Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

6-1

SOLUTION

1.

Revenue Budget

For the Month of April

Units

Selling Price

Total Revenues

Cat-allac

530

$205

$108,650

Dog-eriffic

225

310

69,750

Total

$178,400

2.

Production Budget

For the Month of April

Product

Cat-allac

Dog-eriffic

Budgeted unit sales

530

225

Add target ending finished goods inventory

30

10

Total required units

560

235

Deduct beginning finished goods inventory

10

25

Units of finished goods to be produced

550

210

3.

Direct Material Usage Budget in Quantity and Dollars

For the Month of April

Material

Plastic

Metal

Total

Physical Units Budget

Direct materials required for

Cat-allac (550 units × 4 lbs. and 0.5 lb.)

2,200 lbs.

275 lbs.

Dog-eriffic (210 units × 6 lbs. and 1 lb.)

1,260 lbs.

210 lbs.

Total quantity of direct material to be used

3,460 lbs.

485 lbs.

Cost Budget

Available from beginning direct materials inventory

(under a FIFO cost-flow assumption)

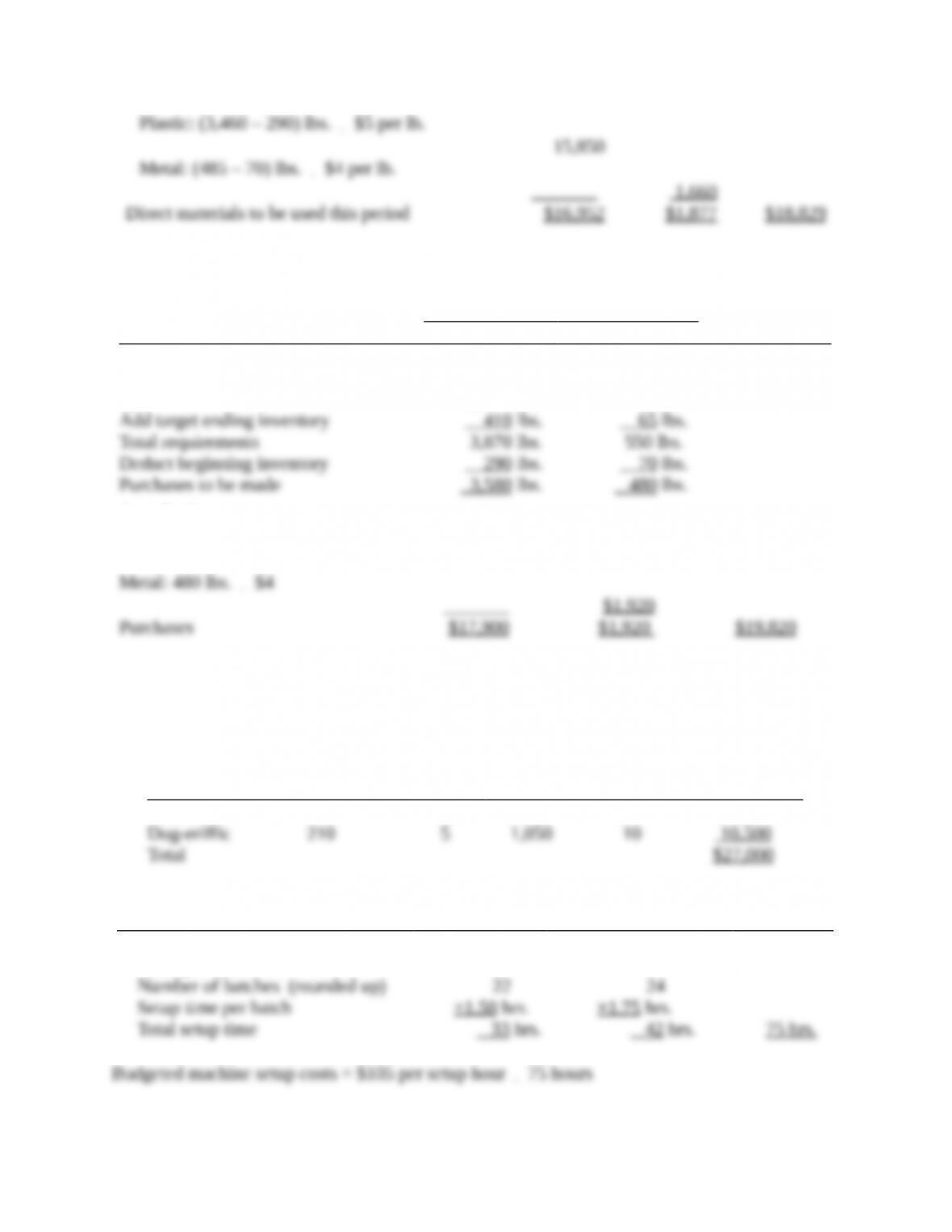

Plastic: 290 lbs. × $3.80 per lb.

$ 1,102

Metal: 70 lbs. × $3.10 per lb.

$ 217

To be purchased this period

Plastic: (3,460 – 290) lbs.

$5 per lb.

15,850

Metal: (485 – 70) lbs.

$4 per lb.

_______

1,660

Direct materials to be used this period

$16,952

$1,877

$18,829

6-2

Direct Material Purchases Budget

For the Month of April

Material

Plastic

Metal

Total

Physical Units Budget

To be used in production (requirement 3)

3,460 lbs.

485 lbs.

Add target ending inventory

410 lbs.

65 lbs.

Total requirements

3,870 lbs.

550 lbs.

Deduct beginning inventory

290 lbs.

70 lbs.

Purchases to be made

3,580 lbs.

480 lbs.

Cost Budget

Plastic: 3,580 lbs.

$5

$17,900

Metal: 480 lbs.

$4

_______

$1,920

Purchases

$17,900

$1,920

$19,820

4.

Direct Manufacturing Labor Costs Budget

For the Month of April

Output Units

Produced

DMLH

Total

Hourly Wage

(requirement 2)

per Unit

Hours

Rate

Total

Cat-allac

550

3

1,650

$10

$16,500

Dog-eriffic

210

5

1,050

10

10,500

Total

$27,000

5. Machine Setup Overhead

Cat-allac

Dog-eriffic

Total

Units to be produced

550

210

Units per batch

÷ 25

÷9

Number of batches (rounded up)

22

24

Setup time per batch

×1.50 hrs.

×1.75 hrs.

Total setup time

33 hrs.

42 hrs.

75 hrs.

Budgeted machine setup costs = $105 per setup hour

75 hours

= $7,875

Processing Overhead

Budgeted machine-hours (MH) = (11 MH per unit × 550 units) + (19 MH per unit × 210 units)

= 6,050 MH + 3,990 MH = 10,040 MH

Budgeted processing costs = $10 per MH × 10,040 MH

= $100,400

Inspection Overhead

Budgeted inspection-hours = (0.5

22 batches) + (0.7

24 batches)

= 11 + 16.8 = 27.8 inspection hrs.

Budgeted inspection costs = $15 per inspection hr.

27.8 inspection hours

= $417

Manufacturing Overhead Budget

For the Month of April

Machine setup costs

$ 7,875

Processing costs

100,400

Inspection costs

417

Total costs

$108,692

6.

Unit Costs of Ending Finished Goods Inventory

April 30

Product

Cat-allac

Dog-eriffic

Cost per

Input per

Input per

Unit of

Input

Unit of

Output

Total

Unit of

Output

Total

Plastic

$ 5

4 lbs.

$ 20.00

6 lbs.

$ 30.00

Metal

4

0.5 lbs.

2.00

1 lb.

4.00

Direct manufacturing labor

10

3 hrs.

30.00

5 hrs.

50.00

Machine setup

105

0.06 hrs.1

6.30

0.2 hr1

21.00

Processing

10

11 MH

110.00

19 MH

190.00

Inspection

15

0.02 hr2

0.30

0.08 hr.2

1.20

Total

$168.60

$296.20

1 33 setup-hours ÷ 550 units = 0.06 hours per unit; 42 setup-hours ÷ 210 units = 0.2 hours per unit

2 11 inspection hours ÷ 550 units = 0.02 hours per unit; 16.8 inspection hours ÷ 210 units = 0.08 hours per unit

Ending Inventories Budget

April 30

Quantity

Cost per unit

Total

Direct Materials

Plastic

410

$ 5

$2,050

Metals

65

4

260

$ 2,310

Finished goods

Cat-allac

30

$168.60

$5,058

Dog-eriffic

10

296.20

2,962

8,020

Total ending inventory

$10,330

7.

Cost of Goods Sold Budget

For the Month of April

Beginning finished goods inventory, April, 1 ($1,000 + $4,650)

$ 5,650

Direct materials used (requirement 3)

$18,829

Direct manufacturing labor (requirement 4)

27,000

6-4

Manufacturing overhead (requirement 5)

108,692

Cost of goods manufactured

154,521

Cost of goods available for sale

160,171

Deduct: Ending finished goods inventory, April 30 (requirement 6)

8,020

Cost of goods sold

$152,151

8.

Nonmanufacturing Costs Budget

For the Month of April

Salaries ($32,000 ÷ 2

1.05)

$16,800

Other fixed costs ($32,000 ÷ 2)

16,000

Sales commissions ($178,400

1%)

1,784

Total nonmanufacturing costs

$34,584

9.

Budgeted Income Statement

For the Month of April

Revenues

$178,400

Cost of goods sold

152,151

Gross margin

26,249

Operating (nonmanufacturing) costs

34,584

Operating income

$ (8,335)

10. Preparing a budget helps Animal Gear manage costs based on revenues and production

needs, look for opportunities to increase efficiencies, reduce costs, particularly in areas where costs

are high, coordinate and communicate across different parts of the organization, create a framework

for judging performance and facilitating learning, and motivate management and employees to

achieve “stretch” targets of higher revenues and lower costs.

6-36 (25 min.) Cash budget (Continuation of 6-35) (Appendix)

Refer to the information in Problem 6-35.

Assume the following: Animal Gear (AG) does not make any sales on credit. AG sells only to

the public and accepts cash and credit cards; 90% of its sales are to customers using credit cards,

for which AG gets the cash right away, less a 2% transaction fee.

Purchases of materials are on account. AG pays for half the purchases in the period of the

purchase and the other half in the following period. At the end of March, AG owes suppliers

$8,000.

AG plans to replace a machine in April at a net cash cost of $13,000.

Labor, other manufacturing costs, and nonmanufacturing costs are paid in cash in the month

incurred except of course depreciation, which is not a cash flow. Depreciation is $25,000 of the

manufacturing cost and $10,000 of the nonmanufacturing cost for April.

6-5

AG currently has a $2,000 loan at an annual interest rate of 24%. The interest is paid at the end

of each month. If AG has more than $10,000 cash at the end of April it will pay back the loan. AG

owes $5,000 in income taxes that need to be remitted in April. AG has cash of $5,900 on hand at

the end of March.

Required:

1. Prepare a cash budget for April for Animal Gear.

2. Why do Animal Gear’s managers prepare a cash budget in addition to the revenue, expenses,

and operating income budget?

SOLUTION

Cash Budget

April 30

Cash balance, April 1

$ 5,900

Add receipts

Cash sales ($178,400 × 10%)

17,840

Credit card sales ($178,400 × 90% × 98%)

157,349

Total cash available for needs (x)

$181,089

Deduct cash disbursements

Direct materials ($8,000 + $19,820 × 50%)

$ 17,910

Direct manufacturing labor

27,000

Manufacturing overhead ($108,692 ─ $25,000 depreciation)

83,692

Nonmanufacturing salaries

16,800

Sales commissions

1,784

Other nonmanufacturing fixed costs ($16,000 ─ $10,000 depreciation)

6,000

Machinery purchase

13,000

Income taxes

5,000

Total disbursements (y)

$171,186

Financing

Repayment of loan

$ 2,000

Interest at 24% ($2,000

24%

1

12

)

40

Total effects of financing (z)

$ 2,040

Ending cash balance, April 30 (x) ─ (y) ─ (z)

$ 7,863

Note: The solution assumes that the loan is repaid. Some students may point out that the cash

balance at the end of April is anticipated to be slightly less than $10,000 [$9,903 ($181,089 –

$171,186)], and so Animal Gear would not repay the loan. Under this assumption, the $2,000

repayment would not be shown.

2. Animal Gear’s managers prepare a cash budget in addition to the operating income budget

to plan cash flows to ensure that the company has adequate cash to pay vendors, meet payroll, and

pay operating expenses as these payments come due. Animal Gear could be very profitable on an

accrual accounting basis, but the pattern of cash receipts from revenues might be delayed and result

6-6

in insufficient cash being available to make scheduled payments for its expenses. Animal Gear’s

managers may then need to initiate a plan to borrow money to finance any shortfall. Building a

profitable operating plan does not guarantee that adequate cash will be available, so Animal Gear’s

managers need to prepare a cash budget in addition to an operating income budget.

6-37 (60 min.) Comprehensive operating budget, budgeted balance sheet.

Skulas, Inc., manufactures and sells snowboards. Skulas manufactures a single model, the Pipex.

In the summer of 2014, Skulas’ management accountant gathered the following data to prepare

budgets for 2015:

Skulas’ CEO expects to sell 2,900 snowboards during 2015 at an estimated retail price of $650 per

board. Further, the CEO expects 2015 beginning inventory of 500 snowboards and would like to

end 2015 with 200 snowboards in stock.

Variable manufacturing overhead is $7 per direct manufacturing labor-hour. There are also

$81,000 in fixed manufacturing overhead costs budgeted for 2015. Skulas combines both variable

and fixed manufacturing overhead into a single rate based on direct manufacturing labor-hours.

Variable marketing costs are allocated at the rate of $250 per sales visit. The marketing plan calls

for 38 sales visits during 2015. Finally, there are $35,000 in fixed nonmanufacturing costs

budgeted for 2015.

Other data include:

6-7

The inventoriable unit cost for ending finished goods inventory on December 31, 2014, is $374.80.

Assume Skulas uses a FIFO inventory method for both direct materials and finished goods. Ignore

work in process in your calculations.

Budgeted balances at December 31, 2014, in the selected accounts are as follows:

Required:

1. Prepare the 2015 revenues budget (in dollars).

2. Prepare the 2015 production budget (in units).

3. Prepare the direct material usage and purchases budgets for 2015.

4. Prepare a direct manufacturing labor budget for 2015.

5. Prepare a manufacturing overhead budget for 2015.

6. What is the budgeted manufacturing overhead rate for 2015?

7. What is the budgeted manufacturing overhead cost per output unit in 2015?

8. Calculate the cost of a snowboard manufactured in 2015.

9. Prepare an ending inventory budget for both direct materials and finished goods for 2015.

10. Prepare a cost of goods sold budget for 2015.

11. Prepare the budgeted income statement for Skulas, Inc., for the year ending December 31,

2015.

12. Prepare the budgeted balance sheet for Skulas, Inc., as of December 31, 2015.

13. What questions might the CEO ask the management team when reviewing the budget? Should

the CEO set stretch targets? Explain briefly.

14. How does preparing the budget help Skulas’ management team better manage the company?

SOLUTION

6-8

Note: There is a typo on page 241. The In some print version of the book, the budgeted

balances in the problem balance sheet items that appear just before the requirements are as

shown as balances for December 31, 2014. These balances are for December 31, 2015, and

not for December 31, 2014.

1. Schedule 1: Revenues Budget for the Year Ended December 31, 2015

Units Selling Price Total Revenues

Snowboards 2,900 $650 $1,885,000

2. Schedule 2: Production Budget (in Units) for the Year Ended December 31, 2015

Snowboards

Budgeted unit sales (Schedule 1) 2,900

Add target ending finished goods inventory 200

Total requirements 3,100

Deduct beginning finished goods inventory 500

Units to be produced 2,600

3. Schedule 3A: Direct Materials Usage Budget for the Year Ended December 31, 2015

Wood Fiberglass Total

Physical Units Budget

Wood: 2,600 × 9.00 b.f. 23,400

Fiberglass: 2,600 × 10.00 yards _______ 26,000

To be used in production 23,400 26,000

Cost Budget

Available from beginning inventory

Wood: 2,040 b.f. × $32.00 $ 65,280

Fiberglass: 1,040 b.f. × $8.00 $ 8,320

To be used from purchases this period

Wood: (23,400 – 2,040) × $34.00 726,240

Fiberglass: (26,000 – 1,040) × $9.00 ________ 224,640

Total cost of direct materials to be used $791,520 $232,960 $1,024,480

Schedule 3B: Direct Materials Purchases Budget for the Year Ended December 31, 2015

Wood Fiberglass Total

Physical Units Budget

Production usage (from Schedule 3A) 23,400 26,000

Add target ending inventory 1,540 2,040

Total requirements 24,940 28,040

Deduct beginning inventory 2,040 1,040

Purchases 22,900 27,000

Cost Budget

Wood: 22,900 × $34.00 $778,600

Fiberglass: 27,000 × $9.00 ________ $243,000

Purchases $778,600 $243,000 $1,021,600

4. Schedule 4: Direct Manufacturing Labor Budget for the Year Ended December 31, 2012

6-9

Labor Category

Cost Driver

Units

DML Hours per

Driver Unit

Total

Hours

Wage

Rate

Total

Manufacturing labor

2,600

5.00

13,000

$29.00

$377,000

5. Schedule 5: Manufacturing Overhead Budget for the Year Ended December 31, 2015

At Budgeted Level of 13,000

Direct Manufacturing Labor-Hours

Variable manufacturing overhead costs

($7.00 × 13,000) $ 91,000

Fixed manufacturing overhead costs 81,000

Total manufacturing overhead costs $172,000

6. Budgeted manufacturing overhead rate:

$172,000

13,000

= $13.23 per hour

7. Budgeted manufacturing overhead cost per output unit:

$172,000

2,600

= $66 per output unit

8. Schedule 6A: Computation of Unit Costs of Manufacturing Finished Goods in 2015

Cost per

Unit of

Inputa Inputsb Total

Direct materials

Wood $34.00 9.00 $306.00

Fiberglass 9.00 10.00 90.00

Direct manufacturing labor 29.00 5.00 145.00

Total manufacturing overhead 66.00

$607.00

aCost is per board foot, yard, or per hour

bInputs is the amount of each input per board

9. Schedule 6B: Ending Inventories Budget, December 31, 2015

Cost per

Units Unit Total

Direct materials

Wood 1,540 $ 34.00 $ 52,360

Fiberglass 2,040 9.00 18,360

Finished goods

Snowboards 200 607.00 121,400

Total Ending Inventory $192,120

10. Schedule 7: Cost of Goods Sold Budget for the Year Ended December 31, 2015

From

Schedule Total

Beginning finished goods inventory

January 1, 2015, $374.80 × 500 Given $ 187,400

Direct materials used 3A $1,024,480

6-10

Direct manufacturing labor 4 377,000

Manufacturing overhead 5 172,000

Cost of goods manufactured 1,573,480

Cost of goods available for sale 1,760,880

Deduct ending finished goods

inventory, December 31, 2015 6B 121,400

Cost of goods sold $1,639,480

11. Budgeted Income Statement for Skulas for the Year Ended December 31, 2015

Revenues Schedule 1 $1,885,000

Cost of goods sold Schedule 7 1,639,480

Gross margin 245,520

Operating costs

Variable marketing costs ($250 × 38) $ 9,500

Fixed nonmanufacturing costs 35,000 44,500

Operating income $ 201,020

12. Budgeted Balance Sheet for Skulas as of December 31, 2015

Cash $ 14,000

Inventory Schedule 6B 192,120

Property, plant, and equipment (net) 854,000

Total assets $1,060,120

Current liabilities $ 21,000

Long-term liabilities 182,000

Stockholders’ equity 857,120

Total liabilities and stockholders’ equity $1,060,120

13. The CEO would want to probe if the revenue budget is sufficiently stretched. Is the

increase growing faster than the market? Should the company increase marketing and advertising

spending to grow sales? Would increasing the sales force or giving salespersons stronger

incentives result in higher sales?

The CEO would want to ask the production manager if production could be more closely

tailored to demand? Could the efficiency and productivity of direct materials and direct

manufacturing labor be increased? Could direct materials inventory be reduced?

The CEO should set stretch targets that are challenging but achievable because creating

some performance anxiety motivates employees to exert extra effort and attain better

performance. A major rationale for stretch targets is the psychological motivation that comes

from loss aversion—people feel the pain of loss more than the joy of success. Setting challenging

targets motivates employees to reach these targets because failing to achieve a target is seen as

failing. At no point should the pressure for performance push employees to engage in illegal or

unethical practices. So, while setting stretch targets, the CEO must place great emphasis on

adhering to codes of conduct and following appropriate norms and values. The CEO should also

not set targets that are very difficult or impossible to achieve. Such targets demotivate employees

because they give up on trying to achieve them.

6-11

14. Preparing a budget helps Skulas manage costs based on revenues and production needs, look

for opportunities to increase efficiencies, reduce costs, particularly in areas where costs are high,

coordinate and communicate across different parts of the organization, create a framework for

judging performance and facilitating learning, and motivate management and employees to achieve

“stretch” targets of higher revenues and lower costs.