Company provides glassware machines for major department store retailers. The company has been investigating a new piece of machinery for its production department. The old equipment has a remaining life of five years and the new equipment […]

Acc 155 Homework

1) Implementing activity-based costing system involves use of different cost rates for different activities to compute indirect costs of a product. 2) Fixed costs for the period are by definition a lump sum of costs that remain unchanged and therefore […]

ACC 162 Quiz

1) Which of the following is true of flexible budget? A) It calculates total variable cost by multiplying actual units by budgeted variable cost per unit. B) It calculates total fixed cost by multiplying actual units by budgeted fixed cost […]

ACC 199 Quiz 2

1) Contribution margin = Contribution margin percentage x Revenues (in dollars). 2) It is best to rely totally on financial performance measures rather than using a combination of financial and nonfinancial performance measures. Answer: FALSE Explanation: It is best to […]

Acc 211 Midterm 1

1) Aunt Ethel’s Fancy Cookie Company manufactures and sells three flavors of cookies: Macaroon, Sugar, and Buttercream. The batch size for the cookies is limited to 1,000 cookies based on the size of the ovens and cookie molds owned by […]

Acc 213 Homework 1 If the

1) If the production planners set the budgeted machine hours standards too tight, one could anticipate there would be a favorable variable overhead efficiency variance. 2) Possible reasons for the larger actual materials-handling labor-hours per batch include the possibility of […]

ACC 288 Midterm 2

1) The formal management control system includes shared values, loyalties, and mutual commitments among members of the company, company culture, and norms about acceptable behavior for managers and other employees. 2) Reducing the investment base involves decreasing idle cash, managing […]

ACC 290 Midterm

1) In joint costing, outputs with no sales value are always excluded when costs are allocated using physical measures. 2) A capital budgeting project is accepted if the required rate of return equals or exceeds the internal rate of return. […]

Acc 294 Homework

1) Roberson Corporation manufactured 30,000 ice chests during September. The variable overhead cost-allocation base is $11.25 per machine-hour. The following variable overhead data pertain to September: What is the flexible-budget amount? A) $121,500 B) $151,875 C) $165,000 D) $168,750 2) […]

ACC 305

1) ABC systems and department costing systems use totally different approaches towards indirect cost allocation and can never be used together. 2) A performance report compares actual performance to the amount budgeted. Answer: TRUE 3) Managers cannot use human resource […]

ACC 305 Test 1

1) The ideal database for estimating cost functions contains ________. A) numerous cost driver observations B) only the independent variable and not the dependent variable C) cost driver observations spanning a narrow range D) a few values of the cost […]

ACC 349 Test 1

1) When actual cost-allocation rates are used, managers of the supplier division are motivated to improve efficiency. 2) Activity -based costing plays a more significant role in job costing as compared to process costing as companies using process costing have […]

ACC 397

1) The Fortise Corporation manufactures two types of vacuum cleaners, the Victor for commercial building use and the House-Mate for residences. Budgeted and actual operating data for the year 2015 were as follows: What is the contribution margin for the […]

Acc 402 Quiz 2

1) Product-cost cross-subsidization is very common when costs are uniformly spread across various products. 2) The net present value (NPV) method calculates the expected monetary gain or loss from a project by discounting all expected future cash inflows and outflows […]

Acc 414 Test

1) The standard error of the estimated coefficient indicates how much the estimated value, b, is likely to be affected by random factors. 2) The single cost-allocation method makes no distinction between fixed and variable costs. Answer: TRUE 3) When […]

Acc 434 Test

1) Jacob’s Manufacturing sales is equal to production.If Jacob’s Manufacturing presented a Financial Accounting Income Statement emphasizing gross margin showing operating income of $180,000, a Contribution Income Statement emphasizing contribution margin would show a different operating income. 2) A firm […]

Acc 440

1) Favorable overhead variances are always recorded with credits in a standard cost system. 2) The stand-alone method of allocating determines the weights for cost allocation by considering each user of the cost as a separate entity. Answer: TRUE 3) […]

Acc 442 Test 2

1) Budgeted fixed manufacturing costs of a product using practical capacity ________. A) represents the cost per unit of supplying capacity B) can result in setting selling prices that are not competitive C) includes the cost of unused capacity D) […]

Acc 460 Test 1

1) The main difference between variable costing and absorption costing is the way in which fixed manufacturing costs are accounted for. 2) Step fixed-cost functions are variable over the long run. Answer: TRUE 3) Cross-sectional data pertain to the same […]

Acc 498 Midterm

1) Companies that only record the invoice price can usually track the magnitude of price discounting. 2) Economic value added, unlike residual income, charges managers for the costs of their investments in long-term assets and working capital. Answer: FALSE Explanation: […]

ACC 501 Test

1) The opportunity cost of the stockout includes lost contribution margin on the sale not made plus any contribution margin lost on future sales due to customer ill will. 2) Cost of quality financial measures will usually deteriorate when nonfinancial […]

ACC 510 Midterm 2

1) The financial perspective of the balanced scorecard identifies targeted customers and market segments and measures the company’s success in these segments. 2) The same cost concept used for external and internal reporting purposes. Answer: FALSE 3) In a job-cost […]

ACC 522 Test

1) Cost bases that include fewer costs also have lower markups. 2) If U.S dollar strengthens against the Japanese Yen, Japanese producers selling goods in U.S markets will have to increase the prices of products to recover the extra cost […]

Acc 537 Midterm 1

1) Companies implementing kaizen budgeting believe that employees who actually do the job have the best knowledge of how the job can be done better. 2) Proration is the spreading of underallocated or overallocated overhead among ending work in process, […]

Acc 641 Midterm 1

1) The economic order quantity model completely ignores ________. A) carrying costs B) ordering costs C) stockout costs D) the size of a purchase order 2) Ways to “produce for inventory” that result in increasing operating income include ________. A) […]

Acc 666 Quiz 3

1) Bar charts and a whale curve are some of the common ways of displaying the results of customer-profitability analysis. 2) Financial accounting information focuses on internal reporting. Answer: FALSE Explanation: Management accounting information focuses on internal reporting and financial […]

ACC 677 Test 2

1) In joint costing, the physical measures are generally used for products or services that are processed and, after splitoff, additional value is added to the product and a selling price can be determined. 2) The Required Rate of Return […]

ACC 710 Quiz

1) Direct materials and direct manufacturing labor become a part of work-in-process inventory on the balance sheet because the direct manufacturing labor transforms the direct materials to another asset, work-in-process inventory. 2) Service-sector companies have no use of variance analysis […]

ACC 776 Test

1) A budget serves as much as a control tool as a planning tool because ________. A) it aids in the coordination and communication among various business functions B) it helps to evaluate customer needs and feedback C) it is […]

Acc 842 Quiz

1) Supply the missing data for each of the following proposals: Proposal A Proposal B Proposal C Initial investment (a) $62,900 $226,000 Annual net cash inflow $60,000 (c) (e) Life, in years 10 6 10 Salvage value $0 $10,000 $0 […]

Accounting 134

1) A time driver is any factor that causes a change in the speed of an activity when the factor changes. 2) Companies that overcost products will most likely lose market share. Answer: TRUE 3) All cost functions are linear. […]

Accounting 164 Test

1) Under the weighted-average method, the stage of completion of beginning work in process ________. A) is relevant in determining the equivalent units B) must be combined with the work done during the current period to determine the equivalent units […]

Accounting 190 Midterm 1

1) Accounting methods for internal reporting purposes are specified by Generally Accepted Accounting Principles (GAAP). 2) A favorable flexible-budget variance for variable costs may be the result of using more input quantities than were budgeted. Answer: FALSE Explanation: An unfavorable […]

Accounting 252

1) Customer life-cycle costs focus on the total costs incurred by a customer to acquire, use, maintain, and dispose of a product or service. 2) Inflation and fluctuations in foreign-currency exchange rates affect performance measurement. Answer: TRUE 3) The actual […]

Accounting 260

1) Some companies present financial and nonfinancial performance measures for various organization units in a single report called the balanced scorecard. 2) If indirect-cost rates were based on actual short-term usage, periods of lower demand would result in lower costs […]

Accounting 298 Quiz 1

1) Bonuses given to employees based on performance is an example of extrinsic reward. 2) The breakeven points are the same under both variable costing and absorption costing. Answer: FALSE Explanation: The breakeven points are generally different under both variable […]

Accounting 354 Quiz 3

1) Direct material price variance is likely to be unfavorable if the purchasing manager switched to a lower-price supplier. 2) A linear cost function can only represent fixed cost behavior. Answer: FALSE Explanation: A linear cost function can represent fixed, […]

Accounting 480 Homework

1) The contribution-margin format of the income statement distinguishes manufacturing costs from nonmanufacturing costs. 2) An organization’s strategy matches its capabilities with the opportunities in the marketplace to accomplish its objectives. Answer: TRUE 3) Separable costs include manufacturing costs only. […]

Accounting 584

1) A company with sales of $50,000, variable costs of $35,000, and fixed costs of $25,000 will earn a net income of $15,000. 2) A cost object is anything for which a measurement of costs is desired. Answer: TRUE 3) […]

Accounting 607 Test

1) At the end of the fiscal year, the fixed overhead spending variance is always prorated among work-in-process control, finished goods control, and cost of goods sold on the basis of the fixed overhead allocated to these accounts. 2) Kaizen […]

Accounting 614 Midterm 1

1) A company may use job costing to assign costs to different product lines and then use process costing to calculate unit costs within each product line. 2) Long-run pricing is an operational decision and not a strategic decision as […]

Accounting 638 Quiz 3

1) Activity-based costing attempts to identify the most relevant cause-and-effect relationship for each activity pool without restricting the cost driver to only units of output or variables related to units of output. 2) Practical capacity rather than master-budget volume is […]

Accounting 672

1) Under the step-down method, once a support department’s costs have been allocated, all subsequent support-department costs are allocated back to it. 2) The equivalent unit concept is a means by which a process costing system can compare partially completed […]

Accounting 789 Test

1) Fox Studios, the movie production house, uses process costing to estimate costs. 2) Merchandising companies hold only one type of inventory: direct material. Answer: FALSE Explanation: Merchandising companies normally hold only one type of inventory: merchandise inventory. 3) Management […]

Accounting 792

1) Fixed costs remain constant at $400,000 per month. During high-output months variable costs are $320,000, and during low-output months variable costs are $80,000. What are the respective high and low indirect-cost rates if budgeted professional labor-hours are 16,000 for […]

Accounting 835 Homework

1) Buzz’s Educational Software Outlet sells two or more of the video games as a single package. Managers are keenly interested in individual product-profitability figures. Information pertaining to three bundled products and the stand-alone prices is as follows: Using the […]

Accounting 836

1) Benchmarking is the continuous process of measuring products, services, and activities against the best possible levels of performance, either inside or outside the organization. 2) An individual cost item can be simultaneously a direct cost of one cost object […]

Accounting 860 Test 1

1) A variance is the difference between the actual cost for the current and expected (or budgeted) performance. 2) Operating income plus total fixed costs equals the contribution margin. Answer: TRUE Explanation: Total revenues less total variable costs equal the […]

Accounting 894

1) Aerated Water Company makes internal transfers at 180% of full cost. The Soda Refining Division purchases 30,000 containers of carbonated water per day, on average, from a local supplier, who delivers the water for $30 per container via an […]

Acct 134 Quiz 3

1) One problem with total factor productivity revolves around the measurement of combined productivity of all inputs. 2) The t-value of a coefficient measures how large the value of the estimated coefficient is relative to its standard error. Answer: TRUE […]

ACCT 145 Quiz 3

1) One way to increase capacity is to reduce the time it takes for setups and processing. 2) Direct costs are traced the same way for actual costing and normal costing. Answer: TRUE 3) All inventory costs are available in […]

Acct 175

1) The purchase-order lead time is the ________. A) time between placing an order and its delivery B) time between receiving a customer order and producing the products C) time between receiving a customer order and delivering the items D) […]

ACCT 205 Test 1

1) Velshi Printers has contracts to complete weekly supplements required by forty-six customers. For the year 2015, manufacturing overhead cost estimates total $840,000 for an annual production capacity of 12 million pages. For 2015 Velshi Printers has decided to evaluate […]

Acct 211 Quiz 2

1) Under the incremental method of allocating common costs ________. A) the parties are interested in being viewed as primary users B) each party bears a proportionate share of the total costs in relation to their individual stand-alone costs C) […]

Acct 224 Quiz

1) In a cost center, a manager is responsible for investments, revenues, and costs. 2) Tightly budgeted machine time standards can lead to unfavorable variable overhead efficiency variance. Answer: TRUE 3) When using the cause-and-effect criterion, cost drivers are selected […]

ACCT 234 Quiz 3

1) Rework labor time is considered an overhead cost and not a direct labor cost. 2) As a company reduces its inventory levels, operating income differences between absorption costing and variable costing become immaterial. Answer: TRUE 3) A company usually […]

ACCT 250 Test 2

1) To evaluate overall aggregate performance, return on investment and residual income measures are more appropriate than return on sales. 2) The cost driver of an indirect cost is often used as the cost-allocation base. Answer: TRUE 3) Fixed cost […]

ACCT 255 Midterm

1) Distribution of questionnaires to customers regarding product quality and improving the product on certain key areas based on the inferences drawn from the questionnaires is an example of a nonfinancial measure of quality. 2) An example of a physical […]

Acct 259

1) The tariffs and customs duties governments levy on imports of products into a country also affect the transfer pricing practices of multinationals. 2) An organization should design its management control system independently of its strategies, so that the system […]

ACCT 277 Test 2

1) Absorption costing helps managers to artificially inflate profits by encouraging the production of products that absorb the highest amount of fixed manufacturing costs. 2) The weighted-average process costing method does not distinguish between units started in the previous period […]

ACCT 293 Quiz

1) Variable cost per labor-hour is $8.50. Fixed cost is $10,500. Calculate the total cost for 350 labor hours. Machine hours during the period are 50. A) $10,925 B) $13,475 C) $13,900 D) $3,400 2) Which of the following is […]

ACCT 341

1) Use of practical capacity results in an unrealistically small fixed manufacturing cost per unit because it is based on an idealistic and unattainable level of capacity. 2) A company should use the same denominator level capacity for all the […]

Acct 347

1) Reverse engineering can be used to analyze competitors’ products to determine product designs and materials and to understand the technologies competitors use. 2) The dependent variable is a cost to be predicted and managed, whereas an independent variable or […]

ACCT 399 Midterm 2

1) Indirect manufacturing costs should be allocated equally to each job. 2) Kaizen budgeting does NOT make sense for cost centers. Answer: FALSE Explanation: Kaizen budgeting can be used in any type of responsibility center. 3) Engineered costs result from […]

ACCT 426

1) A price-bidding decision for a one-time-only special order includes an analysis of all ________. A) manufacturing costs B) cost drivers related to the product C) direct and indirect variable costs of each function in the value chain D) fixed […]

Acct 441

1) The prime cost for September was: A) $114,000 B) $100,000 C) $103,000 D) $47,000 2) Netzone Company is in semiconductor industry and fabrication of silicon-wafer chips splits off two types of memory chips, Standard and Premium. The following information […]

Acct 544 Midterm

1) The selling price per unit is $25, variable cost per unit $15, and fixed cost per unit is $4. When this company operates above the breakeven point, the sale of one more unit will increase net income by $6. […]

Acct 545 1 Determining the

1) Determining the “right” level of capacity is one of the most strategic and difficult decisions managers face. 2) The difference between total revenues and total variable costs is called contribution margin. Answer: TRUE 3) Multiple regression analysis estimates the […]

ACCT 553

1) Supervision costs have both value-added and non-value-added components. 2) Evaluating a performance helps in the future decision-making process. Answer: FALSE Explanation: Feedback and learning helps in the future decision-making process. 3) An advantage of the single-rate method is that […]

Acct 558 Quiz 3

1) The internal rate-of-return (IRR) method calculates ________. A) the discount rate at which an investment’s present value of the total of all expected cash inflows equals the present value of its expected cash outflows. B) the discount rate at […]

ACCT 569

1) Too high a price may ________. A) deter a customer from purchasing a product B) increase demand for the product C) indicate supply is too plentiful D) decrease a competitor’s market share 2) Which of the following is an […]

Acct 589 Quiz 3

1) The two broad strategies that companies follow are cost leadership strategy and product differentiation strategy. 2) In a series of interdepartmental transfers, each department is regarded as separate and distinct for accounting purposes. Answer: TRUE 3) Management by exception […]

Acct 606 Quiz 1

1) Lukehart Industries, Inc., produces air purifiers. Lukehart, Inc., produces the air purifiers in batches. To manufacture a batch of the purifiers, Lukehart, Inc., must set up the machines and assembly line tooling. Setup costs are batch-level costs because they […]

ACCT 627 Test 2

1) Pearl Lights sells only pearl necklaces. 8,000 units were sold resulting in $240,000 of sales revenue, $60,000 of variable costs, and $40,000 of fixed costs. The breakeven point in total sales dollars is ________. A) $40,000 B) $53,334 C) […]

ACCT 681 Final

1) Gambino Corporation is a wholesaler that sells a single product. Management has provided the following cost data for two levels of monthly sales volume. The company sells the product for $138.80 per unit. The best estimate of the total […]

ACCT 701 Test 1

1) In joint costing, using physical measures at splitoff to allocate costs enables the accountant to obtain individual product costs and gross margins. 2) To reduce the undesirable incentives to build up inventories that absorption costing can create, a number […]

Acct 749 Midterm 2

1) Products S5 and CP8 each are assigned $100.00 in indirect costs by a traditional costing system. An activity analysis revealed that although production requirements are identical, S5 requires 45 minutes less setup time than CP8. According to an ABC […]

ACCT 752 Midterm 1

1) Under both variable and absorption costing, research and development costs are period costs. 2) Actual prices paid for materials usually serve as actual direct-cost rates for charging material costs to jobs. Answer: TRUE 3) Backflush costing is a costing […]

Acct 771 Midterm

1) Bismite Corporation purchases trees from Cheney lumber and processes them up to the splitoff point where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to […]

ACCT 786

1) Post-investment audits prevent managers from overstating the expected cash inflows from projects and accepting projects they should reject. 2) Activity-based budgeting would permit the use of multiple drivers and multiple cost pools in the budgeting process. Answer: TRUE 3) […]

ACCT 787 Test

1) The high-low method uses cost and activity data from just two periods to establish the formula for a mixed cost. 2) Direct costs of a cost object are costs related to a particular cost object that can be allocated […]

Acct 807 Homework

1) The production method for recognizing byproducts reduces the cost of manufacturing the main or joint products in the income statement. 2) All costs other than direct materials and direct manufacturing labor are classified as indirect costs. Answer: TRUE 3) […]

ACCT 809 Test 1

1) Management is primarily a human activity that should focus on encouraging individuals to do their jobs better. 2) As budgeting is not a cross-functional activity, it tends to be accurate and reliable with regard to forecasts. Answer: FALSE Explanation: […]

ACCT 839 Midterm 1

1) Tracking price discounts by customer and by salesperson helps improve customer profitability. 2) As companies increase supply, the cost of producing an additional unit initially declines but eventually increases. Answer: TRUE 3) A cost function is a mathematical description […]

ACCT 847 Quiz 3

1) The classification of costs as variable and fixed depends on the relevant range, the length of the time horizon, and the specific decision situation. 2) To determine outputs at each stage of production, MRP uses a bill of materials […]

Acct 883 Quiz 2

1) Productivity describes the relationship between different quantities of inputs consumed and the quantities of output produced. 2) When budgeted cost-allocation rates are used, variations in actual usage by one division affect the costs allocated to other divisions. Answer: FALSE […]

Acct 887 Midterm 2

1) Competence includes maintaining an appropriate level of professional expertise by continually developing knowledge and skills. 2) A refined costing system provides better measurement of the costs of indirect resources used by different cost objects, no matter how differently various […]

ACT 106 Test 2

1) For each cost pool listed select an appropriate allocation base from the list below. An allocation base may be used only once. Assume a manufacturing company. Allocation bases for which the information system can provide data: 1.Number of employees […]

ACT 126 Homework

1) To comply with antitrust laws, a company must not engage in predatory pricing, dumping, or collusive pricing which lessen competition, put another company at a competitive disadvantage, or harm consumers. 2) Total factor productivity explicitly considers gains from using […]

ACT 249 Quiz

1) Ventaz Corp manufactures glasses. The manufacturing cycle efficiency is 70%. What is its waiting time if the manufacturing lead time is 120 minutes per keyboard? A) 38.00 minutes B) 42.00 minutes C) 48.00 minutes D) 36.00 minutes. 2) Gloria’s […]

ACT 310 Test 2

1) In a just-in-time production system, inventory carrying costs would be high. 2) Wood used to manufacture chairs is considered a direct variable cost. Answer: TRUE 3) An unfavorable price variance for materials-handling labor indicates that the actual cost per […]

ACT 383 Midterm 1

1) Process costing ________. A) allocates all product costs, including materials, and labor B) results in different costs for different units produced C) is commonly used by general contractors who construct custom-built homes D) is used exclusively in manufacturing 2) […]

ACT 388 Midterm 1

1) The Allianz Company produces a specialty wood furniture product, and has the following information available concerning its inventory items: Relevant ordering costs per purchase order$450 Relevant carrying costs per year for each package: Required annual return on investment15% Required […]

ACT 397

1) The weighted-average cost of capital (WACC) equals ________. A) the after-tax average cost of all the long-term and short-term funds B) the after-tax average cost of all the long-term funds C) the pre-tax average cost of all the short-term […]

ACT 425 Final

1) Ridez Manufacturing currently produces 1,000 bicycles per month. The following per unit data apply for sales to regular customers: The plant has capacity for 3,000 bicycles and is considering expanding production to 2,000 bicycles. What is the per unit […]

ACT 427 Homework

1) Inventoriable costs and period costs flow through the income statement at a merchandising company similar to the way costs flow at a manufacturing company. 2) A particular cost item could be variable for one cost object and fixed for […]

ACT 444 Test 2

1) All else being constant, an increase in operating income will result in an increase in net income. 2) Throughput costing results in a higher amount of manufacturing costs being placed in inventory than either variable or absorption costing. Answer: […]

ACT 539

1) It is appropriate to incorporate expected learning-curve efficiencies when evaluating performance. 2) An organization which uses product differentiation strategy will charge higher prices. Answer: TRUE 3) After a budget is agreed upon and finalized by the management team, the […]

ACT 554 Test 2

1) Customer response time comprises of ________. A) manufacturing cycle time and delivery time only B) receipt time and manufacturing cycle time only C) receipt time, manufacturing cycle time, and delivery time D) manufacturing time and delivery time only 2) […]

ACT 565

1) Manufacturing overhead cost is an example of indirect engineered costs. 2) Downsized capacity is the amount of productive capacity available over and above the productive capacity employed to meet customer demand in the current period. Answer: FALSE Explanation: The […]

ACT 614 Test 2

1) The Standards of Ethical Conduct for management accountants include concepts related to ________. A) competence, performance, diligence, and reporting B) competence, confidentiality, integrity, and credibility C) experience, diligence, reporting, and objectivity D) diligence, objectivity, conflicts of interest, and credibility […]

ACT 674 Quiz

1) Budgeted production equals ________. A) beginning finished goods inventory + budgeted unit sales – targeted ending finished goods inventory B) targeted ending finished goods inventory + beginning finished goods inventory – budgeted unit sales C) budgeted unit sales + […]

ACT 679

1) The NPV method is the preferred method over IRR for selecting projects because ________. A) its use leads to shareholder value maximization B) it accounts for the time value of money C) it assumes that cash flows are reinvested […]

ACT 690

1) Total manufacturing costs is comprised of ________. A) direct materials costs and period costs B) direct materials costs, direct manufacturing labor costs, and manufacturing overhead costs C) indirect materials costs, indirect manufacturing labor costs, and manufacturing overhead costs D) […]

ACT 706