1) Supervision costs have both value-added and non-value-added components.

2) Evaluating a performance helps in the future decision-making process.

3) An advantage of the single-rate method is that it is the most accurate method of

cost-allocation.

4) An investment center is always a decentralized subunit.

5) Reengineering benefits are most significant when they focus on one business

function rather than crossing functional lines of the business process.

6) Direct manufacturing labor efficiency variance is likely to be unfavorable if

underskilled workers are put on a job.

7) The selling prices method under stand-alone revenue-allocation method is best

because the weights explicitly consider the prices customers are willing to pay for the

individual products

8) Advances in information-gathering technology make it more likely that multiple

cost-pool systems will pass the cost-benefit test.

9) When actual production is below practical capacity, there will be unused-capacity

cost only in the manufacturing function and not in nonmanufacturing parts like

distribution function.

10) To calculate the breakeven point in a multiproduct situation, one must assume that

the sales mix of the various products remains constant.

11) A cost-allocation base is a necessary element when using a strategy that will refine a

costing system.

12) Corporate-sustaining costs are costs of activities to support individual customers,

regardless of the number of units or batches of product delivered to the customer.

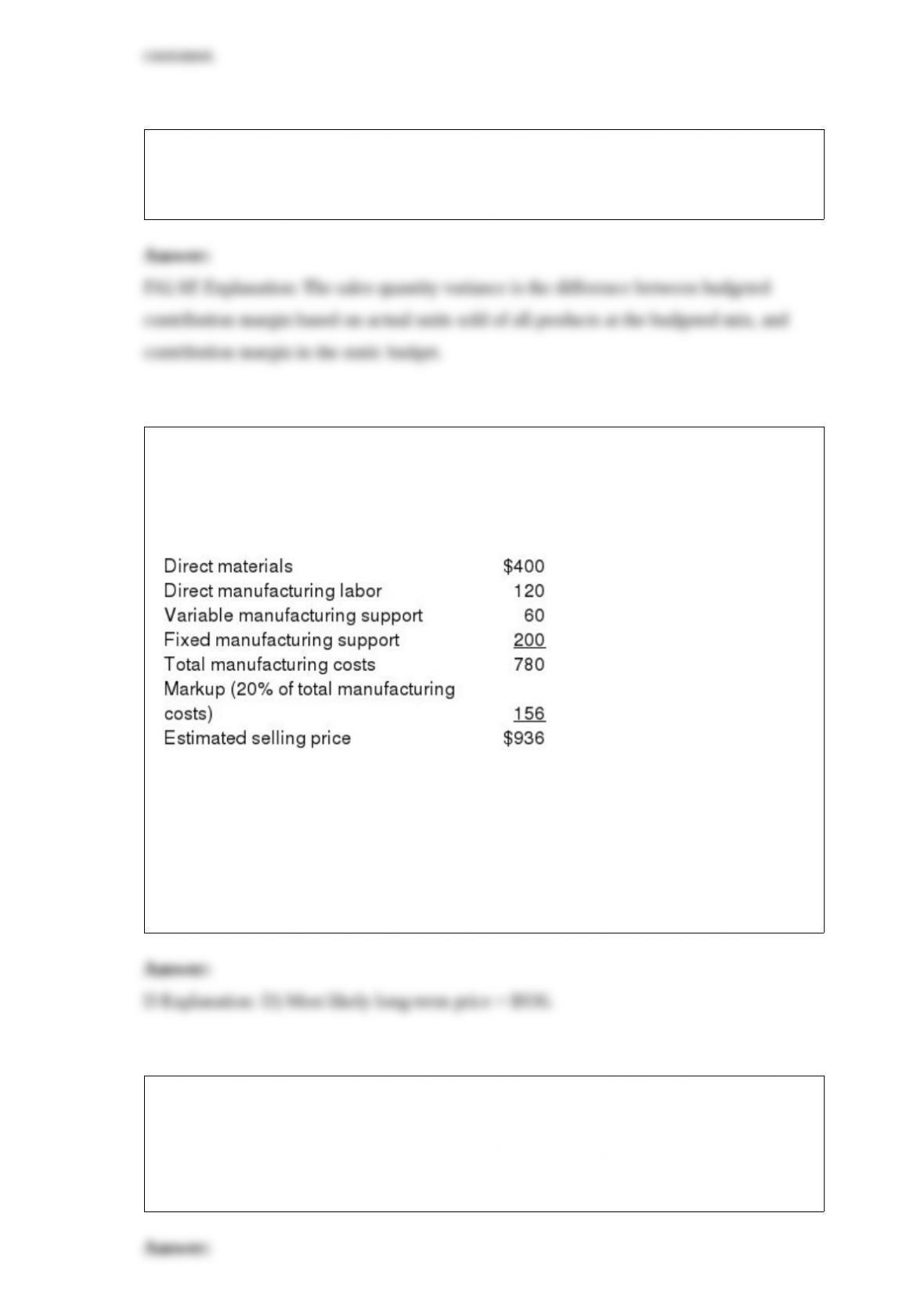

13) The sales quantity variance is the difference between budgeted contribution margin

based on actual units sold of all products at the budgeted mix, and contribution margin

in the flexible budget.

14) Zolas’ Heaters is approached by Ms. Leila, a new customer, to fulfill a large

one-time-only special order for a product similar to one offered to regular customers.

Zolas’ Heaters has excess capacity. The following per unit data apply for sales to regular

customers:

If Ms. Leila wanted a long-term commitment, and not a one-time-special order, for

supplying this product, calculate the most likely price to be quoted assuming the

markup remains same?

A) $780

B) $580

C) $520

D) $936

15) Total factor productivity will increase if ________.

A) technical productivity occurs

B) the company uses more total inputs per output

C) the company incurs fewer costs per input

D) current technology becomes obsolete

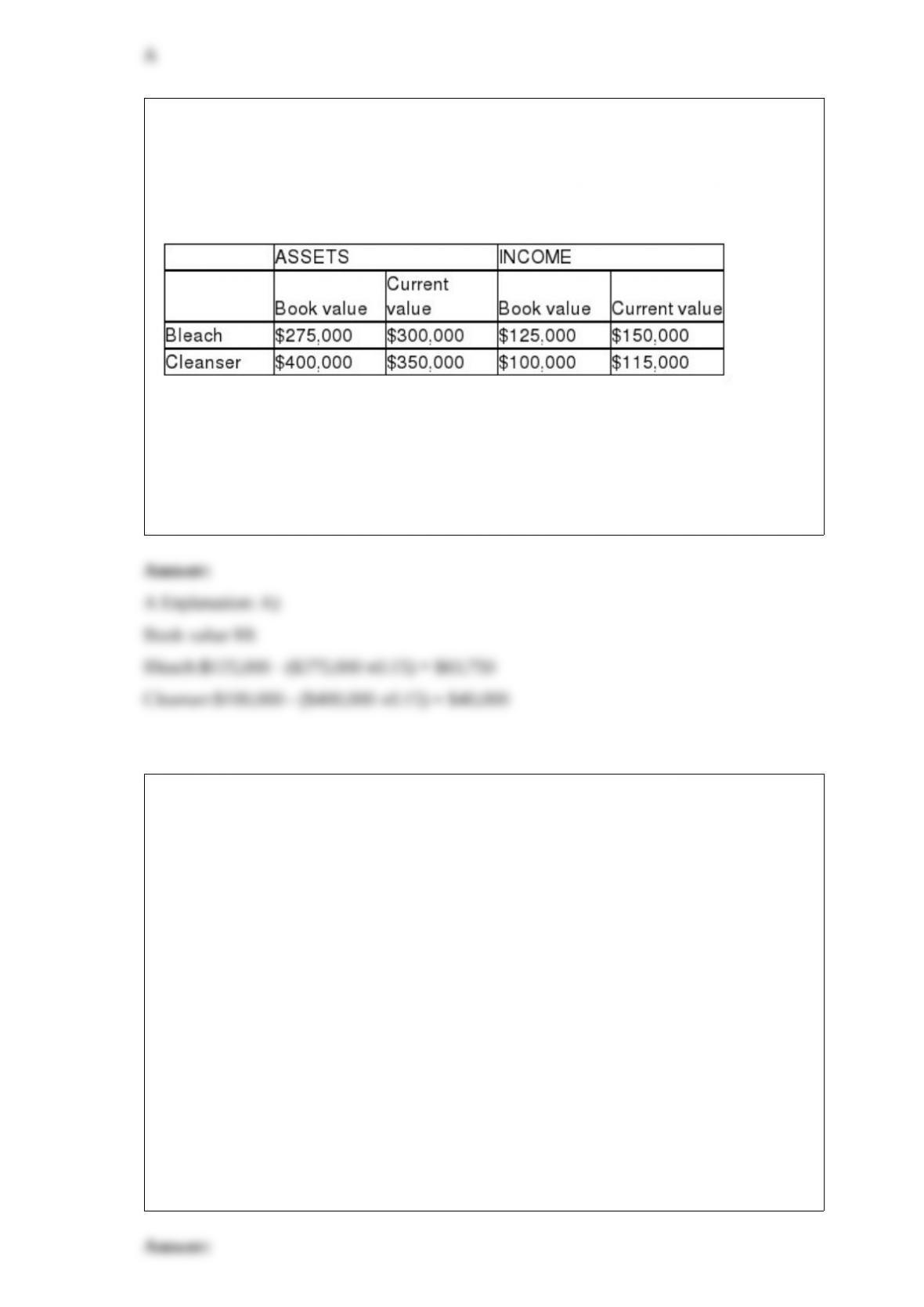

16) Home Decor Inc., manufactures home cleaning products. The company has two

divisions, Bleach and Cleanser. Because of different accounting methods and inflation

rates, the company is considering multiple evaluation measures. The following

information is provided for 2015:

The company is currently using a 15% required rate of return.

What are Bleach’s and Cleanser’s residual incomes based on book values, respectively?

A) $83,750; $40,000

B) $110,000; $67,500

C) $67,500; $110,000

D) $81,500; $40,250

17) Cysco Corp has a budget of $1,200,000 in 2015 for prevention costs. If it decides to

automate a portion of its prevention activities, it will save $100,000 in variable costs.

The new method will require $50,000 in training costs and $140,000 in annual

equipment costs. Management is willing to adjust the budget for an amount up to the

cost of the new equipment. The budgeted production level is 200,000 units.

Appraisal costs for the year are budgeted at $500,000. The new prevention procedures

will save appraisal costs of $50,000. Internal failure costs average $30 per failed unit of

finished goods. The internal failure rate is expected to be 5% of all completed items.

The proposed changes will cut the internal failure rate by one-half. Internal failure units

are destroyed. External failure costs average $50 per failed unit. The company’s average

external failures average 2.5% of units sold. The new proposal will reduce this rate to

1%. Assume all units produced are sold and there are no ending inventories.

How much will internal failure costs change if the internal product failures are reduced

by 40% with the new procedures?

A) $138,000 decrease

B) $126,000 decrease

C) $120,000 decrease

D) $84,000 increase

18) Purchasing at the EOQ recommended level, how many deliveries will be made

during each time period?

A) 2 deliveries

B) 6.0 deliveries

C) 7.91 deliveries

D) 12 deliveries

19) A manufacturing plant produces two product lines: golf equipment and soccer

equipment. An example of direct costs for the golf equipment line is ________.

A) beverages provided daily in the plant break room

B) monthly lease payments for a specialized piece of equipment needed to manufacture

the golf driver

C) salaries of the clerical staff that work in the company administrative offices

D) overheads incurred in producing both golf and soccer equipment

20) Which of the following can be a reason for a favorable price variance for direct

materials?

A) a decrease in the price of materials due to an oversupply of materials

B) an unexpected increase in the price of materials

C) less amount of material used during production than planned for actual output

D) workers taking less time to produce the products

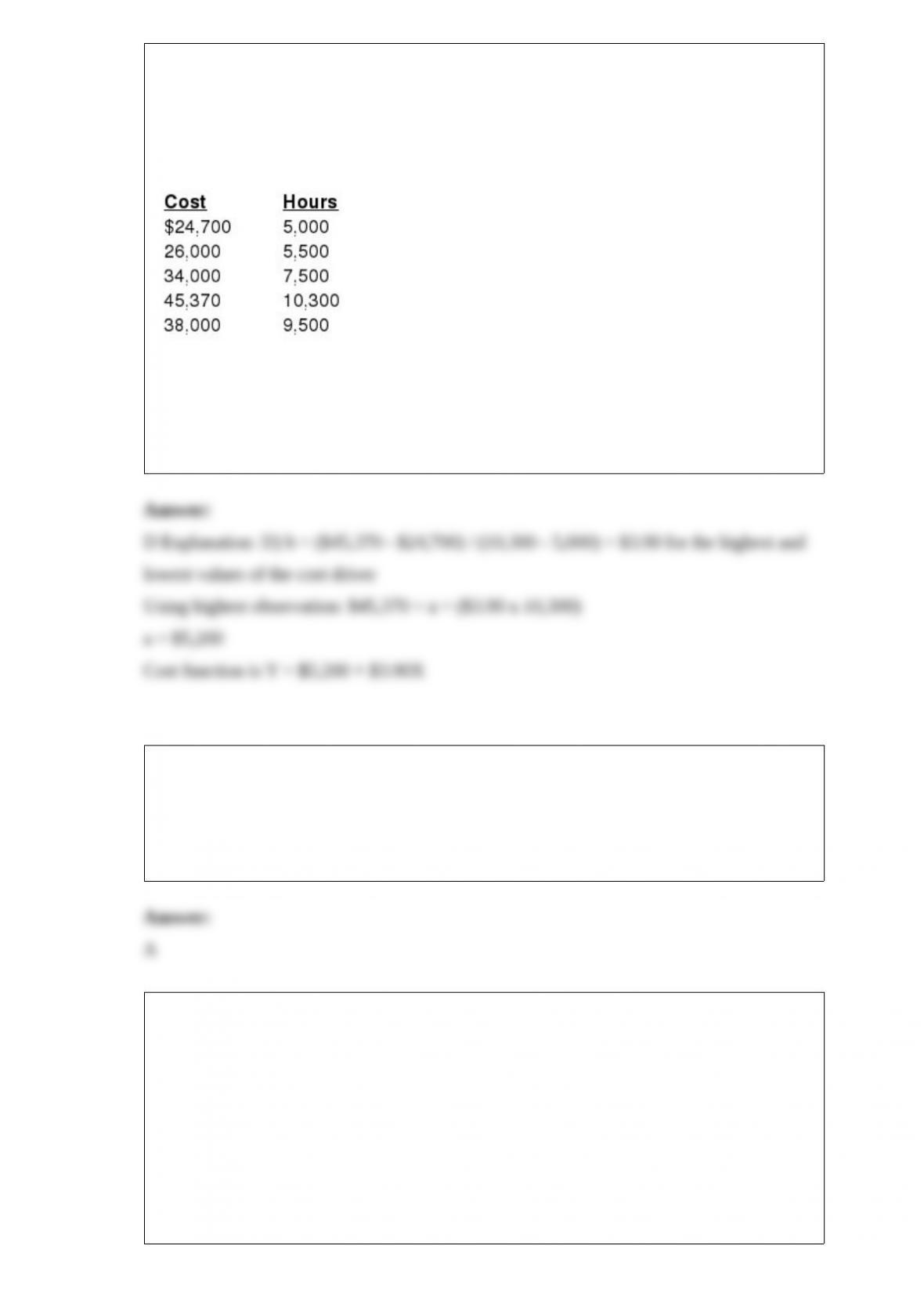

21) The Frontive Company has assembled the following data pertaining to certain costs

that cannot be easily identified as either fixed or variable. Frontive Company has heard

about a method of measuring cost functions called the high-low method and has

decided to use it in this situation.

What is the cost function?

A) y = $45,370 + $4.19X

B) y = $24,700 + $4.40X

C) y = $34,000 + $4.94X

D) y = $5,200 + $3.90X

22) Merchandising-sectors ________.

A) purchase and then sell tangible products without changing their basic form

B) provide intangible products

C) purchase materials and components and convert them into finished goods

D) purchase and then sell tangible products by changing their basic form

23) Speedy Dress Manufacturing has two workstations, cutting and finishing. The

cutting station is limited by the speed of operating the cutting machine. Finishing is

limited by the speed of the workers. Finishing normally waits for work from cutting.

Each department works an eight-hour day. If cutting begins work two hours earlier than

finishing each day, the two departments generally finish their work at about the same

time. Not only does this eliminate the bottleneck, but also it increases finished units

produced each day by 160 units. All units produced can be sold even though the change

increases inventory stock by 20% from 400 units. The cost of operating the cutting

department two more hours each day is $1,600. The contribution margin of the finished

products is $6 each. Inventory carrying costs are $0.40 per unit per day.

What is the change in the daily contribution margin if the change is made?

A) $(608)

B) $(634)

C) $(672)

D) $800

24) Which of the following reduces manufacturing cycle times and delays?

A) increasing the capacity of a bottleneck resource

B) selling of an existing equipment to save up on depreciation costs

C) increasing the time it takes for setups and processing

D) outsourcing the job to a third party

25) Managing inventories to increase net income requires companies to effectively

manage costs associated with goods for sale.

Required:

Classify the below listed items as either Purchasing Costs, Ordering Costs, Carrying

Costs, Stockout Costs, Costs of Quality, or Shrinkage Costs.

________a.costs of obtaining purchase approvals

________b.costs resulting from embezzlement by employees

________c.internal failure costs

________d.opportunity cost of the investment tied up in inventory

________e.costs associated with storage

________f.costs of lost sales as a result of not having an item requested by a customer

________g.freight-in charges

________h.special processing costs

________i.costs of wages for work-in-process inspections

________j.costs that result from misclassifications and clerical errors

26) Costs in the cost pool having the same or a similar cause-and-effect or

benefits-receiving relationship

with the cost-allocation base can be achieved in adopting ________.

A) indirect cost pools

B) homogeneous cost pools

C) hetrogeneous cost pools

D) direct cost pools

27) Which of the following statements is true of the methods for allocating joint costs?

A) The net realizable value method uses the sales value of the units sold during the

accounting period to allocate joint costs.

B) The sales value at splitoff method always results in the same gross-margin

percentage for all products.

C) The sales value at splitoff method allocates joint costs to each product in proportion

to the sales value of total production.

D) The net realizable value method results in the same joint production cost per unit for

all products.

28) Which of the following forms a part of decision making in CVP analysis?

A) selection of inventory method for financial reporting purposes

B) decision to form a capital policy

C) decision to advertise

D) decision to improve the efficiency of the work force

29) Which of the following statements is true of costs associated with goods for sale?

A) Information-gathering technology increases the reliability and timeliness of

inventory information and increases the costs related to inventory.

B) Opportunity costs are not recorded in financial accounting systems because they are

not a significant component in several cost categories.

C) The costs of receiving and inspecting the items are included in the purchase orders

are ordering costs.

D) Opportunity costs are recorded in financial accounting systems but are a not

significant component in several cost categories.

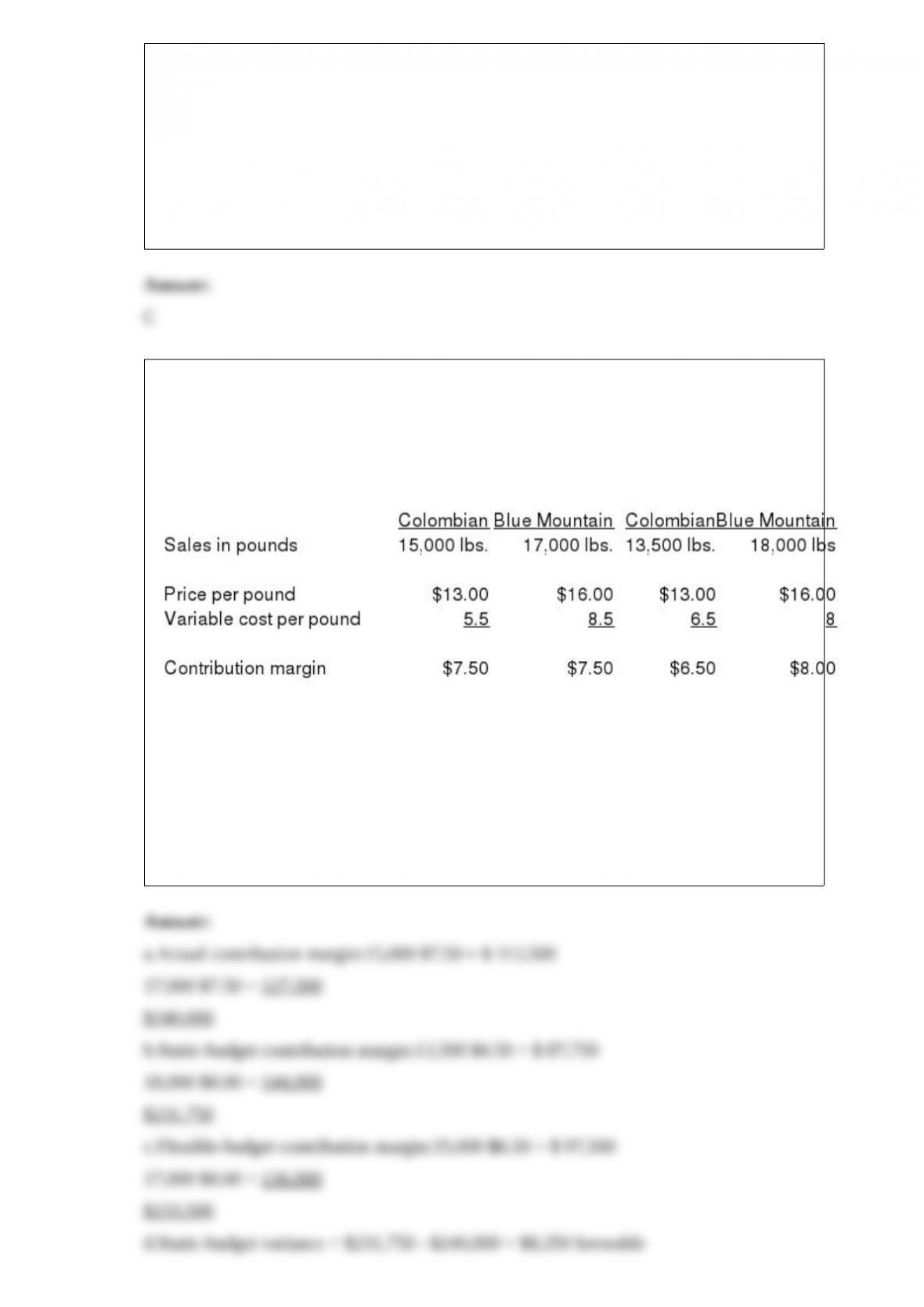

30) Synor Coffee, Inc., sells two types of coffee, Colombian and Blue Mountain. The

monthly budget for U.S. coffee sales is based on a combination of last year’s

performance, a forecast of industry sales, and the company’s expected share of the U.S.

market. The following information is provided for March:

ActualBudget

Budgeted and actual fixed corporate-sustaining costs are $60,000 and $72,000,

respectively.

Required:

a.Calculate the actual contribution margin for the month.

b.Calculate the contribution margin for the static budget.

c.Calculate the contribution margin for the flexible budget.

d.Determine the total static-budget variance, the total flexible-budget variance, and the

total sales-volume variance in terms of the contribution margin.