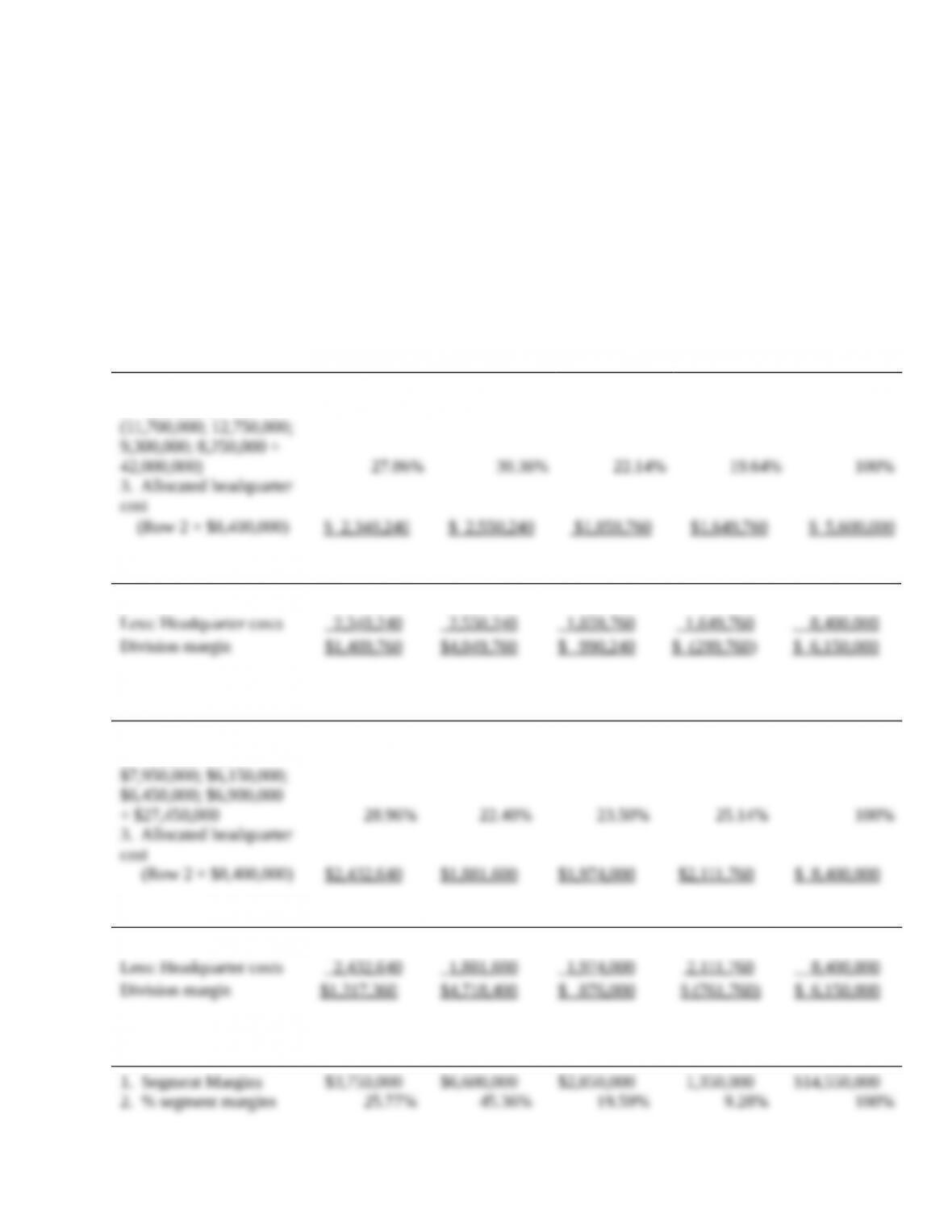

2. % segment margins

$3,750,000; $6,600,000;

$2,850,000; $1,350,000

÷ $14,550,000

25.77%

45.36%

19.59%

9.28%

100%

3. Allocated headquarter

cost

(Row 2 × $8,400,000)

$2,164,680

$3,810,240

$1,645,560

$779,520

$8,400,000

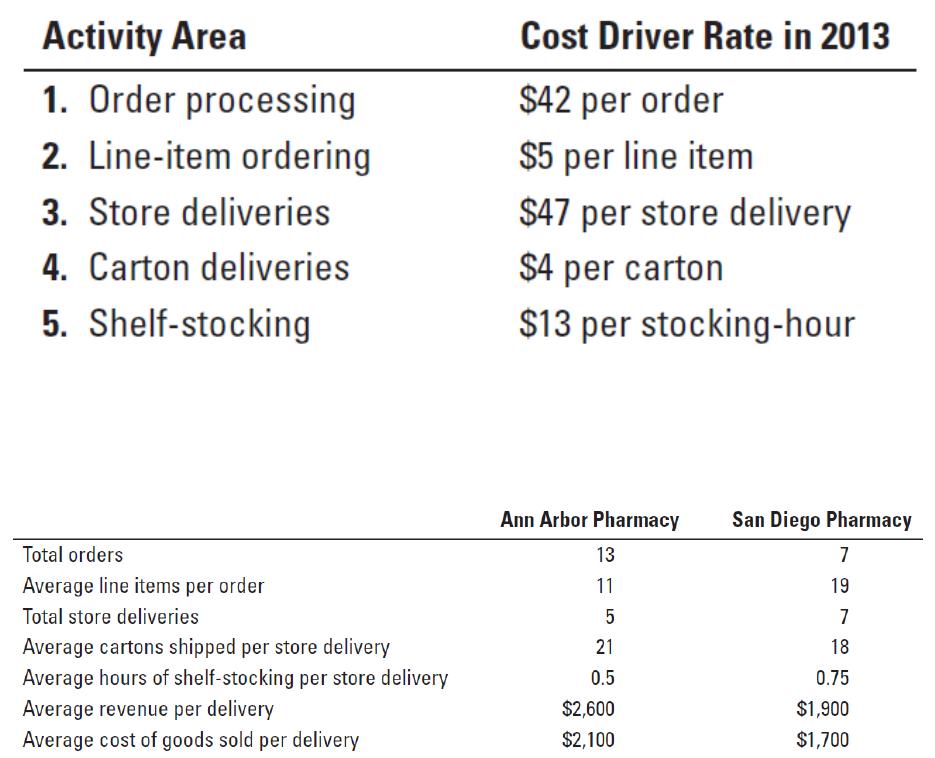

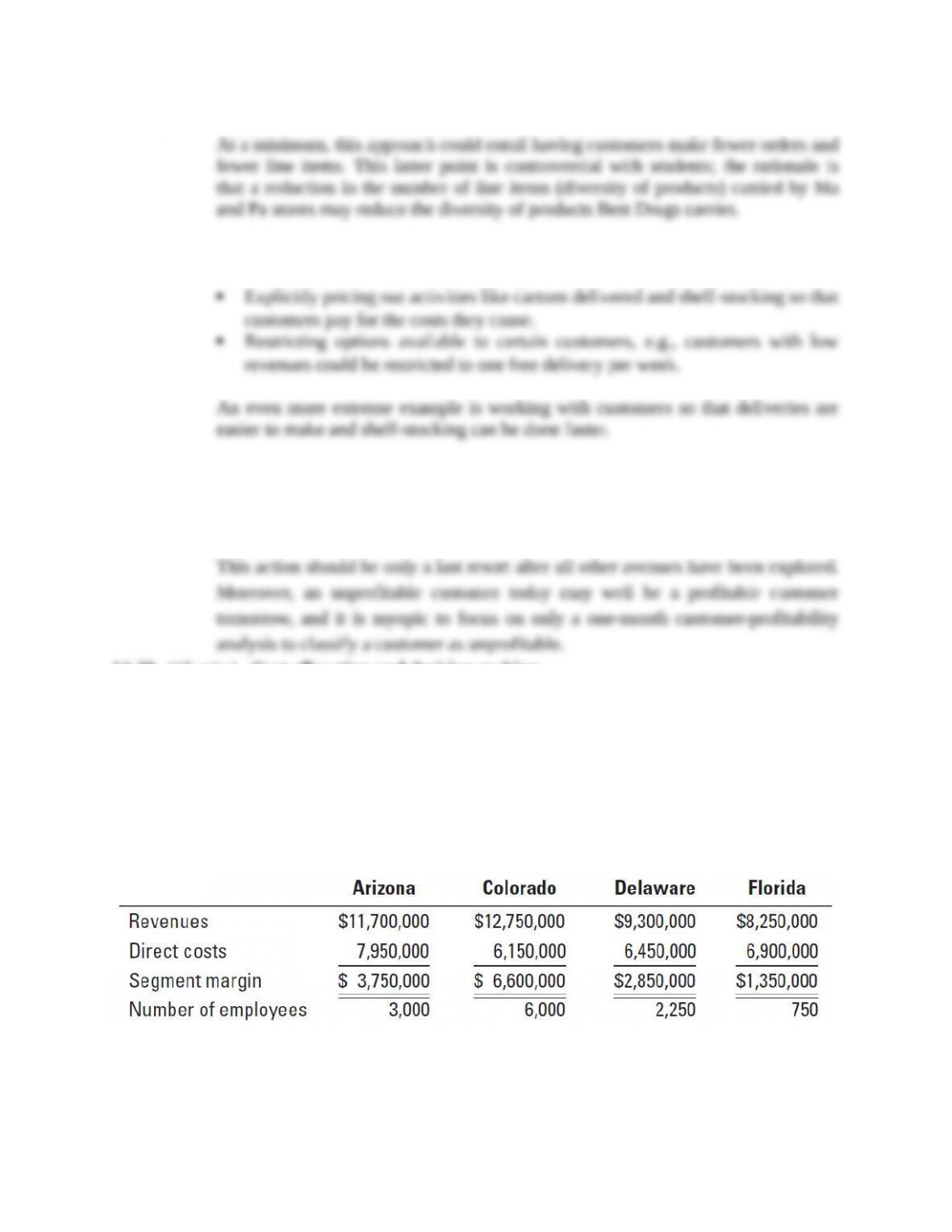

Arizona

Colorado

Delaware

Florida

Total

Segment margin

$3,750,000

$6,600,000

$2,850,000

$1,350,000

$14,550,000

Less: Headquarter costs

2,164,680

3,810,240

1,645,560

779,520

8,400,000

Division margin

$1,585,320

$2,789,760

$1,204,440

$ 570,480

$ 6,150,000

Allocations based on number of employees.

Arizona

Colorado

Delaware

Florida

Total

1. Number of Employees

3,000

6,000

2,250

750

12,000

2. % Number of employees

3,000; 6,000; 2,250; 750

÷ 12,000

25%

50%

18.75%

6.25%

100%

3. Allocated headquarter cost

(Row 2 × $8,400,000)

$2,100,000

$4,200,000

$1,575,000

$525,000

$8,400,000

Arizona

Colorado

Delaware

Florida

Total

Segment margin

$3,750,000

$6,600,000

$2,850,000

$1,350,000

$14,550,000

Less: Headquarter costs

2,100,000

4,200,000

1,575,000

525,000

8,400,000

Division margin

$1,650,000

$2,400,000

$1,275,000

$ 825,000

$ 6,150,000

2. The Florida Division manager will prefer to use the number of employees as the allocation

base because it results in the highest operating margin for the division.

3. The Arizona Division and the Delaware Division receive roughly the same percentage

allocation of headquarter costs regardless of the allocation base used (Arizona range =

25%–29%; Delaware range = 18.75%–23.5%). However, the Colorado Division and the

Florida Division vary widely (Colorado range = 22.4%–50%; Florida range = 6.25%–

25.1%). All four methods are reasonable options, but none clearly meets the cause-and–

effect criterion for selecting the allocation base. If larger divisions tend to consume more

of headquarters’ resources, then using division revenues or number of employees seem to

be the best choices. Without compelling reason to change, Greenbold should stay with the

division revenues as the allocation base.

Another alternative is to use segment margin as the allocation base on the grounds that

this best captures the ability of different divisions to bear corporate overhead costs.