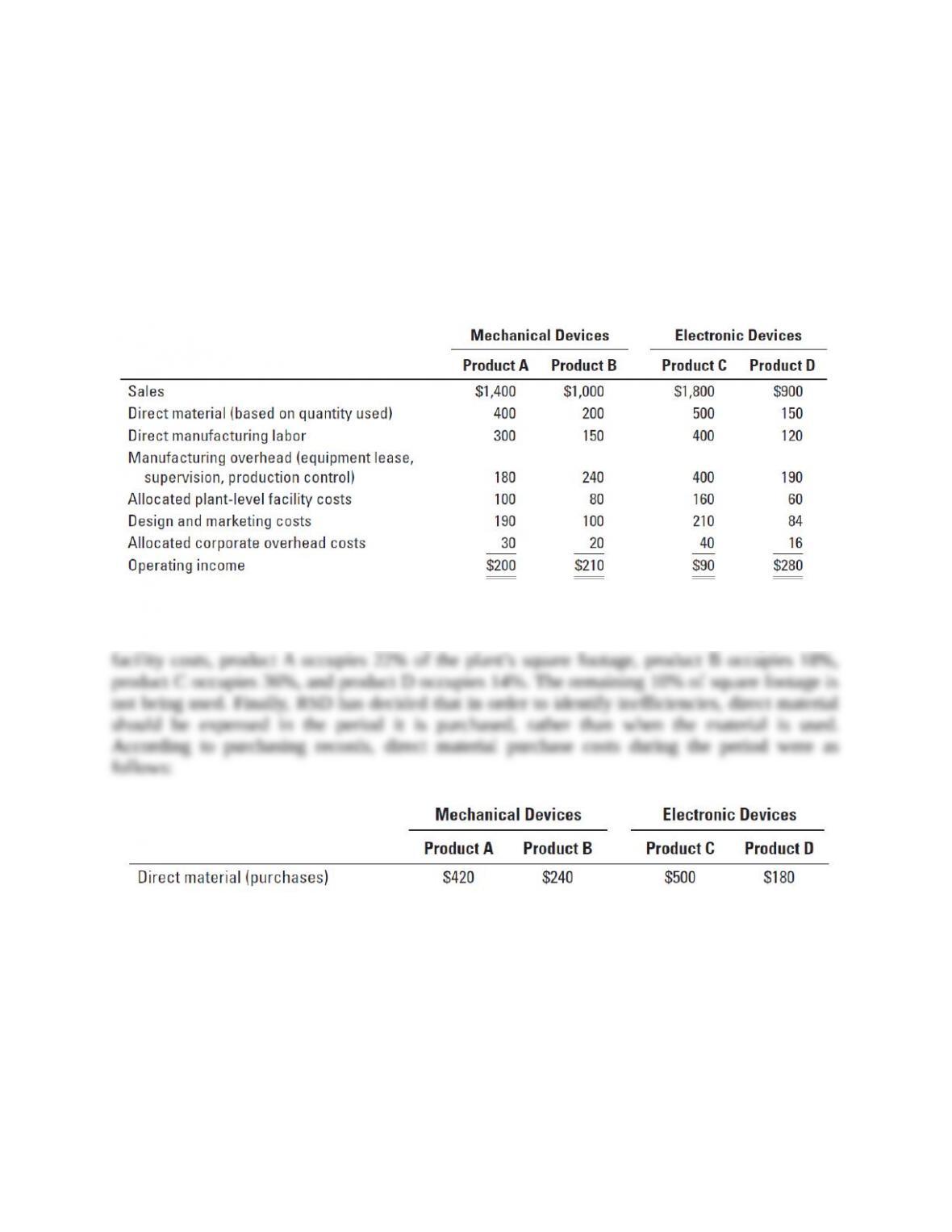

Plant-level operating income

$ 400

$ 396

For Mechanical Devices, the total plant-level costs are $2,000,000, while the total value

stream costs are $1,980,000 (99% of $2,000,000). For Electronic Devices, the total plant–level

costs are $2,304,000, while the total value stream costs are $2,284,000 (99.1% of $2,304,000). The

difference between the total value-stream costs and the total plant-level costs is very small,

indicating that the main opportunity for improving efficiency to reduce costs and improve

profitability is reducing unused plant-level facility costs.

The value-stream operating income as a percentage of revenues for Mechanical Devices is

17.5% ($420,000 ÷ $2,400,000) and for Electronic Devices is 15.4% ($416,000 ÷ $2,700,000).

Mechanical Devices has higher value stream operating income as a percentage of revenue than

Electronic Devices but both value streams can improve profitability by being more efficient in

their purchases of direct materials. Mechanical Devices purchases $60,000 ($660,000 − $600,000)

more direct materials than it uses while Electronic Devices purchases $30,000 ($680,000 −

$650,000) more. If Mechanical Devices had purchased $60,000 less direct materials, its value–

stream operating income would be $480,000 ($420,000 + $60,000) and its profitability percentage

would be 20% ($480,000 ÷ $2,400,000). If Electronic Devices had purchased $30,000 less direct

materials, its value-stream operating income would be $446,000 ($416,000 + $30,000) and its

profitability percentage would be 16.5% ($446,000 ÷ $2,700,000). Given that Electronic Devices

is less profitable than Mechanical Devices, it is more urgent for Mechanical Devices to make

efficiency improvements.

Value-stream operating income analyses ignore allocated corporate overhead costs because

these costs cannot be controlled or influenced by plant-level managers. The following factors

explain the differences between traditional operating income and lean accounting income for the

two value streams (in thousands of dollars):

Mechanical

Devices

Electronic

Devices

Traditional operating income

($200 + $210; $90 + $280)

$410

$370

Additional cost of direct materials purchased

over direct materials used

($660 − $400 – $200; $680 − $500 – $150)

(60)

(30)

Decrease in allocated plant-level overhead

($100 + $80 – $160; $160 + $60 – $200)

20

20

Add back allocated corporate overhead costs

($30 + $20; $40 + $16)

50

56

Value stream operating income

$420

$416