Department

Cost

Driver

Sanders

Hanley

Stanley

Design

Engineering

Construction

Design-hours

Engineering-hours

Labor-hours

10%

32

33

50%

32

35

40%

36

32

The Sanders project uses only 10% of design-hours in 2014 and uses 32% of engineering–

hours and 33% of construction hours. The result is that the overhead rate, based on allocating costs

equally to all projects (33%), will greatly overestimate the cost of resources used on the Sanders

project, which uses very few design-hours. This explains the 26% decrease in indirect costs

assigned to the Sanders project when department rates are used.

In contrast, the Hanley and Stanley projects use more of design (50% and 40%,

respectively). Hence, the use of department rates will report higher indirect costs for Hanley and

Stanley than does a single overhead rate.

Sanders was probably complaining about the costs resulting from using the simple system

because its project was being overcosted relative to its consumption of overhead resources. Hanley

and Stanley, on the other hand, were having their projects undercosted and underpriced by the

simple system. If the new department-based rates are used to price projects, Hanley and Stanley

will be unhappy. CKM should explain to Hanley and Stanley how the calculations were done and

point out their high use of design resources. CKM should discuss ways of reducing the

consumption of design resources, if possible, and show willingness to partner with them to do so.

CKM could even offer to phase in the new prices.

4. It would not be worthwhile to further refine the cost system into an ABC system if (1) a

single activity accounts for a sizable proportion of the department’s costs or (2) significant costs

are incurred on different activities within a department, but each activity has the same cost driver

or (3) there wasn’t much variation among contracts in the consumption of activities within a

department. If, for example, most activities within the design department were, in fact, driven by

design-hours, then the more refined system would be more costly and no more accurate than the

department-based cost system.

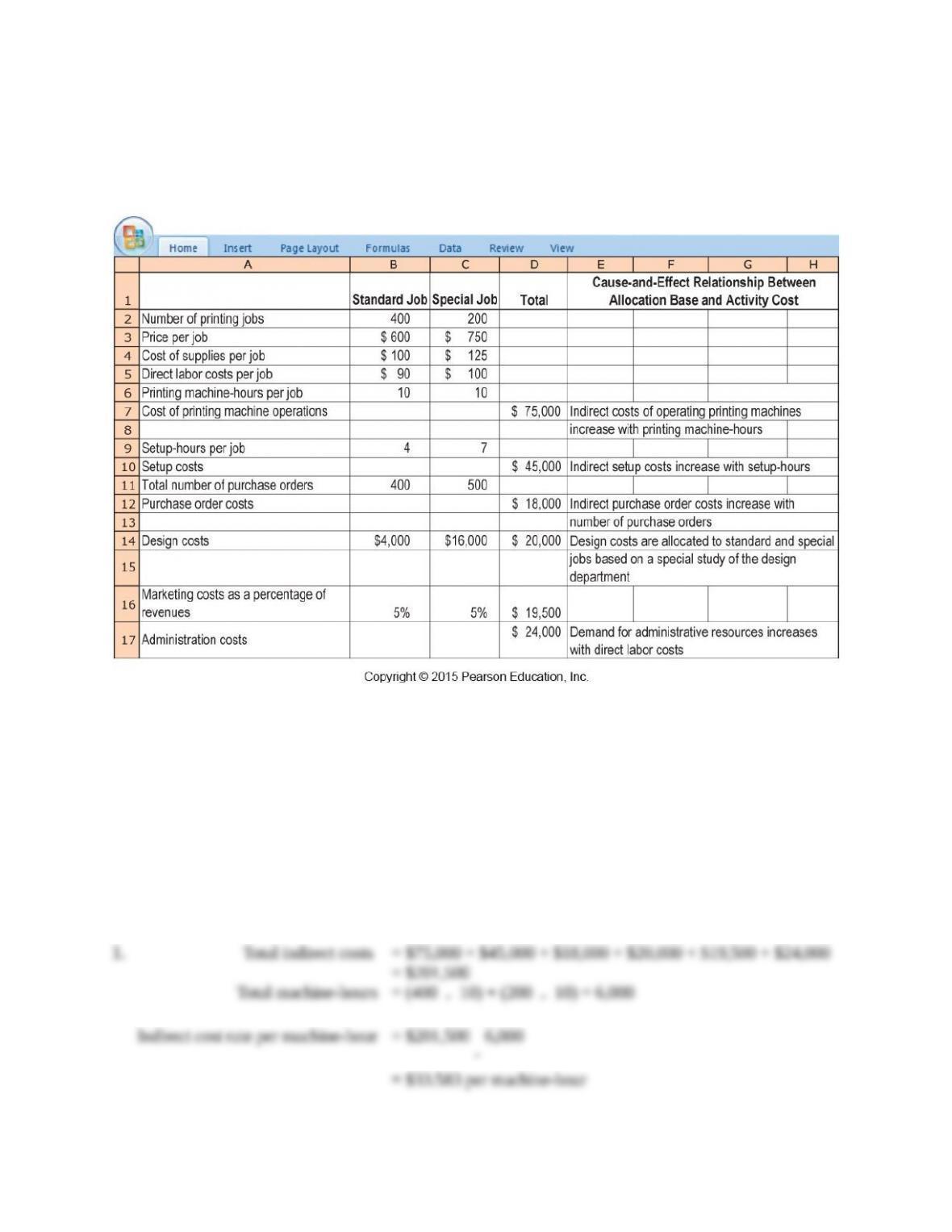

5-23 (30 min.) Activity-based costing, service company.

Speediprint Corporation owns a small printing press that prints leaflets, brochures, and advertising

materials. Speediprint classifies its various printing jobs as standard jobs or special jobs.

Speediprint’s simple job-costing system has two direct-cost categories (direct materials and direct

labor) and a single indirect-cost pool. Speediprint operates at capacity and allocates all indirect

costs using printing machine-hours as the allocation base.

Speediprint is concerned about the accuracy of the costs assigned to standard and special jobs

and therefore is planning to implement an activity-based costing system. Speediprint’s ABC

system would have the same direct–cost categories as its simple costing system. However, instead

of a single indirect-cost pool there would now be six categories for assigning indirect costs: design,

purchasing, setup, printing machine opera– tions, marketing, and administration. To see how

activity-based costing would affect the costs of standard and special jobs, Speediprint collects the

following information for the fiscal year 2014 that just ended.

Activity

(1)

Total Cost of

Activity

(2)

Cost Driver

(3)

Cost Driver

Quantity

(4)

Allocation Rate

(5) = (2) (4)

Product scheduling

$190,000

production runs

125c

$1,520.00

per production run

Material handling

$ 90,000

material moves

240d

$ 375.00

per material move

Machine setup

$ 50,000

machine setups

200e

$ 250.00

per setup

Assembly

$120,000

machine hours

10,000

$ 12.00

per machine hour

Inspection

$ 16,000

inspections

400f

$ 40.00

per inspection

Marketing

Percentage of

revenues

$ 0.03

per dollar of sales

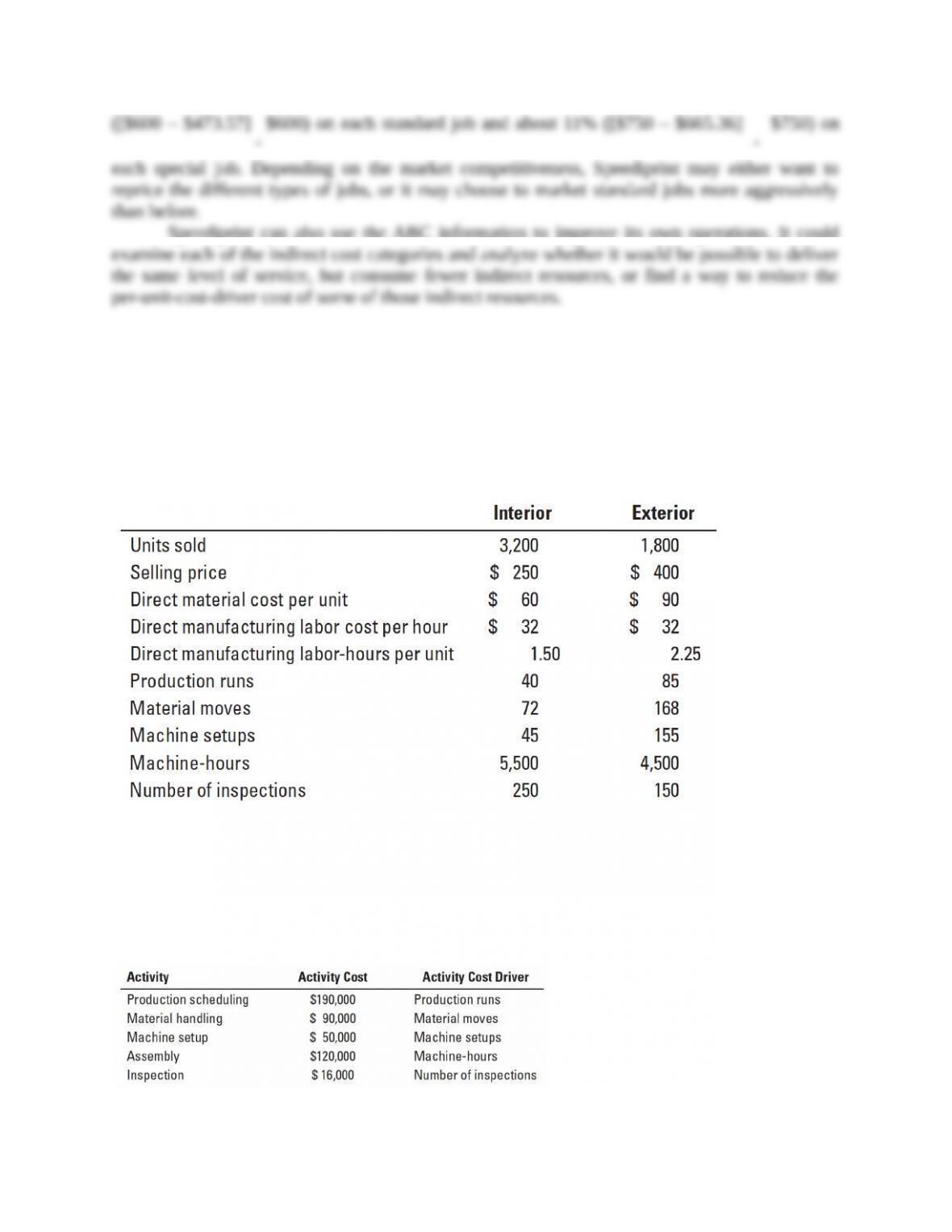

c 40 + 85 = 125; d 72 + 168 = 240; e 45 + 155 = 200; f 250 + 150 = 400

ABC System

Interior

Exterior

Direct materials

$192,000

$162,000

Direct manufacturing labor

153,600

129,600

Indirect costs allocated:

Product scheduling ($1,520 per run

40; 85)

60,800

129,200

Material handling ($375.00 per move

72; 168)

27,000

63,000

Machine setup ($250 per setup

45; 155)

11,250

38,750

Assembly ($12 per MH × 5,500; 4,500)

66,000

54,000

Inspection ($40 per inspection × 250; 150)

10,000

6,000

Marketing (0.03

$250

3,200; 0.03

$400

1,800)

24,000

21,600

Total costs

$544,650

$604,150

Total cost per unit

($544,650 ÷ 3,200 units; $604,150 ÷ 1,800 units)

$ 170.20

$ 335.64

3.

Cost per unit

Interior

Exterior

Simple Costing System

$195.93

$289.90

Activity-based Costing System

$170.20

$335.64

Difference (Simple – ABC)

$ 25.73

$ (45.74)

Relative to the ABC system, the simple costing system overcosts interior doors and undercosts

exterior doors. Interior doors require 1.72 machine-hours per unit while exterior doors require 2.5

machine-hours per unit. In the simple-costing system, overhead costs are allocated to the interior

and exterior doors on the basis of the machine-hours used by each type of door. The ABC study

reveals that the ratio of the cost of production runs, material moves, and setups for each exterior

door versus each interior door is even higher than the ratio of 2.5 to 1.72 machine-hours for each

exterior relative to each interior door. This higher ratio results in higher indirect costs allocated to

exterior doors relative to interior doors in the ABC system.

4. Fancy Doors, Inc. can use the information revealed by the ABC system to change its pricing

based on the ABC costs. Under the simple system, Fancy Doors was making an operating margin

of 21.6% on each interior door ([$250 – $195.93]

$250) and 27.5% on each exterior door ([$400

– $289.90]

$400). But, the ABC system reveals that it is actually making an operating margin

of about 32% ([$250 – $170.20]

$250) on each interior door and about 16% ([$400 – $335.64]

$400) on each exterior door. Fancy Doors, Inc., should consider decreasing the price of its

interior doors to be more competitive. Fancy Doors should also consider increasing the price of

its exterior doors, depending on the competition it faces in this market.

Fancy Doors can also use the ABC information to improve its own operations. It could

examine each of the indirect cost categories and analyze whether it would be possible to deliver

the same level of service, but consume fewer indirect resources, or find a way to reduce the per–

unit-cost-driver cost of some of those indirect resources. Making these operational improvements

can help Fancy Doors to reduce costs, become more competitive, and reduce prices to gain further

market share while increasing its profits.

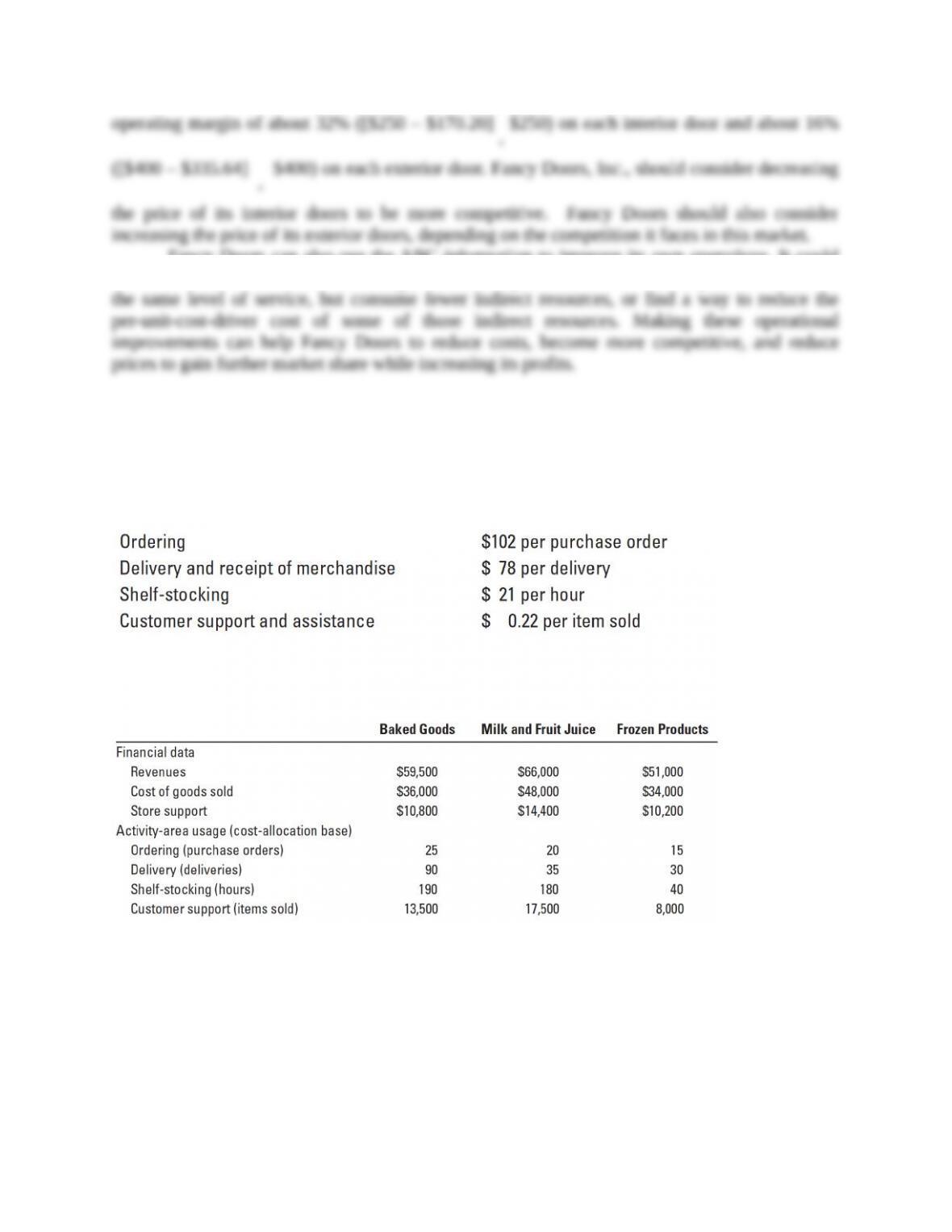

5-25 (30 min.) ABC, retail product-line profitability.

Henderson Supermarkets (HS) operates at capacity and decides to apply ABC analysis to three

product lines: baked goods, milk and fruit juice, and frozen foods. It identifies four activities and

their activity cost rates as follows:

The revenues, cost of goods sold, store support costs, activities that account for the store support

costs, and activity-area usage of the three product lines are as follows:

Under its simple costing system, HS allocated support costs to products at the rate of 30% of cost

of goods sold.

Required:

1. Use the simple costing system to prepare a product-line profitability report for HS.

2. Use the ABC system to prepare a product-line profitability report for HS.

3. What new insights does the ABC system in requirement 2 provide to HS managers?

SOLUTION

1. The simple costing system (Panel A of Solution Exhibit 5-25) reports the following:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

Total

Revenues

Costs

Cost of goods sold

Store support (30% of COGS)

Total costs

Operating income

Operating income ÷ Revenues

$59,500

36,000

10,800

46,800

$12,700

21.34%

$66,000

48,000

14,400

62,400

$ 3,600

5.45%

$51,000

34,000

10,200

44,200

$ 6,800

13.33%

$176,500

118,000

35,400

153,400

$ 23,100

13.09%

2. The ABC system (Panel B of Solution Exhibit 5-25) reports the following:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

Total

Revenues

Costs

Cost of goods sold

Ordering ($102 × 25; 20; 15)

Delivery ($78 × 90; 35; 30)

Shelf-stocking ($21 × 190; 180; 40)

Customer support

($0.22 × 13,500; 17,500; 8,000)

Total costs

Operating income

Operating income ÷ Revenues

$59,500

36,000

2,550

7,020

3,990

2,970

52,530

$ 6,970

11.71%

$66,000

48,000

2,040

2,730

3,780

3,850

60,400

$ 5,600

8.48%

$51,000

34,000

1,530

2,340

840

1,760

40,470

$10,530

20.65%

$176,500

118,000

6,120

12,090

8,610

8,580

153,400

$ 23,100

13.09%

These activity costs are based on the following:

Activity

Cost Allocation Rate

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

Ordering

Delivery

Shelf-stocking

Customer

support

$102 per purchase order

$78 per delivery

$21 per hour

$0.22 per item sold

25

90

190

13,500

20

35

180

17,500

15

30

40

8,000

3. The rankings of products in terms of relative profitability are:

Simple Costing System

ABC System

1. Baked goods 21.33%

2. Frozen products 13.33

3. Milk & fruit juice 5.45

Frozen products 20.65%

Baked goods 11.71

Milk & fruit juice 8.48

The percentage revenue, COGS, and activity costs for each product line are:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

Total

Revenues

COGS

Activity areas:

Ordering

Delivery

Shelf-stocking

Customer support

33.71

30.51

41.67

58.06

46.34

34.62

37.39

40.68

33.33

22.58

43.90

44.87

28.90

28.81

25.00

19.36

9.76

20.51

100.00

100.00

100.00

100.00

100.00

100.00

The baked goods line drops sizably in profitability when ABC is used. Although it constitutes

30.71% of COGS, it uses a higher percentage of total resources in each activity area, especially

the high-cost delivery activity area. In contrast, frozen products draw a much lower percentage of

total resources used in each activity area than its percentage of total COGS. Hence, under ABC,

frozen products are much more profitable.

Henderson Supermarkets may want to explore ways to increase sales of frozen products.

It may also want to explore price increases on baked goods.